Kinder Morgan's Long-term Dividend Growth Prospects

Kinder Morgan (KMI) has had a rough four years, enduring a painful turnaround that included billions in asset sales (to pay down debt) and a 75% dividend cut in late 2015.

As a result, income investors have had to endure a -50% total return during a time when the S&P 500 is up 60%.

Recently, Kinder Morgan announced what it expects to be the last major asset sale of its turnaround effort, which it believes will allow it to return to some of the fastest and safest dividend growth in the midstream industry.

Let's take a look at what dividend investors need to know, including how safe Kinder's dividend really is and what kind of income growth investors might be able to achieve over the long term.

Kinder Morgan Gives Up On Trans Mountain Pipeline, Slashing Growth Backlog In Half

Kinder Morgan's turnaround plan was necessitated by its poor decision to retain very little cash flow to fund its growth during the boom years when oil prices were consistently over $100 per barrel.

The company focused on growing its dividend very quickly, and thus had a distribution coverage ratio below 1.1 in late 2015. That means the firm was paying out more than 90% of its distributable free cash flow (DCF).

DCF is calculated by subtracting interest expense, taxes, and maintenance costs from EBITDA. It is similar to free cash flow for the industry and supported Kinder Morgan's dividend which management had been saying would grow at 10% annually through 2020.

However, the oil crash meant that credit and equity markets slammed shut and thus cut off Kinder Morgan from cheap growth funding sources.

To avoid a downgrade to junk bond status (which would have drastically increased its borrowing and refinancing costs), Kinder Morgan cut its dividend by 75% in late 2015 in order to adopt a self-funding business model.

Under this more conservative approach, Kinder Morgan would be funding its $12 billion growth backlog of projects with retained DCF rather than issuing additional equity (no shares have been issued since 2015), while it focused on deleveraging its balance sheet.

The company's deleveraging efforts involved over $6 billion in asset sales that resulted in its DCF per share remaining essentially flat over the last four years.

One of Kinder Morgan's biggest headaches over this time was its struggles to expand its Trans Mountain Pipeline, a major oil pipeline in Canada which would help bring significantly more Canadian crude to offshore markets. This $5.7 billion project represented nearly 50% of the firm's growth backlog.

The project has been facing numerous legal challenges from environmental, indigenous groups, and the local and provincial governments in British Columbia since it was announced in late 2013.

After nearly five years and $870 million sunk into the project, management decided the risks of being able to complete it were too great and on May 29, 2018, announced it was cancelling the TMP expansion.

What's more, the company said it would sell the entire pipeline system to the Canadian government for $3.5 billion. Kinder Morgan's share (it owns 70% of Kinder Morgan Canada that was actually building the project) of the post-tax proceeds of the sale will come to $2 billion.

Management says the proceeds will go towards further paying down its debt, which will bring total debt reduction to $8 billion. These deleveraging efforts should lower the company's net debt/EBITDA ratio to 4.7, which is down from close to 6 times in 2015 and more in line with levels that are reasonably safe in this industry.

As a result, Kinder Morgan expects to get a credit rating upgrade from its current BBB- level, which should lower its borrowing costs in the future.

The downside of this major asset sale (which management says is the last it plans to do) is that Kinder Morgan's dividend growth potential has been drastically reduced.

Plan For Accelerating Short-Term Dividend Growth Remains On Track

Before the TMP sale, Kinder Morgan had announced a new shareholder capital plan that involved: a $2 billion share buyback authorization, a 60% dividend hike for 2018, and 25% dividend hikes in 2019 and 2020.

The 60% dividend hike was made official last quarter, and despite the loss of the TMP management remains committed to delivering on its target of 36% annual dividend growth between 2017 and 2020.

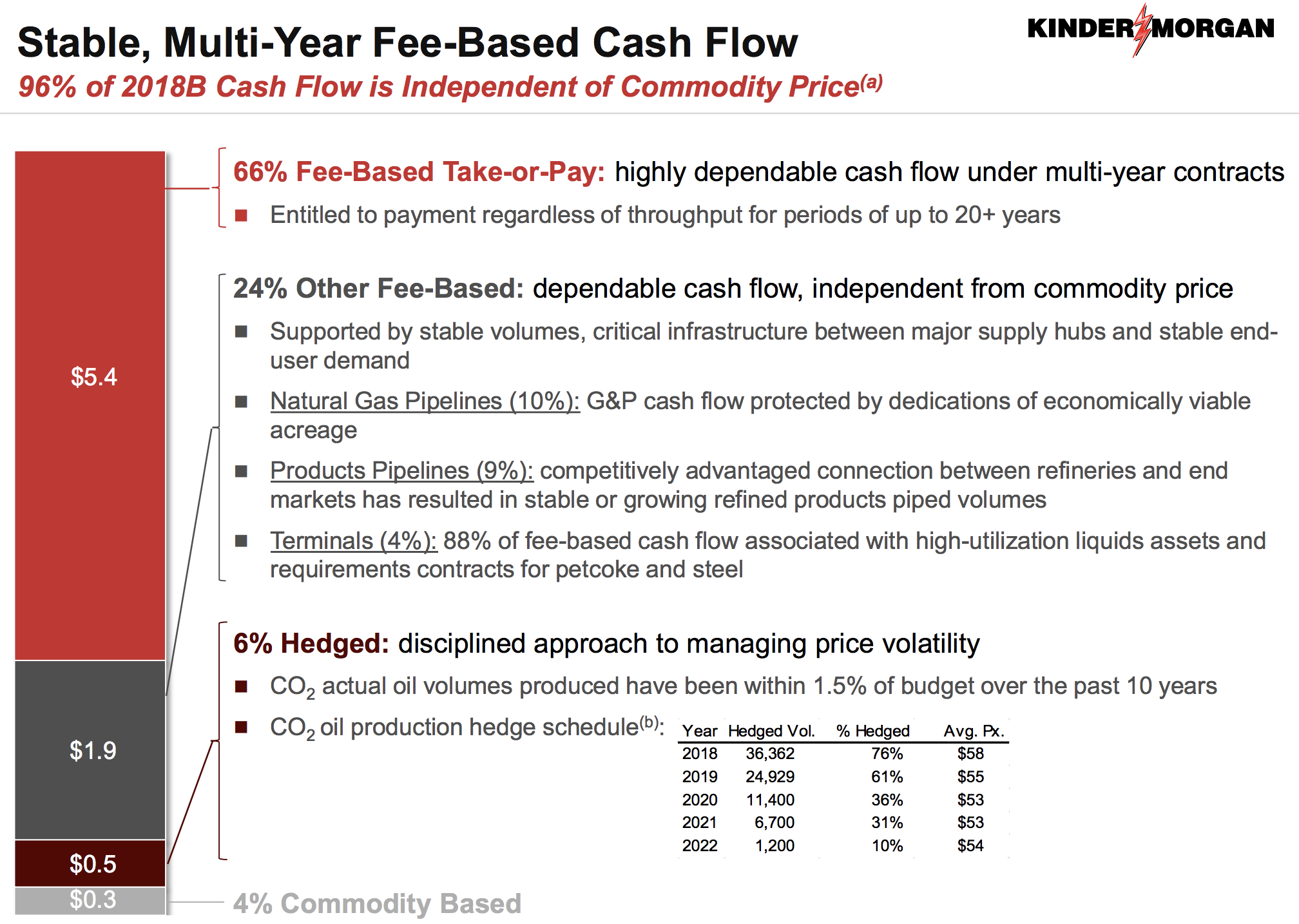

The reason Kinder Morgan believes it can safely do this is because it expects to generate $4.6 billion in stable DCF this year (90% from take-or-pay and other fee-based contracts; 96% of cash flow independent of commodity prices) and spend just $2.4 billion on growth projects.

Source: Kinder Morgan Investor Presentation

That leaves the business with approximately $2.2 billion in excess DCF to pay the $1.75 billion larger dividend, as well as potentially keep buying back shares.

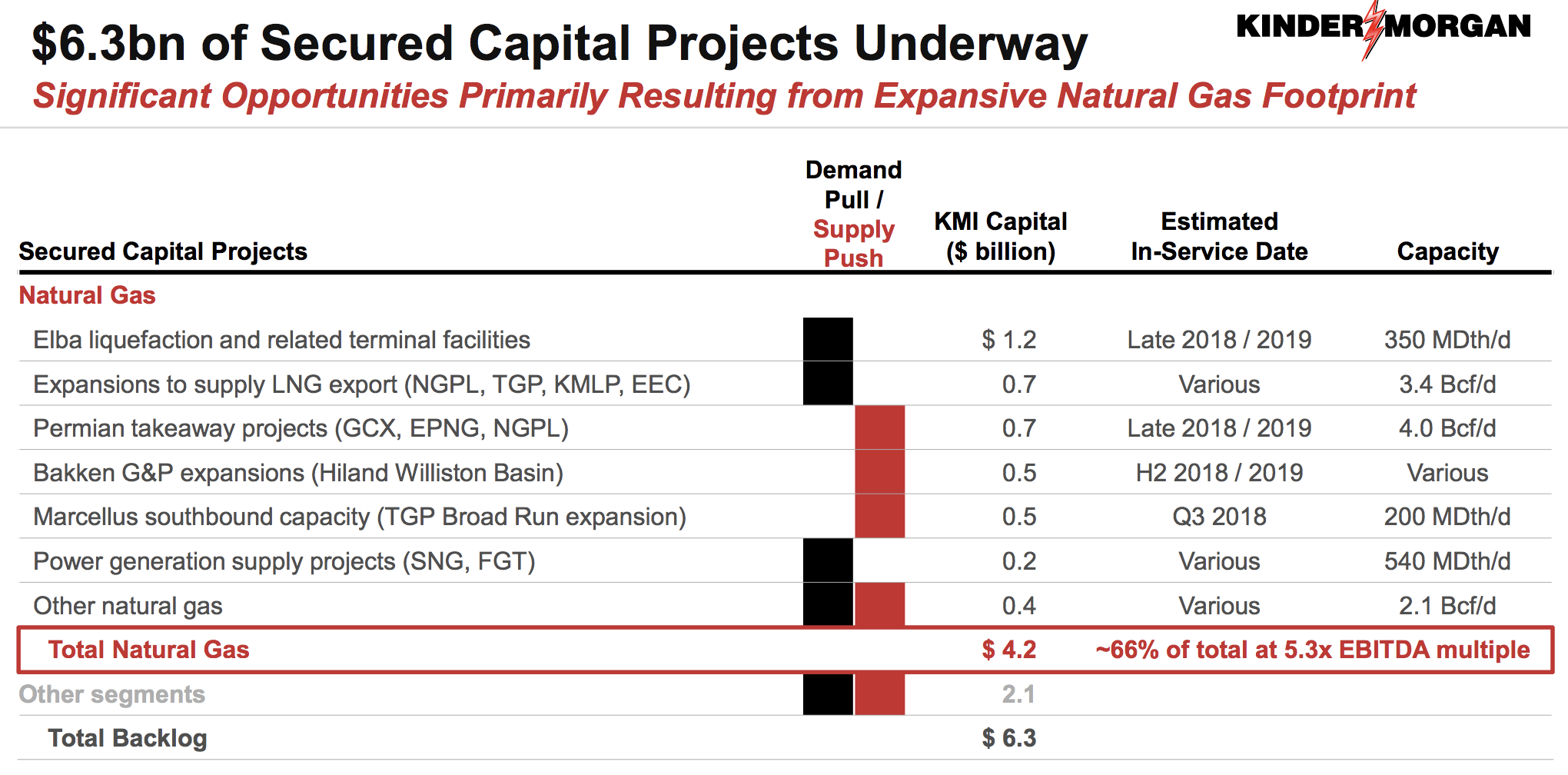

Management has also managed to find new growth projects to start replacing the massive blow it took from selling the TMP. Those include two large gas pipelines designed to carry gas from the booming Permian basin (gas production expected to double over the next five years) to export facilities on the Gulf Coast.

Those two $3.75 billion projects are joint ventures with other midstream/energy companies that Kinder Morgan will own 50% of. Thus it conservatively estimates it should be able to find at least $2 billion in annual organic growth opportunities, ones that are very profitable.

Source: Kinder Morgan Investor Presentation

For example, according to CEO Steven Kean, assuming a cash yield on investment of 14% on projects going forward (current backlog average is 16.7% with gas projects yielding 18.9%) and $2 billion in annual growth spending, Kinder's DCF should be able to grow at about 4% per year.

Therefore, once the TMP sale goes through (end of 2018) Kinder Morgan will likely face just one more flat year of growth in 2019, and then see consistent DCF per share growth for the foreseeable future.

In fact, analysts expect Kinder's 2021 DCF to hit $2.68 per share which would be about 2.2 times its planned $1.25 dividend for 2020. In other words, Kinder Morgan would be retaining 55% of its cash flow after paying its dividend, or about $3.1 billion per year.

That sum is likely sufficient to fund the company's now more conservative long-term growth plans. As a result, management expects Kinder's leverage to continue to fall over time.

As this plays out, the firm has potential to enjoy future credit upgrades, lower borrowing costs, and increased financial flexibility to accelerate organic and acquisitive growth.

Simply put, while the sale of the TMP is yet another unexpected blow during Kinder Morgan's turnaround saga, the worst appears to be behind the company.

However, despite Kinder Morgan's turnaround efforts appearing to be nearly over, its long-term growth outlook has been drastically reduced, making it one of the less appealing high-yield income choices in this fast-growing industry.

Closing Thoughts on Kinder Morgan

Kinder Morgan made some major mistakes with its capital allocation before the oil crash, including relying far too much on dangerous amounts of debt to fund its growth.

That being said, management appears to have learned its lesson, and the company's self-funding growth strategy is a far safer and more conservative approach.

And thanks to its long-term contracted cash flow and remaining $6.3 billion backlog of simpler and profitable growth projects, the company should be able to resume modest but steady DCF per share growth beyond 2019.

Regardless, the loss of the Trans Mountain Pipeline and thus half its growth backlog does mean that Kinder Morgan's long-term dividend growth is likely to be far slower than it has been prior to the oil crash.

While management's plan to increase the dividend 60% in 2018 and 25% in 2019 and 2020 appears reasonable, that fast growth rate is unsustainable since it comes at the expense of DCF payout ratio expansion.

Management has indicated that it plans to fund most of the firm's organic growth projects ($2 billion to $3 billion per year) with retained cash flow, which means that Kinder Morgan will likely have to reduce its dividend growth rate in 2021 and beyond to match its DCF per share growth.

Based on management's most recent guidance, that would imply 4% to 6% long-term dividend growth. While that's a decent pace for a stock with a yield of 4.5% (and 25% dividend growth expected in each of the next two yeras), it's still hard to favor Kinder Morgan over some of its more conservative peers such as Enterprise Products Partners (EPD) and Magellan Midstream Partners (MMP).

These firms benefit from the same tollbooth-like business model as Kinder Morgan, but they have stronger balance sheets (BBB+ credit ratings, the best in the industry) and also enjoy self-funding business models (no need to issue equity to grow).

More importantly, they have never had to cut their payouts and are guided by management teams who deserve the benefit of the doubt when it comes to long-term capital allocation decisions.