How Safe is Blackstone Mortgage Trust's (BXMT) High Yield?

With roots tracing back to 1966, Blackstone Mortgage Trust (BXMT) is one of the largest commercial real estate mortgage REITs (mREITs). The firm is externally managed by BXMT Advisors, a subsidiary of Blackstone Group (BX), a world leader in real estate development and investment.

BXMT itself has $120 billion in real estate assets under management (AUM), but Blackstone Group is far larger with $450 billion in AUM across its various investment vehicles which are focused on: private equity, real estate, public debt and equity, and bonds. Management is provided by Blackstone Group in exchange for a 1.5% base management fee (on equity) and a 20% cut of earnings growth (above a 7% hurdle rate).

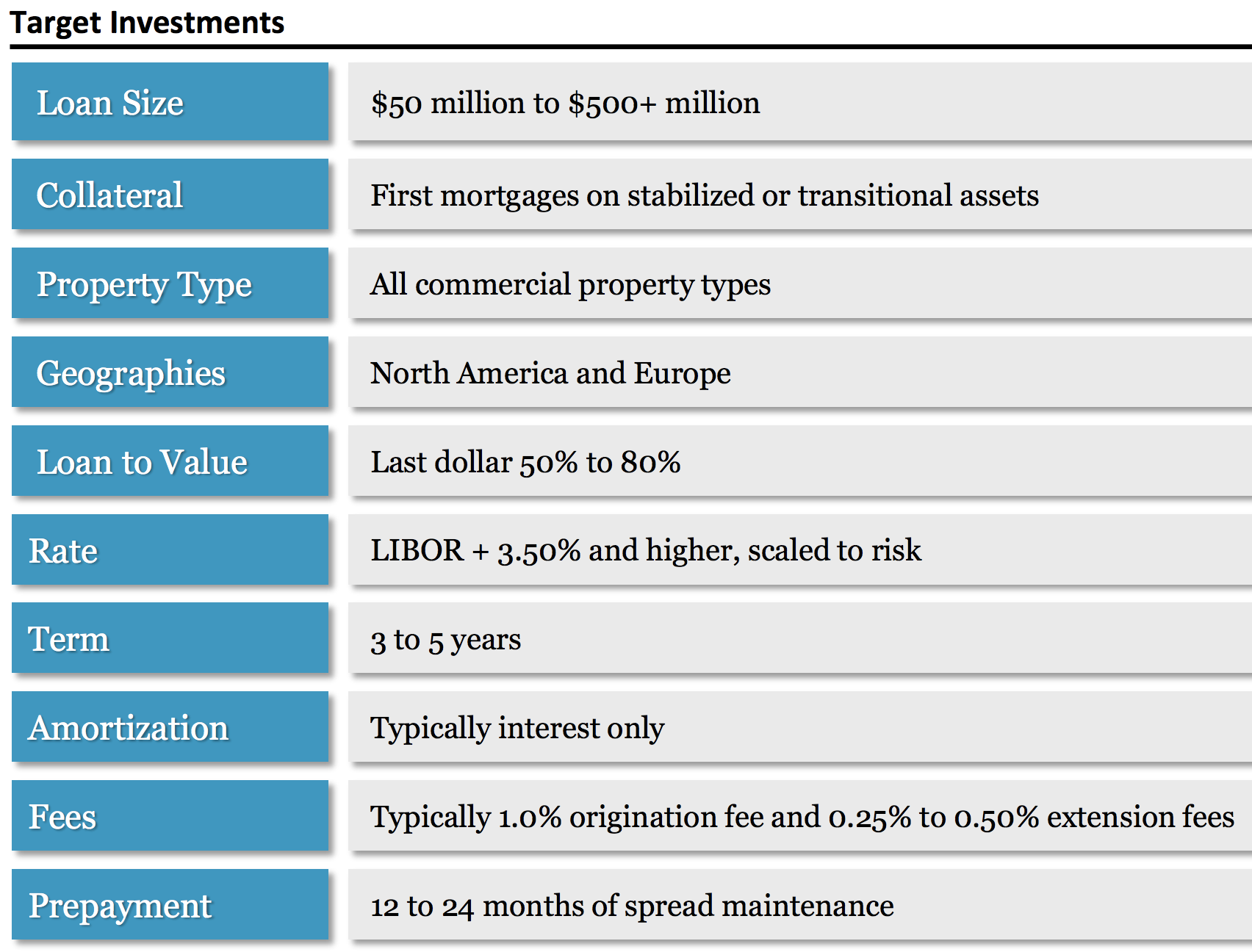

Blackstone Mortgage Trust specializes in 100% senior secured commercial real estate loans, mostly for the construction of new commercial buildings in North America and Europe.

While the firm is diversified geographically, nearly half of Blackstone's commercial mortgages are to companies constructing office buildings. Its loans are almost all floating rate (variable interest rate), tied to the London Interbank Offer Rate (LIBOR), the international commercial lending standard.

Source: Blackstone Mortgage Trust Investor Presentation

Blackstone Mortgage Trust makes money by borrowing at lower interest rates (also indexed to LIBOR) and lending at higher rates, with contractually obligated interest rates that rise if global commercial interest rates do. The difference between its borrowing costs and lending rates is what generates its core earnings.

Unlike equity REITs, which own commercial real estate properties that generate rental income, mortgage REITs tend to be financial companies who own little to no physical assets.

Rather they are pure financial companies, providing funding to various aspects of the real estate market. In addition, all of their assets (loans) are usually short-term in nature (average of 3.7 years), meaning that Blackstone Mortgage must constantly make new loans to replace maturing ones that roll off its balance sheet.

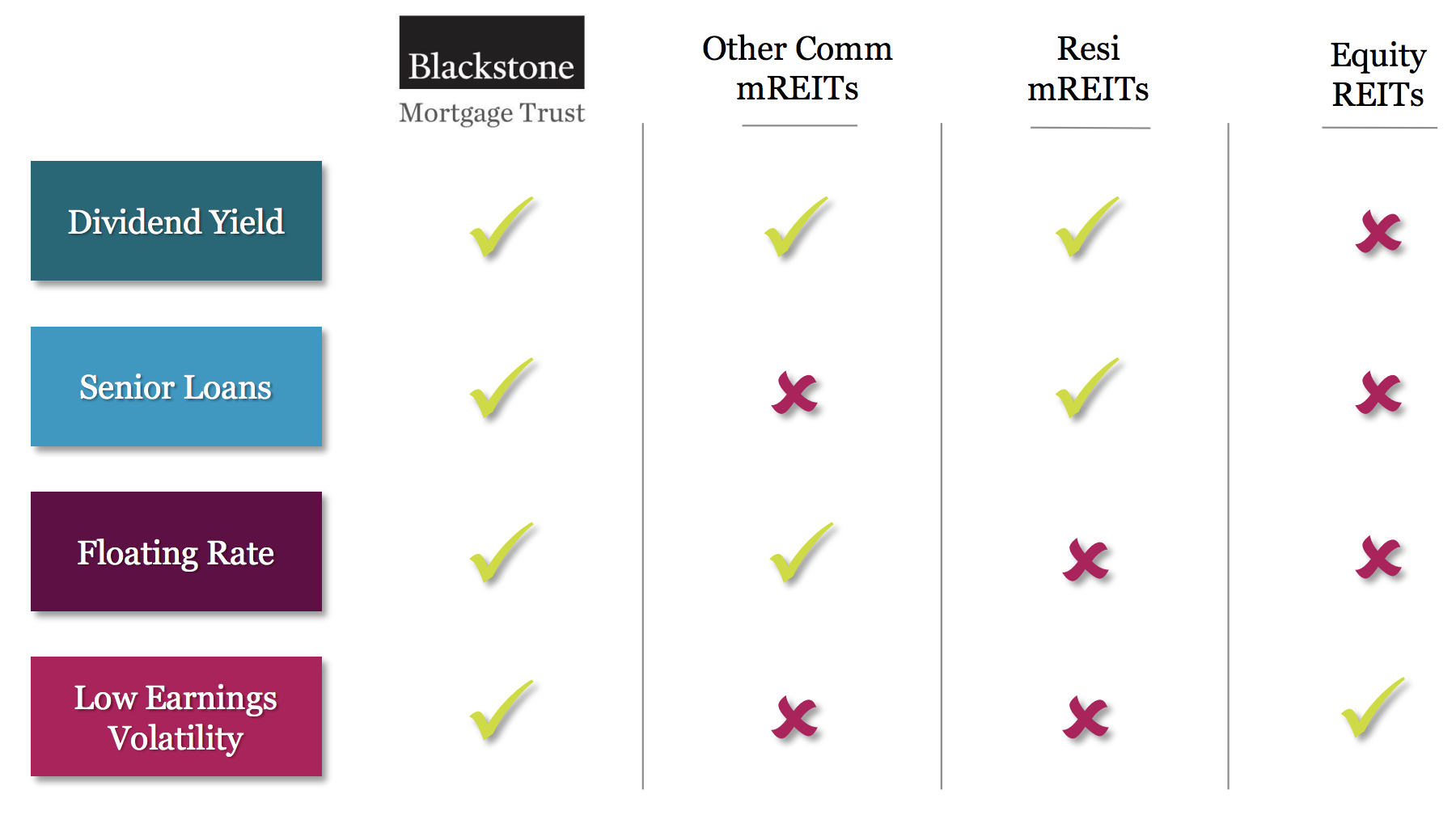

In the case of commercial mREITS like Blackstone Mortgage, the funding is for floating rate senior mortgage loans used to construct new buildings. While the commercial mREIT industry can be highly complex (as are mREITS in general), Blackstone Mortgage is one of the simplest business models to understand.

That's because unlike some of its peers, Blackstone Mortgage Trust is a "pure play" commercial mortgage lender. In other words, it earns 100% of its revenue and core earnings from senior mortgage loans to commercial builders rather than through monetizing its loans by selling pieces of them to others, or servicing commercial real estate loans.

Source: Blackstone Mortgage Trust Investor Presentation

The mREIT industry is inherently a "no moat" business, meaning there are no barriers to entry. However, Blackstone Mortgage Trust has an advantage over most of its smaller peers thanks to its affiliation with Blackstone Group.

That's because Blackstone Group operates globally and has extensive industry knowledge, strong access to numerous funding channels (banks), and enormous deal flow. This allows Blackstone Mortgage Trust to obtain relatively lower cost capital to fund larger and more profitable commercial mortgages (due to economies of scale).

However, competitive financing costs are only part of the equation. Due to the highly leveraged nature of commercial mortgage lending (Blackstone Mortgage Trust's debt/equity ratio is 2.3), risk management is paramount.

Blackstone Mortgage Trust operates a relatively low risk business model (for being an mREIT) in several ways. First, its loan-to-value (LTV) ratio is relatively low indicating that its customers are making large down payments on its mortgages.

In addition, because its mortgages are all senior debt, this means that in the event of a default Blackstone Mortgage Trust is first in line to recoup its investment. In most cases, that means reprocessing and selling the property its capital funded the construction of. Having a low LTV ratio means that Blackstone's potential to book a large loss on a loan is smaller, assuming it can get a good price for the property it sells.

The final risk mitigation factor is management's expertise, which allows the firm to more easily sell repossessed properties and mitigate any loan losses. For example, Blackstone Mortgage has a proprietary risk rating system that ranks all loans from 1 (low risk of loss) to 5 (high risk of loss). The average loan rating per this system is 2.7 with no loans below 3 (average risk of loss).

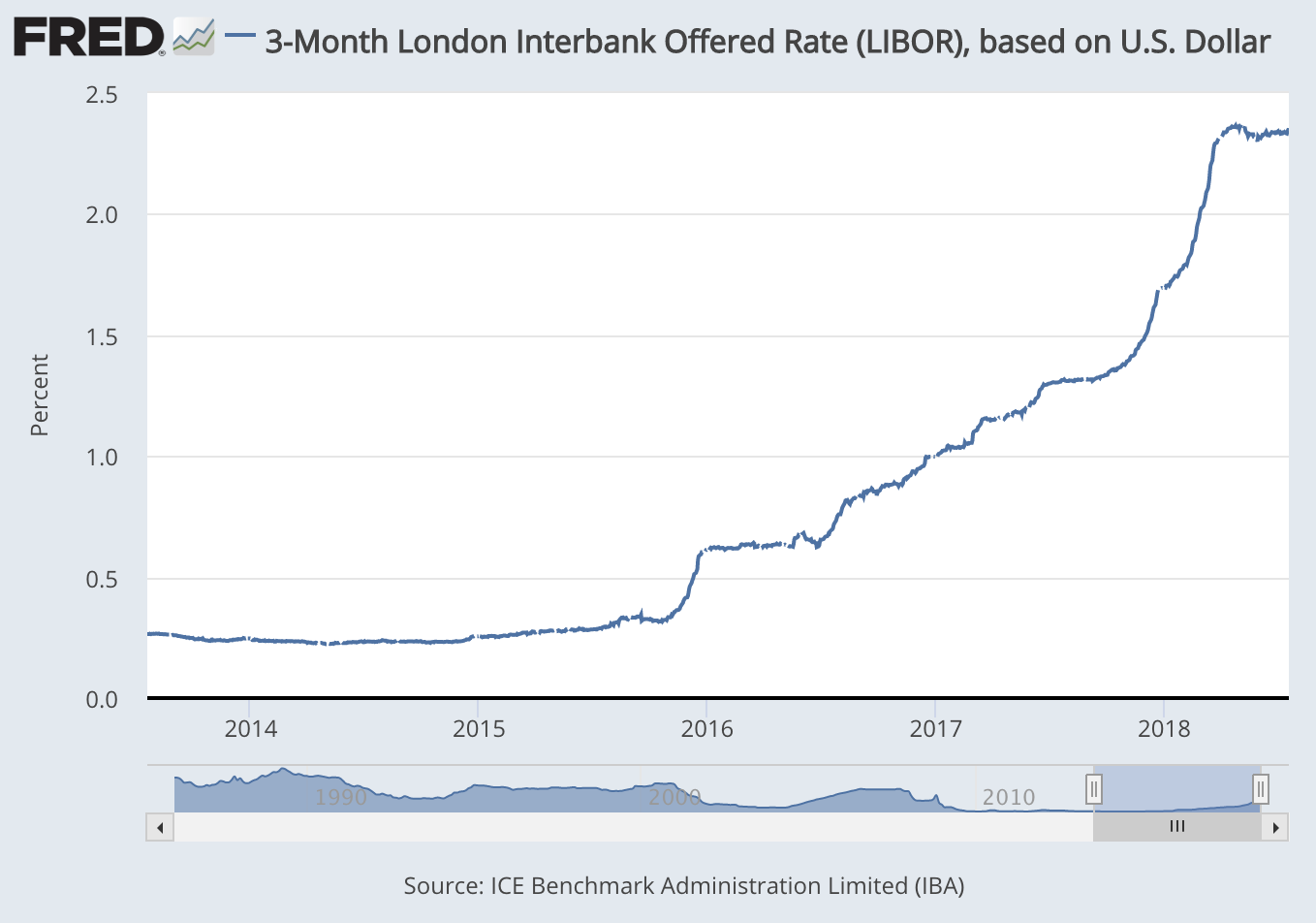

In recent years Blackstone Mortgage has benefitted from a cyclical boom for all commercial lenders, driven by the second longest economic expansion in U.S. history. In addition, accelerating global growth caused LIBOR rates to rise significantly, boosting profitability of all commercial mREITs. For example, the 3-month LIBOR, which sets the mREIT's borrowing and lending rates, is up 130 basis points in the past year.

Source: St. Louis Federal Reserve

On average, Blackstone Mortgage Trust lends to customers at LIBOR + 5.8%, which is why management estimates that for each 1% increase in LIBOR, its core EPS will rise by $0.24 annually, or 9%.

In general, economic growth and expanding commercial real estate will likely help Blackstone Mortgage Trust grow its core EPS and dividend at around a mid-single-digit pace over the long term.

However, investors need to be very careful to understand that Blackstone Mortgage Trust's business model is highly cyclical. The company also faces numerous challenges that make it a poor choice for low-risk income investors.

Key Risks

Like almost all mREITs, Blackstone Mortgage is externally managed, meaning that there is the risk of a conflict of interest between shareholders and management. Specifically, management fees are not based on a per share basis, but on absolute amounts. Therefore, the mREIT has an incentive to grow for growth's sake, even if doing so won't necessarily increase core earnings per share, dividends per share, or book value per share (what the share price generally tracks).

For example, in the first quarter of 2018 management fees totaled $15.5 million, consuming 22% of the mREIT's revenue. This high intrinsic cost structure (present in all externally managed mREITs), combined with the fact that 90% of taxable income must be paid out as dividends (by law), creates meaningful long-term growth challenges.

Over the past five years Blackstone Mortgage Trust's revenues have grown over 300%, book its book value (net asset value) per share has increased just 9%. This is due to the large number of shares the company must frequently issue to raise growth capital (share count up over 275% in past five years). In fact, despite growing its loan portfolio by 15% in the first half of 2018, Blackstone Mortgage's book value per share remained about flat (increasing from $26.93 to $27.08).

This rising share count dilutes existing investors and creates large equity sensitivity. All REIT investors need to realize that these businesses can only grow their dividends if their cash flow (or in this case core EPS) grows over time.

However, that requires being able to issue accretive equity, meaning that shares are priced high enough to increase cash flow per share. For mREITs the key to accretive (profitable) equity raises is that the share price must be above an mREIT's book value per share.

If it is not, then each new share sold to grow the loan portfolio will actually decrease the value of the mREIT. mREITs are usually priced off book value which means that if the share price isn't high enough, then investors won't actually benefit from an mREIT's growth in terms of: rising book value per share, core EPS, and most importantly dividends.

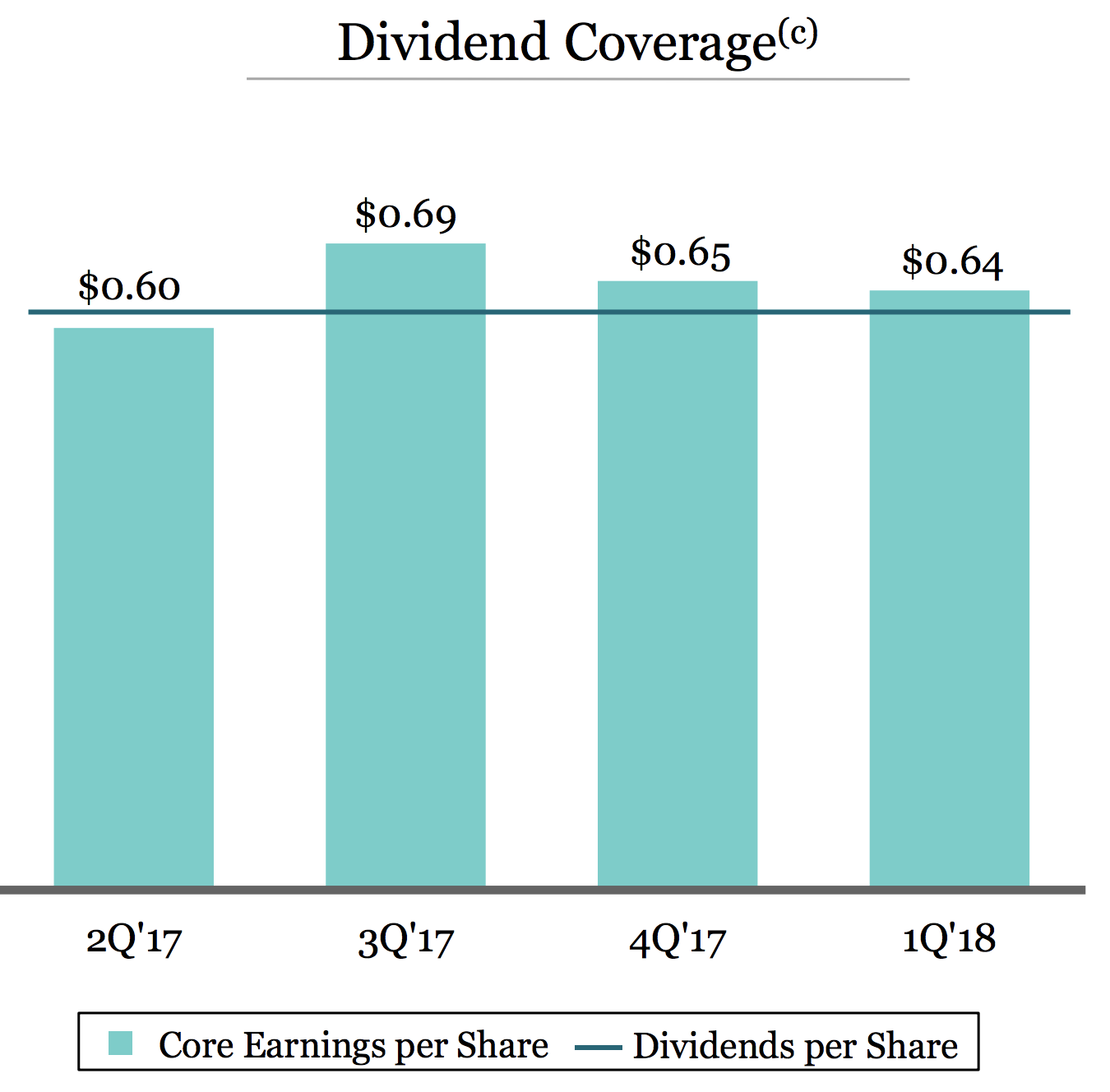

Blackstone Mortgage's price-to-book value is currently about 1.2, which means it can raise equity growth capital at slightly profitable levels. However, this is still heavily dilutive (premium isn't very high) so each new share raises its dividend expense and results in Blackstone Mortgage Trust maintaining a very high dividend payout ratio.

Source: Blackstone Mortgage Trust Investor Presentation

This is largely why Blackstone Mortgage's quarterly dividend, while frozen at 62 cents per share since late 2015, remains high risk. With a payout ratio hovering around 90%, there is little safety cushion should industry conditions worsen. It should be noted that most mREIT's have 95% to 100% payout ratios, meaning that a lack of a safety cushion is inherent to the entire industry's business model.

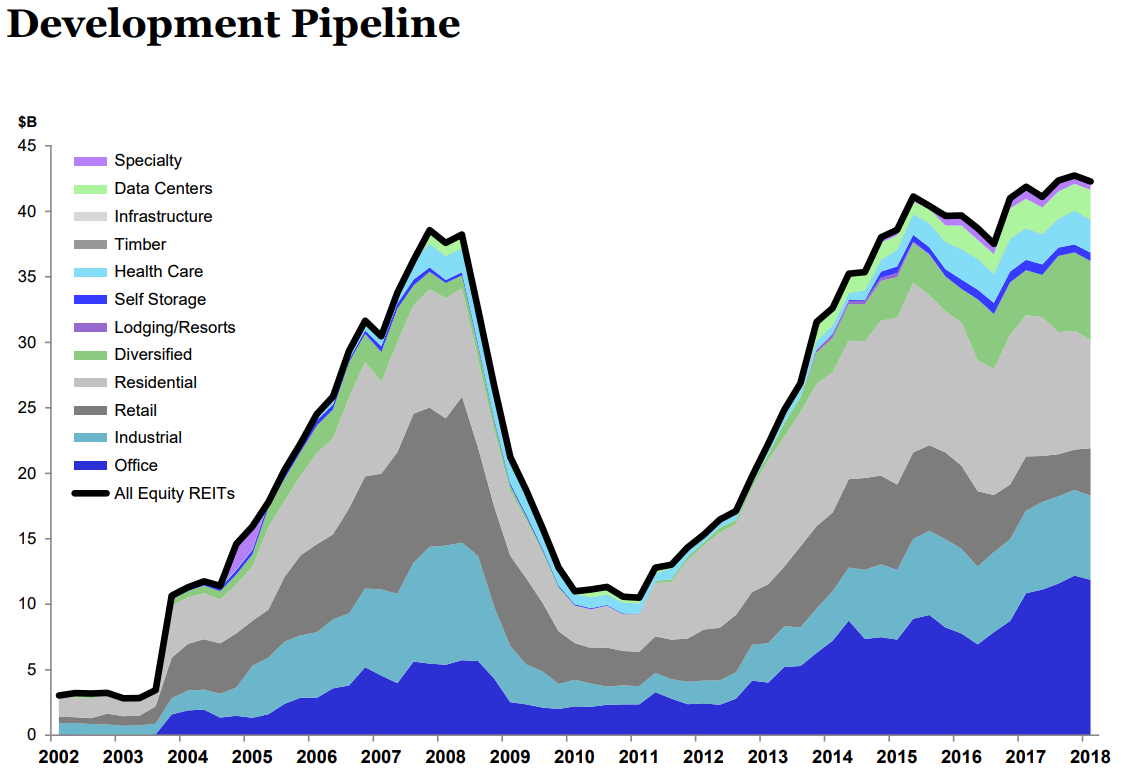

Remember that Blackstone Mortgage has also benefitted from over nine years of steady economic growth and strong commercial real estate markets created by demand outstripping supply. This was caused by the collapse of commercial real estate lending during the financial crisis, followed by an eventual boom in construction.

As you can see, now commercial real estate lending is robust, and commercial real estate developers are aggressively investing in capacity expansion.

Source: NAREIT

This threatens to result in lower rental growth for developers even if the economy remains robust and growing as it is now. And if the U.S. (and Europe) were to experience a recession, then distressed commercial lenders are likely to end up defaulting on their mortgages, hurting Blackstone Mortgage Trust's core EPS and threatening its dividend.

Furthermore, the value of commercial real estate falls during economic downturns, meaning that even Blackstone Mortgage's senior loans and low LTV ratios might not protect its earnings much.

Ultimately, this means that Blackstone Mortgage Trust, like most mREITs, is a fair weather high-yield stock. When the economy is doing well and rates are rising, it can generate sufficient core EPS to (barely) cover its attractive dividend.

However, during recessions no mREIT has thus far been able to maintain its dividend over time. In fact, during the financial crisis Blackstone Mortgage not just lowered its dividend but suspended it entirely in 2008. Not until 2013 did it reinstate regular quarterly dividends.

The result of this dividend variability is extreme price swings. For example, during the financial crisis, when Blackstone Mortgage suspended its dividend, the firm's share price fell 97% from its all-time high. While a future recession is likely to be less extreme than what we saw during the Great Recession, the point is that Blackstone Mortgage represents a very high risk of a large loss of capital during economic and industry downturns.

But what about rising commercial lending (LIBOR) rates? Won't that help boost Blackstone Mortgage's core EPS, increase dividend safety, and even potentially allow it to grow?

While that is one possibility, there is no guarantee that LIBOR will keep rising; no one can predict how fast or how long global economic growth will continue, much less the direction of interest rates.

Even if Blackstone Mortgage is able to grow its core EPS impressively, its payout ratio is likely to remain near 100% and its dividend high risk since by law it must pay out almost all earnings as dividends.

Therefore, while Blackstone Mortgage Trust is arguably one of the simplest and best-managed commercial mREITs, the stock remains a poor choice except for all but the most risk tolerant investors. And even they might want to ask themselves if any yield that is likely to be cut substantially during the next recession (or potentially eliminated entirely) is high enough to compensate them for the risks built into Blackstone Mortgage Trust's business model.

Closing Thoughts on Blackstone Mortgage Trust

The mREIT industry is nothing like the REITs that most investors are used to. These purely financial companies own no physical assets, have externally managed structures (with conflicts of interest), and pay dividends that are likely to be variable over full economic cycles (fall during recessions).

With that said, commercial mREITs like Blackstone Mortgage Trust are superior to residential mREIT cousins (like Annaly Capital) because they enjoy fixed lending spreads and benefit from strong economic growth and rising interest rates. And Blackstone Mortgage Trust in particular enjoys some of the industry's best deal flow and profitability thanks to its affiliation with Blackstone Group.

That being said, Blackstone Mortgage Trust's business model makes it an inherently high-risk dividend stock. One that's likely to have to cut its payout during a recession. Therefore, the stock should probably only be considered by the most risk tolerant investors who are comfortable trying to time an exit before the next recession hits (no one has a crystal ball here).

Put another way, mREITs like Blackstone Mortgage Trust are not good "buy and hold" income investments to own across the entire economic cycle.