Alliance Resource's Dividend Safety Score Downgraded to Unsafe on Mounting Coal Headwinds

About 60% of America's coal is mined by companies that have been through bankruptcy in the past five years, according to data cited by The Wall Street Journal.

Only three of the 10 largest U.S. coal producers have not declared bankruptcy during that period, demonstrating the industry's challenges (high capital intensity, secular decline in coal demand, cheap alternatives such as natural gas, etc.).

Alliance Resource Partners (ARLP) is one of the few major producers that has not only remained solvent but also continued paying distributions, thanks to its solid balance sheet and low cost of production.

However, continued deterioration in the coal industry has weakened Alliance's ability to generate the cash flow necessary to comfortably cover its distribution. As a result, we are downgrading the company's Dividend Safety Score to Unsafe from a low Borderline Safe rating.

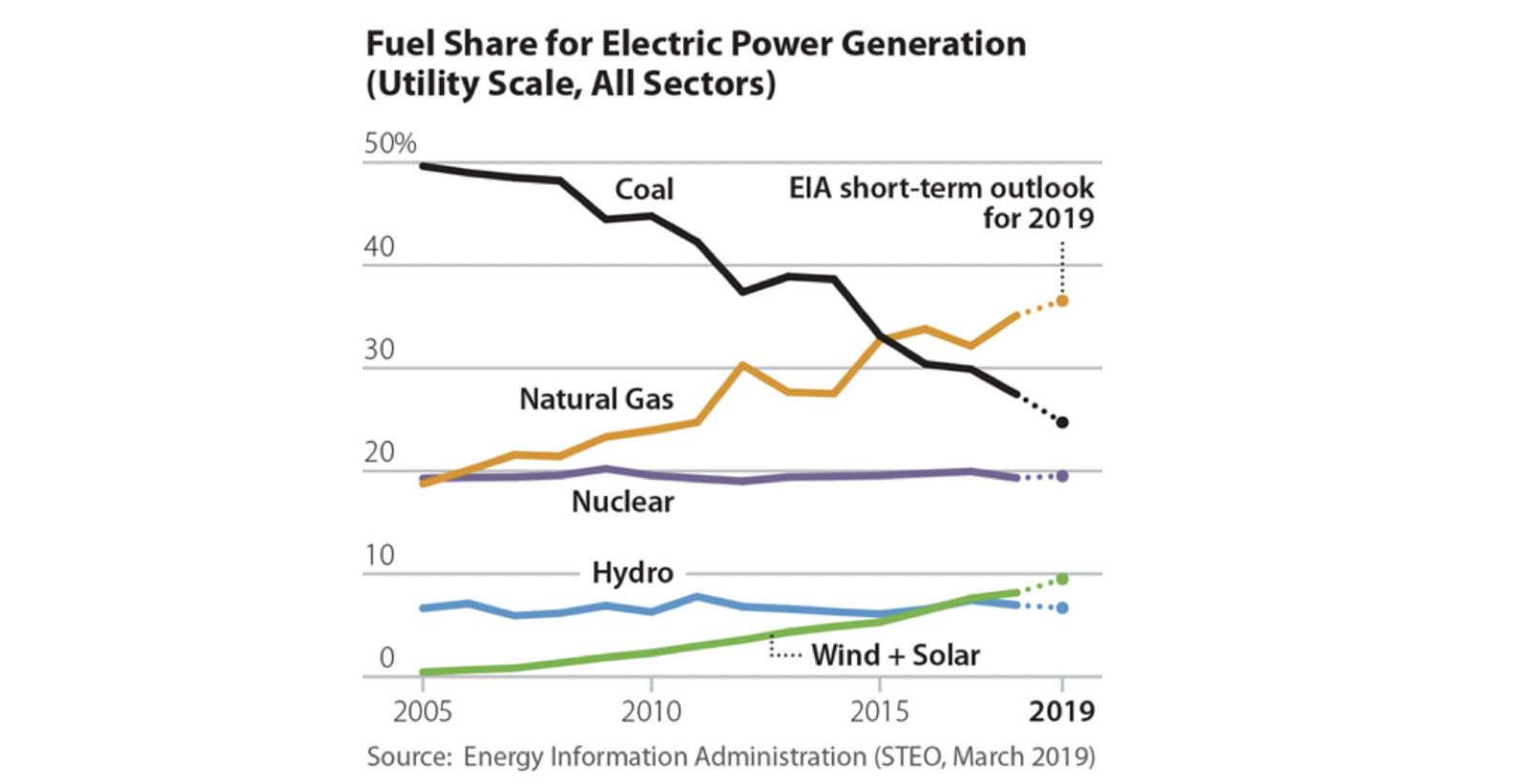

Unlike most cyclical industries, coal is in secular decline. In 2005 coal was the fuel used to generate about 50% of all electric power in America. Today coal generates less than 30% of the nation's power, and the Energy Information Administration projects coal's share of electricity generation to fall to 22% in 2020.

Source: Institute for Energy Economics and Financial Analysis

Electric power consumes the most coal by far, but power plants are focused on reducing their carbon footprint significantly. Cheap natural gas (prices hit a 20-year low in mid-2019) and wind and solar energy are displacing coal in America.

The story is similar abroad. For example, coal generation in Europe fell by about 20% in the first half of 2019. Meanwhile, China, the world's largest coal consumer (and biggest greenhouse gas emitter), could see coal demand begin declining by 2025.

Simply put, it's hard to imagine the decline in coal consumption reversing.

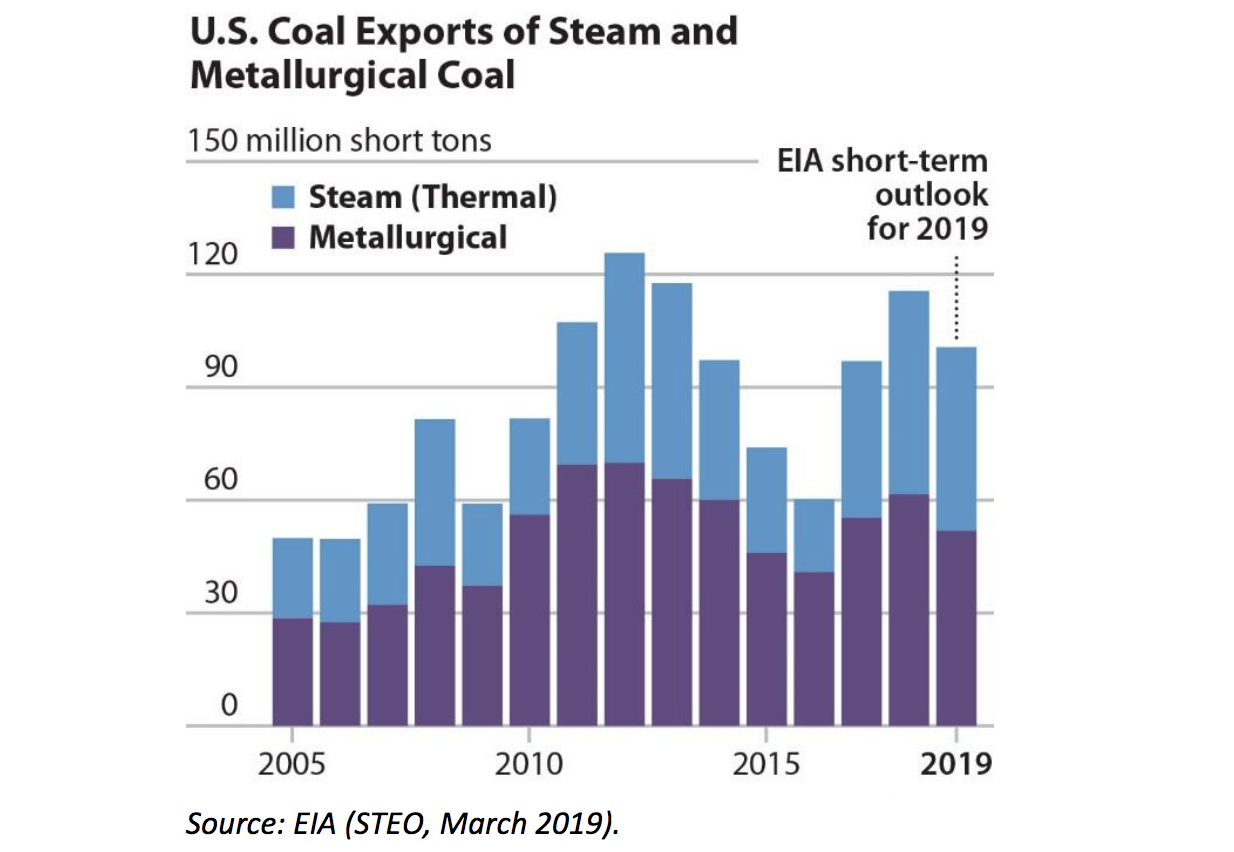

Source: U.S. Energy Information Administration

As domestic demand has continued to fall, desperate producers have increasingly banked on export markets. Exports historically accounted for less than 10% of U.S. coal production, according to the Institute for Energy Economics and Financial Analysis (IEEFA).

However, that changed in 2017 and 2018, with exports rising to 12.5% and 15.4% of tons produced, respectively.

Unfortunately, the U.S. acts as a swing supplier, participating in foreign markets when other suppliers are unable to meet demand. The distance between the U.S. and major importers in Asia and Europe renders the economics borderline except during the strongest markets, according to energy blog iamrenew.

As a result, U.S. coal exports are volatile from one year to the next.

Source: IEEFA

With countries worldwide working to reduce their coal consumption, today's elevated coal exports seem unlikely to prove sustainable. Excessive coal stockpiles in Europe, transportation difficulties in America, and cheap liquefied natural gas (LNG) exports are some of the challenges facing the coal export market.

Next year is setting up to be a difficult one for America's coal miners as some production that was finding a home in fickle international markets likely returns to the U.S., where consumption continues falling.

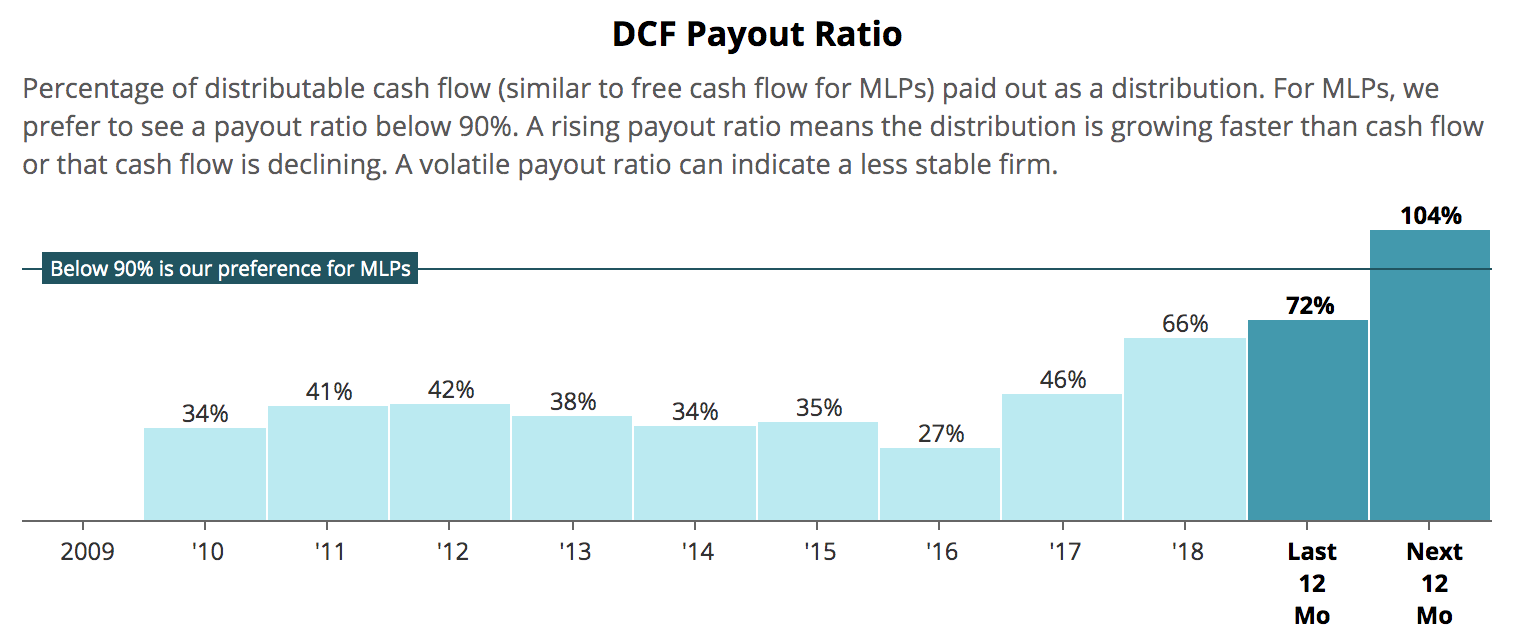

Alliance Resource and others are bracing for a correction. The challenging outlook for coal production and prices has weighed on Alliance's distributable cash flow. In the year ahead, the firm's cash flow may not cover its distribution for the first time in at least a decade.

Source: Simply Safe Dividends

Despite the market's skepticism over the distribution's safety (as demonstrated by the stock's 20% distribution yield), management still sees a path to maintaining the current payout if Alliance can secure the volume it needs:

"As we look at the distribution going into 2020, first off, we think 2020 will definitely be – it's going to be a correction year for the industry. And I think with that correction year we should be coming out of 2020 a lot stronger and be in a position to have coverage ratios greater than 1x and closer to what we've experienced in the past.

As we look at 2020 and we stress test the opportunities in front of us, it really comes down to what kind of volume can we secure. And based on what we have targeted, if we can achieve our objectives, we believe that we can have a distribution at current levels at 1x coverage ratio...if we do our job then we can achieve the sales commitments that we have targeted, and we should be able to sustain this distribution." – CEO Joseph Craft

Management cut the distribution by 35% in April 2016 to strengthen Alliance's balance sheet in light of a weak coal market, so another reduction would not be surprising given the industry's current state and the potential for some customers to defer their purchases as the transition away from coal continues.

Even if the distribution remains covered next year, a cut could still be necessary to improve Alliance's ability to build its oil and gas minerals business, which represents the firm's attempt to gradually diversify away from coal.

Although Alliance's financial leverage remains conservative, in October 2019 management said that the firm was struggling to access debt capital markets on favorable terms, blaming recent activity by several distressed competitors that has rattled investor confidence.

Management plans to wait for conditions to improve before accessing debt markets. However, if financing conditions do not rebound, then Alliance hinted on its third quarter earnings call that it would look at reducing the distribution to maintain its balance sheet.

Overall, the coal industry likely faces a prolonged secular decline as the world seeks out cleaner energy. It's difficult to imagine many coal miners becoming larger, more profitable businesses in the long term as growth pressures rise.

Although Alliance has been managed more conservatively than most of its peers and is not a high-cost producer, it is still not immune from the industry's challenges, which appear to be mounting in the year ahead.

With access to capital markets tightening up, a core product in secular decline, dependence on volatile export markets, and little to no excess cash flow expected to be retained after paying distributions (at least in the short term), Alliance may not be a reliable income investment.

Expectations don't look demanding and it's always possible the coal market isn't as bad as investors fear, but our preference as conservative investors would be to move on to other businesses that have safer payouts and clearer paths to becoming more valuable enterprises in the long term.