AT&T to Provide Update on Leverage Goals Later This Quarter; Dividend Expected to Be Sustained

Investors will have to wait a little longer to find out how much AT&T spent in a recent record-setting auction for spectrum and how its deleveraging plans will be impacted.

As part of its earnings report in late January, AT&T told investors it was still in the quiet period for the FCC's spectrum auction and could not comment on the details of its bids yet.

The company will instead host an analyst day by the end of March to update investors on where its leverage ratio stands following the auction and provide goals for the future.

The recently frozen dividend will remain part of the plan, with management "committed to sustaining our dividend at current levels" after finishing 2020 with a "payout ratio at a very comfortable level" (about 55% of free cash flow).

But AT&T's elevated debt load and slipping profits continue to create some anxiety about the dividend's sustainability if deleveraging efforts ultimately need to be stepped up.

Prior to the pandemic, AT&T reduced its leverage ratio (net debt-to-adjusted EBITDA) from 3.0x in mid-2018 when it acquired Time Warner to its short-term goal of 2.5x in 2019. The firm was also on track to reach its long-term leverage ratio target range of 2.0x to 2.25x by 2022.

AT&T planned to get there by generating 1% to 2% annual revenue growth, expanding its margins to grow EBITDA by about 10%, and continuing to pay down debt with excess cash flow and nonstrategic asset sales.

Then, the pandemic hit. AT&T's revenue and EBITDA last year fell by 5% and 8%, respectively.

WarnerMedia (15% of EBITDA) faced the most disruption as postponed theatrical releases, content production delays, and cable network ad revenue declines resulted in a 14% sales slump.

Traditional pay-TV (7% of EBITDA) also continued its secular decline with an 11% revenue drop, and AT&T's legacy voice and data wireline services (less than 5% of EBITDA) fell more than 10%.

Management expects revenue growth of about 1% this year, driven by a 2% rise in wireless service sales (over 50% of EBITDA) and a gradual improvement in WarnerMedia's top line.

However, adjusted EBITDA is expected to decline slightly in 2021 as the pay-TV business keeps contracting and AT&T chooses to continue investing in promotions to boost its customer count momentum in its growth businesses.

This aggressive strategy helped AT&T's core wireless services business last year record its highest postpaid phone net adds in a decade and register its lowest postpaid phone churn on record in the third and fourth quarters.

But with adjusted EBITDA not expected to rebound this year, AT&T's leverage ratio faced upward pressure that will now be exacerbated by the firm's splurge on spectrum.

Analysts believe AT&T may have spent as much as $20 billion in the recent spectrum auction to improve the competitiveness of its wireless network for the 5G era.

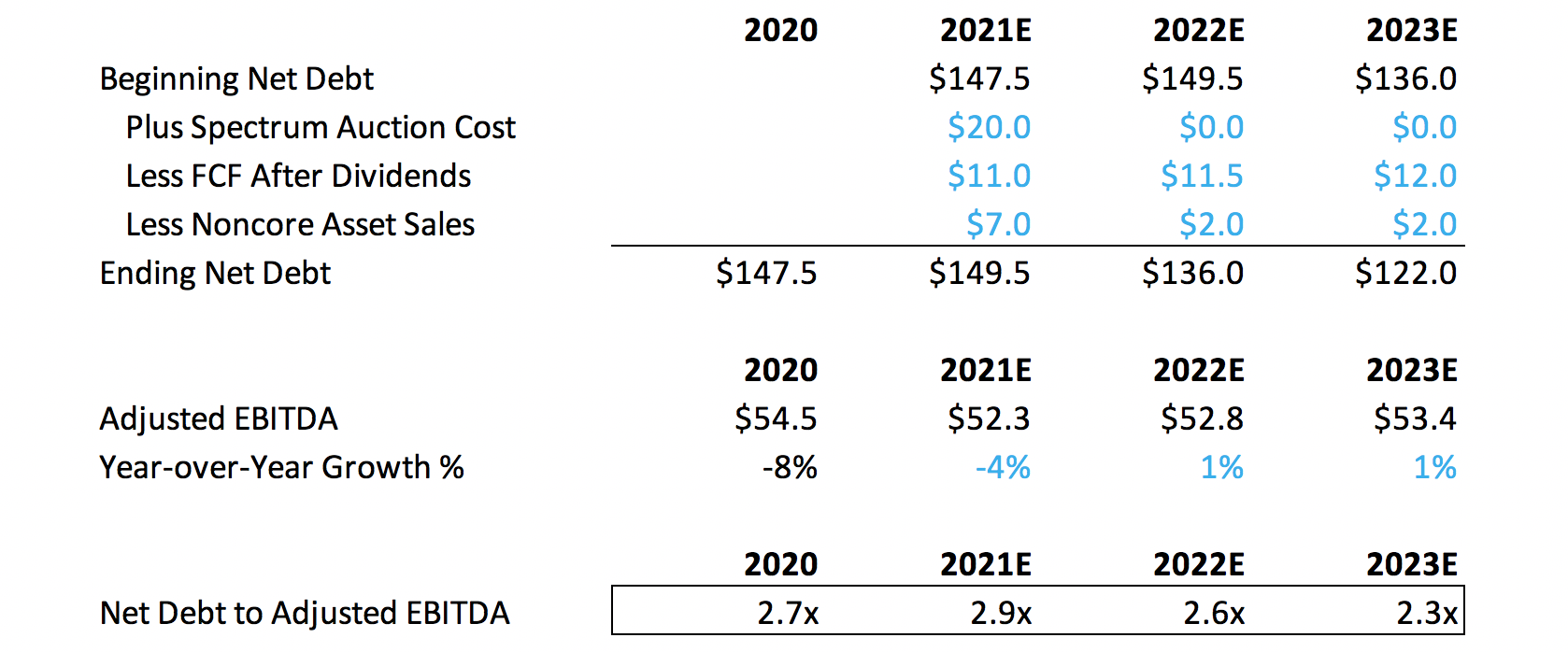

For context, AT&T's net debt totaled $147.5 billion at the end of 2020, and the company had reduced its debt by about $32 billion since acquiring Time Warner in 2018.

In other words, this unexpectedly steep spectrum cost could offset more than half of AT&T's debt reduction progress since the Time Warner merger closed.

How bad could AT&T's balance sheet look following the spectrum auction?

We estimate AT&T's leverage ratio could rise to 2.9x by the end of 2021, up from 2.7x in 2020 and 2.5x in 2019. Leverage could stand at its highest level since the Time Warner acquisition closed in mid-2018 (3.0x).

Needless to say, AT&T will not be able to hit management's original goal of reducing leverage to 2.0x to 2.25x by 2022.

We estimate that AT&T's leverage could decline around 0.3x per year beginning in 2022, putting the company on track to hit its original leverage target around two years later than management originally hoped.

Source: Simply Safe Dividends, Company Filings

Our leverage ratio projections above assume that AT&T's spectrum bids increase its debt load by $20 billion.

Debt will then be reduced by using all free cash retained after paying dividends ($11 billion to $12 billion per year) and proceeds from non-core asset sales ($7 billion in 2021, assuming AT&T sells around 50% of DirectTV, and $2 billion per year thereafter).

Finally, we assume adjusted EBITDA falls around 4% in 2021 (accounting for a potential partial sale of DirecTV) before returning to 1% annual growth beginning in 2022.

Management originally believed adjusted EBITDA could reach as much as $65 billion in 2022 (versus our $53 billion estimate), so hopefully these longer-term assumptions prove to be conservative.

Source: Simply Safe Dividends

Assuming AT&T does not need to significantly ratchet up its spending on important areas such as 5G, fiber internet, and streaming, there still seems to be a reasonable path to return AT&T's balance sheet to a healthier place while keeping the dividend intact.

Management has also taken advantage of favorable debt market conditions to reduce refinancing risk. Less than $8 billion of AT&T's debt matures annually through 2025 (covered by retained free cash flow), and the firm's average interest rate cost is only around 4%.

Meanwhile, AT&T's BBB credit rating sits two notches above junk status and has a stable outlook from S&P and Moody's, further reducing pressure to accelerate deleveraging.

Based on what we know today, we are continuing to maintain AT&T's Safe Dividend Safety Score.

However, we would consider downgrading AT&T's score to Borderline Safe if the firm's spectrum costs significantly exceed $20 billion or if management signals a willingness to run the business with a higher leverage ratio in the long term.

A downgrade could also occur if AT&T's cash flow outlook deteriorates beyond 2021. This could happen if AT&T's wireless business starts to show cracks as 5G takes hold, HBO Max struggles to grow and requires more investment, or some other material headwind arises.

After all, investors understandably do not have much faith in management's capital allocation abilities following AT&T's ill-timed and costly expansions into pay-TV and media.

The firm's acquisition of DirecTV alone could result in a loss of more than $50 billion, or roughly a quarter of AT&T's current market cap. AT&T paid $67 billion (including debt) for DirecTV in 2015, but offers today are reportedly near $15 billion following years of subscriber losses for linear TV.

That said, we estimate that over 80% of AT&T's EBITDA is generated from businesses that can become larger and more profitable over time – wireless services, WarnerMedia, high-speed internet, and managed business services such as networking.

Aside from WarnerMedia, which suffered from unusual circumstances caused by the pandemic, all of these businesses grew their top lines last year.

As these cash cows hopefully become even larger contributors to AT&T's overall mix, the company can be better positioned to restore its balance sheet and demonstrate that it is not a shrinking ice cube.

Management has a long ways to go to regain credibility with investors, and AT&T's upcoming analyst day can serve as an important step in that journey. We plan to provide another update once this information becomes available.