AbbVie has demonstrated enough progress deleveraging its balance sheet, integrating its transformative acquisition of Allergan, and advancing its drug pipeline to earn a Dividend Safety Score upgrade from Borderline Safe to Safe.

Progress across these areas is critical to protect the dividend in 2023 and beyond when blockbuster drug Humira (40% of sales) loses exclusivity in America. AbbVie will face fierce biosimilar competition eager to chip away at Humira's $16 billion of U.S. sales.

When Humira lost patent protection in Europe in late 2018, the drug's revenue slumped 45% in the first year. Management expects a similar result in the U.S., implying the firm could lose at least $8 billion of sales (15% of total revenue) in a single year. Company-wide sales are expected to fall in 2023 before returning to modest growth in 2024.

No one knows how rapidly Humira will fade, especially since AbbVie will face potentially twice as many biosimilar competitors in the U.S. compared to Europe. However, the company has increased its margin of safety to weather the storm and keep its dividend intact.

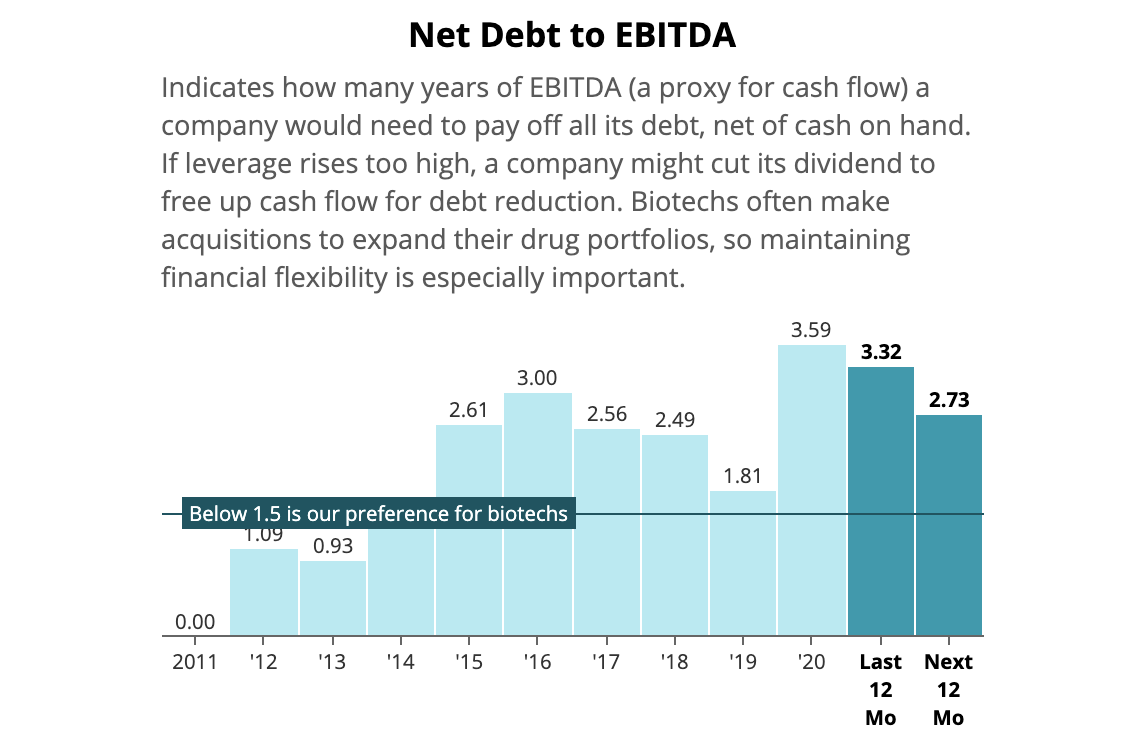

Starting with the balance sheet, AbbVie remains on track to reduce its net debt to EBITDA leverage ratio from 3.5x at the time Allergan closed to less than 2.5x by the end of 2021. The firm has already paid down about a third of the incremental debt it took on to fund the acquisition, and leverage is expected to fall to 2x in 2022.

If AbbVie then lost 20% of its EBITDA as Humira faded, we estimate the firm's leverage ratio would still sit at a reasonable level near 2.5x. This would likely support the firm's BBB+ credit rating and provide some capacity for acquisitions as AbbVie focuses on diversifying its portfolio and returning to growth.

Source: Simply Safe Dividends

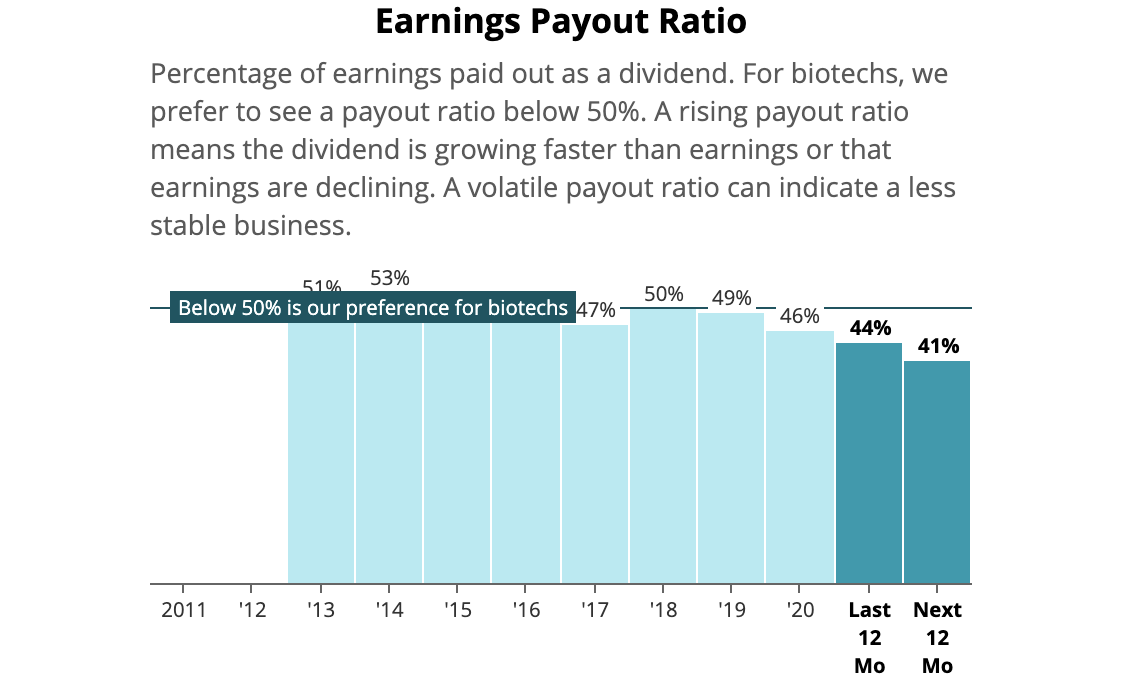

Assuming Humira's 2023 erosion does not create much pressure for AbbVie to improve its balance sheet, the company could afford to run its business with an elevated payout ratio until earnings recover.

Management in recent years has grown the dividend at a slower pace than earnings to provide some cushion for Humira's inevitable decline.

AbbVie's payout ratio has fallen from 50% in 2018 to a projected 41% in the year ahead, reaching its lowest level in the company's history and the low end of the 40% to 50% range maintained by most of its biopharma peers.

Source: Simply Safe Dividends

In 2023, we estimate AbbVie's payout ratio could spike to close to 60%, depending on how quickly Humira's U.S. sales erode. This would not necessarily endanger the dividend, but AbbVie's pace of dividend growth could slow substantially until earnings rebound.

AbbVie's post-Humira earnings profile is the trickiest piece of the story to analyze. Predicting which drugs will become blockbusters, sizing up their peak sales potential, weighing regulatory risks, and monitoring patent expirations for the rest of the portfolio makes long-term projections challenging.

For these reasons, we prefer to invest in pharma companies which own well-diversified drug portfolios, reducing their dependence on any single product's success.

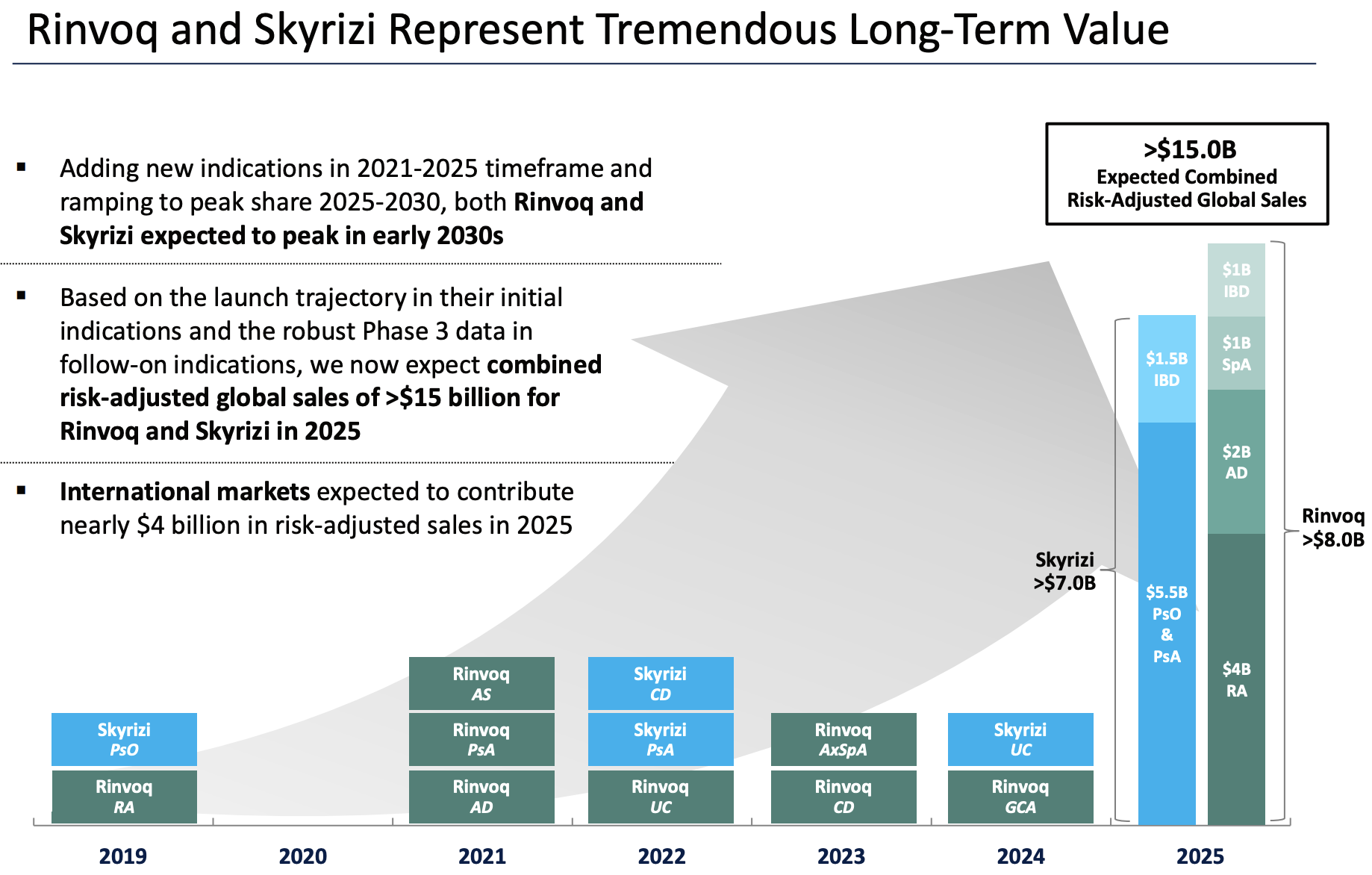

AbbVie expects more than a dozen new products or indications to gain commercial approval over the next two years. However, recent launches Skyrizi (treats psoriasis) and Rinvoq (rheumatoid arthritis) are expected to generate more than $15 billion in annual revenue in 2025, or around 30% of firm-wide sales.

In the first quarter of 2021, revenue from these two products more than doubled to reach nearly $900 million (7% of total sales), or an annualized pace of $3.5 billion. These key drugs still have a long ways to go to reach their potential.

Source: AbbVie Investor Presentation

Imbruvica, a cancer drug, also has potential to reach at least $7 billion in annual revenue. The product is already on pace to exceed $5 billion in sales this year and accounts for 11% of revenue, making it AbbVie's second largest drug.

Continued traction across these three products is critical to AbbVie's outlook. While it's difficult to predict the long-term success of these drugs, we will keep monitoring their results over these next few important years.

Outside of AbbVie's drug pipeline, Allergan's business has performed well since the acquisition closed last May.

Allergan derived about 30% of its sales from an aesthetics business (now 9% of AbbVie's revenue), which includes Botox plastic surgery. This business has boomed during the pandemic as clients adjust to more face time on Zoom calls and address weight fluctuations experienced during quarantine.

Botox's cosmetics revenue is now 27% above its 2019 pre-Covid level, and management believes AbbVie's aesthetics business can sustain a high single-digit pace of growth in the long term. This would help fill some of the hole left by Humira.

AbbVie is also on pace to deliver merger synergies of $1.7 billion in 2021 and greater than $2 billion in 2022. This would meet management's goal for the transaction and provides support for the firm's 2021 guidance calling for 10% revenue growth and 18% EPS growth.

Overall, AbbVie has executed well following its 2019 announcement to acquire Allergan. Humira has fallen from 60% of revenue to 40%, leverage is coming down to safer levels, merger integration work has met expectations, the payout ratio has declined to provide a greater margin of safety, and the combined company is enjoying solid growth.

That said, Humira will likely remain an overhang on the stock. This key product could still represent over 30% of revenue heading into 2023, so investors will anxiously watch how quickly competition erodes Humira's U.S. sales.

Assuming the rest of AbbVie's portfolio continues meeting expectations and Humira revenue does not plunge significantly more than 50% in 2023, we expect the company's dividend to remain safe, albeit with modest growth prospects for a couple years.

We will continue monitoring AbbVie's evolution and provide updates as needed.