Iron Mountain's Restructuring Progress Improves Dividend's Sustainability

Iron Mountain reported earnings on Wednesday and delivered better-than-feared results for the year. Sales in 2020 fell 3%, and adjusted EBITDA was flat.

But the bigger story was management's guidance. Iron Mountain expects 2021 organic revenue and adjusted EBITDA to grow by 2-6% and 7-10%, respectively.

If realized, this would mark the company's highest level of growth in a decade and nudge Iron Mountain's payout ratio and leverage closer to management's target levels.

Based on the midpoint of guidance, the REIT's adjusted funds from operations (AFFO) payout ratio is projected to sit near 75% this year. That's down from 82% in 2019 and could reach the firm's long-term target (low to mid-60s) by 2023.

Meanwhile, Iron Mountain's adjusted leverage ratio finished 2020 at about 5.5x, down from 5.7x at year-end 2019. Management expects to end this year with leverage near the high end of their target range of 4.5x to 5.5x.

In light of Iron Mountain's stabilizing results, we are returning the company to a Borderline Safe Dividend Safety Score.

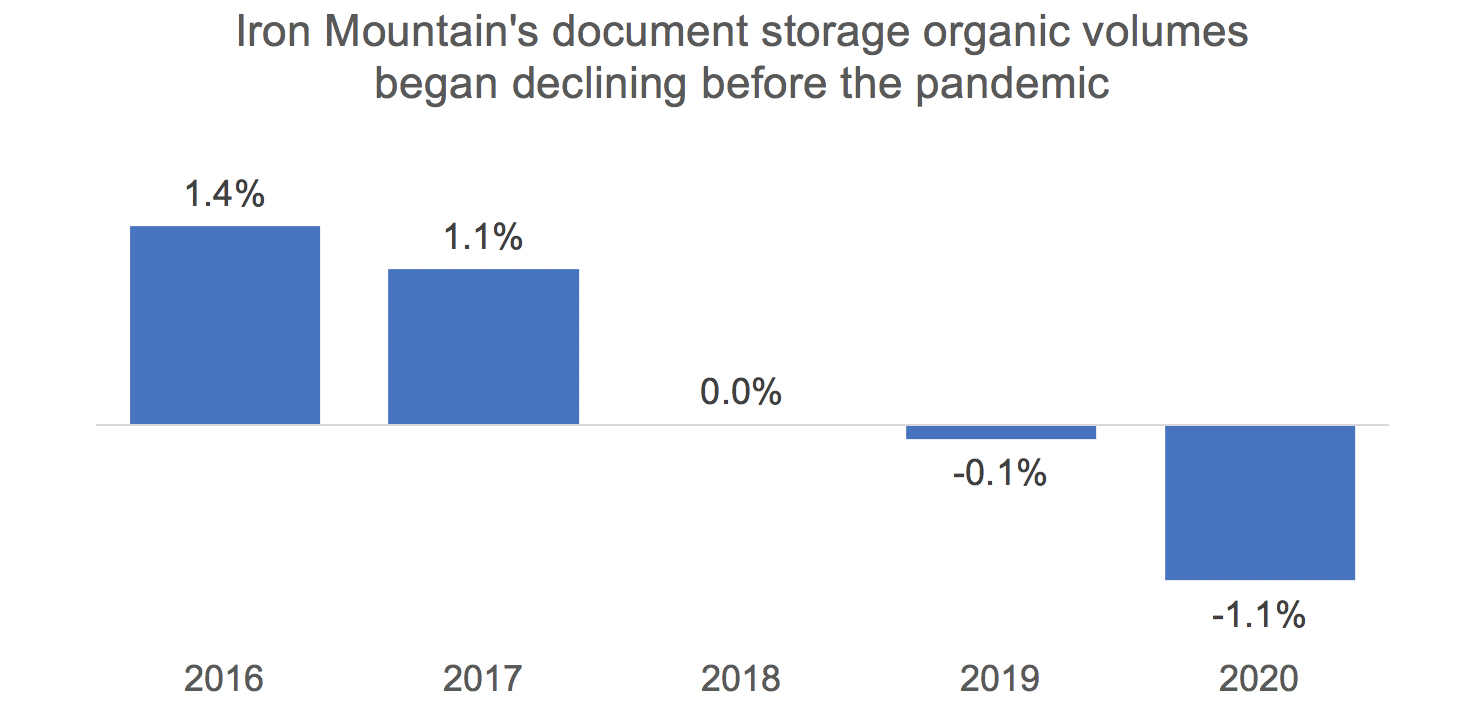

The REIT's core document storage business, which accounts for over 60% of revenue and an even higher share of profits, was experiencing volume declines as more companies moved to paperless (i.e. digital) documents.

Source: Simply Safe Dividends, Company Data

Annual price increases of 2% to 3% were still enough to offset volume pressures, but Iron Mountain realized it needed to extend its business into other areas to combat this long-term secular decline.

However, the REIT's elevated payout ratio limited Iron Mountain's ability to internally fund growth projects. And the firm's high leverage, which earns the REIT a BB- junk credit rating from S&P, didn't provide financial flexibility either.

When the pandemic struck, management doubled down on efforts to take costs out of the business and get creative with financing to protect cash flow and the dividend.

The company used the downturn to broaden the scope of this initiative, upping the expected cost savings to $375 million by the end of 2021. To appreciate the magnitude of these cost reductions, they represent roughly 25% of Iron Mountain's 2019 EBITDA.

Project Summit provided adjusted EBITDA benefits of $165 million in 2020, playing a critical role in helping Iron Mountain hold its annual EBITDA flat at about $1.5 billion.

On the financing front, Iron Mountain has worked to find ways to keep investing in data centers without increasing its leverage.

The REIT in 2020 only retained about $170 million of cash flow after paying dividends but invested more than $300 million in growth projects.

To fund the gap without taking on more debt, the company engaged in several sale-leaseback transactions in which it sold some of its industrial properties and then rented them back.

With property values rising, Iron Mountain was able to use some of this cash infusion to cover growth investments without increasing its adjusted leverage. The REIT has also pursued joint venture agreements to spread out its data center costs.

These levers, coupled with rising cash flow, are expected to help Iron Mountain cover growth expenditures of $410 million in 2021 without increasing its leverage.

That said, Iron Mountain continues to walk a fine line between protecting its dividend and looking out for its future.

Since excess cash flow is not available for debt reduction, management is banking on Iron Mountain growing its way back to a healthier balance sheet and payout ratio.

The plan is to take out more costs and continue expanding into businesses such as data centers, consumer storage, electronic content management, and fine arts and entertainment services.

But these areas represent less than 20% of revenue and an even smaller share of profits. Iron Mountain needs its core document storage business to remain stable as its mix gradually transitions into faster-growing markets.

Document storage is still expected to drive around 80% of Iron Mountain's incremental revenue growth this year, with management anticipating 2% to 3% price increases and flat to slightly positive volume growth.

However, the pandemic has potential to accelerate the secular shift away from paper media as more businesses have been forced to conduct their operations digitally since last March.

Existing customers could continue sending Iron Mountain fewer boxes of documents to store, creating more pressure on volumes over time.

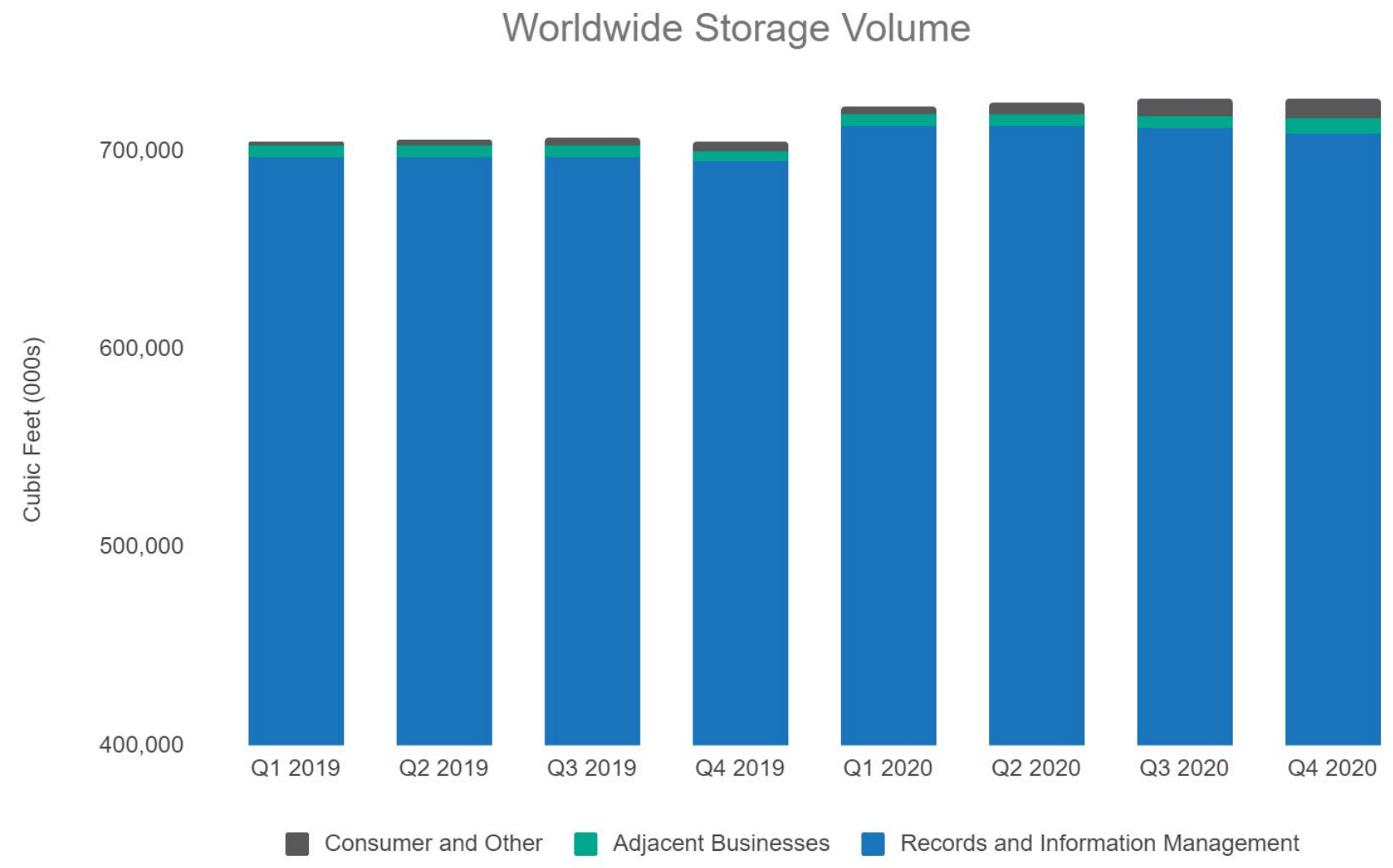

Consumer and adjacent businesses have increased from 0.4% of Iron Mountain's total storage volume in the fourth quarter of 2017 to 2.4% at the end of 2020, but these opportunities may not be big enough to move the needle if core document storage volumes decline.

Source: Iron Mountain Earnings Supplement

Overall, Iron Mountain has done a nice job defending its profitability by taking out substantial costs, making its operations more efficient, and finding ways to fund growth on a leverage-neutral basis.

The company's core document storage business also continues to provide solid cash flow, but Iron Mountain's sub-investment grade credit rating, high cost of capital, and lack of significant retained cash flow relative to its growth budget reduce its margin for error.

If everything goes as planned, income investors should not expect any dividend growth until at least late 2022 when the payout ratio approaches management's target level. But Iron Mountain's results at least suggest the dividend is on steadier ground for now.

We will continue monitoring trends in the company's core storage business and provide updates as needed.