AT&T's Rebased Dividend Supported by Stronger Balance Sheet, Improved Business Mix

AT&T's long-anticipated dividend reduction became official last week as the telecommunications giant reduced its payout by 47%, in line with management's previous guidance.

With the firm's rebased dividend in place, we are upgrading AT&T's Dividend Safety Score to Safe. This reflects the company's improved financial position and more defensive business mix.

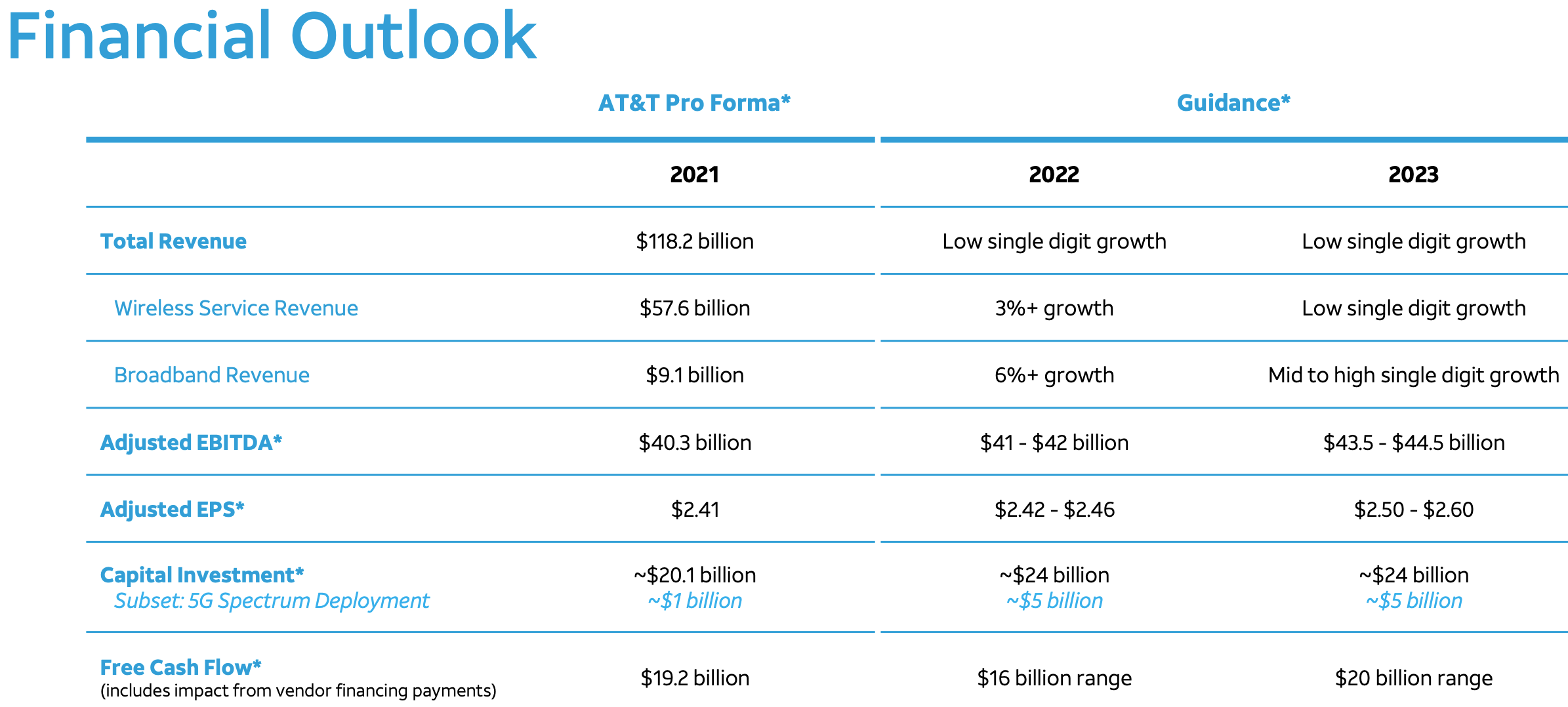

Going forward, AT&T's dividend will consume roughly 40% of the company's free cash flow, down from around 60% previously. Retaining more cash flow provides AT&T with flexibility to increase investment in 5G wireless and fiber internet while enabling faster debt reduction.

Management forecasts leverage (net debt to EBITDA ratio) will fall to 2.5x by the end of 2023, down from around 3x in 2021 and reaching its lowest level since AT&T acquired Time Warner in 2018.

Credit rating agency S&P expects AT&T to maintain its BBB investment-grade rating with a stable outlook, noting that the firm's leverage ratio will remain "comfortably below" S&P's downgrade threshold.

We expect AT&T's remaining operations to deliver more predictable results, too. The company's mobile phone services business now accounts for around 80% of operating income, followed by business wireline contributing roughly 15% of profits and consumer wireline adding about 5%.

These defensive businesses benefit from having large subscriber bases, recurring revenue, recession-resistant services, and high barriers to entry given their capital intensity.

While parts of the wireline business such as legacy landline phones face secular decline, we believe management's forecast calling for low single-digit revenue and EPS growth is reasonable.

Source: AT&T Analyst Day

AT&T's wireless and broadband services drive the bulk of profits and are already recording top and bottom line growth. These businesses should further benefit from management's increased focus and higher capital spending on 5G spectrum deployment and high-speed fiber lines.

Despite facing stiff competition from other wireless carriers and cable companies, AT&T's network investments have potential to drive growth by allowing AT&T to sell pricier 5G data plans and offer more homes and businesses faster internet that can be delivered more cost efficiently compared to today's copper wires.

As investments in 5G deployment and fiber moderate beyond 2023, AT&T expects its annual capital expenditures to begin tapering from $24 billion to around $20 billion.

Combined with cost savings, lower interest expense from debt reduction, and overall earnings growth, we believe AT&T's free cash flow has potential to approach $24 billion in several years.

The company's $8 billion dividend should remain well covered as the business slowly rolls forward, and management will have even more flexibility to pay down additional debt, buy back stock, or reward investors with faster dividend growth.

For now, income investors should probably expect no more than low single-digit dividend growth as management prioritizes network investments and debt reduction. But the outlook for payout raises will improve by late 2023 if all goes according to plan.

We plan to keep holding our small position in AT&T in our Conservative Retirees portfolio. After the spin-off executes, which will cause AT&T's stock price to fall by the value of the spin-off (we estimate $6 to $7 per AT&T share), AT&T will sport a safe dividend yield north of 6% and a forward P/E ratio near 7, representing about a 20% discount compared to Verizon's multiple.

However, given our portfolio's goals of generating safe income and preserving capital, we plan to sell the shares of Warner Bros. Discovery (WBD) we are entitled to.

As we discussed in February, WBD's big bet on streaming demands substantial investment in content and seems unlikely to turn a profit for many years. Coupled with WBD's high debt load, we do not expect this company to pay a dividend for the foreseeable future.

AT&T shareholders of record as of April 5 will receive an estimated 0.24 shares of WBD for each share of AT&T common stock whenever the transaction closes later in April.

Beginning on April 4 and continuing through the business day before the merger closes, AT&T investors will have the option to sell the right to receive shares of WBD while retaining shares of AT&T stock.

This option will be available under the temporary symbol "WBDWV" and is the likely path we will pursue in our portfolio to exit the spin-off. Trades under this symbol will settle after the closing date of the WarnerMedia-Discovery transaction. See AT&T's press release here for more details.

As always, we will send out an email before we make any trades in our portfolio.

Overall, AT&T is in the final stage of undoing the major capital allocation blunders it has made over the past decade. Acquiring DirecTV and Time Warner ultimately destroyed tens of billions of dollars for shareholders while impairing management's credibility.

AT&T's remaining operations focused on wireless and internet services should remain durable cash cows, and the stock's valuation appears to provide a decent margin of safety for income investors who are willing to give the simplified company another chance.

We will continue monitoring AT&T's progress executing the spin-off and provide updates as needed.