Cisco: A Strong Technology Brand with a Safe Dividend

Cisco (CSCO) was founded in 1984 and has grown to become one of the most important technology companies in the world. While the business sells a wide variety of products and services to businesses of all sizes, its main offerings connect computing devices to networks or computer networks with each other.

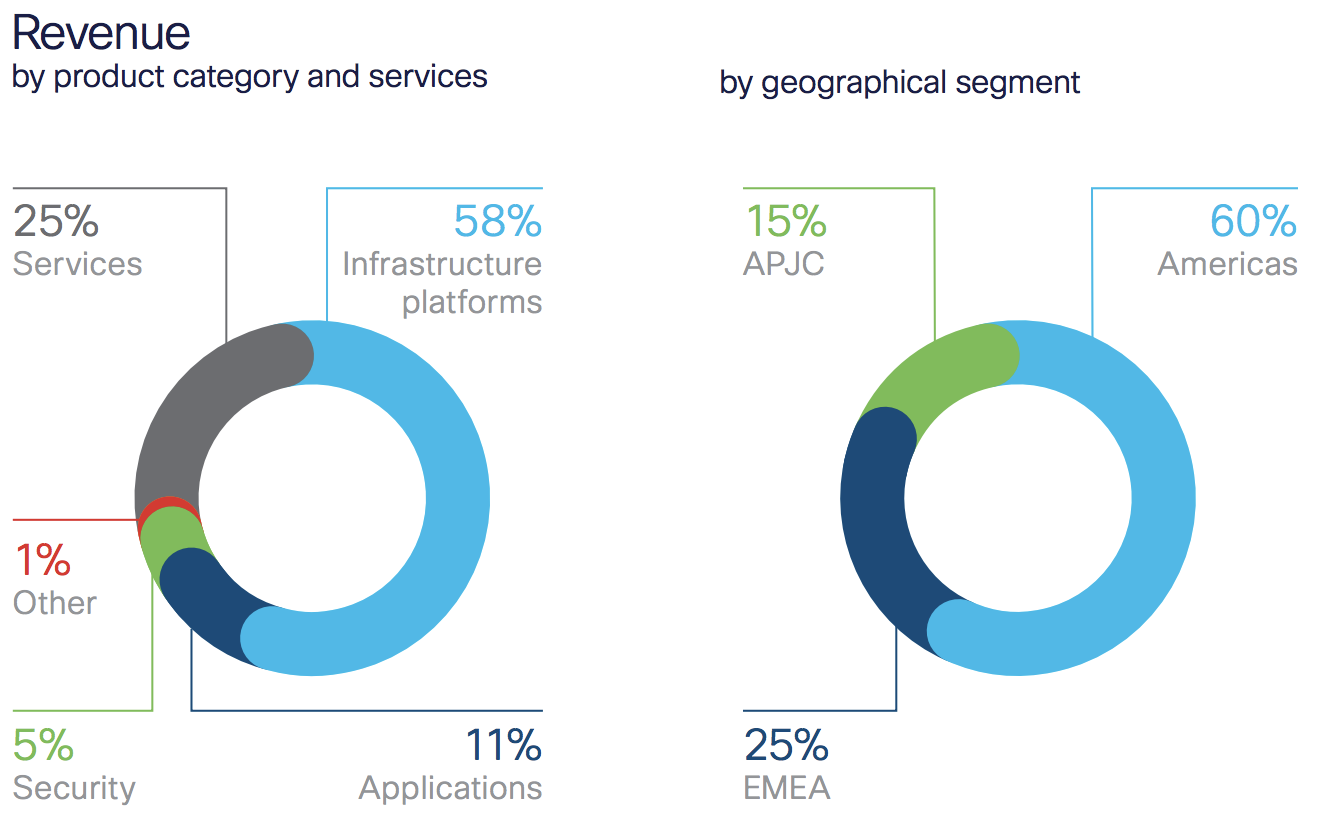

The company’s website provides an overview of switches and routers, which are Cisco’s largest product segments and part of its infrastructure platform business segment.

Switches are used in buildings, offices, and data centers to connect devices such as workstations, servers, and phones together on a computer network. They help receive and forward data to the right device.

Routers pass along data packets between computer networks to connect wireline and mobile networks used for mobile, data, voice, and video applications. They essentially direct the internet’s traffic to the appropriate destination.

Besides routers and switches, which act as the backbone of Cisco's infrastructure platforms, the rest of the firm's revenue is spread among a number of faster-growing segments – applications (11% of revenue), security (5%), and services (25%), which consist of technical support, subscriptions, and software spread across its various segments.

Source: Cisco Annual Report

Cisco's stated goal is to shift away from cyclical hardware sales and focus more on recurring software and service revenue (over 30% of revenue is now from recurring sources). This helps to stabilize cash flow over time.

By geography, approximately 60% of Cisco’s sales last fiscal year were in the Americas with another 25% in EMEA (Europe, the Middle East, and Africa) and 15% in Asia.

Cisco only began paying a dividend in 2011, but the tech giant has raised its dividend each year since.

Business Analysis

Cisco dominates most of its core markets. According to market research firm IDC, Cisco’s share in the Ethernet switching market was about 51% at the end of the third quarter of 2019. The company’s market share in routers and services stood at approximately 38%.

Cisco’s dominance is partly explained by its ability to offer customers an entire suite of solutions with its network equipment and services. The company has evolved from selling networking hardware into offering higher-value packages of complete architectures and solutions that improve customers’ businesses.

Selling architectural solutions is much more profitable for Cisco and allows the customer to deal with fewer vendors and potentially enjoy a lower total cost of ownership.

Most of Cisco’s competitors do not have the same breadth of products and services (security, switching, wireless, routing, collaboration, etc.), making them less of a factor in these lucrative deals.

Cisco has spent more than $18 billion on research and development over the last three years combined to stay relevant and build out its portfolio, a magnitude of spending that few companies can come close to matching.

Cisco makes acquisitions to keep adapting its portfolio as well. Since 1995 the firm has spent more than $80 billion to acquire over 250 companies. These deals have also helped Cisco’s multiyear transition as it shifts its model from a primarily hardware business into more of a software and services business, which has been a top priority for CEO Chuck Robbin since he took the helm in July 2015.

About 33% of Cisco’s revenue is now recurring, and by 2022 the company expects that figure to reach 37%. The company's legacy domination of IT data connection hardware has helped this effort by creating a large installed base and a sticky ecosystem.

IT departments usually replace hardware every three to seven years. However, since the majority of IT transitions are done manually (an often complex and time-consuming job), many of Cisco's customers are loath to switch over to new hardware suppliers. That's because errors and troubleshooting problems during such transitions can cost a business dearly in down time.

Thanks to Cisco’s enormous breadth of hardware products and software services, along with some of the headaches involved with switching networking suppliers, it’s difficult for competitors to match the company’s product lineup and ongoing convenience.

By focusing on developing extremely reliable hardware, building a brand based on quality, and using its economies of scale to keep costs low, Cisco typically enjoys price premiums and very healthy margins on its products.

Beyond its technology portfolio and unique ability to deliver architectural solutions, Cisco is a sales and marketing juggernaut that has established one of the most valuable brands in the world.

A substantial portion of Cisco’s products and services are sold through channel partners, such as telecom providers (e.g. Verizon) and systems integrators. Cisco has maintained these relationships for a long period of time and is uniquely positioned to meet the needs of its biggest partners thanks to its broad portfolio, brand strength, and ability to deliver high volumes of product.

As a result, the company has built up a massive installed base that provides steady revenue opportunities.

Overall, Cisco just does a great job of providing cost-effective, reliable, and often integrated solutions at scale to customers.

Given the perceived similarities between many of the products in Cisco’s markets, its branding and long-lasting channel partner and customer relationships are especially important.

In addition to possessing a clear economic moat, many of the best dividend stocks also operate in industries characterized by a slow pace of change. After all, change is often the enemy of predictable cash flow generation.

Cisco’s core markets are no doubt characterized by a faster pace of change than other industries such as trash collection, but their importance should not be overlooked either.

Cisco’s networking products are extremely important for any infrastructure environment and are necessary for virtually any business. Without Cisco, much of the country’s communications infrastructure would not function.

As the use of data and bandwidth continues to see exponential growth, more networking infrastructure and software is also needed to handle the traffic and keep it secure, providing a long stream of demand.

There seems to be no end in sight to the number of consumer and business devices needed to be connected to a network. While this certainly doesn’t guarantee Cisco’s future success, the mission-critical nature of most of the company’s products and services provides some comfort.

Key Risks

Cisco's biggest growth markets are in emerging economies like Brazil, India, China, and Mexico. However, not only do such economies tend to be more cyclical, but the company's faster sales growth in these markets means its sensitivity to currency fluctuations is increasing over time.

If the U.S. dollar rises significantly against local currencies in these countries, then Cisco's U.S. dollar-denominated results could take a hit. Fortunately, currency translation issues tends to cancel out over time.

More importantly in the short term, volatility in IT spending trends can impact demand for Cisco’s products and services any given quarter and cause the company to miss near-term earnings estimates. However, this risk doesn’t have any bearing on Cisco’s long-term earnings potential.

The bigger concerns in most technology markets are changing trends that make a company’s products irrelevant, as well as increased competition that commoditizes previously profitable technologies.

For example, in recent years Cisco’s largest product segments, switching and routing, have lost market share and struggled to achieve profitable growth.

This has been driven in part by intensified competition (e.g. Arista) and the rise of the cloud, which shrinks companies’ data centers (and need for switches), reduces network complexity, and provides more opportunity for tech giants such as Amazon to handle companies’ networking requirements.

Technology shifts require Cisco to continuously innovate to remain dominant in its markets. In the firm's 2015 shareholder letter, Cisco’s CEO notes that much of the company’s “success has come from [its] ability to lead market transitions.”

That’s why Cisco is somewhat shifting focus from its traditional business (switches and routers) to emphasize investments in emerging areas such as cybersecurity, the Internet of Things, and cloud computing.

Perhaps the most discussed technological risk facing Cisco is the rise of software-defined networking (SDN). SDN is part of the market’s transition to more programmable, flexible, and virtual networks.

SDN essentially moves some networking functions away from hardware to software, reducing demand for networking equipment (or at least reshaping it) and enabling the substitution of lower-priced, unbranded gear. Unbranded systems can also provide an opportunity for customers to customize their systems based on their unique computing needs.

Cisco has historically been strongest in branded networking hardware, which is why SDN gets so much attention. Cisco is responding to this risk by building and acquiring new software and services and is actually a leading player in SDN today with its own solution.

It’s also important to realize that most companies implementing SDN still require a lot of networking hardware. Non-branded, "white box" equipment seems unlikely to ever dominate the market, but it's a risk for long-term investors to monitor.

After all, it's hard for technology giants to stay nimble and respond to changing trends in a timely and profitable manner. Simply put, the rise of the cloud, mobile devices, and big data are forcing IT architectures and computing to evolve and become more flexible, forcing Cisco to adapt quickly to remain relevant.

Overall, Cisco’s technologies will continue facing functional and pricing pressures as its markets change. The company seems to have the strengths (financially, technologically, and strategically) necessary to remain a large cash cow, but its sheer size also causes it to move slowly.

Cisco can’t be as cutting edge as some of its smaller rivals, but its entrenchment with customers should also be recognized.

Closing Thoughts on Cisco

Cisco’s investment case certainly isn’t perfect. Some of Cisco’s legacy businesses have been under pressure for years as competition has intensified and technology trends have evolved (software-defined networking, the cloud, etc.).

It will also take time for the company to achieve needle-moving success in faster-growing areas such as security, which face immense competition.

Fortunately, Cisco appears to have a strong foundation in network equipment and services, as well as the necessary financial firepower, business partners, installed base of customers, and brand recognition to make the investments necessary to stay relevant over time.

As a result, Cisco’s dividend continues to look very safe with solid growth prospects. Assuming Cisco shows continued stability in its core hardware businesses and greater traction in its faster-growing segments, which provide nice recurring revenue, the company seems like a reasonable holding for a diversified dividend growth portfolio.