MetLife (MET): A High-Yield Insurer Paying Uninterrupted Dividends Since 2000

Founded in 1863, MetLife (MET) offers a range of insurance products (life, dental, disability, vision, and accident and health coverages), annuities, employee benefits, and asset management. In total, the company's services are offered in over 50 countries around the world and serve more than 100 million individual and institutional customers.

MetLife operates through five business segments:

U.S: 42% of adjusted earnings

Asia: 21% of adjusted earnings

Latin America: 9% of adjusted earnings

Europe, Middle East: 5% of adjusted earnings

MetLife Holdings: products and businesses that are no longer actively marketed in the U.S., such as certain life insurance products, different annuities, and long-term care insurance: 23% of adjusted earnings.

While the company is globally diversified, the U.S. market remains the most important and fastest growing market. In fact, MetLife is the second-largest life insurance provider in the U.S.

Business Analysis

Insurance companies make money in two main ways. First, they use their expertise in statistics (actuarial data) to attempt to underwrite profitable policies. This can be seen by what's called the combined ratio which shows how profitable the average policy is over time.

For example, a combined ratio of 90% indicates that a company made a 10% return on a policy over its life. A combined ratio of 100% is breakeven, and over 100% means a company lost money on its policies, usually due to either poor underwriting (underpricing its risk), weak internal controls (its statistical models are wrong), or a large catastrophic event.

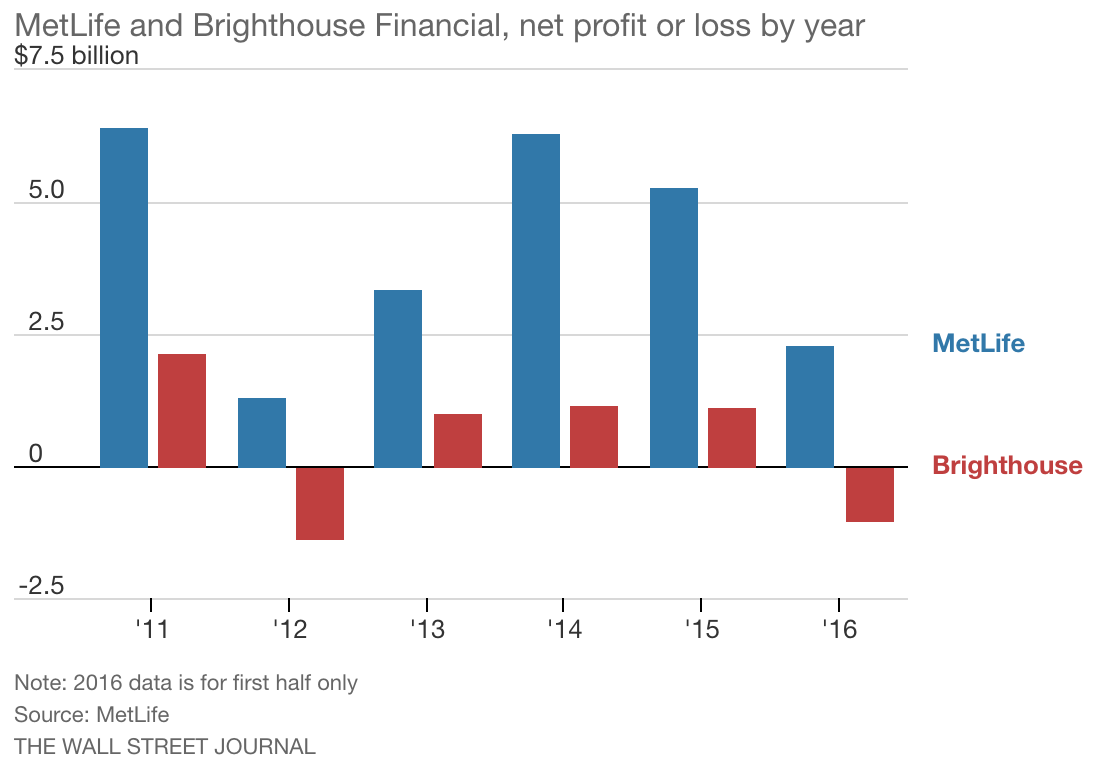

In 2016 and 2017, MetLife reported a combined ratio above 300%, but this was due to tax reform and the spin-off of many U.S. consumer assets into Brighthouse Financial (BHF), which is now a separate company. The company spun off 81% of Brighthouse in 2017 and plans to exit the rest of its position by the end of 2018.

The Brighthouse Financial spin-off was part of management's plan to shift to a less capital intensive business with stronger free cash flow focused more on its core insurance offerings.

Specifically, Brighthouse was mostly a retail-focused insurance subsidiary which means it was less profitable over time due to the fact that it sold insurance to individual customers one at a time (higher cost model), as opposed to the company's new core business which is focused on institutional customers (who buy in bulk).

Per The Wall Street Journal, Brighthouse's slower-growing operations were also weighed down by low U.S. interest rates and a tough market for variable annuities.

Source: The Wall Street Journal

Separating Brighthouse means that investors won't be able to see the long-term profitability of the company's underwriting until 2019, once the rest of Brighthouse is gone and the one-time charges related to tax reform are no longer affecting its financials.

However, looking at some of MetLife's individual unit combined ratios, you can see that the company generally does a good job of underwriting profitable policies:

U.S. life insurance: 87% combined ratio in 2017, long-term goal 85% to 90%

U.S. health insurance: 77%, long-term goal 75% to 80%

Home owner policies: 98%, long-term goal 88% to 93%

From these figures, it's also clear that MetLife's most profitable policies tend to be related to long-term health and life insurance, while its property policies are currently struggling to break even due to the highly competitive nature of insurance.

Management believes that as long as 10-year interest rates (proxy for long-term interest rates) remain between 1.5% and 4%, the firm will continue to be highly profitable and generate healthy and increasingly steady cash flow.

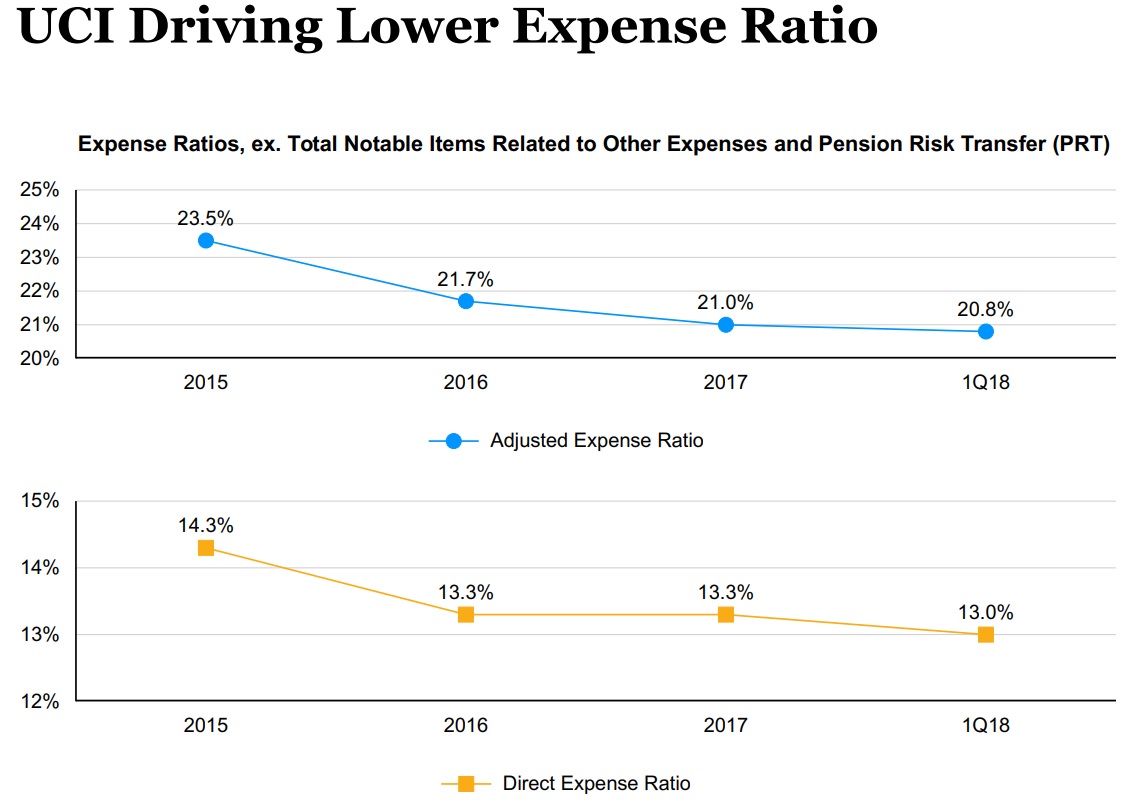

One of the keys to keeping MetLife's profits growing is the company's unit cost improvement (UCI) program. This is a company-wide cost savings initiative that aims to cut annual expenses by $800 million by 2020. UCI has already helped the company significantly drive down the expense ratios on its policies (cost of underwriting and servicing policies divided by premiums).

Source: MetLife Earnings Presentation

Besides the potential for better underwriting profits, the second way insurance companies make money is reinvesting their float, which is excess cash they hold as premiums come in ahead of future payouts.

At the end of 2017, MetLife had a portfolio of $457 billion invested primarily in: investment grade corporate bonds, structured finance securities, mortgage loans and U.S. Treasury and agency securities, as well as real estate and corporate equity.

The insurance business is highly commoditized, with very little material difference between policies. It can also be challenging because companies can only estimate the long-term costs of a policy.

This means that in addition to potentially strong price competition, an insurance company might underprice its risk for years without realizing it, resulting in lower than expected profitability. MetLife does have two competitive advantages that help mitigate these negative factors.

One of the company's advantages over smaller insurance rivals is the firm's substantial sales and customer support forces, which results in a steady flow of new business around the world:

U.S.: 5,500 sales reps, insurance agents, and independent sales people

Asia: 57,500 sales/support agents

Latin America: 12,000 sales/supports agents

Europe, Middle East: 10,900 sales/support agents

This sales and support infrastructure has been built up over more than a century and is something that smaller rivals can't hope to emulate (while still turning a profit).

The other key advantage MetLife has is that, with over 150 years of operations, it has collected some of the industry's most robust data sets, allowing it to fine-tune its actuarial models to maximize the chances of correctly pricing risk.

The larger a company's customer base is, the easier it is to amortize fixed costs (general, administrative, regulatory compliance) as well, resulting in greater profitability. In other words, MetLife's size grants it good economies of scale, which are reflected in the company's adjusted return on equity (excluding one-time restructuring charges) near 13%, its highest level since 2014.

In the past, MetLife has attempted to grow its product offerings via acquisitions, some of which didn't work out and resulted in write-downs. But today Metlife's acquisition strategy looks far more disciplined and focused on more profitable areas of business.

For example, in 2017 the company acquired Logan Circle Partners, L.P. for $250 million. Logan Circle is a fundamental research-based investment manager providing institutional clients actively managed investment solutions across a broad spectrum of fixed income strategies, with more than 100 institutional clients.

Such acquisitions, combined with the Brighthouse spin-off, indicate that Metlife is attempting to move away from lower margin and commoditized insurance products and towards offering higher margin and more specialized financial services for institutional clients.

In addition, in 2013 the company finished selling off its retail banking division which had previously made it a significantly important financial institution (SIFI), meaning stricter capital requirements under the 2010 Dodd-Frank Act. Since then, Metlife has managed to get its SIFI status removed which has greatly lowered its compliance costs, allowed it to increase its leverage, and boosted its overall profitability.

Over the long term, MetLife's international presences (especially in Asia), operational cost cutting (boosting margins), and ongoing share buybacks (2% to 3% per year) seem likely to continue pushing the company's earnings higher. Rising U.S. interest rates on the company's float could also provide upside since it results in greater investment income over time.

However, investors need to realize that there are numerous risks facing the company that might cause its future growth to disappoint.

Key Risks

Insurance companies, by their very nature, are highly leveraged (via float) and complex financial companies whose revenue and earnings can be highly variable over time. There are numerous reasons for this, including the performance of their investment portfolios, regulatory changes, tax changes, insurance claims, and underwriting standard changes.

The life insurance business in particular has been a difficult place to find profitable growth, which is another reason why management decided to spin-off Brighthouse. Here's what Fox Business stated in 2017:

"U.S. life insurers' core business has long been under pressure. Sales of individual policies have been largely flat industrywide for nearly a decade, after falling more than 40% from the 1980s through 2008, according to industry-funded research group Limra.

Low interest rates depress the income insurers earn by investing customers' premiums until claims are paid. They also drive up the cost of hedging annuities' lifetime-income guarantees, and they make it tough to turn profits on products that guarantee specified annual interest."

The insurance industry is also one of the most regulated businesses on earth, with regulations at the local, state, and national levels. For example, the 2010 Dodd-Frank regulations in the U.S. required MetLife to maintain higher capital requirements that lowered the company's ability to profitably invest its portfolio. And with operations in over 50 countries, MetLife is constantly dealing with regulatory changes across its subsidiaries.

In addition, changes in U.S. health insurance regulations (which effect the company's most profitable product line) are a wildcard. Congress is frequently proposing regulatory changes, and at times sweeping industry changes (such as ObamaCare), that can create large uncertainties surrounding compliance costs and future profitability of U.S.-based health insurance policies.

Much of insurance regulation applies to operators' capital requirements, which can swing significantly depending on interest rates. That's because most insurance assets are represented by float held in Treasury bonds, whose value on the balance sheet is highly sensitive to interest rates.

In other words, the value of MetLife's portfolio (and its capital levels) are impacted not just by long-term rates in any individual country, but often the difference or spread between short-term rates and long-term rates across numerous countries.

Source: MetLife Investor Presentation

And with close to 60% of its adjusted earnings coming from overseas, MetLife's also has significant currency exposure.

When the U.S. dollar appreciates against local currencies, MetLife's reported foreign sales and earnings can decline, creating growth headwinds. This is especially notable in emerging markets such as Latin America, where short to medium-term currency swings of 10% to 30% are not unheard of.

Source: MetLife investor Presentation

In addition, due to the complex nature of attempting to offer so many long-term insurance policies, sometimes a company determines that its capital reserves are insufficient.

In early 2018, MetLife revealed that due to what turned out to be weaker internal controls on its past underwriting, the firm's pension and annuity liabilities had turned out to be understated and will require additional capital reserves. For example, annuities will require a $500 million one-time capital infusion.

These internal weaknesses triggered a company-wide review of its underwriting and financial modeling which management believes still leaves MetLife on track to achieve its $800 million in cost improvements by 2020 via its UCI program.

Source: MetLife Earnings Presentation

While Metlife's financial restatements and increased capital allocation to these specific insurance products isn't likely to significantly change its long-term investment thesis, it does highlight how complex insurance liability modeling can be. Even a company with over 150 years of experience in the industry can find itself making mistakes, including future ones that might prove more costly.

Finally, with the Brighthouse Financial spin-off being completed in 2018, MetLife's short-term earnings could take a hit and represent a temporary growth headwind. That's because Brighthouse represented about 21% of the company's 2017 earnings, which means that it will take several years to grow out of that one-time dip in the bottom line.

This might be why MetLife's dividend increase of 5% earlier this year is so much lower than its recent five-year average growth rate of 17%. In the past MetLife has managed to preserve its dividend over time, but there have been multi-year stretches where the dividend didn't grow at all. As a result, investors looking for the assurance of annual income hikes might want to look elsewhere.

Closing Thoughts on MetLife

A well-run insurance company can be a decent source of consistent dividend growth. As one of the world's largest insurers with over a century of operating history, MetLife benefits from its substantial sales force and some of the most in-depth actuarial tables around.

This helps the firm maximize its chances of profitable underwriting over time, which combined with a more conservative investment strategy for its large float should allow for steadier earnings and dividend growth.

That being said, the insurance industry is extremely complex and thus not for everyone. Any investor wanting exposure to this industry needs to be well aware of its highly regulated, leveraged, interest rate-sensitive, and variable nature (at least in the short to medium term).