With oil prices more than doubling since the beginning of 2021 to over $100 a barrel, Exxon has used its surging cash flow to repay practically all of the debt it took on during the pandemic.

As a result, the integrated oil giant's debt to capital ratio, or gearing, has fallen from a peak of 29.2% in 2020 to 21.2%. Gearing measures the proportion of a company's financing that is from debt rather than equity.

Exxon's gearing now sits at the low end of management's 20% to 25% target range and near its pre-pandemic level of 19.1%.

Exxon can use its balance sheet capacity to protect its dividend whenever the next downturn in energy prices occurs. When oil falls below the firm's breakeven price needed to cover its capital spending program and dividend, Exxon can borrow debt to plug its cash flow deficit until the pricing environment improves.

All else equal, we estimate Exxon could borrow almost $13 billion before reaching the high end of its gearing target. The company also holds $11 billion of cash, up from $3.1 billion at the end of 2019, that can go towards funding any shortfalls. For perspective, Exxon's dividend costs $15 billion annually.

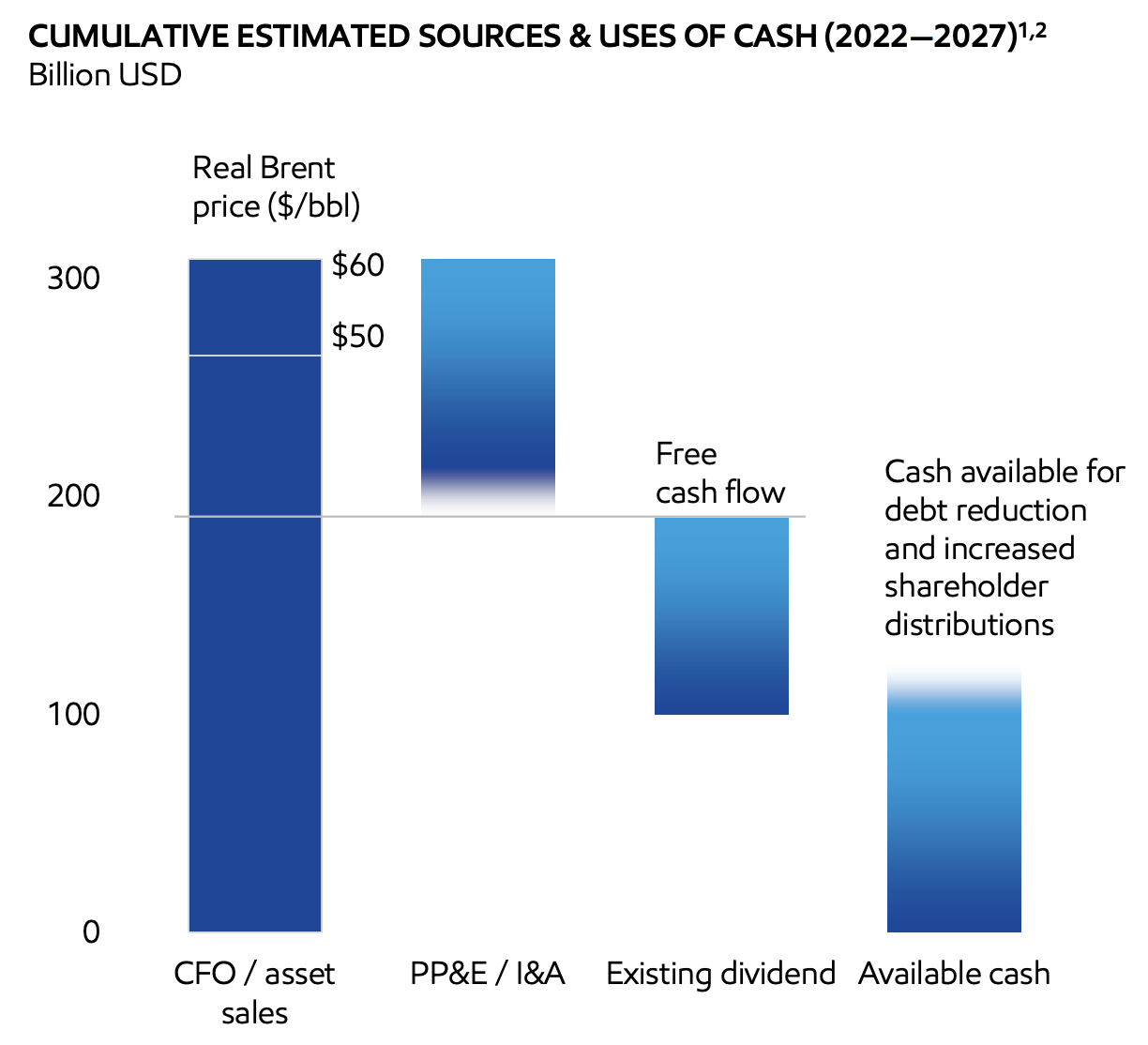

Exxon's financial position has arguably not been this strong since 2015. The firm has also seen its breakeven price fall from an estimated $60 per barrel in 2020 to $41 in 2021, reflecting more disciplined capital spending, cost reductions, and stronger profitability in its downstream and chemical businesses.

Coupled with Exxon's balance sheet capacity, we believe the firm could now support its dividend for at least a couple of years even if oil prices averaged as low as $30 per barrel.

Management sees a path to further reduce the firm's average breakeven to just $35 per barrel over the next five years, too. Structural cost reductions are the biggest driver, but Exxon also sees opportunity to shift more of its portfolio towards low cost-of-supply barrels and higher-value fuel and chemical projects.

In recognition of Exxon's improved positioning to weather future energy market downturns, we are upgrading the company's Dividend Safety Score from Borderline Safe to Safe.

Overall, Exxon's business has rebounded sharply from the depths of the pandemic thanks to the surge in commodity prices. This gives the oil major flexibility to continue rewarding income investors without compromising on its capital allocation plans, which include a gradual mix shift towards lower-emission products such as biofuels and chemicals.

In the meantime, even if oil prices are cut in half, Exxon should remain a cash cow capable of paying a modestly growing dividend and repurchasing more of its shares.

Source: Exxon Investor Presentation

For income investors who share our belief that fossil fuels will remain a core component of the world's energy mix, Exxon seems like a good bet to continue its streak of paying uninterrupted dividends since 1882.