3M Requires Patience as Macro and Legal Challenges Persist But Dividend Remains Safe

Another quarter, another disappointment. That's been 3M's (MMM) story for much of the past two years, and the trend continued earlier this week.

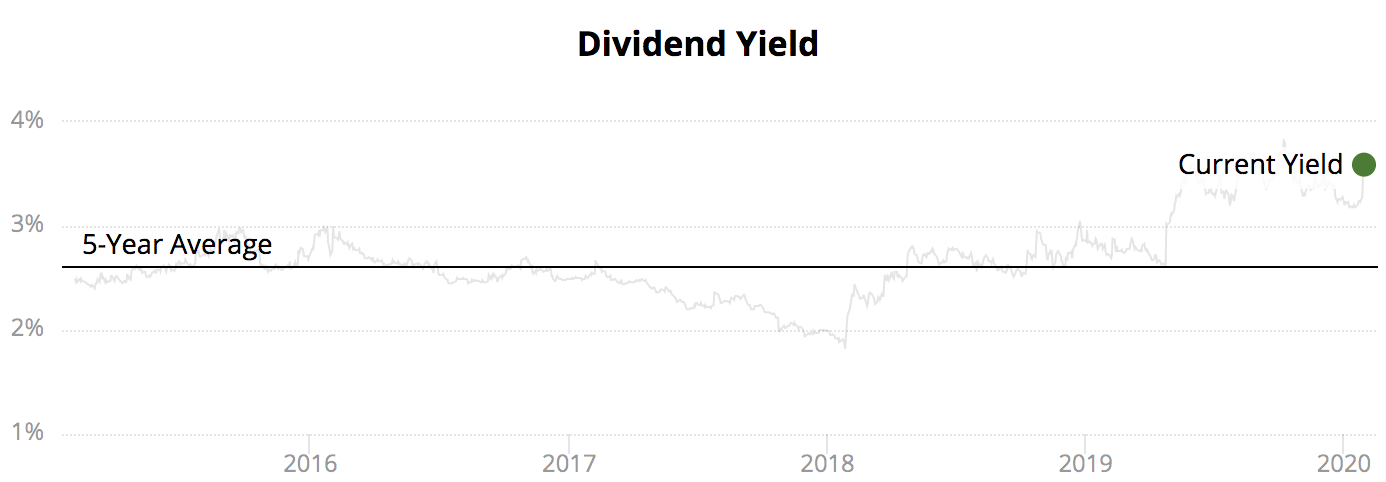

3M reported fourth-quarter earnings on Tuesday, sending its shares falling by about 6%. The company's stock price is nearly unchanged since 2015, and 3M's dividend yield sits near its highest level since the financial crisis.

Source: Simply Safe Dividends

Macro headwinds, slow-moving restructuring plans, and mounting legal liabilities continue weighing on 3M. The end result last quarter was a 2.6% decline in organic sales and a 16% fall in adjusted EPS.

On the macro front, 3M's reach extends to a wide variety of end markets around the world, including many cyclical industries like automotive, electronics, transportation, and industrial products.

As a result, a company this large ($32 billion in revenue) with over 60,000products and about 60% of its revenue derived internationally is inevitably going to be somewhat sensitive to trends in the global economy.

Unfortunately, U.S. manufacturing activity steadily declined in recent months to its weakest reading since 2009. Meanwhile, global automotive and electronics end markets continued slowing, and China's economic growth hit a 30-year low.

Given this backdrop, 3M's ongoing growth struggles are a little more understandable. Investors historically awarded the stock a premium valuation multiple in recognition of the firm's steadier earnings profile compared to most of its industrial rivals, but that could be changing.

For example, during the financial crisis in 2009, 3M's adjusted EPS fell less than 10%. But in 2019, a year when the global economy continued expanding, the company's adjusted EPS fell by about 15%.

3M's CEO Michael Roman, who took the top job in July 2018, has struggled to get the industrial conglomerate back on track. The firm's revenue is nearly 30% higher than its pre-financial crisis level, so perhaps 3M's operations have sprawled too far and become overly complex to manage.

Regardless of the reason, Mr. Roman has initiated several restructuring actions in an effort to return 3M to profitable growth in 2020. The company revealed plans for additional layoffs this week, bringing its announced employee headcount reductions over the past year to about 3.6% of 3M's workforce.

Management also announced plans to continue consolidating 3M's business structure with hopes of improving accountability, making operations more efficient, and improving customer insights.

Some investors question if these plans are bold enough to move the needle. In the meantime, they must deal with additional "one-time" restructuring charges incurred by the company.

Macro challenges and restructuring plans aside, 3M investors also face uncertainty from mounting legal liabilities related to the firm's so-called PFAS chemicals. PFAS was used in firefighting foams, nonstick coatings, fast food wrappers, water resistant clothing, paints, cleaning products, carpets, and many other consumer and industrial products.

3M manufactured PFAS from the 1950s through the early 2000s. Unfortunately, these widespread chemicals have come under significant scrutiny due to environmental and consumer health concerns.

Specifically, 3M faces a growing number of lawsuits across the country accusing the company's PFAS manufacturing sites of polluting water supplies with these toxic chemicals.

Consumers have also claimed that PFAS has led to higher rates of cancer and fertility issues. 3M denies these allegations, which are admittedly more difficult to prove than the environmental damages.

Sizing up 3M's liability exposure is difficult. Under accounting rules, 3M only has to record a liability when costs are probable and reasonably estimable, leaving a lot of information about its total potential exposure in the dark.

In 2018, 3M recorded litigation-related charges of $897 million due to PFAS matters. That included an $850 million settlement deal with the state of Minnesota to end its natural resources damages lawsuit against 3M, representing one of the largest environmental settlements of all time.

In 2019, 3M recorded additional litigation charges of $762 million primarily related to PFAS, including a $214 million hit in the fourth quarter. Management also noted the company is investigating its other manufacturing sites that might have used PFAS.

With a number of environmental and personal injury lawsuits outstanding against the company, it's concerning to see these liabilities continue growing. Some analysts believe 3M's liability could ultimately exceed $10 billion.

For context, 3M generates around $5 billion to $6 billion in free cash flow annually and carries about $20 billion in debt. While PFAS liabilities are not an existential threat to a company this large, they will likely have a material impact on 3M's balance sheet and cash flow.

Coupled with 3M's falling sales, earnings, and margins, it's not hard to understand why 3M's stock has struggled in recent years. Fortunately, it seems unlikely that 3M's struggles will jeopardize its dividend or result in a dividend freeze.

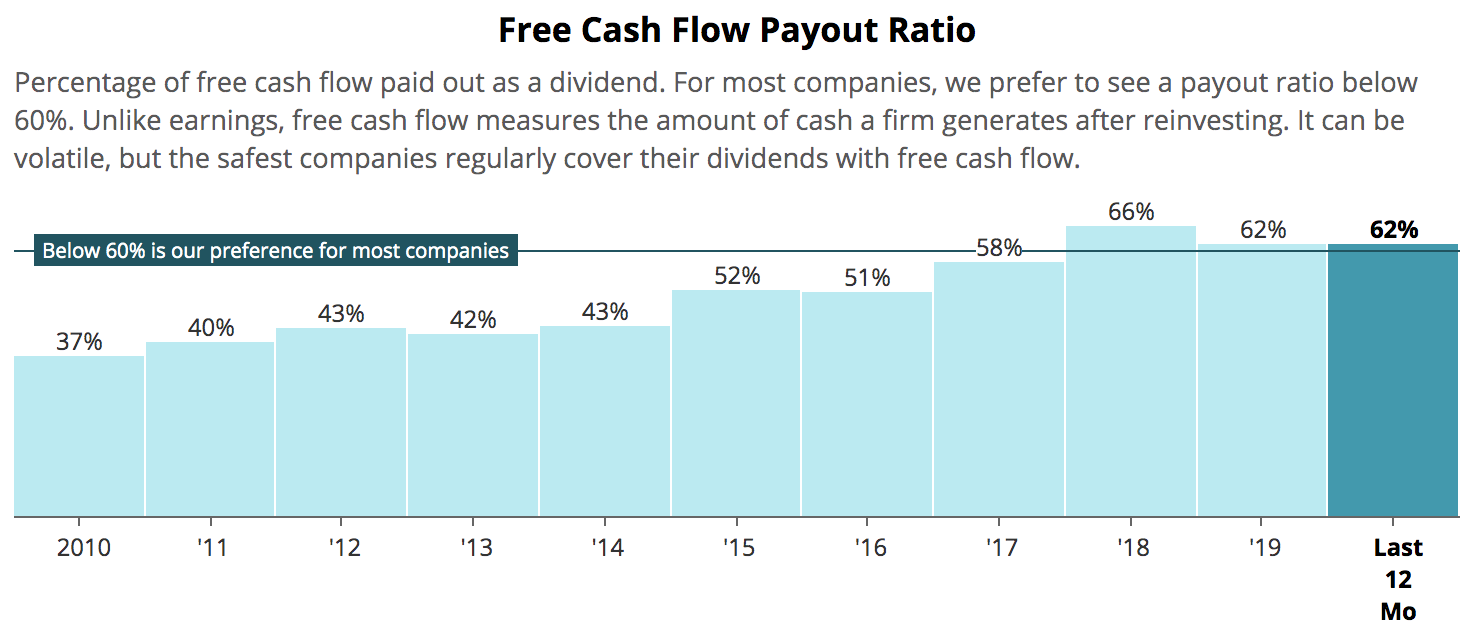

Despite its growth struggles, 3M continues generating a lot of cash. In 2019, 3M's free cash flow increased 10% to $5.4 billion, leaving around $2 billion after paying $3.3 billion in dividends.

A 60% payout ratio is a reasonably safe level for 3M. Although management's guidance deserves some scrutiny, 3M expects to generate $5.3 billion to $6 billion of free cash flow in 2020, indicating that the dividend should remain well covered.

Source: Simply Safe Dividends

PFAS could weigh on 3M's free cash flow generation in the coming years. However, remediation costs would likely be paid out over the course of years or even decades due to drawn out court cases and the multiyear nature of most environmental cleanup work, lessening the annual hit to cash flow.

3M's $2-plus billion in annual retained free cash flow after paying dividends provides the firm with additional financial flexibility to handle PFAS payments, even if the global economy sputters. The company just won't have much ability to create value in other ways, such as acquisitions, share buybacks, and a strong pace of dividend growth.

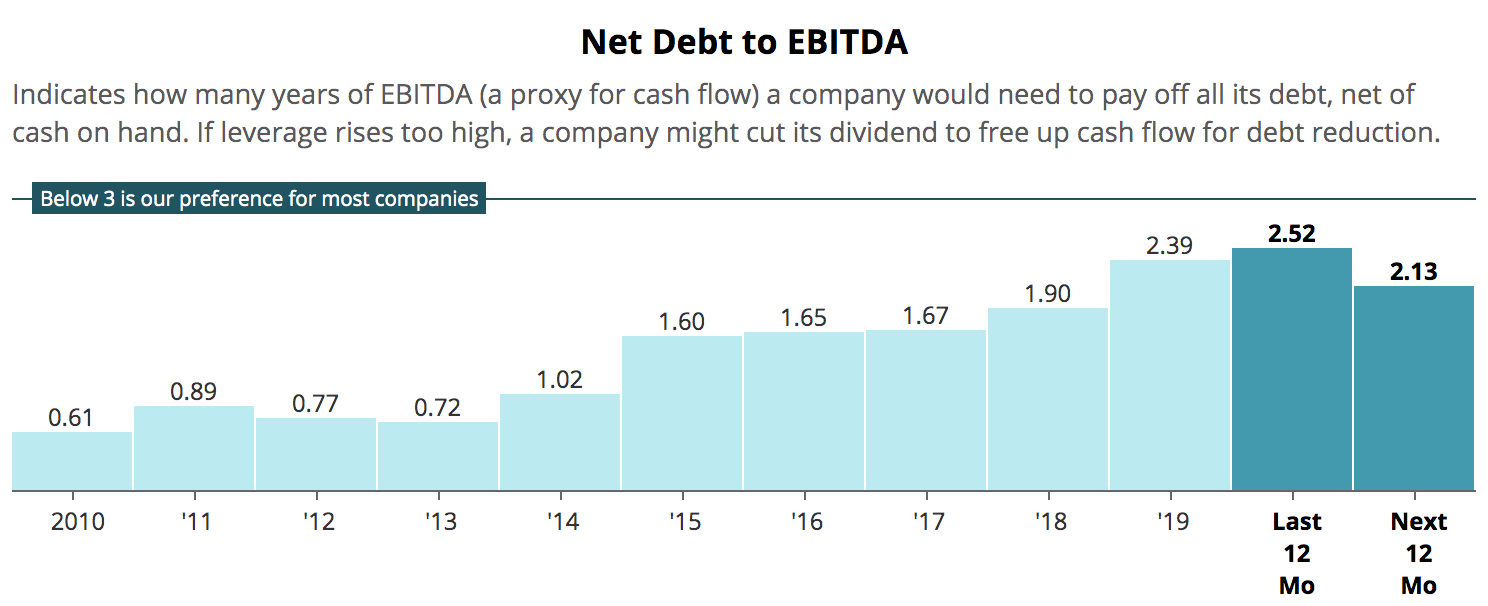

3M's balance sheet remains supportive of the company's dividend safety, too. Leverage has increased in recent years due to 3M's significant share repurchases and its 2019 purchase of healthcare company Acelity in a $6.7 billion deal, the firm's largest acquisition ever.

However, 3M's leverage remains at a healthy level, earning the company an AA- credit rating from Standard & Poor's and providing it with solid access to low-cost financing.

Source: Simply Safe Dividends

If $10 billion is added to 3M's debt due to PFAS liabilities, the company's leverage ratio would rise next year from 2.1x to about 3.3x.

While that's higher than we like to see for most companies, it's unlikely to challenge the firm's Safe Dividend Safety Score. 3M's excellent free cash flow generation would help leverage fall below 3x within two years if all retained cash flow after dividends was directed towards debt reduction.

Management expects 2020 to mark a return to profitable growth for 3M, but investors remain skeptical that the company can meet its guidance calling for 0% to 2% organic sales growth, higher margins, double-digit earnings growth, and lower leverage.

Until 3M demonstrates its restructuring plans are bearing fruit and total PFAS legal costs become clearer, the stock could remain in the penalty box. If the global economy weakens, then 3M's short-term performance could especially remain lackluster.

Despite these challenges, 3M will almost certainly extend its 61-year dividend growth streak in 2020 (likely with an announcement next month). However, the pace of dividend growth could decelerate to a low- to mid-single digit pace. Management likely does not want to increase 3M's payout ratio, and further strengthening the balance sheet seems prudent.

We have owned shares of 3M in our Top 20 Dividend Stocks portfolio since July 2015 and plan on maintaining our position, in part because 3M's valuation has become much less demanding over the last two years.

3M's dividend yield has nearly doubled since early 2018, and the stock's forward P/E ratio of 16.9 now represents an unusual discount compared to the Industrials sector's average P/E ratio of 18.5.

Source: Simply Safe Dividends

Anything can happen in the short term (e.g. 3M's yield shoots above 4% if recessionary concerns mount), but it seems hard to argue that the stock is overpriced unless you believe that the company cannot return to sustained earnings growth in the long term.

Given the pervasiveness of many of the firm's products across so many different end markets, we believe 3M's diversified business will likely at least track global GDP growth over time to become a more valuable company.

This year could mark a welcomed return to growth, but dividend growth investors considering the stock need to be prepared to remain patient. The main overhangs (restructuring and legal liabilities) will take time to resolve while end market volatility could further muddy short-term results.