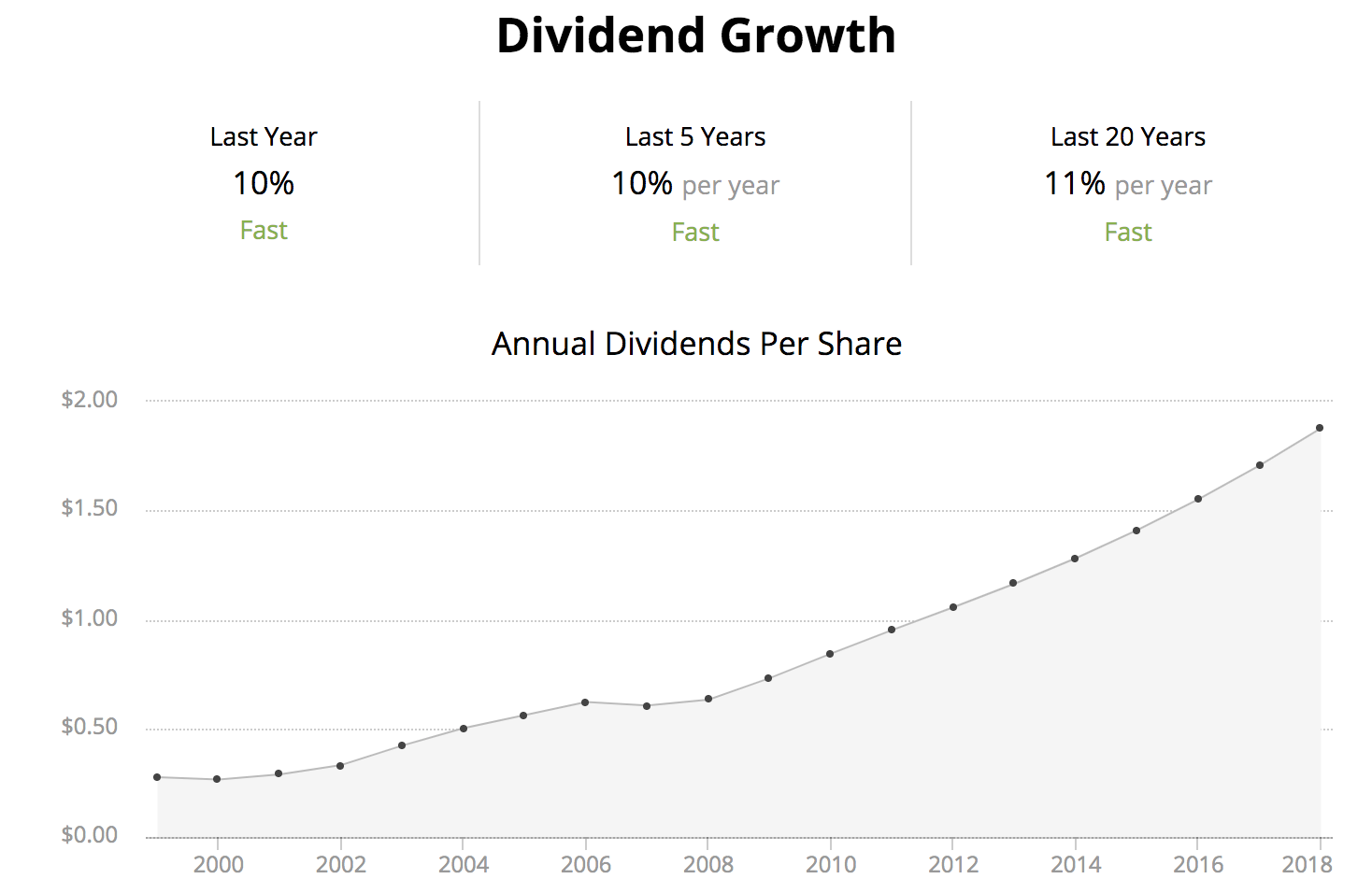

Imperial Brands (IMBBY) boasts an impressive track record of raising its dividend by 10% each year for the past decade, thanks to the predictable cash flow its tobacco business has historically generated.

Source: Simply Safe Dividends

However, shifting consumer habits and regulatory changes have challenged the tobacco market, sending Imperial Brands' dividend yield soaring to 9%.

With a Borderline Safe Dividend Safety Score and the market appearing skeptical of Imperial Brands' ability to maintain its current payout, some income investors are worried what the company's future might hold.

Last week's news didn't help investor sentiment. On July 8, 2019, management announced a revised capital allocation plan and dividend policy that calls for the days of 10% annual dividend growth to end after this year.

Here's an excerpt from the press release:

"The Board reaffirms the 10% dividend growth in respect of the final dividend for the current financial year ending 30 September 2019. The revised dividend policy will be progressive, growing annually from the current level, taking into account underlying business performance. This new policy recognises the Company’s continued strong cash generation and the importance of growing dividends for shareholders, while providing greater flexibility in capital allocation...

Any surplus cash flows will be returned to shareholders via buybacks, enhanced ordinary dividends, or special dividends, depending on market conditions."

Essentially, management hopes to maintain the current dividend, but future growth will likely be minimal since the company needs to retain as much capital as possible to invest in its future and improve its balance sheet.

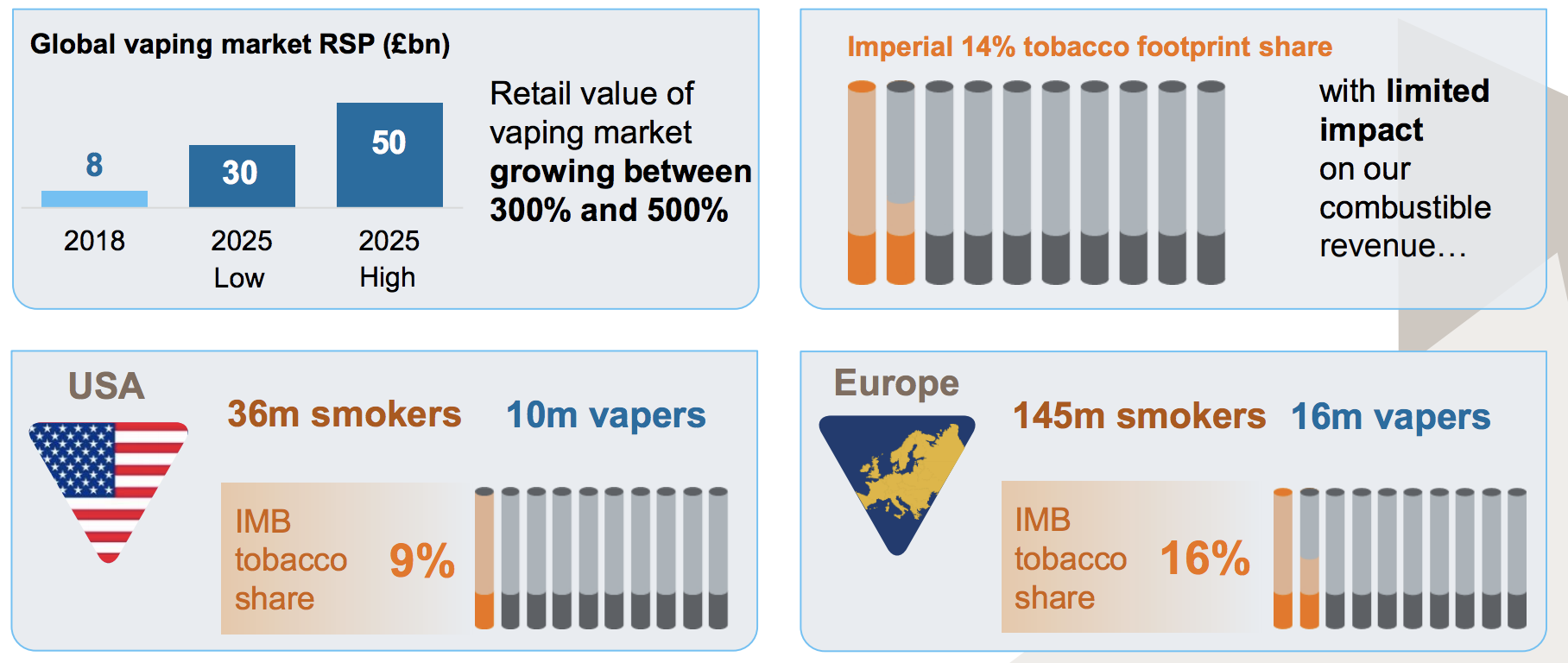

Imperial Brands is one of the smaller players in the tobacco space, with about half as much revenue as Philip Morris International (PM). The firm operates in 160 markets worldwide, but its tobacco share is relatively low, even in its most important markets such as Europe and the U.S.

Source: Imperial Brands

The rise of vaping as an alternative to smoking cigarettes has sent the tobacco giants scrambling to position their businesses for the future of smoking. Per management, about 20% of smokers also vape, and the number of vapers has grown 30% annually since 2011.

Investors are worried that cigarette volume declines could accelerate as consumers and regulators alike continue embracing reduced-risk products.

In fact, Imperial Brands' tobacco volume fell 6.9% in the first half of 2019, though its tobacco business is still growing around 1% to 2% thanks to price increases. Still, investors are looking ahead, and they aren't confident tobacco can remain the big cash cow it has historically been.

Meanwhile, many investors also wonder which companies will dominate next generation products, such as e-cigarettes. Uncertainty swirls around the long-term profitability of these products as well.

Imperial Brands has spent the last decade focused on developing blu, an e-cigarette used for vaping. It has also invested in smaller efforts such as heated tobacco and oral nicotine delivery. However, "next generation products" only account for about 1% of the company's total revenue today.

Slowing its pace of dividend growth will allow Imperial Brands to invest more in these products of the future. The company's dividend already costs it about $2.5 billion per year, so an incremental 10% payout increase would consume another $250 million that could otherwise be used for growth investments and to improve Imperial Brands' financial flexibility.

The company's dividend safety profile appears riskier than most of its peers' due largely to its balance sheet. While Altria and Philip Morris have net debt to EBITDA (leverage) ratios around 2.3 to 2.4, Imperial Brands is a full turn higher near 3.4.

Source: Simply Safe Dividends

Management wants to maintain an investment grade credit rating and has stated a desire to reduce its net debt to EBITDA ratio to a range of 2.0 to 2.5 times. Based on our estimates, if Imperial Brands fails to grow its EBITDA growing forward, it would need to reduce its net debt by nearly 30%, or $5 billion, to hit the high end of its target leverage range.

The business continues generating healthy cash flow, but its aggressive dividend policy of the past has left it with a 70% payout ratio. As a result, Imperial Brands only retains about $1 billion in free cash flow after paying dividends each year, making the deleveraging process slower.

A 70% payout ratio isn't unusually high in the tobacco market. In fact, Altria and Philip Morris actually have higher payout ratios. However, their balance sheets are stronger, and their greater scale provides them with much more capital to invest in growth areas such as e-cigarettes and heated tobacco without compromising their financial flexibility.

Moving away from 10% annual dividend increases makes sense to improve Imperial Brands' financial flexibility. Management is also divesting some non-core tobacco operations which it expects will deliver proceeds of up to $2.5 billion before May 2020 that can be used to reduce debt.

Until Imperial Brands' leverage improves, however, its Dividend Safety Score will likely remain in our Borderline Safe bucket. Companies facing secular change must maintain financial flexibility to stay nimble, and it's not unheard of for leveraged businesses in these situations to cut their dividends.

In early June, a month before the dividend growth policy revision was announced, Imperial Brands maintained that its dividend was "highly affordable" even despite some performance uncertainties:

"We should start by saying our dividend is highly affordable. We are operating at a level where actual payout ratio is in the sort of seven digits, below 70%. We have got significant cash generation supporting our dividend commitment. So, there is no issue here about the affordability of our dividend given our current performance and our anticipated performance as we move forward.

We did some work earlier on in the year where we reached out to a relatively large group of shareholders, and interestingly, the feedback was, "Look, you've done 10% dividend growth for ten years now, how fantastic but don't feel that you have to stick to it indeterminately. We are fine with lower levels of incremental dividend growth." – CFO Oliver Tant

Not surprisingly, Imperial Brands also maintains an optimistic outlook for its tobacco business. Based on "extensive modeling," management said they expect the firm's tobacco business to grow its revenue 1% to 2% and generate better profit growth at the bottom line.

"The tobacco model in itself could deliver within our guidance range, albeit at the lower end of 1-4% revenue growth, 4-8% EPS, but tobacco alone could deliver that." – CEO Alison Cooper

However, based on Imperial Brands' unusually high yield and "cheap" valuation, the market isn't buying management's story.

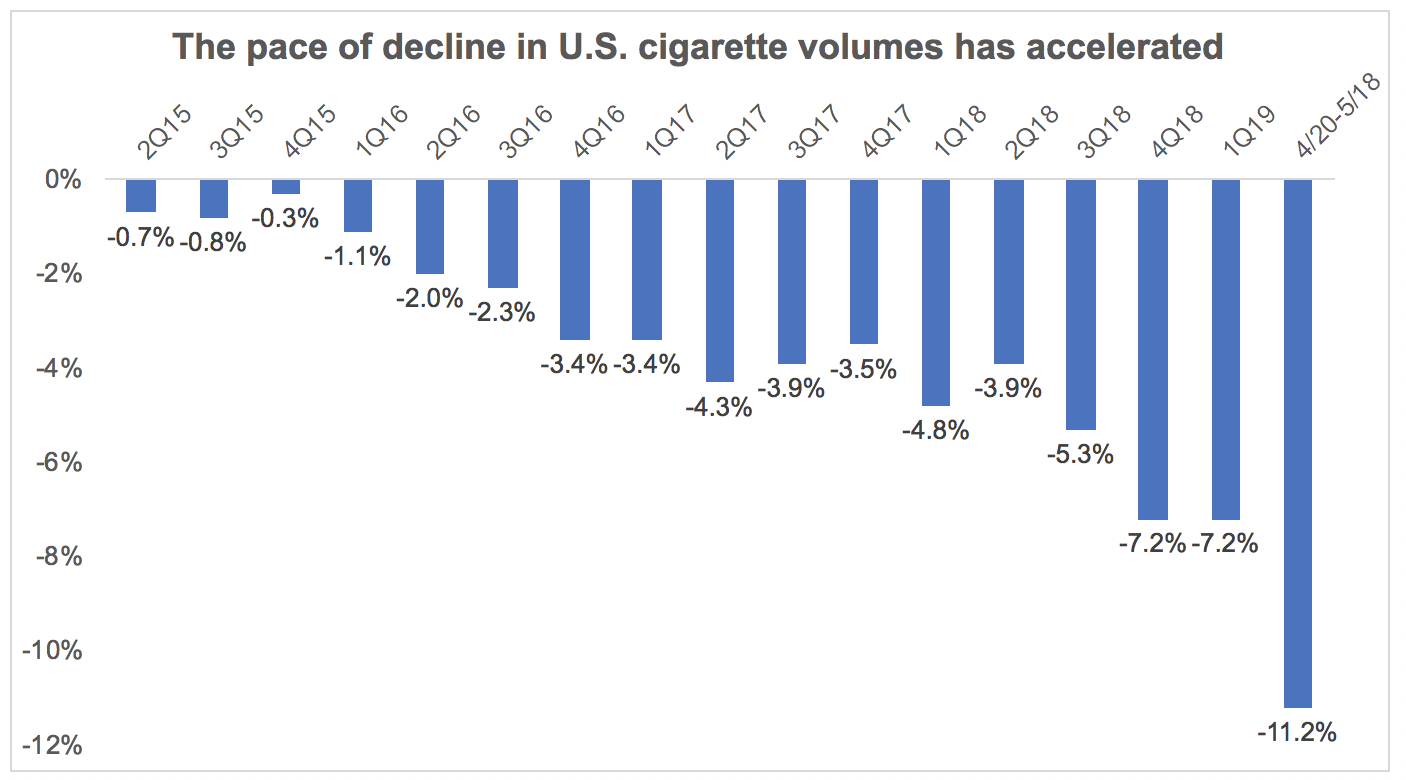

In the Americas region, which generates nearly 30% of Imperial Brands' total revenue and adjusted operating profit, consumer and regulatory challenges abound. As we discussed in our May 2019 note on Altria, U.S. cigarette volume trends appear to be getting worse. This could be the new normal.

Source: Juul, Nielsen, Simply Safe Dividends

Meanwhile, some investors could be nervous that Altria-backed Juul, the dominant e-cigarette company in the U.S. with an estimated 71% market share, could replicate its success overseas. Juul has raised billions of dollars and began aggressive plans to expand internationally last summer.

Europe generates nearly half of Imperial Brands' adjusted operating profit, so a potential accelerated decline in cigarette volumes driven by the rise of Juul and vaping could be difficult to manage.

It's also hard to imagine the firm's blu e-cigarette business holding its lead in markets Juul targets. Significant capital is required to scale consumer products businesses.

In an effort to improve consumer adoption of blu, for example, Imperial Brands increased its investment in brand building and awareness activities by $125 million in the first half of 2019, which is almost as much as the total revenue (roughly $185 million) those products generated during the same period.

Juul has much deeper pockets with a recent valuation topping $38 billion, and its financial flexibility is not limited by a large dividend or stretched balance sheet.

It's too soon to say what will likely happen across the global tobacco and vaping markets over the next few years. However, the combination of a high payout ratio, stretched balance sheet, and cash-burning e-cigarette business raise the stakes for Imperial Brands and make it a riskier stock to own.

If the tobacco market's economics start to break down, likely driven by accelerating volume declines that can no longer be offset by price increases, then the company's dividend could be at risk. A cut would allow management to prioritize deleveraging and make more aggressive investments in next generation products, but it doesn't appear like we are close to that point yet.

Ending the firm's 10% annual dividend growth policy was the prudent thing to do, and it's important that Imperial Brands generates steady results in its tobacco business while delivering on its divestitures and deleveraging plans in the year ahead. We will continue monitoring the tobacco landscape and report on any material changes.