Stanley Black & Decker's Dividend Remains Secure Despite Supply Chain, Inflation Challenges

Stanley Black & Decker has paid uninterrupted dividends for 146 consecutive years, a streak we expect will continue despite a handful of macro headwinds that have sent shares of the world's largest tool maker slumping over 40% in 2022.

With many Asia-based production plants located far from big-box retailers and other customers, Stanley's sprawling footprint has exposed the company to numerous supply challenges and surging transportation costs.

Meanwhile, steel, plastic, batteries, semiconductor chips, and other components represent critical inputs for the company's tools. Prices for these materials have also surged, with some components such as lithium-ion battery cells used in cordless power tools proving hard to source.

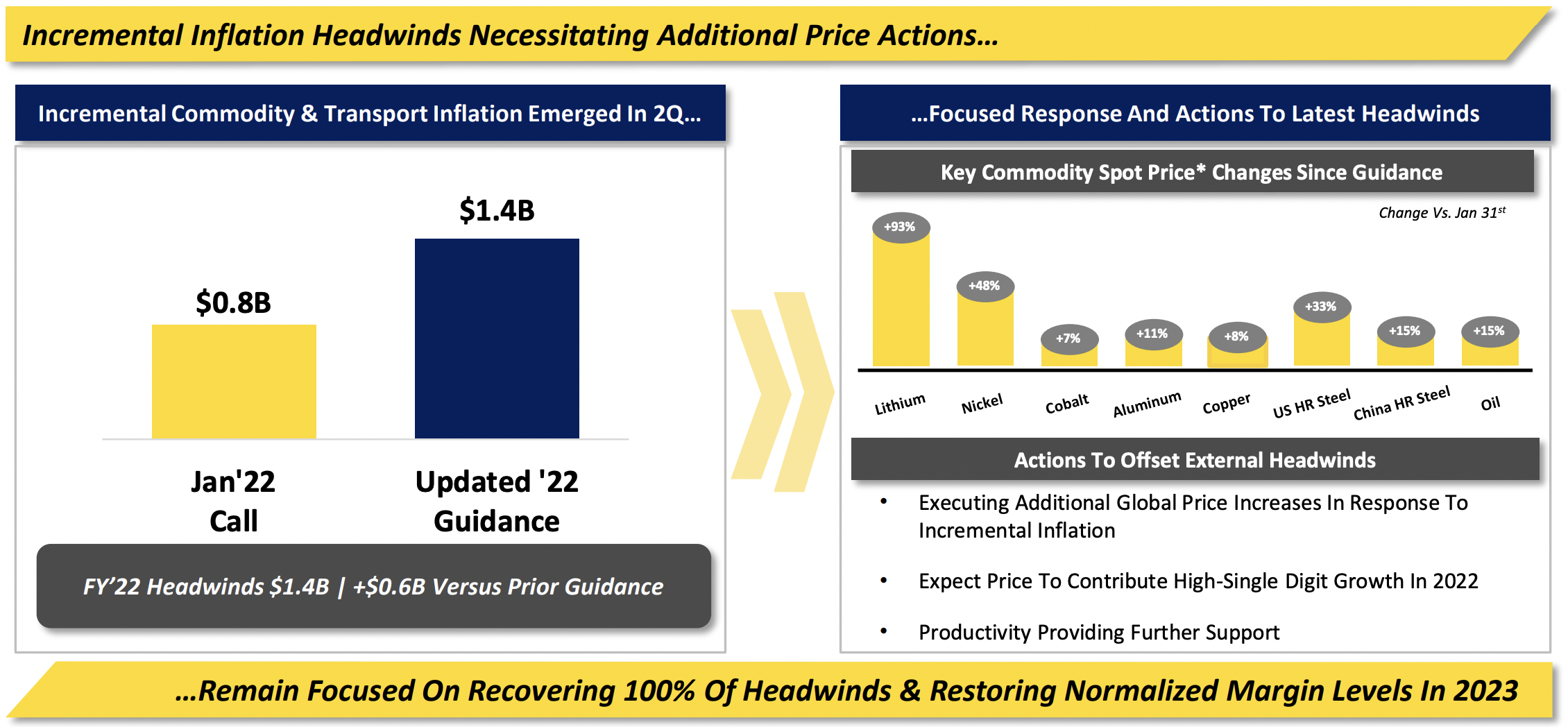

In total, management in April nearly doubled the firm's expected full-year incremental cost from commodity and transportation inflation to $1.4 billion. For context, Stanley's annual free cash flow over the past three years has averaged around $1 billion.

Source: Stanley Black & Decker Investor Presentation

Stanley is addressing supply challenges by adding some capacity closer to end customers and co-investing with certain sourcing partners. These initiatives should result in more efficient transportation and ensure Stanley has adequate product to meet long-term demand.

The company also expects pricing to contribute high single-digit sales growth in 2022. Along with productivity improvements to reduce costs, these actions are intended to return Stanley to historical margin levels in 2023.

However, the near-term outlook will likely remain choppy as inflation persists and certain end markets slow. For example, rising interest rates and surging construction costs are cooling the U.S. housing market, which drives nearly 30% of Stanley's sales.

With many large retailers already struggling with elevated inventory levels, a decline in demand for tools used in home construction and renovation projects could cause key distributors such as Lowe's and Home Depot (30% of Stanley's sales combined) to pull back on orders.

Stepping back, we do not believe any of these issues materially impact Stanley's dividend safety profile or long-term outlook.

Stanley's free cash flow should rebound over the next year to comfortably cover the dividend going forward, and the firm's healthy balance sheet, including an A credit rating, provides flexibility to weather unexpected downturns.

We expect Stanley to raise its dividend in July for the 55th consecutive year, likely at a low-to-mid single-digit pace.

Dividend growth could pick up in future years as Stanley looks to get back on track with its long-term financial goals, which call for 10% to 12% annual sales and earnings per share growth.

The markets for tools, handheld outdoor equipment, and fasteners are very large and fragmented, providing Stanley with a long runway to grow organically and through acquisitions of complementary products.

Stanley's growth potential is further strengthened by the firm's increasing presence in emerging markets and ability to manufacture more electrified products, which seem likely to take share in outdoor equipment and various adjacent markets.

Along with continued product innovation and advertising investment, Stanley's brands should remain in demand for many years to come. The company will face its ups and downs depending on commodity price volatility and macro trends in key markets such as construction, but its profits will likely continue marching higher over long periods of time.

Stanley's supply chain struggles and inflationary headwinds probably aren't issues investors will be talking about years from now, but they provide an opportunity for dividend growth investors to consider the stock at an unusually high dividend yield near 3%.

We will keep monitoring the macro challenges weighing on Stanley's short-term outlook and provide updates as needed.