Simon's Dividend Remains Safe But Don't Expect Much Growth

America's first enclosed mall was built in 1956, and the nation hasn't looked back. About 1,500 malls were built in the U.S. from 1956 through 2005, providing hubs for social gathering and shopping throughout America's booming suburbs.

By 1975, malls accounted for 50% of U.S. retail dollars spent, representing an impressive 13% of GDP. So much property was developed that by 2017 America had an estimated 26 square feet of retail for every person in the country, compared with less than 3 square feet per capita in Europe, according to Time.

But now, in the age of Amazon, many areas of brick-and-mortar retail, including malls, are being forced to right-size their footprints.

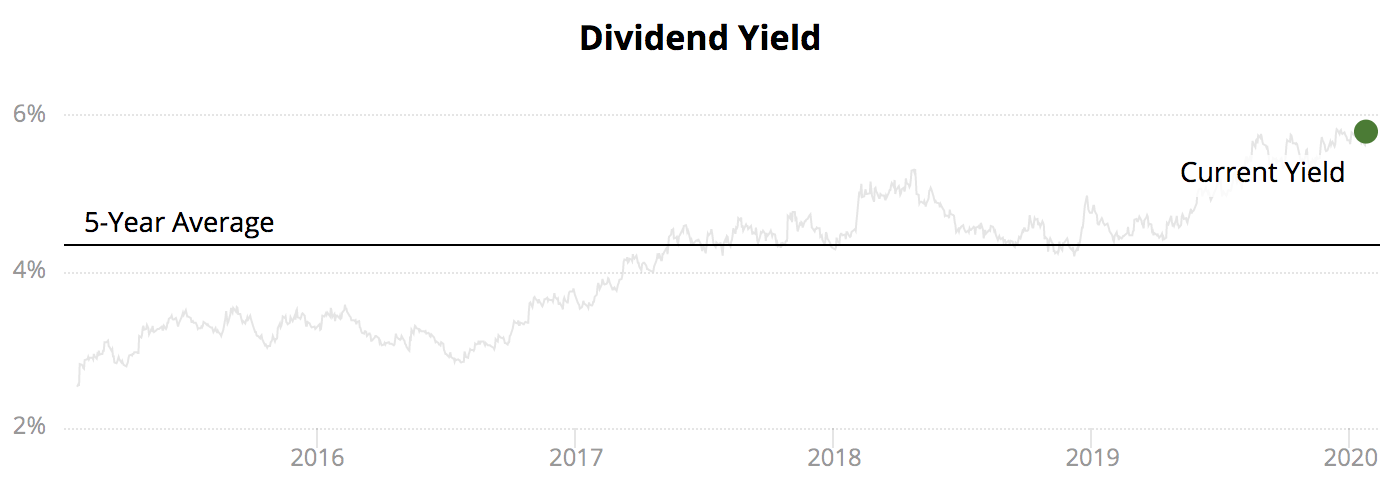

As the nation's largest mall REIT, Simon Property Group (SPG) is no stranger to the "retail apocalypse" concerns. The stock's nearly 6% dividend yield, its highest level since the financial crisis, reflects an increasingly cautious investor base.

Source: Simply Safe Dividends

The good news for income investors is that Simon's dividend continues to look secure thanks to the REIT's solid cash flow and conservative balance sheet.

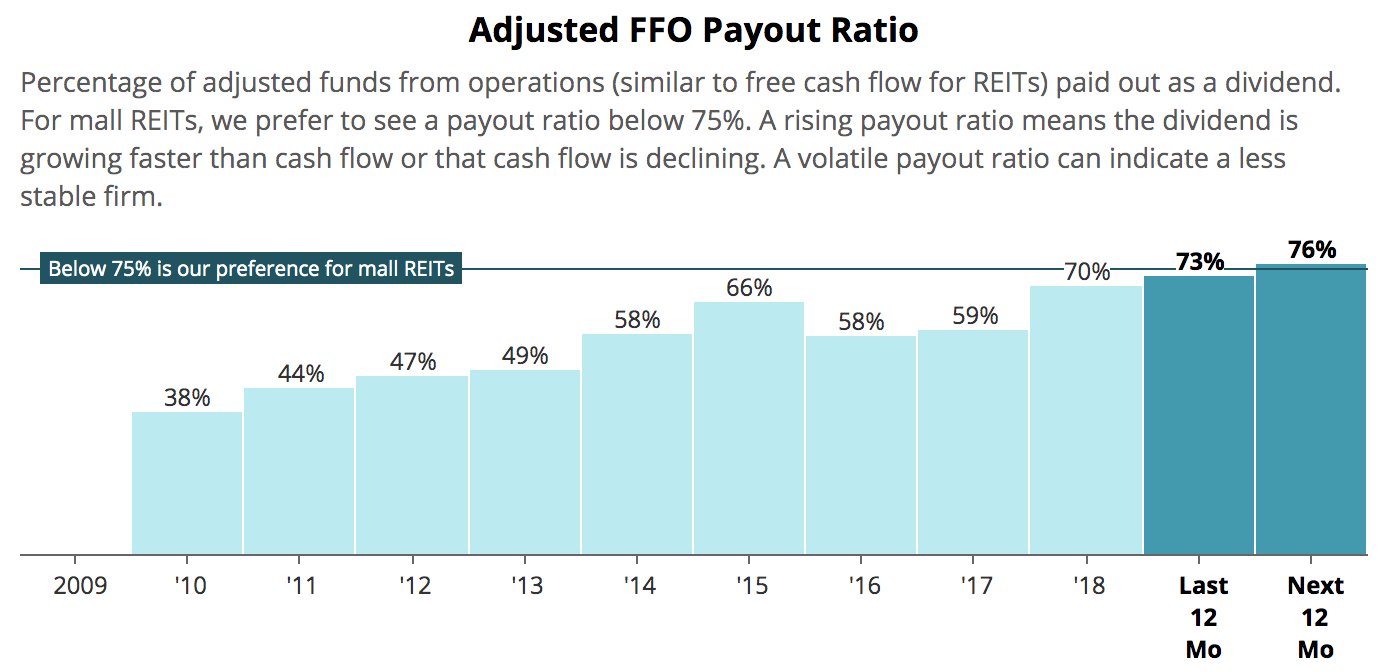

Analysts expect Simon to generate about $3.9 billion in adjusted funds from operations (AFFO) over the next 12 months, which more than covers the firm's $3 billion annual dividend commitment.

Although Simon's payout ratio has roughly doubled over the past decade, it remains at a reasonable level for mall REITs. However, investors probably shouldn't expect much more than 2-4% annual dividend growth going forward given the company's sluggish cash flow growth.

Source: Simply Safe Dividends

Besides its healthy dividend coverage, Simon also holds $3.6 billion in cash and has available borrowing capacity of $6.1 billion under its credit facilities. Combined with its excellent A credit rating from Standard & Poor's, Simon's liquidity and balance sheet are in good shape.

Therefore, Simon's relatively high dividend yield appears to be more of a reflection of the company's weakening growth prospects rather than an imminent dividend safety issue.

The mall business model is evolving, creating challenges in the form of financially challenged retailers, disappearing anchor stores, and an escalating need to redevelop certain properties.

For example, some of Simon's largest tenants include The Gap (3.4% of rent), Ascena Retail (2.2%), Signet Jewelers (1.4%), and Forever 21 (1.4%). Several of these businesses are financially distressed, and each one is closing down a meaningful number of its stores as America's retail right-sizing continues.

Equally problematic, about 31% of Simon's total square footage is occupied by anchor tenants, including troubled department stores such as Macy's (12% of square footage), J.C. Penney (5.7%), and Sears (2.4%).

These retailers contribute less than 2% of Simon's total rent since their primary job is to draw traffic to Simon's 106 malls and 69 premium outlet centers.

However, many of their locations are also closing, forcing Simon to find new anchor tenants or redevelop the space with hopes of keeping its malls filled with enough consumers to support its smaller tenants.

Simon has performed better than most mall stocks, but these challenges have still hurt its business.

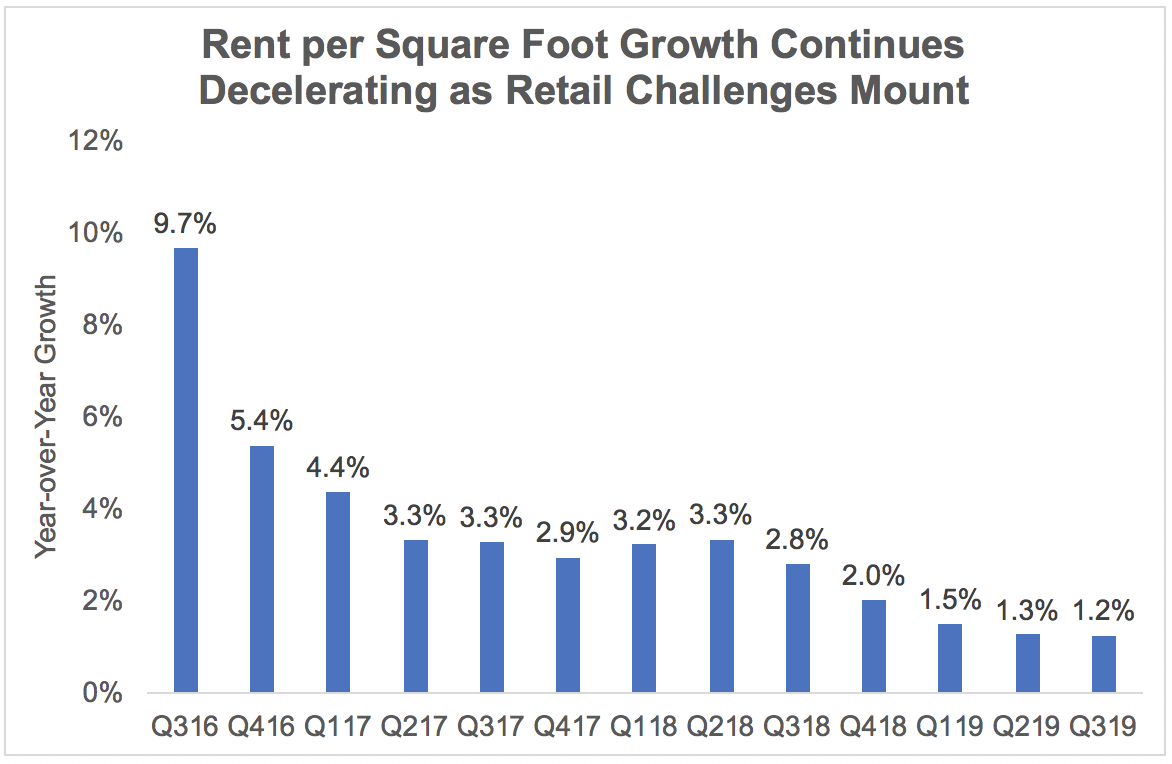

Over the last three years, for example, Simon's occupancy has edged down from 96.3% to 94.7%. Meanwhile, the REIT's rent per square foot has continued increasing, but its year-over-year growth has decelerated to just 1% to 2% in recent quarters.

Source: Simply Safe Dividends

Simon has responded to these headwinds largely by initiating a major redevelopment plan intended to create "modern, innovative, live, work, play, stay and shop communities." Redevelopment activities are underway at more than 30 of Simon's 200-plus properties.

Space previously leased to department stores is being swapped out for restaurants, gyms, hotels, offices, and entertainment centers. Some malls are seeing even more intensive overhauls.

For example, Simon's Northgate mall in Seattle has been around since the 1950s and was one of the first enclosed malls in America. Today, about 60% of the property is being torn down to be replaced with residential and office towers.

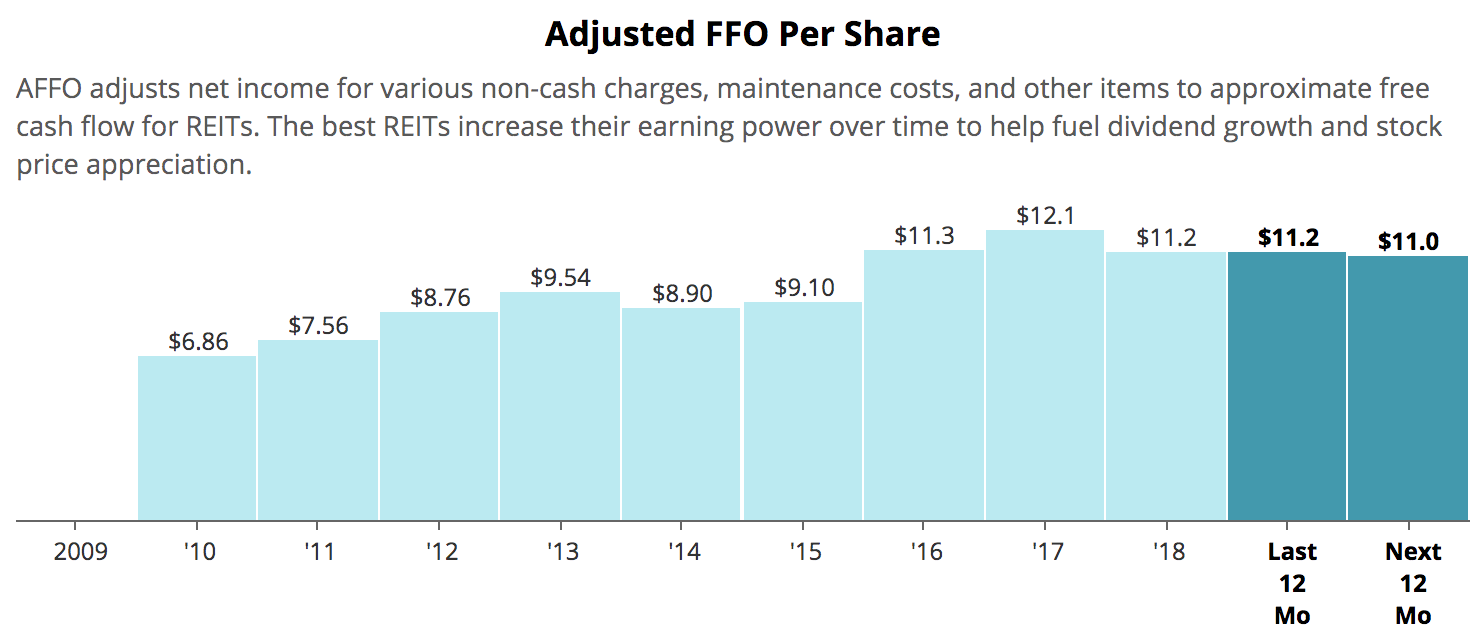

As a result of retailer challenges and higher redevelopment spending, Simon's AFFO per share has stalled in recent years. In mid-2019 management said the company's redevelopment plans were only about a third finished, suggesting it could take several more years to get the entire portfolio better aligned with today's real estate trends.

Source: Simply Safe Dividends

Bullish investors point to the staying power of Simon's "Class A" malls, but the company's extensive redevelopment activities suggest that the long-term outlook for many of these properties isn't great without some heavy lifting.

Simon's proactiveness to prepare the firm for the future is welcomed, but it comes at a steep cost. Rather than being able to run its existing properties for cash (under $200 million in maintenance capital expenditures each year), Simon has earmarked $1.4 billion in total costs for its current slate of redevelopment projects, with more spending expected in future years.

Investors have to trust that these potentially disruptive investments will earn a healthy return, and that risks posed by tenant bankruptcies, unfavorable lease modifications, and store closures will remain manageable during this evolution.

Even then, it's hard to say if this redevelopment spending will be enough to combat the secular decline in malls. Simon's results have held up relatively well thus far (thanks to its tenant diversification and well-located properties), but the retail revolution still feels like it is in the early innings.

Fortunately, Simon has the balance sheet and cash flow needed to manage through its current slate of investments without jeopardizing its dividend, even if the firm has to absorb a few blows from troubled retailers.

However, investors considering the stock will likely need to stay patient for at least a couple of years. Simon has to demonstrate that it can return its business to a stronger pace of profitable growth as the value proposition of traditional malls continues to erode.

As conservative investors with fairly concentrated portfolios (20-30 holdings), we prefer to invest in businesses with clearer paths to long-term growth. The fast-changing nature of the retail sector often does not help with that objective.

With that said, Simon's safe dividend yield near 6% and strong balance sheet provide some downside protection for income investors who are interested in playing the role of contrarian and willing to accept the mall industry's risks.