STAG Industrial: A Monthly Dividend Industrial REIT with a Disciplined Management Team

STAG Industrial (STAG) is a small but fast-growing industrial REIT that went public in 2011 but has existed since 2003. The company owns about 400 industrial properties which are located in 38 states and leased to over 350 tenants. The vast majority of its single-tenant properties are warehouses, distribution centers, and light manufacturing facilities.

Source: STAG Investor Presentation

STAG focuses on buying warehouses in secondary markets such as Spartanburg, South Carolina; Milwaukee, Wisconsin; and Charlotte, North Carolina. Secondary markets account for 51% of rental revenue.

However, in recent years management has gotten more aggressive in purchasing properties in larger primary markets such as Chicago and Philadelphia. Primary markets account for 42% of rental revenue, with tertiary markets making up the remaining 7%.

No individual market accounts for more than 10% of STAG's total rental revenue, and all but one of the industries it serves represents less than 10% of its rent. No tenant exceeds 2.5% of STAG's total rent either.

Source: STAG Investor Presentation

STAG has raised its annual dividend (which is paid on a monthly basis) each year since going public in 2011.

Business Analysis

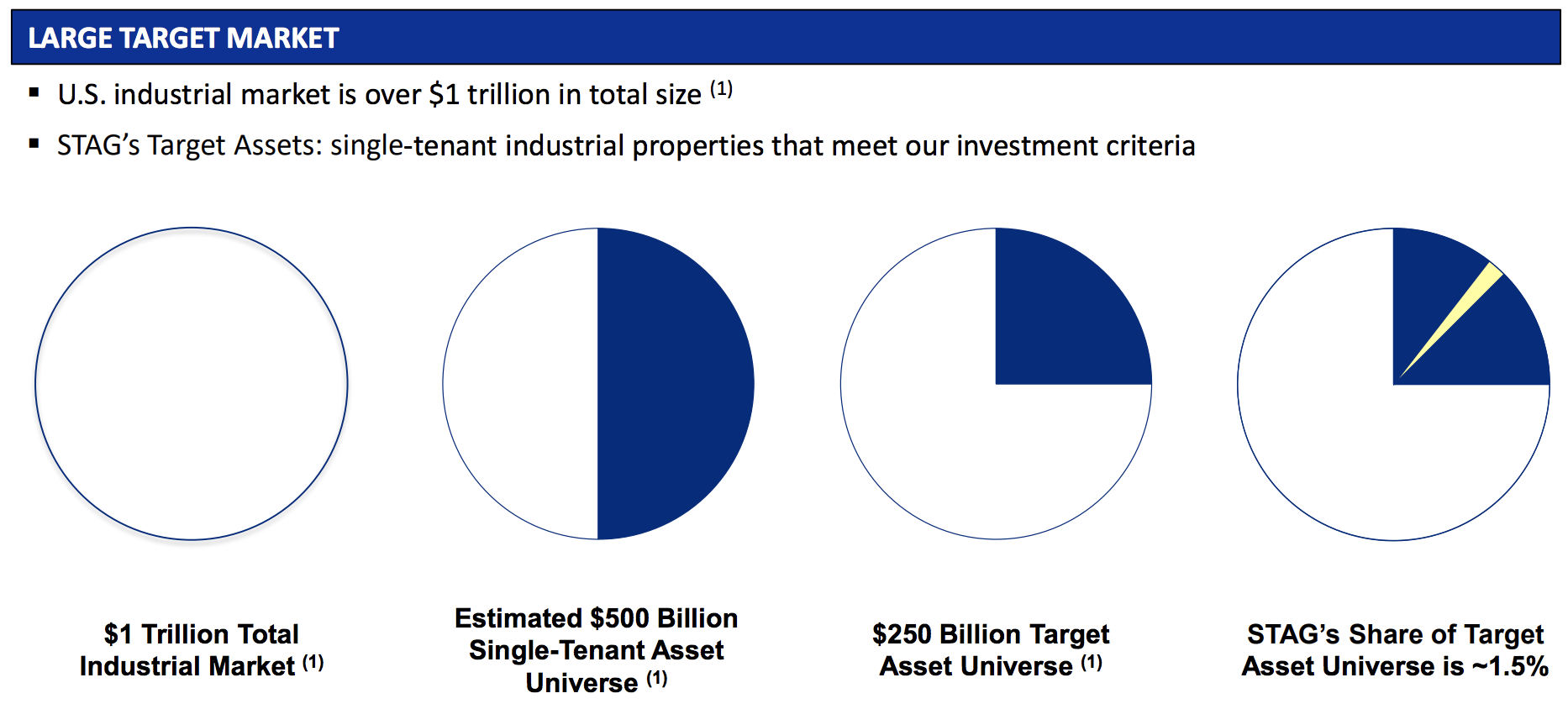

STAG's main appeal is its ability to continue consolidating the vast U.S. industrial real estate market, which is over $1 trillion in total size and highly fragmented. Within this universe, STAG targets a $250 billion slice of single-tenant properties where its market share currently sits at just 1.5%.

Source: STAG Investor Presentation

The industrial real estate market is a large and mature space that's largely tied to the strength of the U.S. economy. While its overall growth profile is modest, the continued rise in online sales is expected to provide a tailwind.

In fact, e-commerce accounts for 10% of U.S. retail sales today, but the U.S. Census Bureau expects that figure to reach 23% by 2025, driving higher demand for warehouses and distribution centers.

Thanks to its relatively small size, STAG expects to capitalize on this trend and the fragmented nature of the industrial real estate market to compound its asset base by more than 20% annually for the foreseeable future.

However, STAG's strategy supporting its ambitious growth plans is rather unique. Unlike REITs with multi-tenant properties, STAG specializes in freestanding or single-tenant buildings, most of which are located in smaller but faster-growing markets.

These industrial real estate assets are usually priced at a discount compared to similar properties located in super primary markets. Many investors believe that assets in larger markets have higher, more stable occupancy and stronger pricing power (higher rents), which makes them worth paying more for.

Based on historical occupancy and rent data, management believes commercial real estate investors have mispriced single-tenant industrial assets in smaller markets due to unjustified concerns over their risk profile, providing an opportunity for STAG to be a savvy acquirer.

After all, in smaller cities there is less available industrial rental space, so tenants often have fewer alternatives to move to. This creates higher switching costs and makes some tenants more willing to remain in place and pay higher rents (or at least demand smaller rental concessions during a recession).

STAG takes its contrarian strategy a step further with the types of tenants it works with. The REIT has its own internal credit team to help it evaluate risk. Once again, STAG believes its skills are superior here, which allows it to do business with tenants that may not be desired by other investors for various reasons.

For example, approximately 25% of STAG's tenants have sub-investment grade credit ratings, and another 45% are not rated at all. Close to 15% of its tenants generate less than $100 million in revenue as well, suggesting they may not have great standalone financial strength.

To reduce risk, STAG focuses on maintaining a well-diversified portfolio with balanced exposure across different properties, tenants, and markets. As previously mentioned, no single city represents more than 10% of STAG's rent, and its top 20 markets account for less than 70% revenue.

Similarly, the REIT's rent is highly diversified by tenant and industry sub-type. The single largest tenant represents 2.2% of rent, and its largest industry exposure is automotive components, which accounts for 12.2% of revenue.

STAG's portfolio diversification seems likely to further improve in the years ahead as management seeks to quickly expand the firm's footprint. To help finance more property acquisitions, STAG has been careful to maintain a reasonable amount of leverage, earning investment grade credit ratings from Moody's and Fitch.

This provides the REIT with access to relatively low-cost debt. Combined with strategic asset dispositions, cash flow retained after paying dividends, and periodic equity issuances, STAG has decent financial firepower to pursue the $250 billion industrial real estate universe it targets.

Overall, STAG Industrial appears to be a well-run, fast-growing industrial REIT. The company pays a generous monthly dividend and appears to have decent long-term growth potential to compound its payout at a mid-single-digit pace.

However, as an industrial REIT with a relatively short track record, investors should note that STAG faces several uncertainties.

Key Risks

Management's strategy of buying "mispriced" industrial assets which potentially possess more durable qualities than other investors realize sounds great in theory. However, STAG's hypothesis that secondary and primary markets will hold up equally well as super primary markets during the next downturn has not yet been tested.

Given the firm's short history as a publicly-traded company, investors don't yet know how the REIT's occupancy, retention rates, or cash flow will perform in future recessions. During the financial crisis, most industrial REITs saw their rent decline by 15% to 25%, and their stocks lost an average of 67% in 2008.

Industrial REITs are cyclical because their tenants' businesses closely track the health of the general economy. It's hard to image STAG bucking this trend, especially given its exposure to volatile industries such as automobiles and capital goods.

While STAG maintains a decent balance sheet, its overall business model still appears somewhat risky. For example, only 30% of its rent comes industrial tenants with investment grade credit ratings, so the firm could face heightened risk that some of its tenants might get into financial trouble during a future recession.

Over 10% of STAG's leases expire each year from 2020 through 2023 as well, and its average lease only runs five years. When combined with the industrial sector's cyclicality and STAG's focus on single-tenant properties, the REIT faces potentially elevated renewal risk in the years ahead compared to other real estate firms.

Finally, management's aggressive growth strategy creates some risk as well. STAG appears to be a disciplined property buyer and competes in a very large market, but there's always a chance that quality is sacrificed for quantity. Again, the next downturn will make the quality of STAG's asset base clearer.

From a dividend safety perspective, STAG's growth ambitions, cyclicality, and elevated payout ratio for an industrial REIT (near 80% as of this writing) make it a less certain bet over a full economic cycle. Should the company's access to capital markets become restricted during a future recession, then reducing the dividend could make sense to alleviate some financial pressure and continue fueling the firm's growth.

Closing Thoughts on STAG Industrial

Certain industrial REITs can be reasonable high-yield investments as part of a well-diversified portfolio. STAG offers several appealing qualities, including a monthly dividend and a management team that embraces a contrarian but disciplined approach to real estate investing.

However, investors need to keep in mind that this industry is more cyclical than most in the REIT sector, with lower retention rates and more volatile cash flows that can result in lumpier and less dependable dividend growth.

Since the company's track record is so short and only covers a period of economic expansion, STAG might not be appropriate for highly conservative investors who seek more proven and defensive investments.