Tyson Foods has tempered its near-term outlook as the costs of raising and securing cattle (~35% of sales), chickens (30%), and pigs (10%) remain elevated while inflationary pressures are leading consumers to shift their meat-buying habits – particularly with lower demand for beef, the firm's historically more profitable segment.

Seemingly, a perfect storm of economic and weather-related challenges has engulfed the nation's largest meat producer, raising concern among investors as the company's stock price has fallen more than 40% over the past year.

These broad challenges affect each of the firm's core protein categories, leading Tyson's CEO to remark, "I've never seen this highly unusual situation where beef, pork, and chicken were all experiencing challenges at the same time."

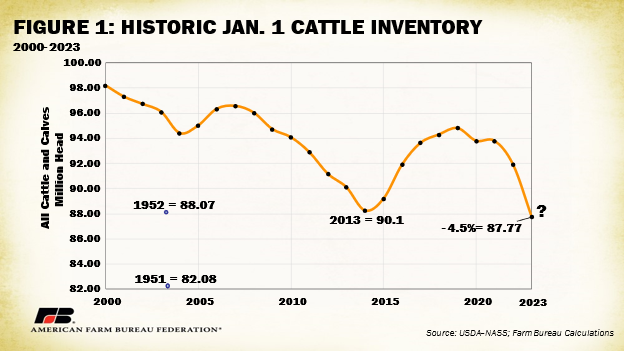

Years of persistent drought conditions have restricted farmers' ability to grow sufficient cow feed (alfalfa, corn, etc.), and natural vegetation in pastures and grazing lands has become less abundant.

Consequently, ranchers adjusted to these conditions by slaughtering more cows than expected and breeding fewer calves – shrinking the cattle supply to its lowest level in over a decade and, in turn, elevating prices.

Source: American Farm Bureau Federation

Pushing cattle prices even higher were record production costs up almost 20% last year, according to the American Farm Bureau Federation.

As beef costs have risen, consumers have shifted consumption from higher-priced cuts like steak to cheaper protein alternatives.

This one-two punch is squeezing Tyson's beef margins, which may remain under pressure for at least a few years. Farmers will likely wait for drought conditions and production costs to improve before expanding herds, and from that point, it will take about two years for new calves to become available for consumption.

In contrast, Tyson's second-most important meat, chicken, has had an oversupply problem the last six months or so that has driven down consumer prices – while the costs to produce chickens (food and labor) remain stubbornly high.

Fortunately, raising broiler chickens (those grown for meat consumption) takes only six to eight weeks, so adjusting supply is a less lengthy problem. And demand for chicken will likely increase as consumers shy away from higher beef costs.

Tyson's management team expects margin improvements from chicken in the back half of this year from supply stabilization and the firm's efficiency and automation efforts (fewer labor inputs).

Finally, pork, Tyson's third staple protein, is also battling an oversupply problem following years of increased domestic production aimed to fill the void created by the massive 2018 African swine fever outbreak in China, the world's largest pork consumer.

But China has been importing fewer hogs as the country's pork production recovers, and U.S. consumption has remained stagnant.

As with chicken, pork is dealing with a supply and demand imbalance that, in conjunction with higher production costs, has reduced profit margins.

Collectively, the challenges faced by each core protein have led Tyson to significantly lower its profit expectations for the year and will push the firm's payout ratio to an unprecedented level.

Source: Simply Safe Dividends

Meanwhile, S&P recently revised its outlook on Tyson's BBB+ credit rating to negative from stable, citing the uptick in leverage that has resulted from the firm's pressured earnings and elevated-but-peaking investments in capacity expansion and automation.

Source: Simply Safe Dividends

In recognition of Tyson's challenging headwinds and pressured payout ratio, we are downgrading the firm's Dividend Safety Score within our Very Safe bucket from 99 to 90.

Although Tyson will likely continue battling margin pressures over the next year or so, animal protein remains a regular part of the American diet, and the long-term outlook remains strong.

Supply should eventually stabilize and promote healthier pricing, and global demand for high-protein and more convenient meat will keep growing with the expanding middle class outside of the U.S.

Producing roughly one out of every five pounds of beef, chicken, and pork sold in the U.S., Tyson also enjoys an entrenched market position, a broad distribution network, and economies of scale that will help the firm ride out this current cycle.

Coupled with a more stable prepared foods segment (25% of income) and an investment-grade credit rating, we believe Tyson is still deserving of a solid Dividend Safety Score.

Conservative investors who believe in the firm's long-term outlook may find now an interesting time to consider the stock, which sports a dividend near its highest level since the depths of the pandemic.

Source: Simply Safe Dividends

For the last decade, Tyson has raised its payout in the third quarter of each year. Because the firm's current challenges seem transitory, we expect the firm will continue that cadence by increasing the dividend by a mere penny – or roughly 2% – later this summer.

While we've reaffirmed our long-term outlook for Tyson, we know these economic disruptions could last longer than anticipated. If that proves to be the case, we would consider downgrading the meat producer's Dividend Safety Score again.

As such, we will closely monitor Tyson and the outlook for beef, providing updates as needed.