Ryder's Dividend Continues to Look Safe Despite Weak Used Truck Prices

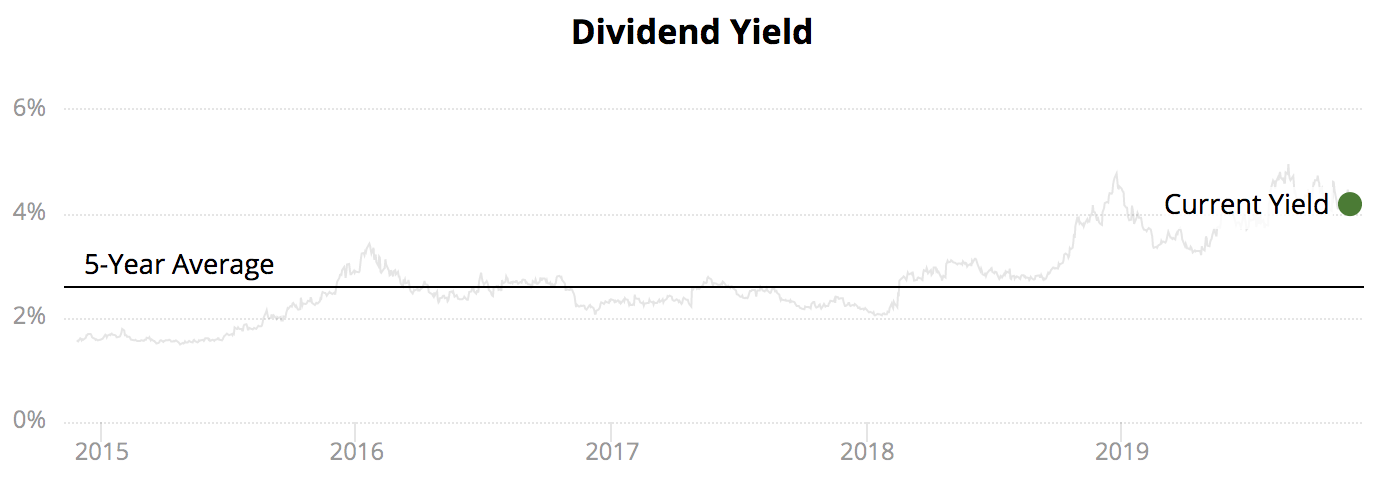

Ryder (R) has paid uninterrupted dividends since 1976 and increased its payout by 10% annually since 2005. However, Ryder recently encountered some challenges, sending its dividend yield above 4% to sit near its all-time high.

Source: Simply Safe Dividends

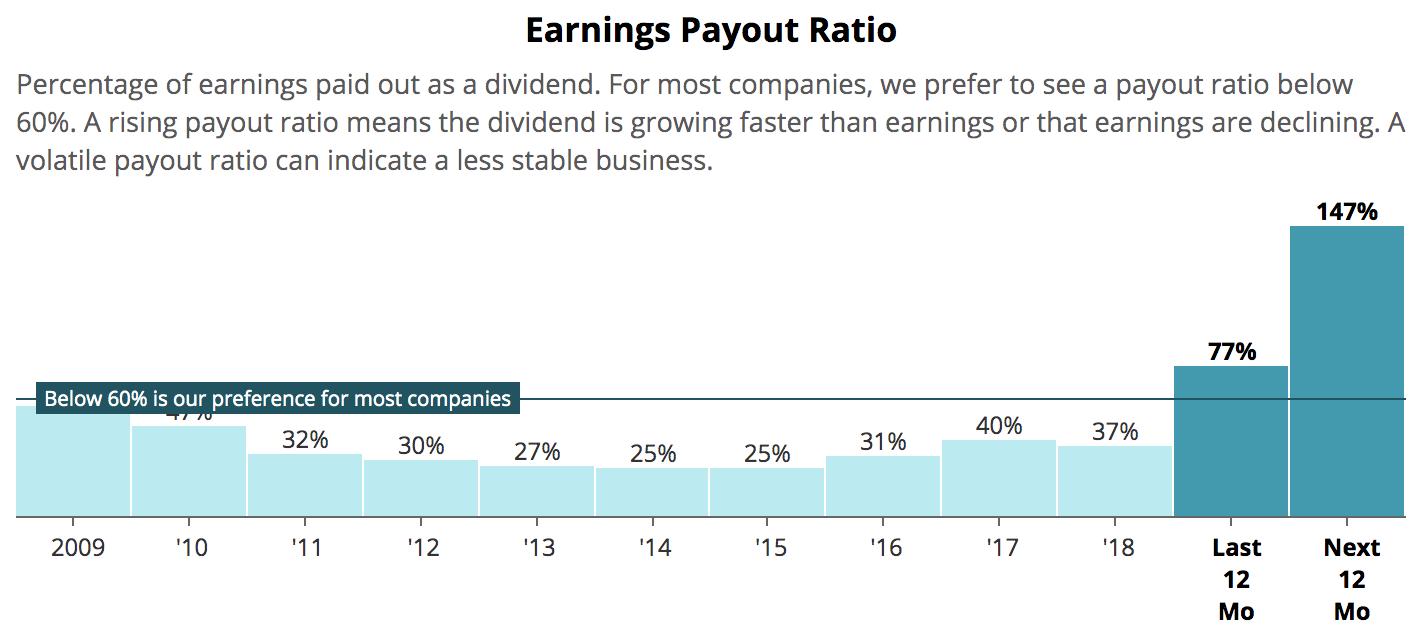

Ryder's payout ratio is also expected to surge above 100% in the next 12 months due to a projected decline in earnings. Some investors are concerned about the safety of Ryder's dividend, but we believe the company's payout remains secure.

Source: Simply Safe Dividends

Ryder has been in business for more than 80 years. The company's largest segment, Fleet Management Solutions (61% of revenue), provides vehicles, maintenance, and related services to businesses that need a fleet of trucks to move products to their customers. About two thirds of the segment's revenue is from contractual lease agreements with an average term of around 6 years.

Source: Ryder Investor Presentation

Ryder purchases trucks at a discount due to its volume, provides guaranteed maintenance to improve customers' uptime and lower their costs, and then sells the vehicles after their leases expire through used truck retail centers.

The rest of Ryder's business consists of Supply Chain Solutions (26% of revenue), which includes managing customers' distribution centers and freight traffic needs, and Dedicated Transportation Solutions (13%), in which Ryder supplies the truck and a driver to make deliveries on behalf of customers.

Due to the cost and complexity of vehicles and maintenance, a shortage of truck drivers, and dynamic supply chains, many companies prefer to outsource their transportation and logistics needs to firms such as Ryder.

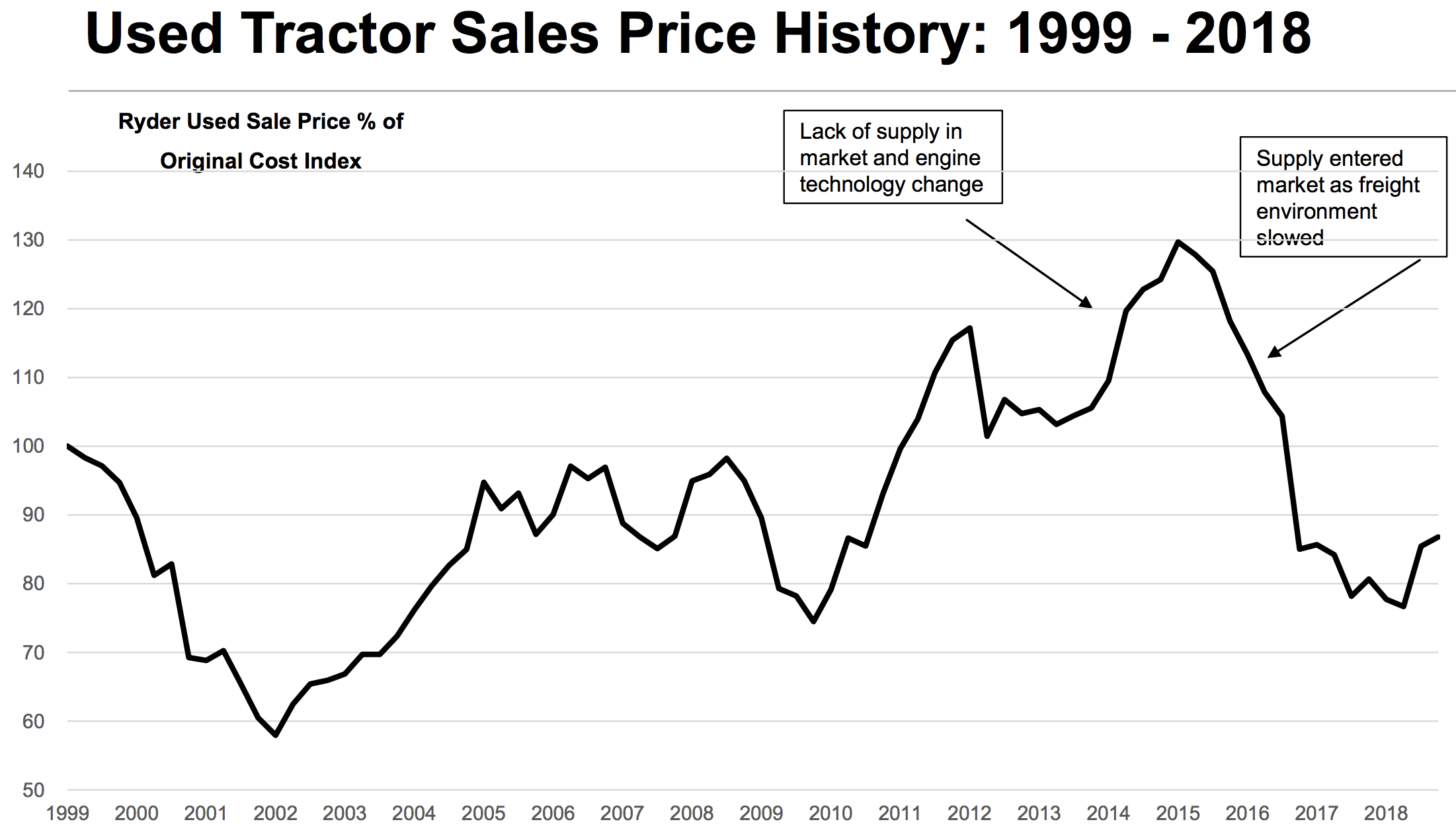

Although about 80% of Ryder's earnings are generated from multiyear contracts with customers, providing predictable cash flow, the business has faced pressure from weak used vehicle prices.

Ryder signs lease agreements with customers before it buys a new truck. The agreement is priced based on the cost of a new vehicle, which management already knows, and then assumptions are made about how much maintenance will cost over the life of the agreement and how much Ryder will receive when it sells the vehicle after the lease ends.

Unfortunately, used vehicle prices are much more challenging today than management anticipated when it signed some leases years ago.

Following the financial crisis, used truck prices surged since few trucks were built during the recession and inventory was low. Truck production began increasing to meet demand, right before the freight environment (and thus demand for used trucks) began to slow in 2016.

As a result, prices have fallen at the fastest pace management has seen in at least 25 years, and Ryder now expects used vehicles be priced at "historically low levels" over the next two years.

Source: Ryder Investor Presentation

Accounting rules require Ryder to record non-cash depreciation charges to its vehicles to reduce their book value to their estimated residual (i.e. salvage) values over the life of these assets.

For example, if Ryder bought a truck for $100, leased it out for 5 years, and believed it could sell the used vehicle for $50 at the end of the lease, the company would depreciate its truck by $10 per year ($100 purchase price – $50 residual value = $50 of total depreciation, recorded as $10 per year over 5 years).

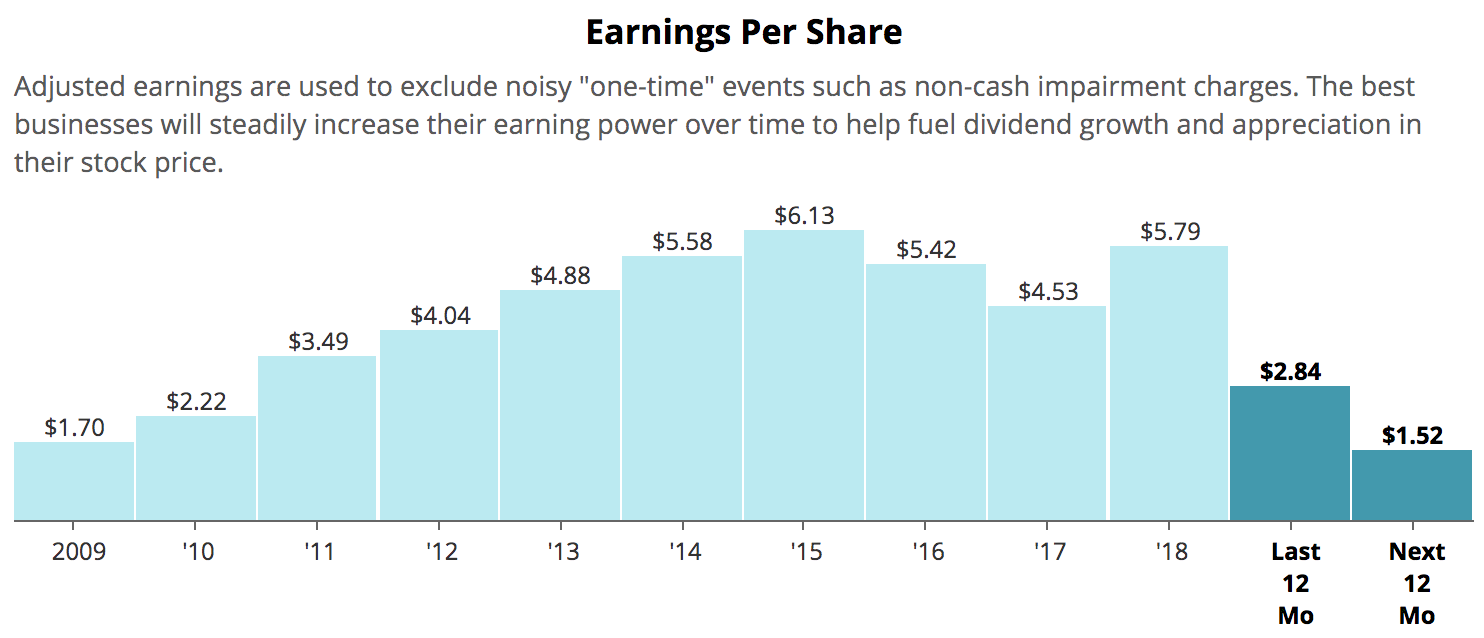

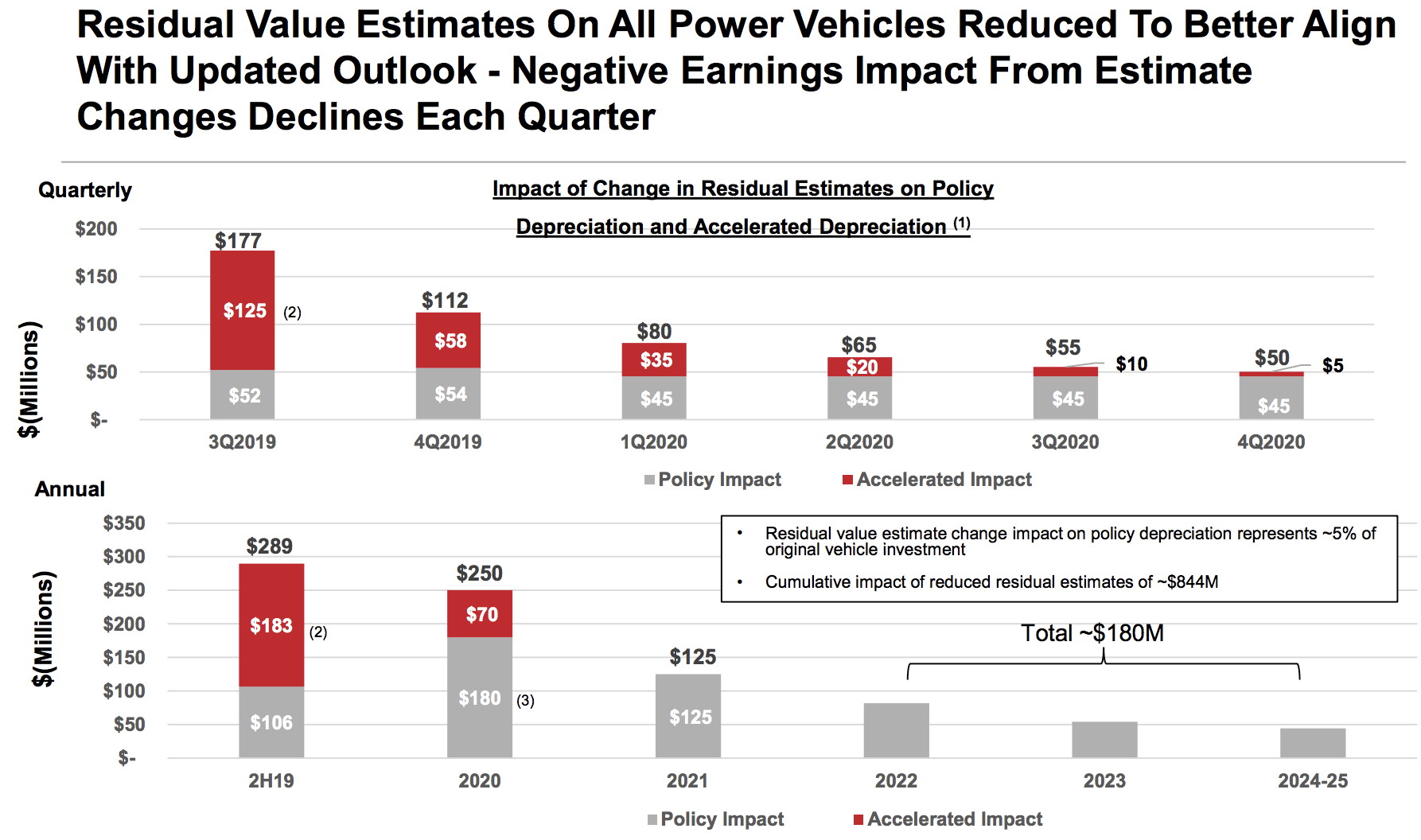

Unfortunately, Ryder hadn't anticipated how weak the used vehicle market would be when it signed new leases years ago. As a result, last month Ryder announced it needed to take accelerated depreciation charges to better align the book value of its vehicles expected to be sold over the next few years with their lower estimated residual values.

These larger, accelerated depreciation charges are depressing Ryder's earnings per share in 2019 and 2020, driving the company's payout ratio above 100%.

Source: Simply Safe Dividends

From a cash flow perspective, the cumulative impact of Ryder's reduced residual estimates is $844 million. In other words, Ryder will still receive proceeds from selling its used vehicles, but over the next few years the firm now expects to receive $844 million less than management previously accounted for.

Source: Ryder Investor Presentation

For context, this estimate change only represents approximately 5% of the original vehicle investment Ryder made.

More importantly, Ryder's operating cash flow is expected to be $2.1 billion in 2019, with another $450 million added from used vehicle sales, which historically accounted for 20% to 25% of the firm's total annual cash flow generated.

Before paying dividends, Ryder must reinvest to maintain and grow its fleet of vehicles. Ryder's capital expenditures are lumpy, depending on how much new business the firm gains and the timing of replacement spending on its fleet.

However, the company's annual maintenance needs total about $2 billion, based on management's comments.

In other words, excluding fleet growth investments (which are not made until a lease contract is signed with a customer), each year Ryder should have on average around $500 million of adjusted free cash flow available.

Ryder's dividend only consumes about $120 million annually, so the company could presumably handle an even deeper or more prolonged slump in used vehicle prices without jeopardizing its payout, assuming its core leasing business continues generating stable results.

Ryder also maintains a BBB investment-grade credit rating from Standard & Poor's, and management expects the negative earnings impact from these vehicles will largely end by 2020.

Going forward, Ryder believes its profitability will organically improve as the lease portfolio turns over and underperforming leases signed prior to 2014, which overestimated used vehicle prices and had higher maintenance costs, exit the fleet.

Leases signed between 2014 and 2017 are expected to yield returns at or above management's 10-12% return on capital target. These leases are benefiting from better-than-priced maintenance costs since Ryder raised pricing related to maintenance costs several years ago. Leases signed after 2017 are expected to see returns above Ryder's target levels, even after the residual value estimate change.

Simply put, cyclical weakness in used vehicle pricing does not appear to threaten Ryder's dividend safety or long-term outlook. The company's elevated payout ratio is more noise than news, and the contractual nature of Ryder's business continues providing enough reliable operating cash flow to protect the dividend despite the truck market's volatility and capital intensity.