Cracker Barrel Battles Surging Food, Wage Costs to Defend Dividend

Cracker Barrel's operating margin sits at roughly half its pre-Covid level, reflecting double-digit commodity and wage inflation along with dine-in traffic that has yet to recover fully from the pandemic's effects.

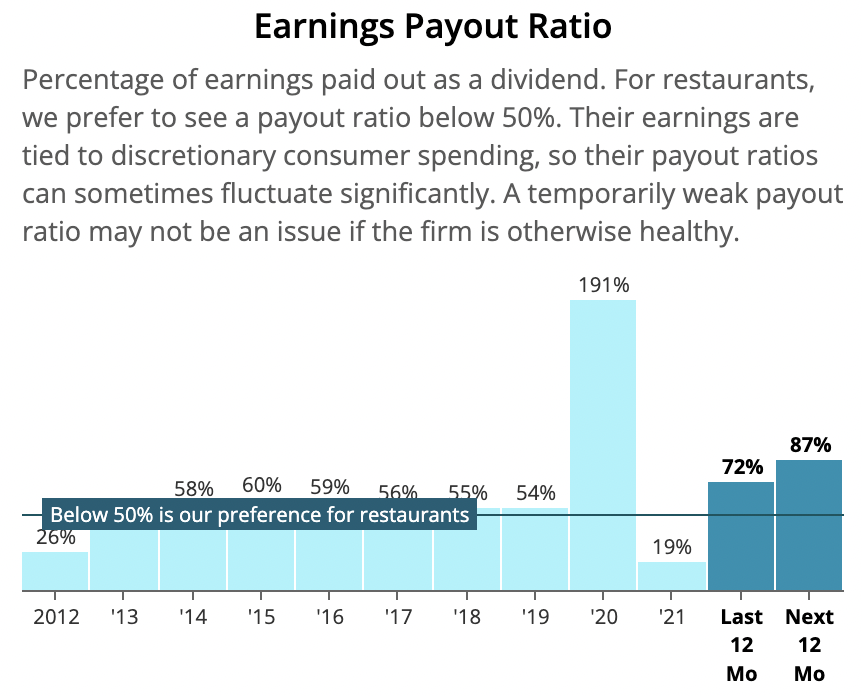

As earnings pressures mount, Cracker Barrel's payout ratio may creep further towards 100%, a level not seen since the onset of the pandemic in 2020.

Source: Simply Safe Dividends

We expect Cracker Barrel to remain committed to its dividend during this difficult period, but the path back to "normal" profitability and dividend coverage will take time.

Compared to other restaurant chains, Cracker Barrel's business model is more sensitive to the challenges posed by today's consumer and inflationary environment.

Over 80% of Cracker Barrel's restaurants are located along interstate highways, with many others positioned near tourist destinations. Travelers account for nearly 40% of visits.

Management believes the spike in gas prices disrupted traditional spring break vacation patterns last quarter, resulting in lower travel visits.

Record fuel prices could also impact summer travel and pinch the finance's of Cracker Barrel's target audience of over 65-year-old guests, many of whom live on fixed incomes and value the chain's affordability.

With an average check under $12 for its homestyle meals, Cracker Barrel may need to take a more delicate approach to raising its prices to combat inflation without hurting its value proposition.

From meat to fruits and vegetables, Cracker Barrel last quarter experienced higher-than-expected commodity inflation of 18% compared to the prior year period, with elevated freight costs and wages also running ahead of its pricing.

To help improve margins, management is implementing new food and labor cost management systems that should partially offset higher commodity costs and wages, which have historically consumed about 65% of the firm's revenue.

Cracker Barrel also plans to hike prices by 7% over the remainder of the year and attain higher average checks by tweaking its menu, including the addition of beer and wine.

Profitability could be further aided if more older guests return to in-person dining as Covid receives, and Cracker Barrel has opportunity to retain a much larger off-premise business (to-go orders, delivery, catering) that ballooned from 9% to 20% of sales during the pandemic.

Overall, we believe Cracker Barrel's long-term outlook remains intact despite a challenging operating environment that could persist for at least several quarters.

Cracker Barrel's dividend coverage will be tight until profitability improves, but the firm's healthy balance sheet, mature footprint of over 700 restaurant locations, and predictable cash flow provide support for the payout.

Reflecting confidence in Cracker Barrel's finances and ongoing commitment to returning capital to shareholders, management earlier this month even announced a new $200 million share repurchase plan. For context, Cracker Barrel's dividend costs around $120 million annually.

It's also worth noting that Cracker Barrel had paid uninterrupted dividends for more than 30 years before the pandemic forced closures of in-person dining, ultimately leading management to suspend the dividend temporarily.

The dividend was restored to pre-pandemic levels by the end of 2021 and seems likely to be defended by the company during hard times, albeit with little to no dividend growth until profitability improves.

We will continue monitoring the impact of inflationary pressures on Cracker Barrel's outlook and dividend safety.