JPMorgan Positioned for Dividend Increase This Summer as Capital Restrictions Ease

In response to economic uncertainty created by the pandemic, the Federal Reserve last year imposed additional capital preservation measures on America's largest banks.

Banks with more than $100 billion in assets – including JPMorgan – were restricted from repurchasing shares until early 2021, and their dividends are still not allowed to be increased. Total buybacks and dividends cannot exceed net income generated over the past year either.

These restrictions helped ensure that the country's most important banks maintained adequate capital reserves to survive a potentially severe recession and continue providing loans to struggling customers.

With the U.S. economy recovering, the Fed on March 25 announced plans to end its capital distribution restrictions in July for most firms. By then the Fed will have completed its latest round of stress tests, which assess a bank's resilience under various hypothetical economic scenarios.

JPMorgan could raise its dividend as early as this summer once the Fed's restrictions are lifted since the bank remains well capitalized and its payout continues to be well covered by earnings.

But the outlook for bank dividends during the next downturn is hazy in light of the events that took place over the past year. Fortunately, the environment turned out better than feared for the industry.

Thanks to the government's unprecedented stimulus measures, the banking sector mostly avoided severe loan losses that were a major concern when the pandemic set in.

Coupled with limits on buybacks and dividends, JPMorgan CEO Jamie Dimon said on the firm's January earnings call that even after setting aside substantial reserves for potential loan losses last year, they "have so much capital, we cannot use it."

Despite tripling its provision for credit losses in 2020, the bank's net income last year still totaled $29 billion, well above its $12 billion dividend and $6 billion of share repurchases, which were made before the Fed's restrictions went into place.

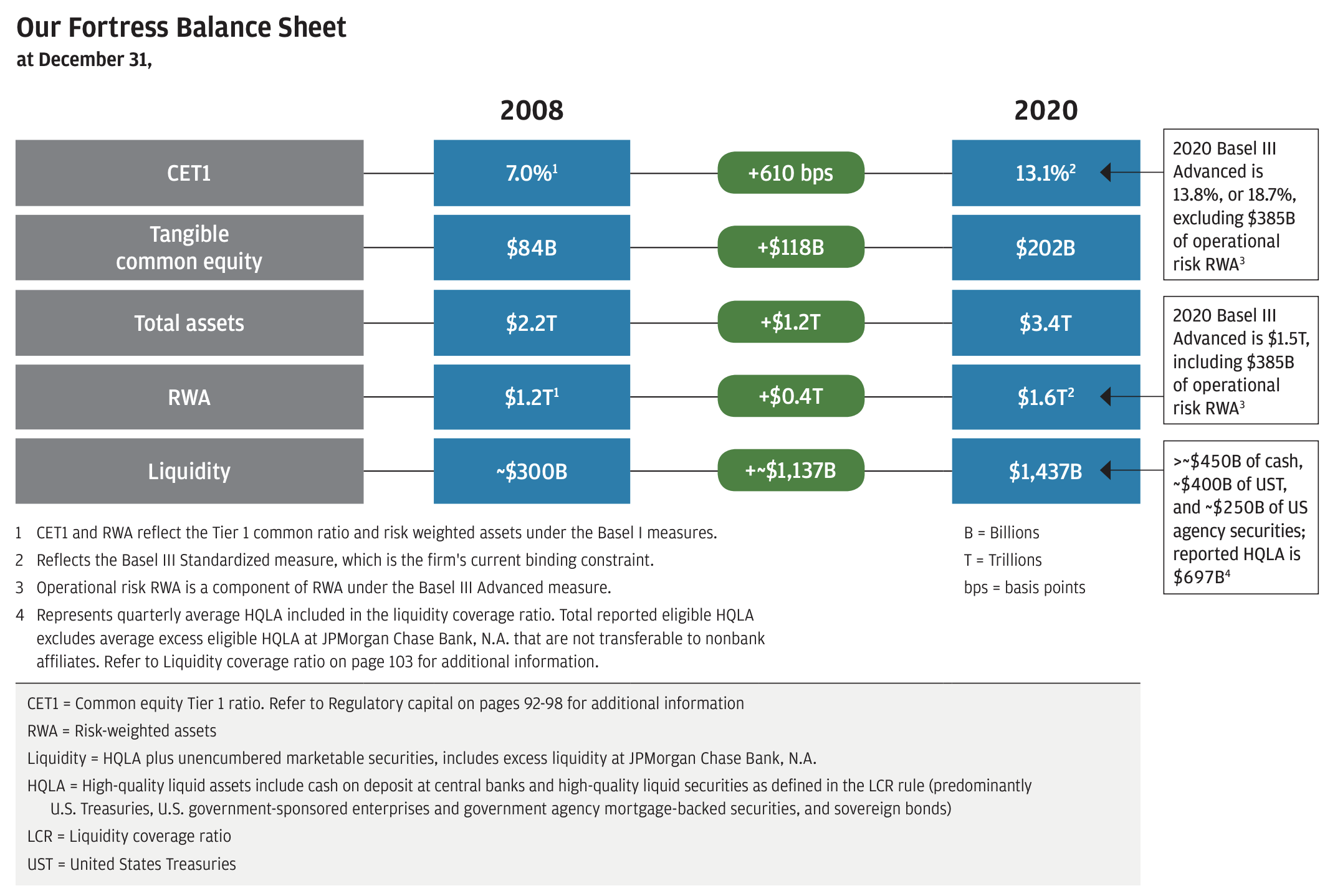

As a result, JPMorgan's capital position strengthened in 2020. The CET1 ratio gauges a bank's ability to absorb losses by comparing its equity capital with the bank's risk-weighted assets, such as loans and investments.

Despite the pandemic, JPMorgan's CET1 ratio ticked up from 12.4% in 2019 to 13.1% last year, remaining well above the minimum level of 11.3% required by regulators.

The bank's CET1 ratio has also nearly doubled compared to 2008, reflecting post-financial crisis regulatory standards which forced banks to hold higher capital levels in hopes of building a more stable financial system.

JPMorgan's liquidity has increased as well, rising nearly fivefold compared to 2008 while the bank's risk-weighted assets have only expanded by about 30%.

Simply put, America's largest financial institutions remain well capitalized and are arguably the most financially sound they have ever been.

Source: JPMorgan 2020 Shareholder Letter

JPMorgan can maintain its high capital and liquidity position even if it needed to handle a substantial increase in reserves (management's best estimate of future loan losses).

The bank's annual profit before credit loss provisions totals around $50 billion. When modeling various pandemic recession scenarios, management expected roughly $20 billion to $30 billion of potential loan losses, with an extreme downside case potentially triggering losses near $50 billion.

In other words, JPMorgan's earnings alone could potentially absorb the losses caused by a major economic downturn, leaving the firm's capital position largely untouched even after paying dividends.

This is primarily why management saw no reason to cut the dividend last year, according to CEO Jamie Dimon's shareholder letter published on Wednesday.

But if an extreme downside scenario appeared to be playing out, that may not have been the case – even if the bank would have likely maintained a strong financial position.

Faced with this level of uncertainty, JPMorgan would consider reducing its dividend out of an abundance of caution for what the future might hold.

"If, however, the worst-case scenario had happened (which means it could have gotten even worse from there), we might have cut our dividend to retain capital out of prudence."

– JPMorgan CEO Jamie Dimon, 2020 Annual Shareholder Letter

This dynamic makes it challenging to assign long-term Dividend Safety Scores to the largest U.S. banks.

On paper, the robust capital levels of most major banks should support their dividends, even in a severe downturn. But the lack of visibility created by such an event could still lead management teams to consider reducing or suspending dividends given the major impact these firms have on the global economy.

Regulators further muddy the outlook. In banks' first serious test since the 2007-09 financial crisis, financial regulators across the U.K., European Union, Australia, and parts of Asia quickly ordered banks to defer, cut, or temporarily suspend dividends regardless of their capital levels.

The Fed ultimately allowed large U.S. banks to continue their dividend programs (so long as payouts did not exceed 100% of trailing net income). But not everyone agreed with the decision given the importance of capital preservation when faced with uncertainty.

"I do not support giving the green light for large banks to [pay dividends or repurchase shares], which raises the risk they will need to tighten credit or rebuild capital during the recovery. This policy fails to learn a key lesson of the financial crisis, and I cannot support it."

Until the next downturn, we expect JPMorgan's dividend to remain safe with the potential for payout increases beginning this summer.

However, our Dividend Safety Scores assess risk over a full economic cycle. As this past year demonstrated, governments control the biggest banks' dividend policies when the tide goes out, regardless of whether banks have met existing capital requirements.

Without knowing the magnitude of the next downturn and the prevailing political and regulatory climate, we feel it is most prudent to maintain a Borderline Safe Dividend Safety Score on JPMorgan and most of its peers.

JPMorgan is one of the best companies in its industry and has the firepower to survive virtually any recession. But income investors should understand that the dividend will likely face risks outside of management's control during future downturns.