Walmart's E-Commerce Traction Strengthens Long-term Outlook

In recognition of Walmart's improved payout ratio, lower leverage, and e-commerce traction, we are upgrading the discount retailer's Dividend Safety Score from Safe to VerySafe.

For years, Walmart's earnings stagnated as labor costs rose faster than sales and more of its product categories lost ground to e-commerce rivals such as Amazon.

This trend never endangered Walmart's dividend, but it clouded the big-box giant's long-term outlook for growth. Walmart's ironclad grip on the brick-and-mortar retail world was being challenged a by a new shopping format, one it had been slow to react to.

Walmart scrambled to catch up, pouring billions of dollars into investments across e-commerce, technology, and its supply chain. The firm also made some poor acquisitions, including its 2016 purchase of Jet.com for $3.3 billion, which it discontinued in 2020.

This investment-heavy period further weighed on Walmart's margins as its fledgling e-commerce business tried to scale. But, fueled in part by the pandemic, management's strategy has put the company back on track for sustainable, profitable growth.

E-commerce has increased from less than 3% of Walmart's fiscal 2016 sales to more than 13% this year. Much of this spending is attributable to online grocery pickup and delivery rather than more lucrative third-party merchandise sales, but it still helps differentiate Walmart from Amazon.

With 90% of Americans living within 10 miles of a Walmart store, management has found success using stores as mini distribution centers. Coupled with its world-class supply chain, the company has a solid foundation on which to further develop its digital capabilities and deliver a seamless omni-channel shopping experience.

E-commerce began driving around half of Walmart's sales growth even prior to the pandemic. With top-line growth strengthening further, Walmart is now leveraging the costly expenses required to support its essential infrastructure for the digital world.

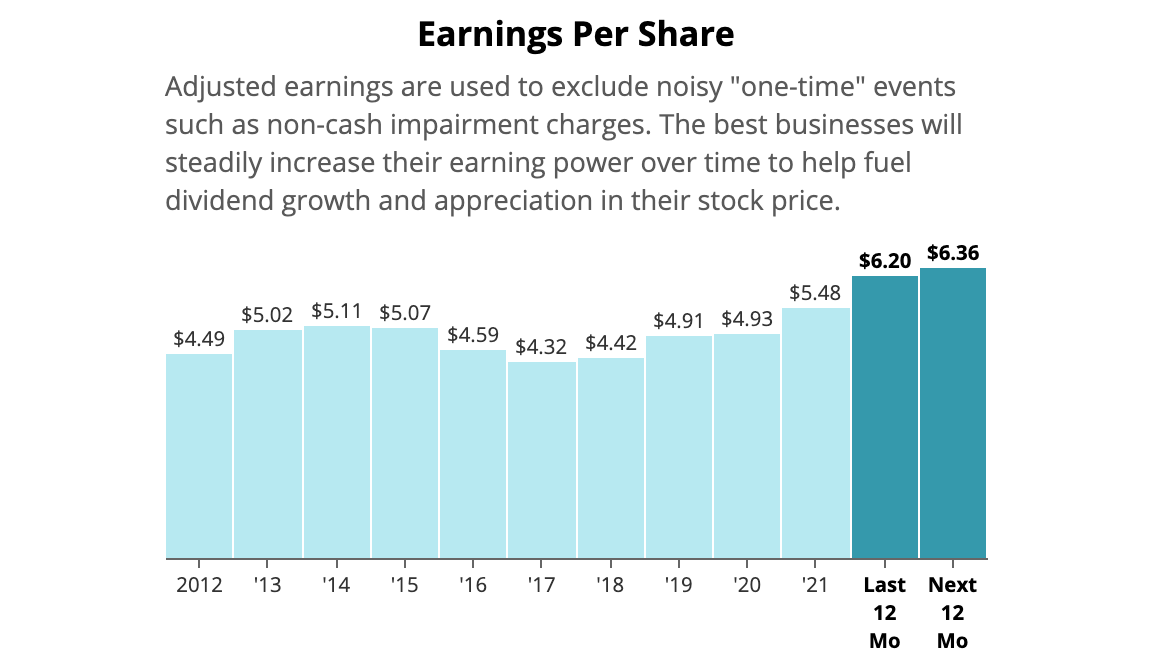

The result: rising earnings after nearly a decade of stagnation.

Source: Simply Safe Dividends

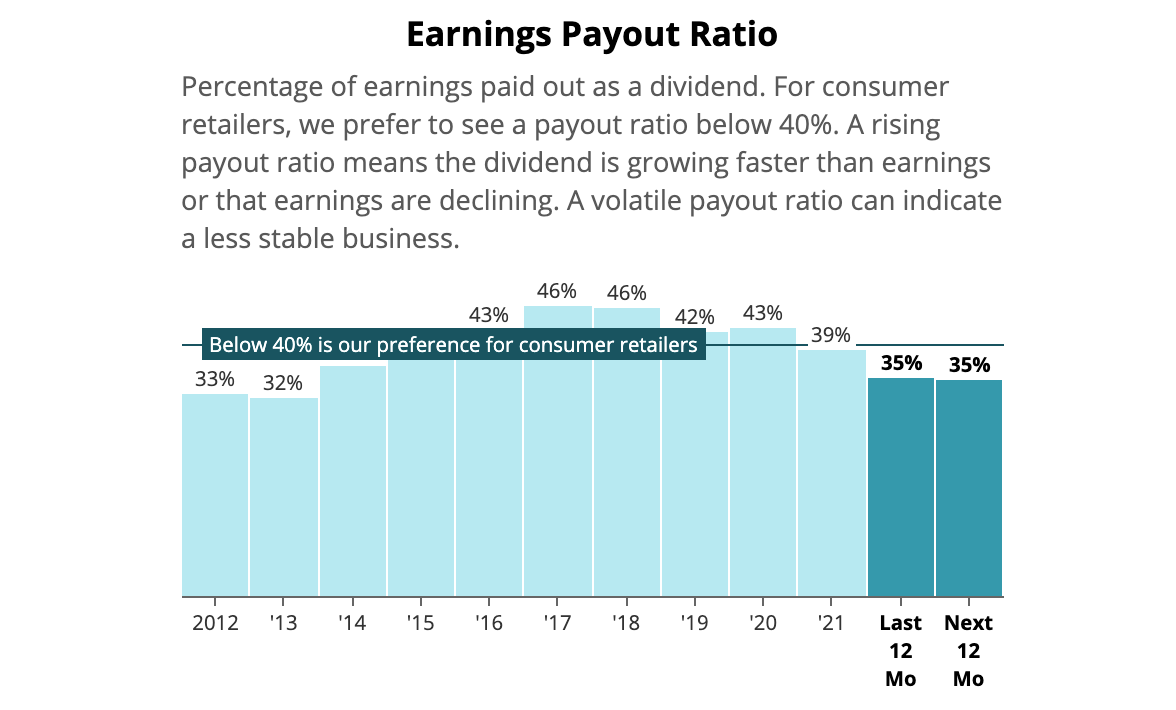

Walmart's earnings have grown at a faster pace than its dividend, reducing the retailer's payout ratio to 35%, its lowest level since 2013. Rising profits have also improved Walmart's leverage ratio to its lowest level in at least a decade, providing strong support for the company's AA credit rating.

Source: Simply Safe Dividends

The company could begin rewarding shareholders with slightly faster dividend growth compared to the token penny increases it has announced in each of the last eight years.

But management may prefer to continue maintaining Walmart's financial flexibility to prioritize investments towards e-commerce and supply chain initiatives.

Either way, Walmart's competitive positioning appears stronger than it did five years ago, and the dividend aristocrat's finances remain in great shape.

A company of this size may never deliver very fast growth, but Walmart's status as a defensive cash cow remains true as ever.