Cardinal Health: A Dividend Aristocrat Facing Challenges

Founded in 1971, Cardinal Health (CAH) is one of the world’s three largest medical supply and pharmaceutical distributors. The company essentially acts as a middleman that sources more than 400,000 medical supplies and drugs from over 5,000 pharmaceutical and medical supply companies.

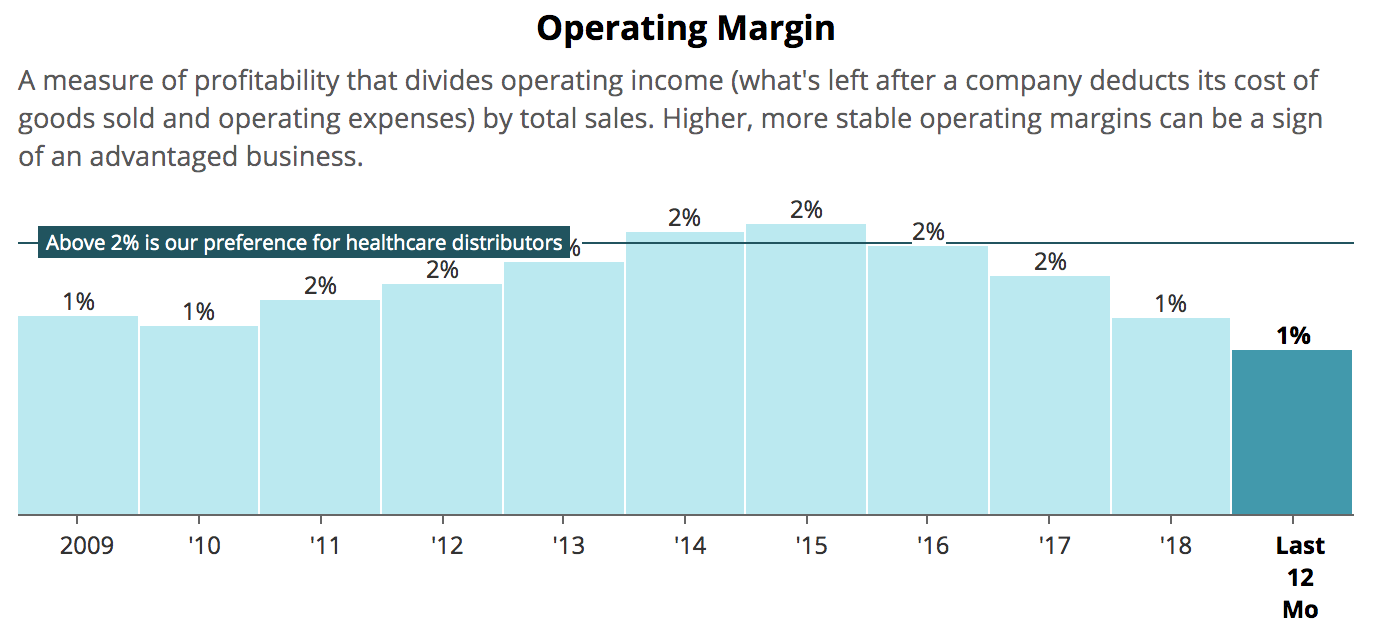

Cardinal Health then distributes these products to various clients along the medical industry supply chain. The company’s operating margin typically sits between 1% and 2%, reflecting the small sliver of profit Cardinal Health makes on each sale. The firm, therefore, depends on generating a high volume of sales to turn a meaningful profit.

The company operates two business segments:

Pharmaceutical (89% of sales, 75% of profits): distributes branded and generic pharmaceutical, specialty pharmaceutical, over-the-counter healthcare, and consumer products to retailers, hospitals, and other healthcare providers, including over 26,000 pharmacies, 140,000 doctors offices and clinics, and 85% of hospitals in the U.S. The pharmaceutical segment offers data and drug supply and distribution management (i.e. back office logistics) services to its clients and suppliers as well.

Medical (11% of sales, 25% of profits): manufactures, sources, and distributes medical, surgical, and laboratory products, including cardiovascular and endovascular products; wound care products; surgical drapes, gowns, and apparel; exam and surgical gloves; fluid suction and collection systems; and incontinence, enteral feeding, urology, operating room supply, electrode and needle, and syringe and sharps disposal product lines to hospitals, ambulatory surgery centers, and clinical laboratories in the U.S., Canada, and Europe.

While Cardinal operates in over 45 countries, about 90% of the company's sales are derived from the U.S.

Cardinal has raised its regular quarterly dividend every year since 1985, making it a dividend aristocrat.

Business Analysis The investment thesis for Cardinal Health hinges on a fast-aging population driving higher U.S healthcare spending, especially on pharmaceuticals and medical supplies, over the coming decade and beyond.

Annual healthcare spending is projected to grow by 5.5% annually through 2027 to reach almost $6 trillion (up from $3.4 trillion in 2016), according to the Centers for Medicare and Medicaid Services. Growth will be largely driven by about 10,000 baby boomers reaching retirement age per day (through 2034) and the natural inclination for older people to require more medical care.

Until recently, Cardinal Health enjoyed impressive growth, compounding its non-GAAP EPS and dividend by 8.2% and 16%, respectively, between fiscal 2012 and 2017. The company's stock price also returned more than 100% during this period.

Between 2012 and 2017 Cardinal Health benefited from the boom in generic drugs. Tens of billions of dollars worth of brand-name drugs lost patent protection in 2012, resulting in a surge in generic competition over the following years.

Generic drugs carry higher margins for Cardinal Health compared to branded drugs. As generic drug pricing increased, the company enjoyed a boost to its gross profits.

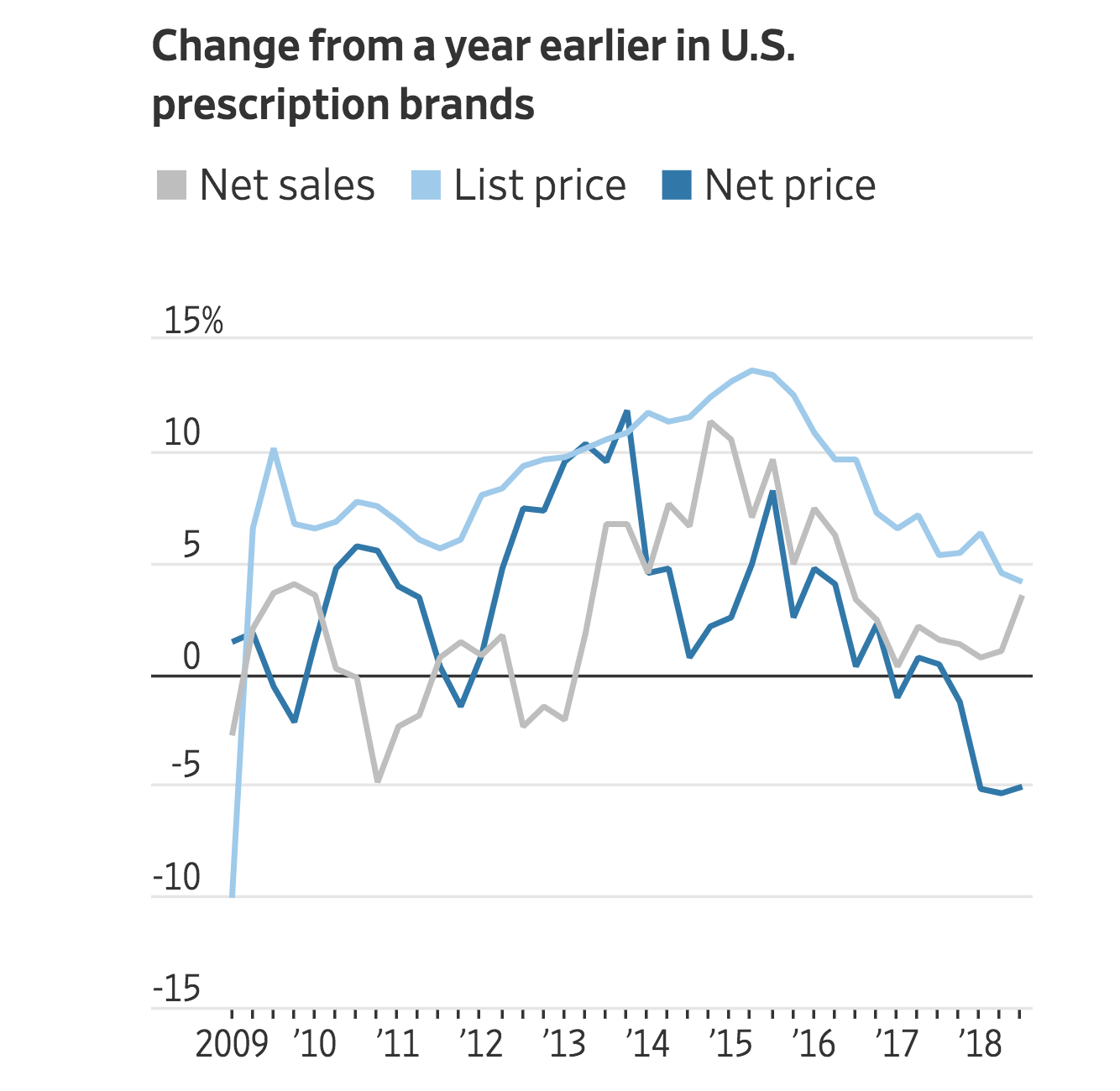

However, the tide is now going back out. Most of the entire pharmaceutical value chain is under pressure to cut costs and make healthcare more affordable.

Many pharma businesses are moderating price increases on their drugs in response to increased political pressure. Generic drug prices have also been hit because of faster approvals by the Food and Drug Administration (resulting in more generic drug supply) and a price-fixing investigation, according to The Wall Street Journal.

Source: Wall Street Journal

The Wall Street Journal notes that “drug distributors had feasted for years on stable or rising drug prices, which allow them to more easily mark up prices while profiting by arbitraging annual price increases. Now, the more rapidly prices fall, the more difficult it becomes for distributors like Cardinal to resell drugs from manufacturers to pharmacies at a profit.”

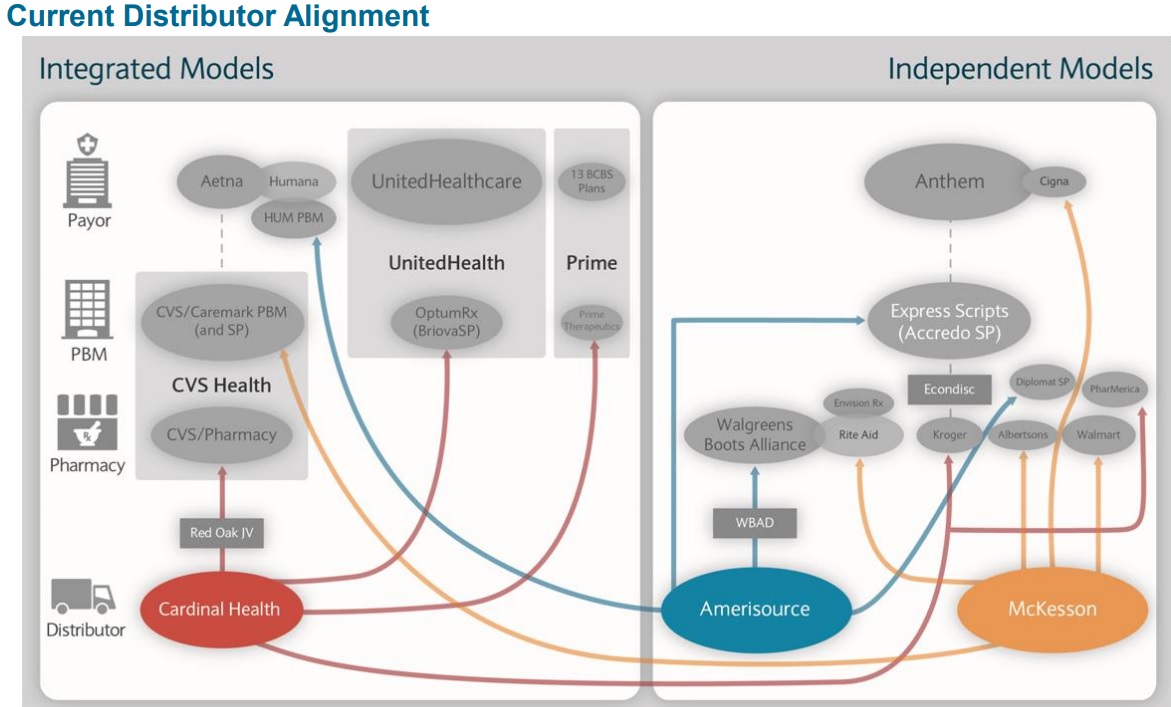

Equally important, pharmacies and other players across the medical supply chain have consolidated in recent years as they faced increased margin pressure from lower reimbursement rates. This consolidation trend has resulted in major pricing pressures on all medical wholesalers because large customers can play the industry giants off each other.

For example, in 2012 Safeway canceled its drug supply contracts with McKesson in favor of Cardinal Health; however, in 2016 Safeway decided to drop Cardinal after its 2015 merger with Albertsons.

Similarly, Cardinal Health had a long and profitable relationship with Walgreens up through 2012, until Walgreens signed a 10-year service agreement with AmerisourceBergen.

Cardinal was able to come back though, thanks to the creation of Red Oak Sourcing, a 50/50 joint venture with CVS Caremark designed to streamline their respective drug supply chains and lower costs through economies of scale.

Another problem for medical wholesalers has been that a traditional source of higher profits, independently owned pharmacies, have now started banding together in Group Purchase Organizations, which increases their collective purchase power over suppliers.

As a result, they have been able to exert more pressure on the prices they pay Cardinal Health for the drugs it resells to them. Simply put, the economics of the drug distribution business appear to be structurally changing.

A company like Cardinal Health will always play a role, but the middlemen seem increasingly likely to bear the brunt of healthcare reform and sell-side consolidation in the form of shrinking margins.

Cardinal Health – Source: Simply Safe Dividends

While rising demand from a growing and aging population could eventually stabilize wholesale drug distribution, even with the growing supply of generics today's environment could very well be the new normal.

DrugChannels.net provided an excellent review of the margin pressures that wholesale distributors face including five key trends it expects to continue through at least 2019:

Slower branded drug inflation and generic deflation will likely pressure wholesale distribution margins

Regulatory changes to drug reimbursement policies challenge the underlying business model

Ongoing pharmacy consolidation will likely continue to pressure the big three distributors as they battle for market share and volumes

Specialty drugs are one of the few positives, with specialty drugs expected to grow to 47% of all drug sales by 2022

But vertical healthcare integration (such as hospitals bringing doctors' practices in-house) potentially limit the upside to specialty drug growth

In other words, industry experts and analysts expect the same challenges of the past few years to continue for the foreseeable future. Since distribution is largely a scale game, these rivals might battle even harder with each other for market share, and the stakes are high.

For example, CVS Health (CVS) accounted for 25% of Cardinal Health’s sales last fiscal year, UnitedHealth's (UNH) OptumRX was another 11%, and the firm's five largest customers totaled about 50% of overall revenue.

Losing major customers or having to further concede on pricing to retain them could really impact the company’s bottom line, especially if Cardinal Health is unable to negotiate better terms with its drug manufacturers.

As part of its long-term growth plan, Cardinal has tried to diversify by making $8 billion worth of mostly debt-funded acquisitions to acquire medical devices businesses from Medtronic and Johnson & Johnson:

October 2015: paid $1.9 billion for J&J's Cardiovascular and Endovascular product lines

July 2017: paid $6.1 billion for Medtronic's Patient Care, Deep Vein, Thrombosis, and Nutritional Insufficiency business lines

This could be another signal that Cardinal Health’s core pharma distribution business might not have the favorable long-term outlook that the company once thought (thus there was increased pressure to diversify).

Adding some of Medtronic’s products will likely provide economies of scale in medical products manufacturing and sourcing, potentially helping profitability while increasing the company’s product breadth. Cardinal Health's medical segment also enjoys higher operating margins than its pharma segment (4-5% vs 1-2%).

However, medical devices still seem like a price-sensitive business that can be challenging to compete in. Cardinal Health may not have much of a durable competitive advantage here either.

Overall, the current growth headwinds facing Cardinal Health seem likely to persist. While drug sales are still expected to grow at 3% to 4% over time, that's a far cry from the double-digit growth of 2014 and 2015.

Until Cardinal can stabilize and improve its profitability, driven largely by cost savings initiatives, the firm's earnings and dividend growth will likely struggle to exceed a low- to mid-single digit pace.

While Cardinal maintains an investment grade credit rating, it's worth noting that its balance sheet has taken a bit of a hit due to the debt it's taken on to make medical device acquisitions. This will further weigh on its dividend growth prospects.

Ultimately, investors should focus more on Cardinal's future outlook and risks rather than get caught up in its storied past as an impressive dividend aristocrat.

Key Risks There are several significant risks to understand before investing in Cardinal Health.

First, the medical industry is highly complex, with five levels of supply chain: manufacturers, distributors, pharmacy, pharmacy benefit managers, and payers – insurance companies or Medicare/Medicaid.

Complexity is further increased by the interplay between private and public funding sources and the government's desperate need to lower medical costs, which have far outpaced inflation for over 30 years.

Combined with the razor-thin margins of many parts of the supply chain (especially distribution and pharmacy), there is an endless shifting of the various players into often confusing relationships as everyone attempts to maximize margin while putting the screws to their own suppliers.

Simply put, it is a very complex and dynamic landscape.

Investors considering the space need to be comfortable with the highly dynamic nature of this business and trust that management will be able to continue growing sales, earnings, cash flow, and the dividend in the coming years despite occasional setbacks, such as loss of supply contracts with major retailers.

Then there’s the constant threat of increased government regulation of medical prices, or even just Medicare/Medicaid potentially being able to negotiate bulk purchases, which could result in ongoing industry uncertainty and potentially permanently lower margins.

The proposal for single-payer healthcare (Medicare-For-All championed by many Democratic presidential hopefuls), while not a high probability short-term risk due to partisan gridlock, is another potential threat to keep in mind. Such a system would likely permanently result in lower profitability across the sector.

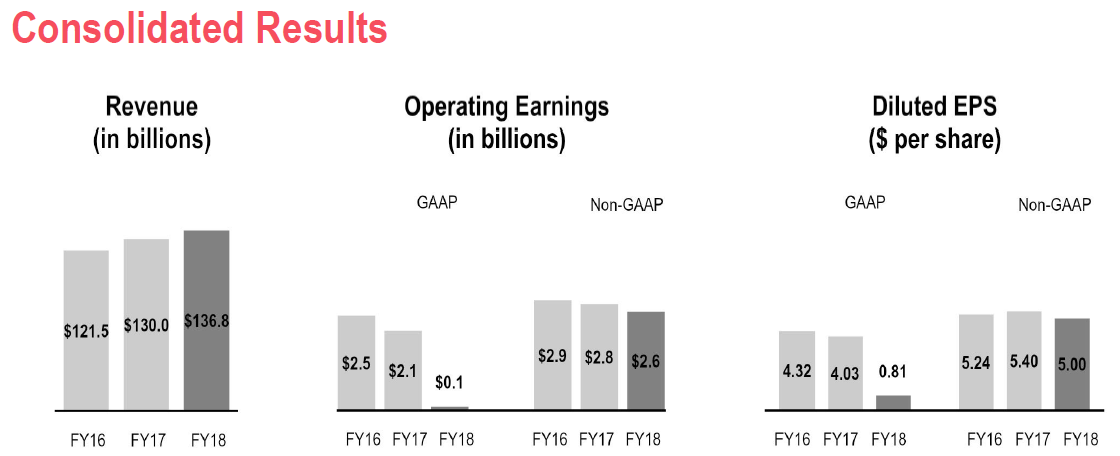

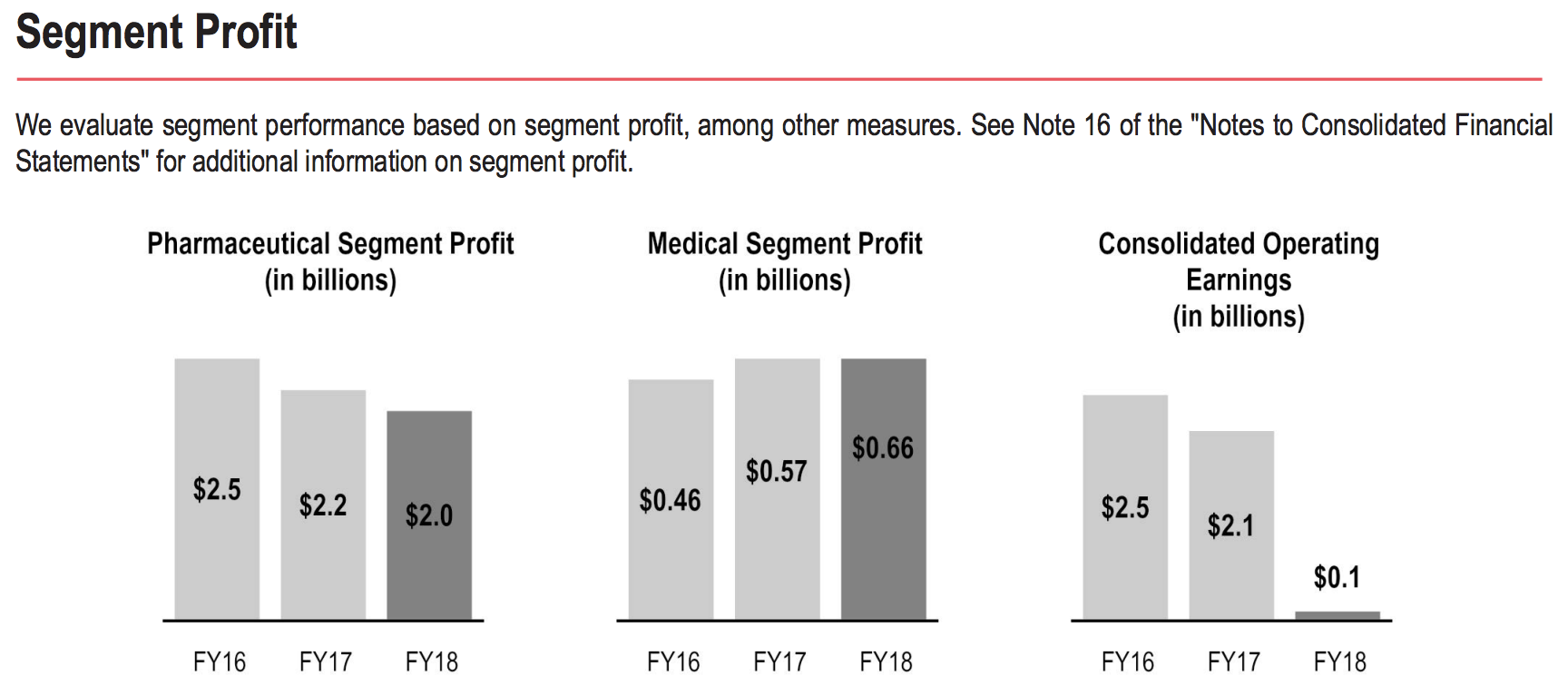

The existing regulatory changes have already greatly impacted the company as you can see by the fact that while sales continue to rise steadily, operating profits are declining.

Source: annual report

The main issue lies in the pharmaceutical segment, where operating margins continue getting squeezed due to lower drug reimbursement and generic drug price deflation.

Source: Cardinal Health Annual Report

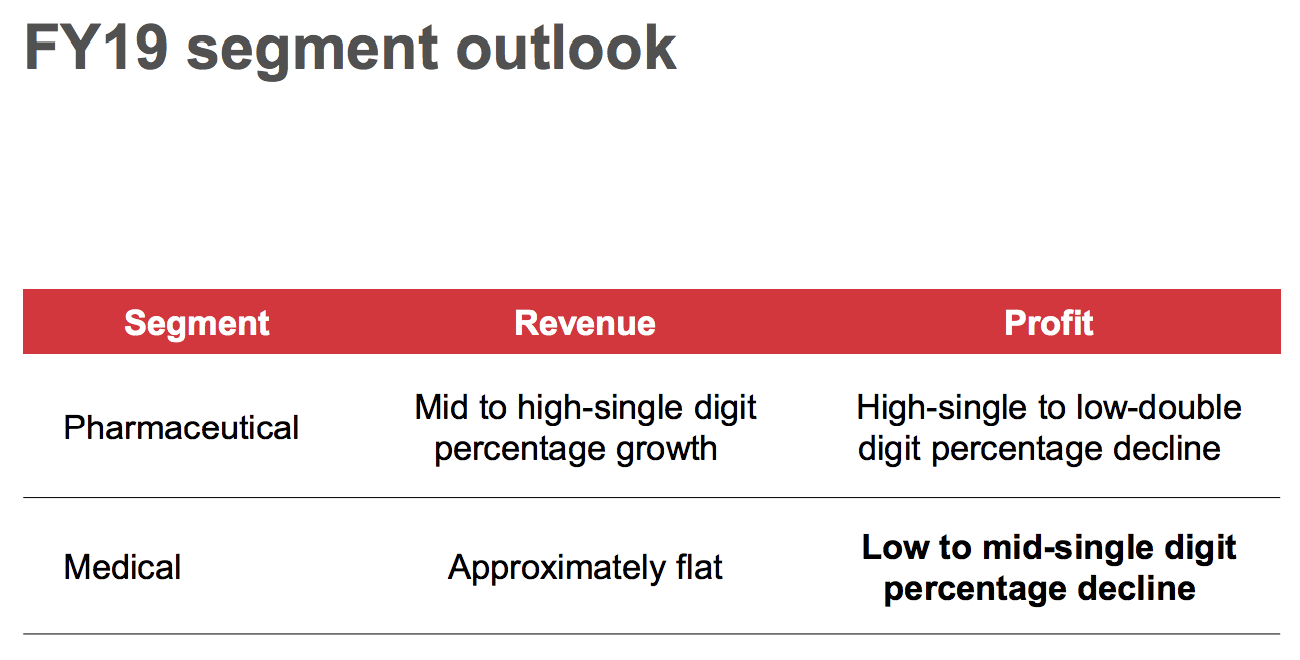

Management expects fiscal 2019 to be another year of negative growth, as outlined it its 2018 annual report:

"Within our Pharmaceutical segment, we expect fiscal 2019 segment profit to be less than our fiscal 2018 segment profitdueto the adverse impact of customer contract renewals, generics program performance, and the previously announced loss of a large pharmaceutical distribution customer."

What about the company's plan to diversify into medical devices? While that sounds like a reasonable plan at first, there are several challenges with it. The first is that Cardinal's expertise is largely in drug distribution, and it has run into some challenges while attempting to diversify its business.

Cardinal's first big medical device deal, Cordis, has been plagued with difficulties since it bought the business from J&J. Specifically, Cordis has struggled with supply chain issues, requiring a $1.4 billion write-down in 2018 (equal to almost 75% of the price the company paid for the entire business).

The company believes it can get them sorted out eventually, as part of Cardinal's overall turnaround plan which includes a two-year $200 million cost-cutting initiative it expects to complete by the end of fiscal 2020.

However, citing "market dynamics" and "incremental supply chain costs," in May 2019 management downgraded its outlook for Cardinal's Medical segment and now believes this business will experience a full-year profit decline (compared to prior expectations for mid to high-single digit growth).

Source: Cardinal Health Earnings Presentation

Flat revenue growth and falling profits are not what management expected when they entered the medical devices business, which has clearly proven to be a competitive and dynamic marketplace.

Unfortunately, Cardinal Health bought these businesses from two well-managed firms who probably had a better read on the future of these markets. After all, Johnson & Johnson and Medtronic sold their medical device businesses to Cardinal to monetize some of their slower growing and lower margin business units.

While the margins on medical devices might be far higher than for pharmaceutical sales (almost four times as great), Cardinal's diversification plans appear to be buying businesses from companies that no longer want them, and possibly for good reason. The firm's reduced 2019 guidance for its medical device segment is evidence towards that effect.

Management has divested several non-core businesses in recent years to try and improve its mix. However, more work may be required here, especially as Cardinal feels pressure to keep its balance sheet strong following several years of large increases in debt, thanks to its pivot into medical devices.

Source: Simply Safe Dividends

Cardinal's debt levels aren't currently dangerous, as demonstrated by its BBB+ investment grade credit rating from Standard & Poor's. However, the firm's net leverage ratio now sits at levels that could cause more cracks in its dividend safety profile if its cash flow outlook further deteriorates.

At the very least, dividend growth will remain very weak (1% increase announced in May) to maximize the amount of retained cash flow available for paying down debt and protecting its credit rating.

In fiscal 2018 Cardinal's retained free cash flow (free cash flow minus dividends) was $1.8 billion compared to about $9 billion in debt. In other words, it could take several years of very slow dividend growth before the company is able to return to historical debt levels that improve its financial flexibility and better position it to adapt to the challenging industry environment.

Only time will tell how the competitive healthcare landscape shakes out, but the high fixed costs and low margins in this business really amplify any changes in revenue, for better or worse. In the meantime, Cardinal has to deliver improved execution compared to the last few years, otherwise its long-term growth potential will likely be permanently impaired, and its dividend safety profile could take a hit.

Closing Thoughts on Cardinal Health The healthcare sector’s desperate need to cut costs means the future of the medical distribution industry will likely be one where scale is larger, but companies like Cardinal Health will struggle to maintain their already low margins.

Management’s plan to diversify into higher-margin medical equipment and wholesaling has its own risks including poor execution in integrating its latest acquisitions thus far.

Given the firm's recent token dividend increase, along with the ongoing fear, uncertainty, and doubt that pervades the industry (and all of its complexities), Cardinal Health doesn't seem suitable for a conservative dividend growth portfolio, despite its dividend aristocrat status.

Owning businesses with greater pricing power and more controllable competitive advantages is preferable. Although Cardinal Health’s relatively low valuation may look tempting, it could be more of an acknowledgment of the company’s structurally lower growth profile and the risks faced by management’s debt-fueled and thus far subpar expansion into medical devices.

Therefore, as we stated in our February 2019 note, anyone interested in this business needs to have realistic growth expectations, as well as be patient enough to possibly endure another year or two of underperformance (and weak dividend growth) while the turnaround hopefully gains traction.

Given the changes taking place in the industry, our preference would be to seek out companies with more predictable outlooks.