Realty Income to Acquire VEREIT for $16 Billion; Dividend Remains Secure

Realty Income on Thursday announced plans to acquire VEREIT, a retail REIT about half of its size. The all-stock transaction is expected to close in the fourth quarter of 2021.

This large acquisition will not impact Realty Income's dividend policy. If anything, the REIT's dividend coverage should improve moderately.

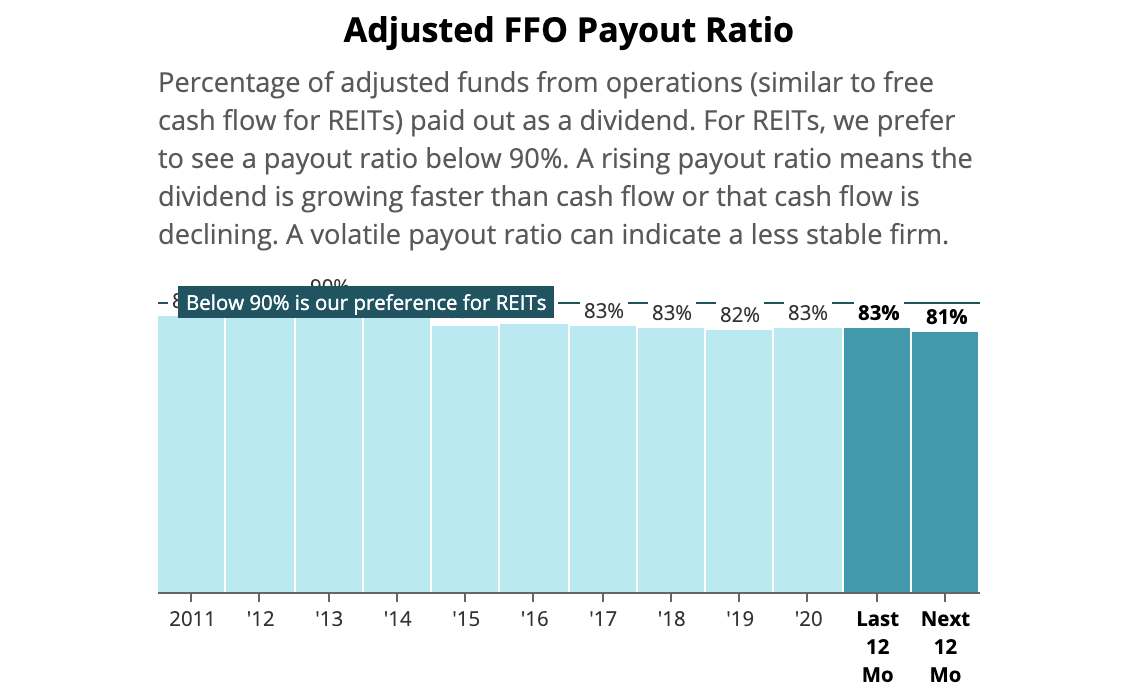

Management expects the deal to increase Realty's adjusted funds from operations (AFFO) per share by at least 10% in year one. Based on the firm's current dividend level and 2021 AFFO guidance, we estimate Realty's pro forma AFFO payout ratio would be 74% this year versus 81% on a standalone basis.

Source: Simply Safe Dividends

Realty Income's balance sheet will remain strong as well since this is an all-stock deal and VEREIT had a BBB investment-grade credit rating. Realty's net debt to EBITDA leverage ratio will tick up only slightly from 5.3x to 5.5x, which S&P expects will remain supportive of the firm's A- credit rating.

From a strategic perspective, Realty Income pursued VEREIT to increase its scale, operating efficiency, and diversification.

The company's portfolio will expand from approximately 6,500 properties to more than 10,000. This will drive rental revenue up from around $1.6 billion to $2.5 billion.

Realty expects to spread its operating expenses across this larger base of revenue to further enhance its profitability. Management also sees opportunity to refinance VEREIT's debt at lower rates to take advantage of the combined company's lower cost of capital, resulting in interest expense savings.

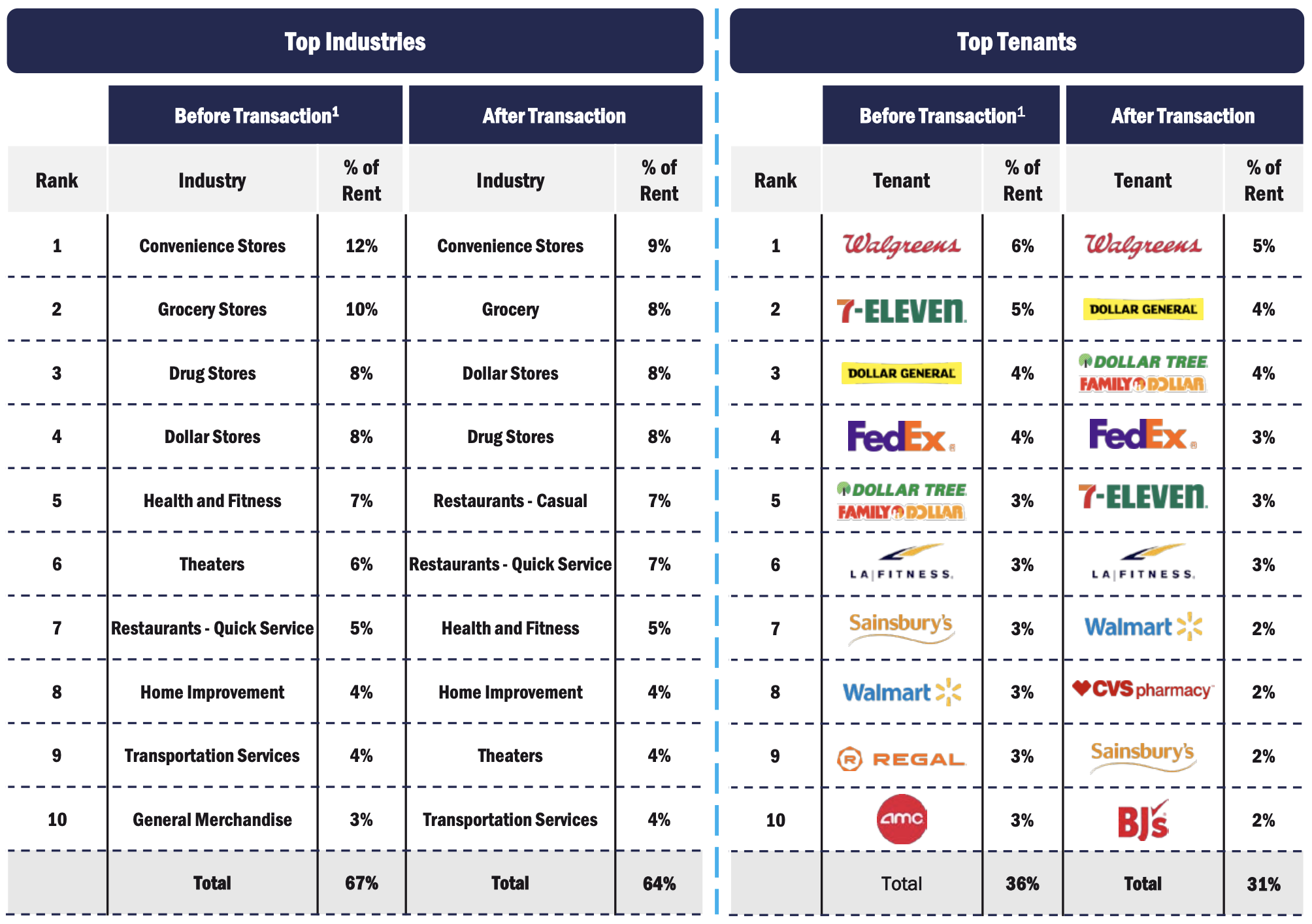

From a business mix perspective, not much will change. Realty Income will generate 83% of its rent from retail with another 14% from industrial markets. In 2020, those figures stood at 84% and 11%, respectively.

Similarly, convenience stores will remain the largest industry exposure at 9% of rent, followed by grocery (8%). Challenged industries such as health and fitness (5%) and theaters (4%) will become somewhat smaller contributors, while restaurants (7% casual, 7% quick service) take on somewhat more prominence.

Source: Realty Income Investor Presentation

Tenants with investment-grade ratings will represent 45% of rent, down slightly from 51% previously. However, Realty Income's mix will become more diversified, strengthening the durability of its earnings.

The REIT's top 10 industries will account for 64% of rent (down from 67%), its 10 largest tenants will combine for 31% of rent (down from 36%), and its largest tenant, Walgreens, will be 5% of rent (down from 6%).

From a valuation perspective, the price Realty Income paid for VEREIT was consistent with most of the property acquisitions it has made recently. The deal implies a cap rate (property operating income / property acquisition price) of about 6%.

For context, during 2020 Realty Income invested over $2.3 billion in 244 properties at a weighted average cap rate of 5.9%.

With some cost synergies and refinancing benefits expected down the road, this acquisition looks like a reasonably priced deal for Realty Income.

Finally, it's worth noting that once the merger closes, Realty Income plans to spin off its office properties into a separate, publicly traded REIT. At that time, shareholders will receive a distribution of shares in this new entity.

Offices represent 3% of Realty's rent and nearly 20% of VEREIT's. We don't expect this to impact Realty's dividend profile and will provide updates as more information about the spin-off's business is made available.

Overall, Realty Income's acquisition of VEREIT looks like a good move. The valuation appears fair, the portfolio's overall quality should remain solid, and the combined company's increased scale and diversification offer potential benefits.

Income investors can keep relying on a safe and growing monthly dividend, too.