UGI’s Dividend Continues Looking Safe Despite Some Softness in Propane Markets

UGI Corporation has a dividend yield nearly twice its historical five-year average. Naturally, this is leading some investors to question the safety of UGI’s dividend.

So, what’s weighing on the stock? The biggest concern appears to be the timing of increased leverage shortly before an economic crisis brought upon by an unexpected global pandemic.

In 2019 UGI completed a merger with AmeriGas, a propane distribution company, and acquired the Columbia Midstream Group, a midstream services business.

These deals totaled over $3.7 billion in value. For context, UGI’s market cap is about $7 billion.

This spending led to a significant jump in leverage by year-end. UGI’s debt had reached its highest level in the past decade.

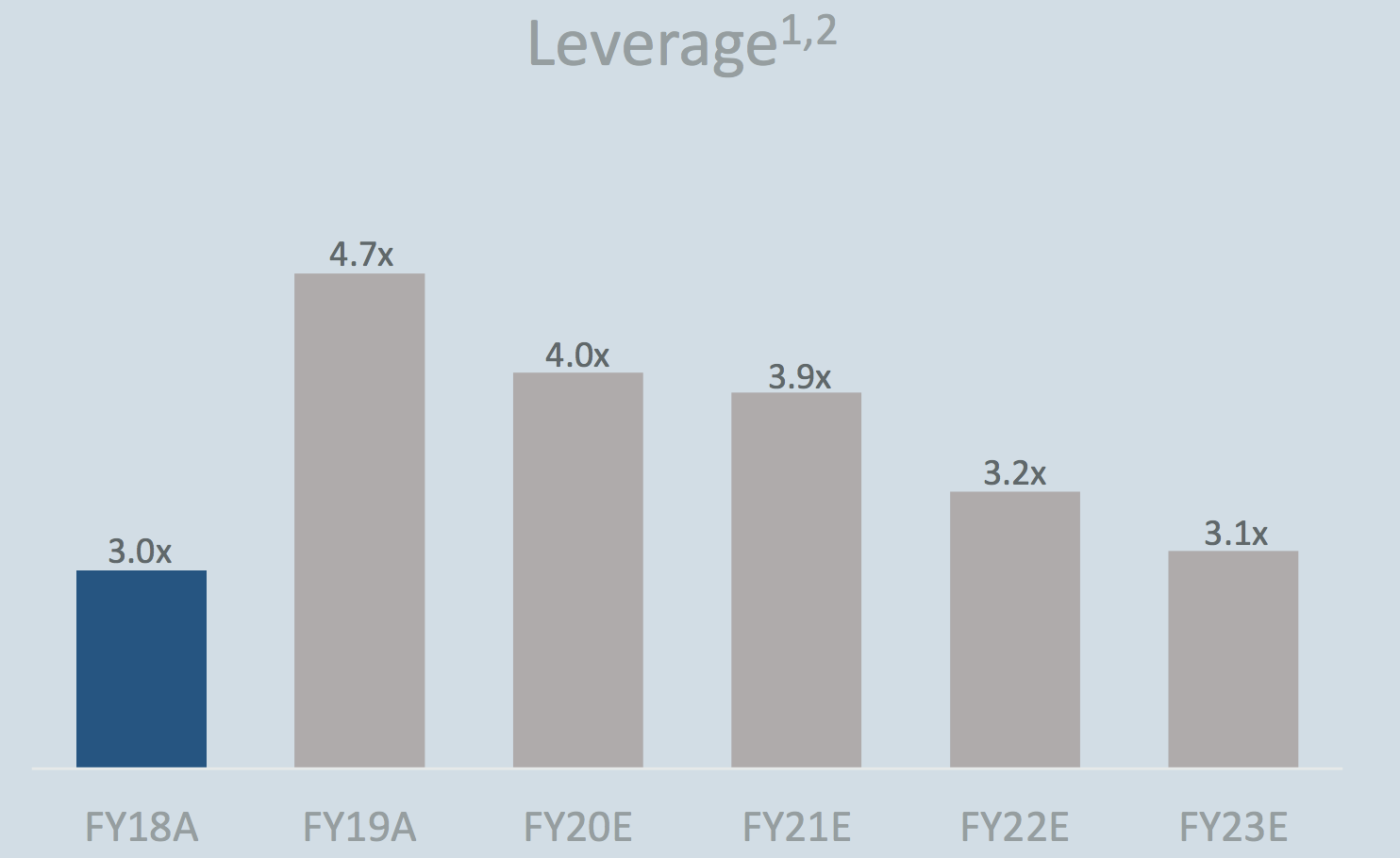

Depicted below is the firm’s current and estimated leverage ratio, as reported by UGI. Management expects to reduce leverage by growing EBITDA while concurrently paying down debt through fiscal year 2023. Source: UGI Investor Presentation Engaged in a moderate to aggressive deleveraging program coupled with an economic crisis, could UGI’s earnings be negatively impacted to the point where management must decide between deleveraging or maintaining their dividend?

Based on what we know today, that seems unlikely. We plan to maintain UGI's Very Safe Dividend Safety Score.

A quick overview of UGI’s businesses helps us understand the stability of and risk to earnings.

For a utility company UGI is unique with four subsidiaries operating in distinct markets.

The firm’s most stable business is a regulated gas utility in Pennsylvania (UGI Utilities), which is responsible for approximately 20% of earnings.

The largest portion of UGI’s business involves the distribution of propane throughout Europe (UGI International) and the U.S. (AmeriGas), collectively accounting for roughly 60% of earnings.

The remaining 20% of earnings come from UGI’s midstream assets and marketing business (UGI Energy Services).

As of this month, UGI Utilities has seen minimal disruption on volumes and only a modest increase in uncollectible accounts due to customer payment issues.

UGI’s relationship with the Pennsylvania Public Utility Commission, which regulates the company’s utilities, is constructive from a credit perspective, according to Fitch. This may help UGI recover any material COVID-related costs if needed in the future.

Overall, the utilities side of the business has remained steady and seems unlikely to cause problems that would impact UGI’s dividend safety.

Unlike its utility operations, UGI’s propane distribution companies are not regulated. They can experience volatility due to changes in weather (colder temperatures are better) and economic activity.

These businesses have seen decreased volume from their non-essential commercial and industrial customers (e.g. restaurants, hotels, and school bus fleets) which were impacted by the pandemic.

However, decreased volumes from commercial customers have been partially offset by increased residential demand with more people staying home.

Overall, Fitch anticipates UGI’s 2020 propane volume declining 5% in the U.S. and 15% internationally.

Although earnings will take a hit, it’s a relatively modest impact and management is optimistic volumes will increase as the global economy begins to recover.

Finally, UGI Energy Services operates in a more fragile part of the natural gas value chain – midstream assets.

These include natural gas storage, gas peaking plants, and gas pipelines, primarily serving the northeastern corner of the U.S. with a heavy presence in Pennsylvania.

The natural gas served by these assets predominantly comes from the low-cost Marcellus and Utica formations.

This year natural gas prices have hovered near levels required for producers to breakeven.

With around only 60% of this segment’s contracts containing take-or-pay provisions, UGI is exposed to some volumetric risk should production decline in response to weak gas prices.

But despite lower gas prices, UGI has not seen any material impact on volumes or margins thus far.

And, at the time of writing, the futures market is predicting natural gas prices to rebound to profitable levels for producers by the end of September.

It's worth keeping an eye on this part of UGI’s business given the uncertain outlook for many energy producers, but as of today there are no major red flags.

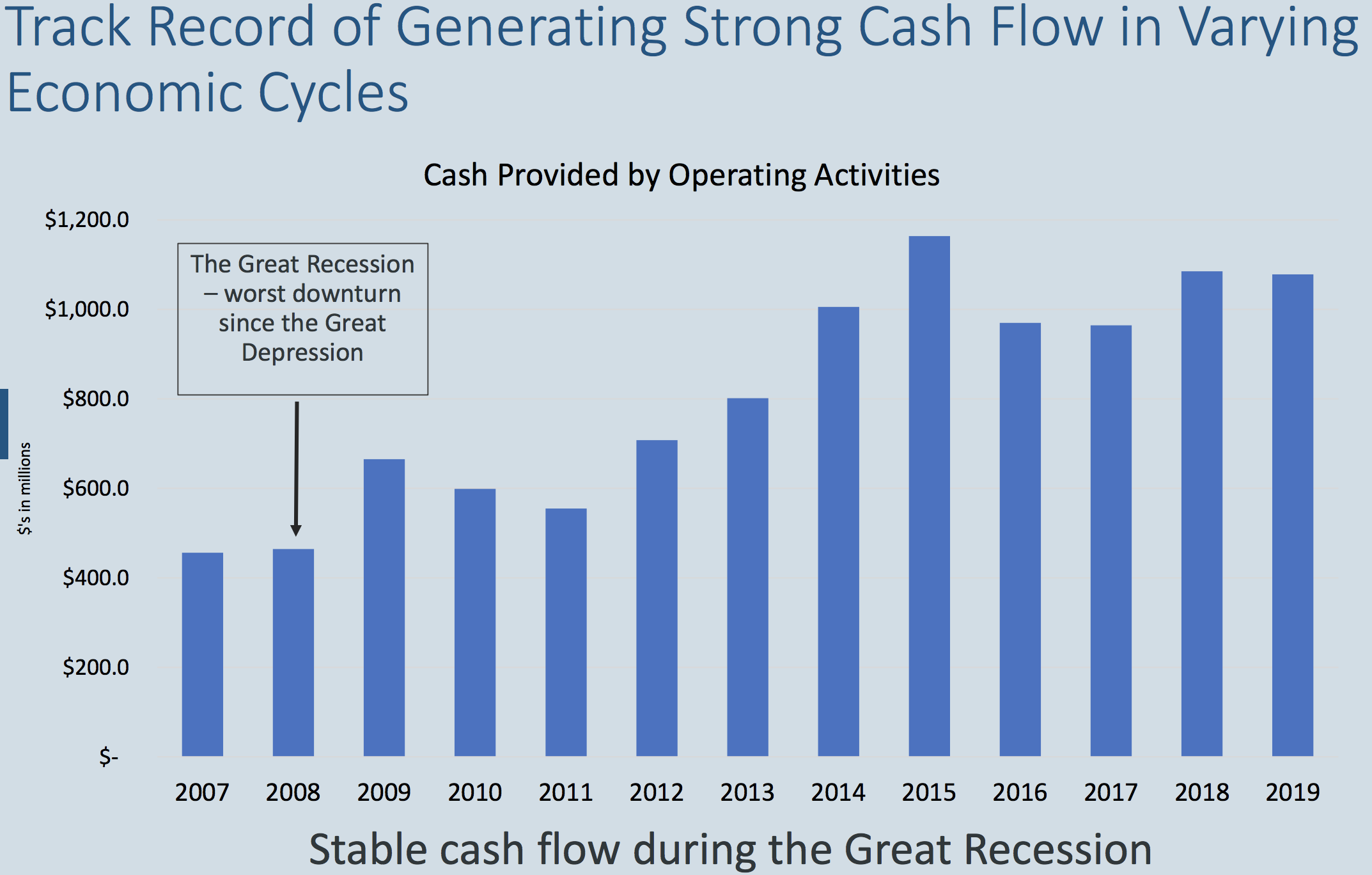

From a financial perspective, UGI’s businesses have proved solid cash flow generators over the years thanks to the essential nature of their services.

Even during the financial crisis of 2007-09, cash flow from operations held steady and grew.

This resilience has manifested again, helped in part by favorable weather in April, as UGI’s operating cash flow increased 4% year-to-date compared to 2019.Source: UGI Investor Presentation That said, management believes the pandemic will reduce 2020 adjusted EPS by around 10%. This would imply a payout ratio in the range of 50-60%, which is above managements long-term target of 35-45%.

But given the stability of cash flows and eventual economic recovery this increased payout ratio doesn’t signal a significant concern for the dividend as it still represents a healthy level for most diversified utilities.

However, retaining less cash flow after paying dividends could slow UGI’s deleveraging efforts.

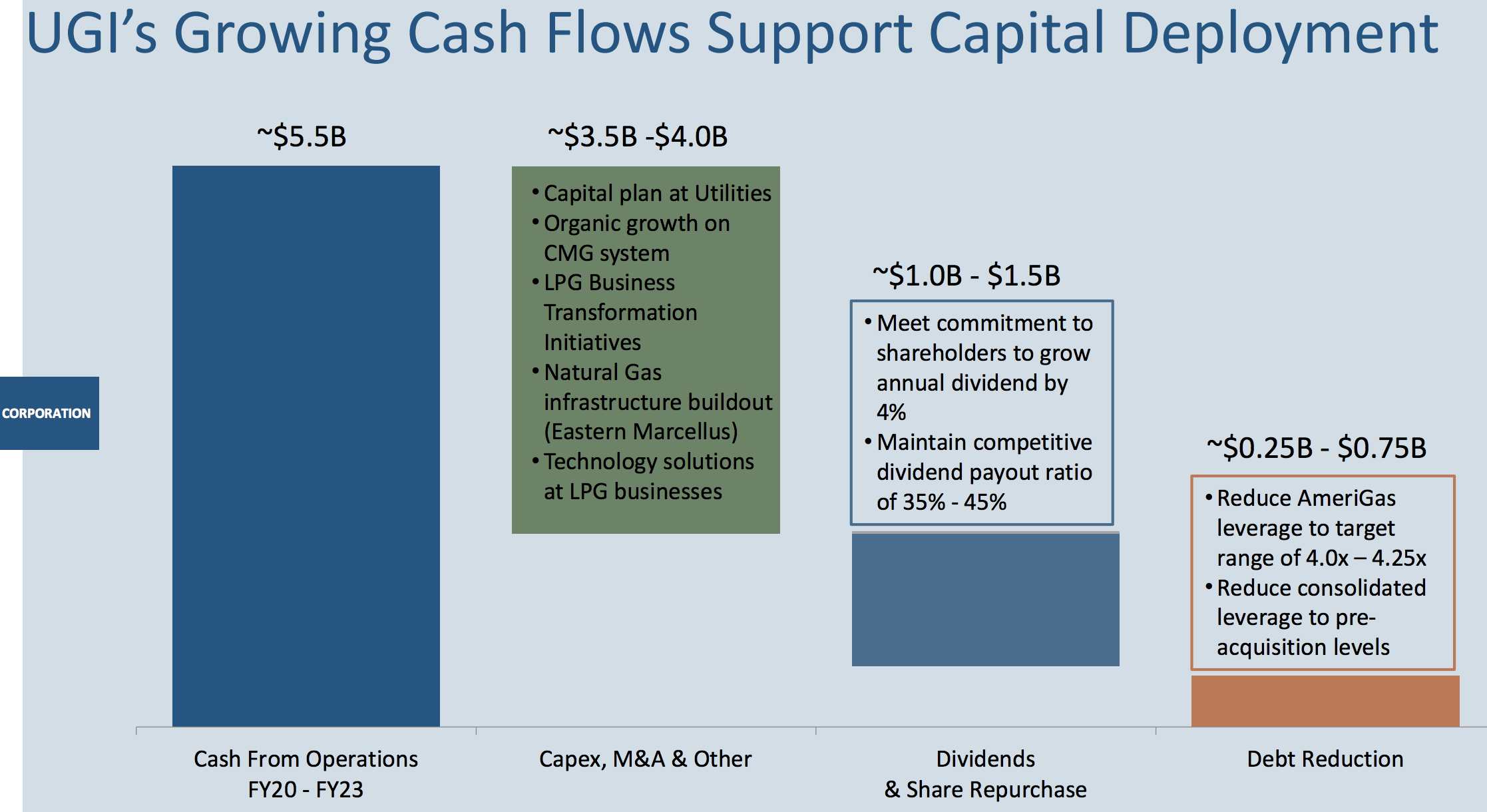

As noted earlier, UGI plans to reduce leverage by growing EBITDA and paying down $250 million to $750 million of debt between fiscal 2020 and fiscal 2023.

During this period UGI expects to generate nearly $1.4 billion of operating cash flow annually and invest upwards of $1 billion per year in capital spending and acquisitions. Source: UGI Investor Presentation This plan would result in close to $400 million per year of free cash flow available for dividends, share repurchases, and debt reduction.

UGI’s current dividend costs about $270 million annually and takes priority over share repurchases, according to management.

Should softness in the propane market intensify and persist for longer than expected, we believe UGI would first consider reducing share repurchases and M&A activity to prioritize the dividend’s safety and debt reduction.

It’s also worth noting, from a financial flexibility perspective, UGI has no debt maturities until 2024, no debt covenant issues, an investment grade credit rating, and $1.6 billion of liquidity. The firm appears well positioned to ride out the storm.

It would likely take management losing faith in the long-term earnings power of its propane businesses and midstream operations to consider cutting the dividend. Based off what we know today, that seems very unlikely.

In fact, in April management raised UGI’s dividend for the 33rd consecutive year. Plus, UGI has paid a dividend without interruption since 1885, a track record it would like to maintain.

We will continue monitoring UGI’s earnings trajectory and its ability to deleverage in a timely manner.

If the pandemic’s impact on the business becomes more significant, we would consider downgrading UGI’s Dividend Safety Score until its balance sheet improves.

For now, we believe UGI is well positioned to continue its demonstrated commitment to a stable and growing dividend.