Can W.P. Carey's Dividend Withstand Higher Rates, Office Weakness?

Over the past year, W.P. Carey's share price has slumped nearly 20%, resulting in the REIT's dividend yield surpassing 6% and reaching its highest level since the beginning of the pandemic.

Some investors might be wondering what's causing this disappointing short-term performance and whether W.P. Carey's dividend remains safe.

While it's not always clear why a stock has underperformed in a given year, higher interest rates and office exposure are the most likely factors weighing on W.P. Carey.

However, we don't expect either issue to threaten the REIT's dividend or long-term outlook.

W.P. Carey has entered this period of rising rates with a solid balance sheet and financial flexibility.

In fact, S&P upgraded W.P. Carey's credit rating to BBB+ in January citing the REIT's above-industry average operating performance, heavy exposure to recession-resistant properties, and solid liquidity that should provide a path for W.P. Carey to manage its upcoming debt maturities.

Source: W.P. Carey Investor Presentation, April 2023

We agree with S&P's assessment. The firm appears well-positioned to navigate tighter credit markets. It has a steady cash flow stream supported by leases that include rent escalators. And around 60% of these leases are CPI-linked, which helps offset increasing borrowing costs.

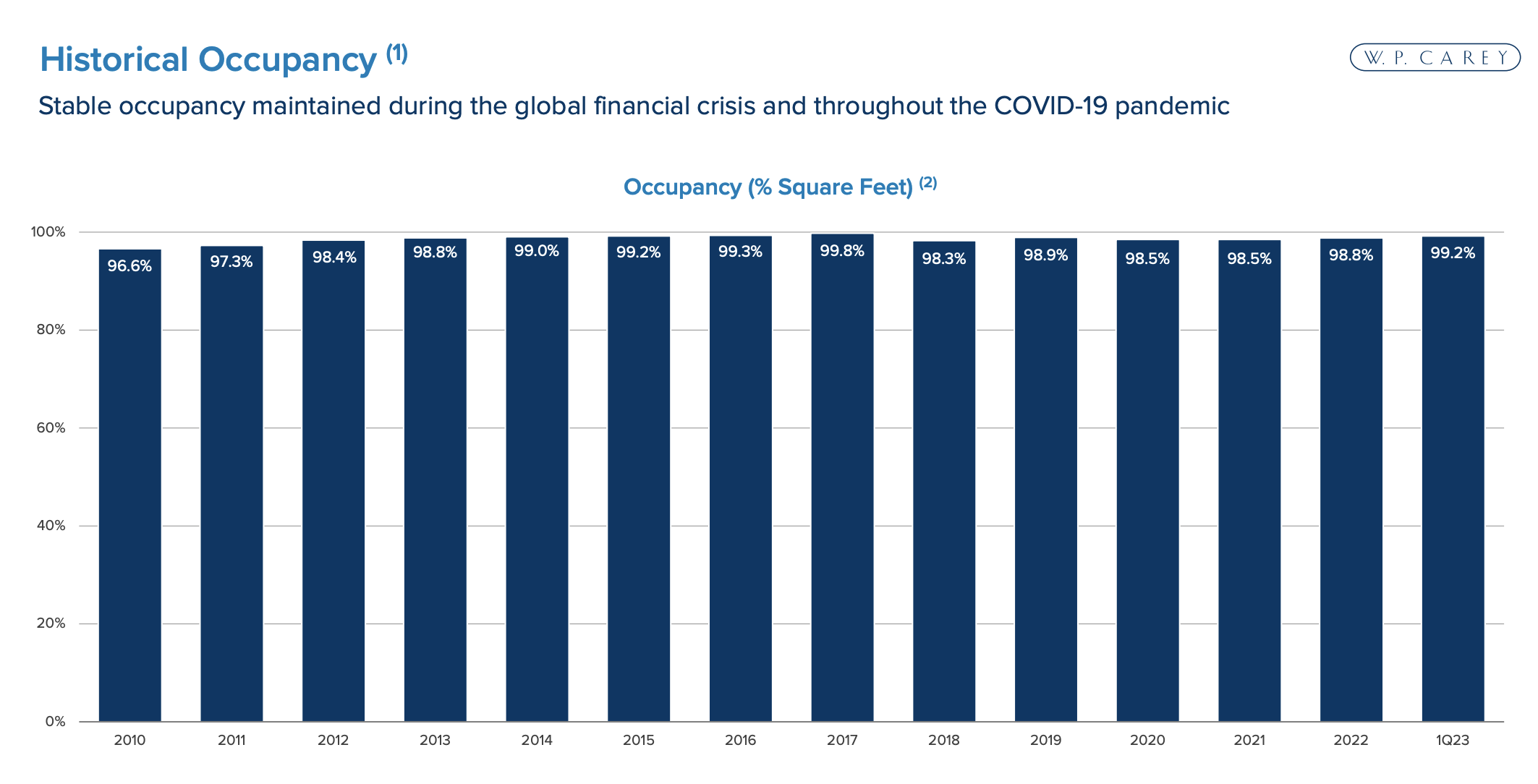

W.P. Carey also boasts a 99% occupancy rate for its portfolio of over 1,400 net-leased properties focused on industrial (27% of rent), warehouse (24%), retail (17%), office (17%), and self-storage (5%) markets.

Source: W.P. Carey Investor Presentation, April 2023

The diversified REIT's disciplined approach to investing in essential properties and selecting creditworthy tenants has helped the firm maintain strong occupancy, including during the depths of the pandemic in 2020.

This selective strategy and the firm's long-dated lease terms (~11 years on average) are also insulating W.P. Carey from remote work pressures that affect many office landlords.

While the challenges for offices are unlikely to fade anytime soon, the firm had already begun pivoting away from the troubled industry before the pandemic.

Over the past six years, W.P. Carey has meaningfully reduced its office exposure from over 30% of total rent to 17% today – a percentage management expects to decrease further as it attempts to dispose of more office buildings in the years ahead.

As such, concerns over the firm's office exposure may be overdone and should fade as the REIT shifts further away from this industry.

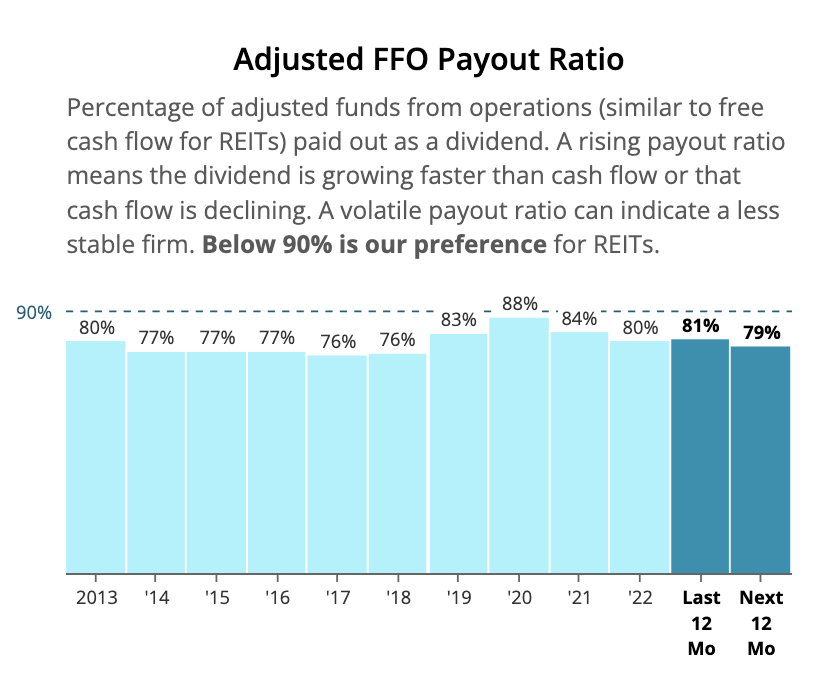

Even if W.P. Carey succumbs to some of these pressures, we estimate that if the firm lost half of its cash flow from office properties, an extreme scenario, the REIT's payout ratio would remain below 90%.

Given the firm's favorable lease structures, high occupancy, solid balance sheet, and exposure to recession-resistant tenants, we are reaffirming W.P. Carey's Safe Dividend Safety Score.

Source: Simply Safe Dividends

Overall, while we view W.P. Carey's refinancing needs and office exposure as concerns worth monitoring, we don't believe they will impact the firm's long-term trajectory, aside from more subdued dividend growth in the next few years.