Philip Morris to Continue Prioritizing Dividend Following $16 Billion Acquisition of Swedish Match

Philip Morris on Wednesday announced plans to acquire Swedish Match in a $16 billion all-cash transaction, marking a major step in the international Marlboro maker's transition to a smoke-free company.

While this deal will increase Philip Morris's leverage ratio from about 2x to 3x, its highest level in at least a decade, management reassured investors that they have "an unwavering commitment" to growing the dividend annually.

Philip Morris seeks to reduce its payout ratio to around 75% compared to a projected level of 90% in the year ahead, but management does not "put any pressure on when we get there, it's a kind of a long-term vision."

The recession-resistant business should remain a cash cow with strong financial health. Commenting on the acquisition on Thursday, S&P Global Ratings indicated that Philip Morris's A credit rating would likely be downgraded just one notch, leaving it firmly in investment grade territory.

We do not see the acquisition materially changing Philip Morris's risk profile, so we are reaffirming the company's Safe Dividend Safety Score.

Since 2016, Philip Morris has had a mission to eventually replace cigarettes with less harmful alternatives, such as heated tobacco and e-vapor.

In 2015, essentially all of the firm's revenues came from cigarettes. In 2021, nearly 30% came from smoke-free products. And by 2025, Philip Morris aims to be a predominantly smoke-free company, with more than half of its revenues coming from such products.

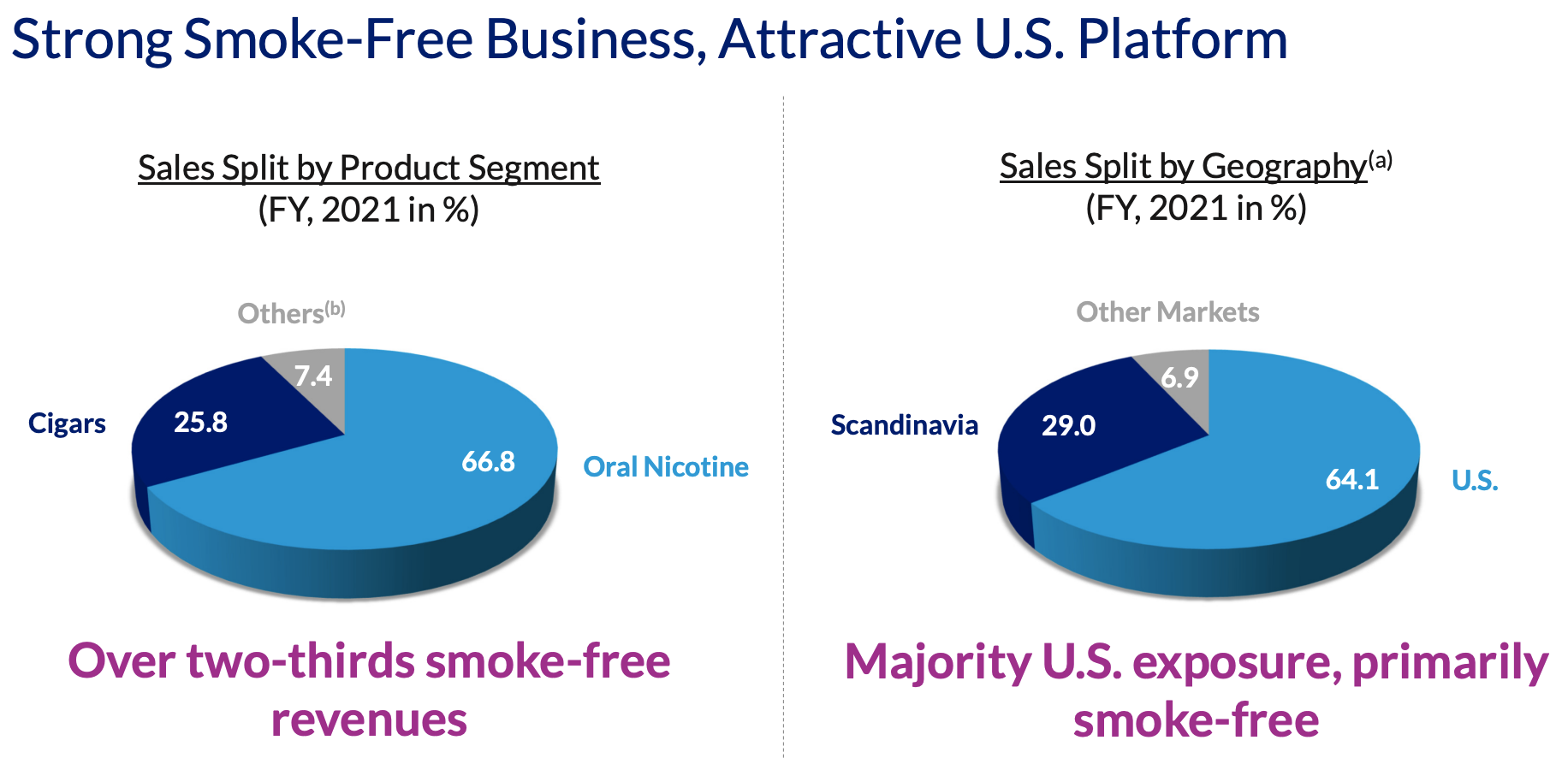

Swedish Match gives Philip Morris an even more comprehensive smoke-free portfolio. The fast-growing, profitable company operates primarily in the U.S. and Scandinavia. Most of its revenue comes from smoke-free products, including the leading nicotine pouch franchise in America.

Source: Philip Morris Investor Presentation

Buying Swedish Match allows Philip Morris to directly enter the large and growing U.S. smoke-free market. The firm can further develop Swedish Match's oral nicotine portfolio and leverage Swedish Match's operational platform in the U.S. to introduce other smoke-free products in future years.

Philip Morris also sees potential in selling Swedish Match's nicotine pouches in international markets, with the category's retail value expected to grow by 30% to 40% annually over the next 5 years.

Simply put, Swedish Match provides a lot of complementary opportunities for growth across geographies and product lines while further advancing Philip Morris's smoke-free ambitions.

Thanks to the healthy profitability of Swedish Match, management also expects the deal to be accretive to the company's margins, earnings, and cash flow.

While there is a lot to like, the main risk is that the U.S. Food and Drug Administration will begin to crack down on oral nicotine products, which have not been regulated as tightly as combustible tobacco or vaping products.

With their sweet flavors appealing to young people, oral nicotine could eventually face more scrutiny that reduces the category's growth potential. For now, it's worth giving Philip Morris the benefit of the doubt.

Overall, Philip Morris continues to establish itself as the global leader in reduced-risk products aimed at traditional smokers. Broadening its product portfolio and geographical reach with Swedish Match provides additional long-term growth opportunities, all while keeping its dividend a solid bet for income investors.