Kimberly-Clark: A Recession-Resistant Dividend Aristocrat

Kimberly-Clark (KMB) was founded in 1872 and has grown into one of the largest manufacturers of tissue and hygiene products. The company's products have such a wide reach that they are used by one-quarter of the world's population.

Kimberly-Clark's products are sold under a number of well-known brands, including five billion-dollar brands: Huggies, Kleenex, Cottonelle, Scott, and Kotex. Products are primarily sold to supermarkets, mass merchandisers, drugstores, and other retail outlets.

Source: Kimberly-Clark Investor Presentation

By segment, Personal Care (diapers, training pants, wipes, feminine and incontinence care) accounts for about 50% of the firm's sales and profits.

Consumer Tissue (facial tissue, bathroom tissue, paper towels) contributes roughly 30% of Kimberly-Clark's mix, and K-C Professional (facial tissue, bathroom tissue, paper towels for away-from-home use, safety products) accounts for nearly 20%.

By geography, just over half of sales and more than 70% of segment operating profit come from North America. Developing and emerging markets account for approximately 30% of the company's overall sales, up from 14% in 2003.

With 47 consecutive years of dividend growth, Kimberly-Clark is a dividend aristocrat and becomes a dividend king in 2022.

Business Analysis Few businesses have survived for as long as Kimberly-Clark has. The company’s size, financial strength, and presence in mature, slow-changing markets make it difficult to disrupt.

Kimberly-Clark’s scale allows it to manufacture its products on a very cost-effective basis and squeeze more favorable terms out of its suppliers. However, the company’s marketing campaigns and brand equity are arguably its strongest advantages.

The company routinely spends more than $600 million annually on advertising, and retailers have few reasons to change the products they choose to promote. There is only so much shelf space for the types of products Kimberly-Clark sells, and retailers want brands that will sell quickly and at healthy margins.

Simply put, retailers have little incentive to do business with new suppliers if their current mix is generating strong results and supported by the massive marketing budgets of companies like Kimberly-Clark. Not surprisingly, it is challenging for potential new entrants to break into the firm's distribution channels.

Kimberly-Clark’s marketing budget also allows it to respond aggressively to smaller players’ efforts to compete on price or release an innovative new product. The company can outspend them, redirect its R&D investments (which routinely exceed $300 million each year), and leverage its well-known brands and distribution channels to eliminate most threats in due time.

As a result, the company enjoys #1 or #2 market share positions in 80 countries. Kimberly-Clark also claims to have created 5 of the 8 major product categories in which it competes, underscoring its strong history of innovation and the returns it has reaped from its consistent investments in research, development, and advertising.

The mature nature of the tissue and hygiene markets adds to the challenges new entrants face. For example, product use cases in these markets hardly change over time (e.g. diapers will continue doing the same job with only incremental technology improvements, such as better sealing).

Furthermore, in categories like diapers, customers want products that are reliable and trustworthy, making them less likely to switch brands.

The industry's slow pace of change also reduces the number of opportunities other players have to capitalize on trends Kimberly-Clark might not have recognized. Consumption patterns are pretty stable as well and tend to track population growth, further limiting the potential for rapid disruption.

All of these factors have combined to help consolidate many of the markets Kimberly-Clark operates in. For example, Kimberly-Clark and Procter & Gamble dominate the global diaper market with over 80% share.

Brand loyalty, large marketing budgets, continuous product innovation, and proven sales success across many retail customers have historically provided incumbents with numerous competitive advantages and favorable pricing power.

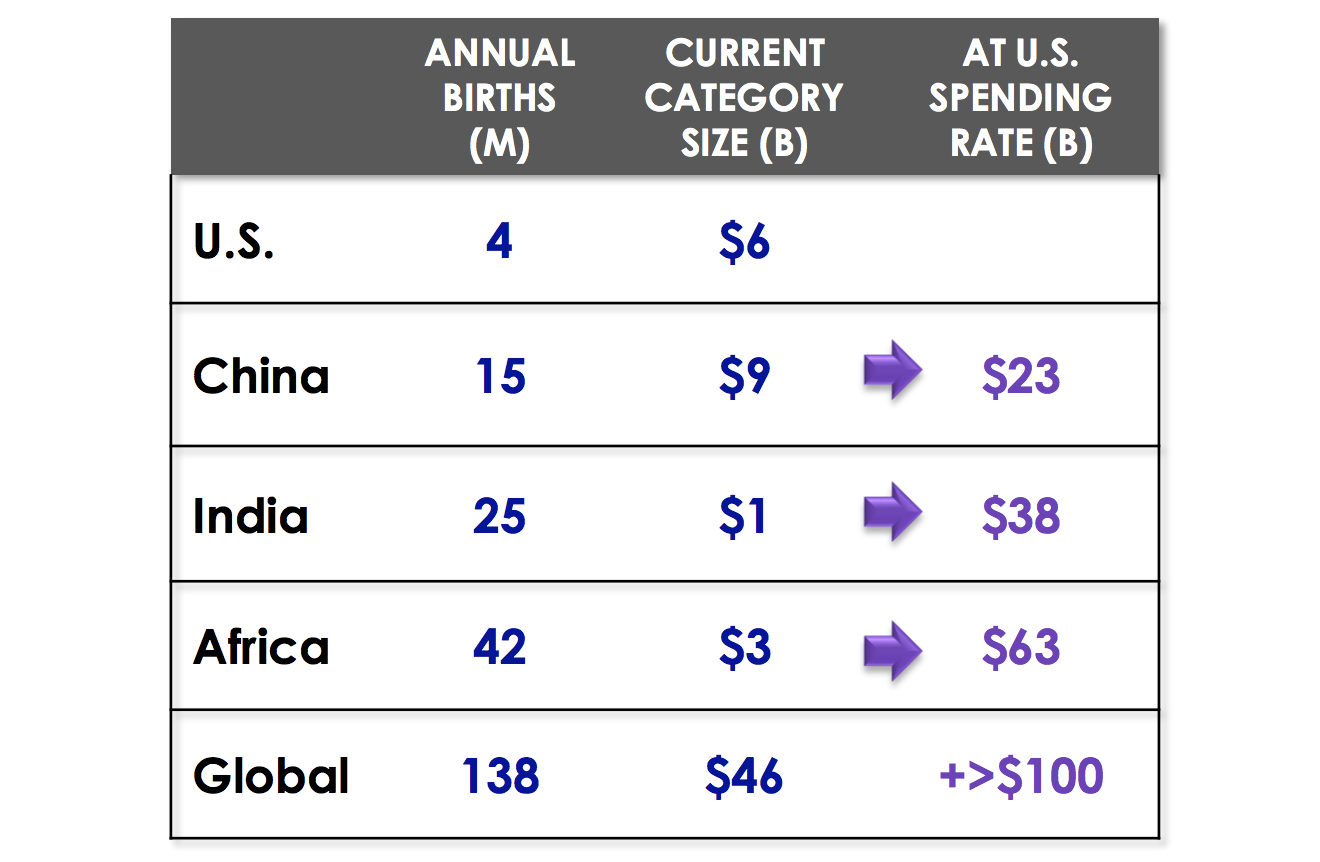

Going forward, Kimberly-Clark is focused on maintaining the strong market share positions of its core brands while accelerating growth in developing and emerging markets, which account for 30% of sales.

Compared to the U.S., birth rates are much higher in developing markets. These regions will likely experience rising consumer wealth over time, increasing the allure of Kimberly-Clark’s products for the growing middle class.

As this plays out, the size of these markets has potential to grow significantly. For example, here's a look at how large the diaper market would be in several developing regions if their spending rate matched America's.

Source: Kimberly-Clark Investor Presentation

Combined with productivity initiatives to remove costs and improve efficiencies, management believes the business can achieve 1-3% annual organic sales growth and mid-single digit EPS growth. Those targets seem reasonable given Kimberly-Clark's historical results and the industry's mature state.

Source: Kimberly-Clark Investor Presentation

Overall, Kimberly-Clark’s business has a strong moat that should allow it to continue generating healthy cash flows and paying safe, growing dividends for years to come. When combined with the company's A credit rating from Standard & Poor's, Kimberly-Clark appears to be a company that is built to last.

That being said, there are a number of challenges the company is facing that could cause it to miss its financial targets.

Key Risks Many of Kimberly-Clark’s products play in the higher quality, higher price tier of the market. This segment can be more susceptible to competition from private label goods (more retailers are pushing back on pricing), upstart rivals using online distribution channels, and low-cost imports if name brands underinvest, the economy weakens, or consumer preferences change.

For these reasons, it is essential that Kimberly-Clark continues advancing its product quality and brand loyalty through new product innovations and appropriate marketing campaigns and packaging.

In North America, a region which generates the majority of Kimberly-Clark's profits, the battle for market share with giants such as P&G is especially tense with America's birth rate falling to its lowest level since the 1980s (people are getting married later and having fewer children).

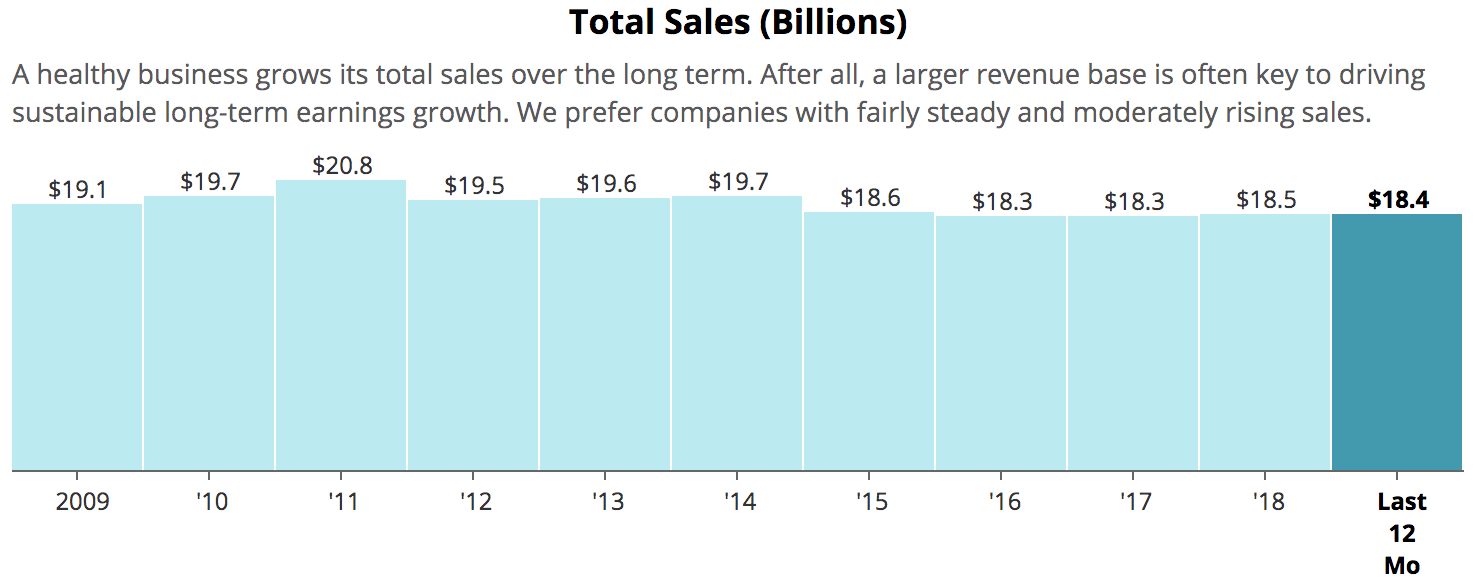

As a result, since 2012 the company has been unable to post better than 1% company-level revenue growth. While much of that weak growth is attributable to selling off commoditized and slower growing business lines, it highlights the fact that Kimberly-Clark's growth struggles are not a new occurrence and may represent "the new normal."

Source: Simply Safe Dividends

Kimberly-Clark's business appears stable today with low-single digit organic sales growth and healthy price increases being pushed through, but low-cost Chinese imports, private label products, and America's declining birth rate could challenge the firm's ability to hit its long-term financial targets in the future.

In the short term, raw material fluctuations and foreign currency exchange rates pose other risks that can disrupt Kimberly-Clark's sales and EPS growth. However, these issues seem unlikely to affect the company's long-term outlook.

Closing Thoughts on Kimberly-Clark Kimberly-Clark is a quality dividend stock. The company has paid dividends for more than 85 years (including 47 consecutive annual increases), and its payout appears to remain very safe with low- to mid-single digit growth potential.

Management's long-term financial targets for the business appear reasonable and very supportive of the dividend as well. While Kimberly-Clark will continue battling a declining birth rate in America and faces intense competition globally, its established market positions, strong brands, timeless products, and excellent balance sheet should keep the business relevant for years to come.

Simply put, Kimberly-Clark continues to possess a number of strengths that make it look like a reasonably appealing holding for a defensive income portfolio.