On Monday, EQM Midstream Partners, LP (EQM) announced yet another cost increase and delay to its targeted in-service date for the Mountain Valley Pipeline, or MVP.

The MVP project is by far the firm's most important growth opportunity, representing over two-thirds of EQM's current backlog and accounting for about 15% of firm-wide EBITDA upon completion.

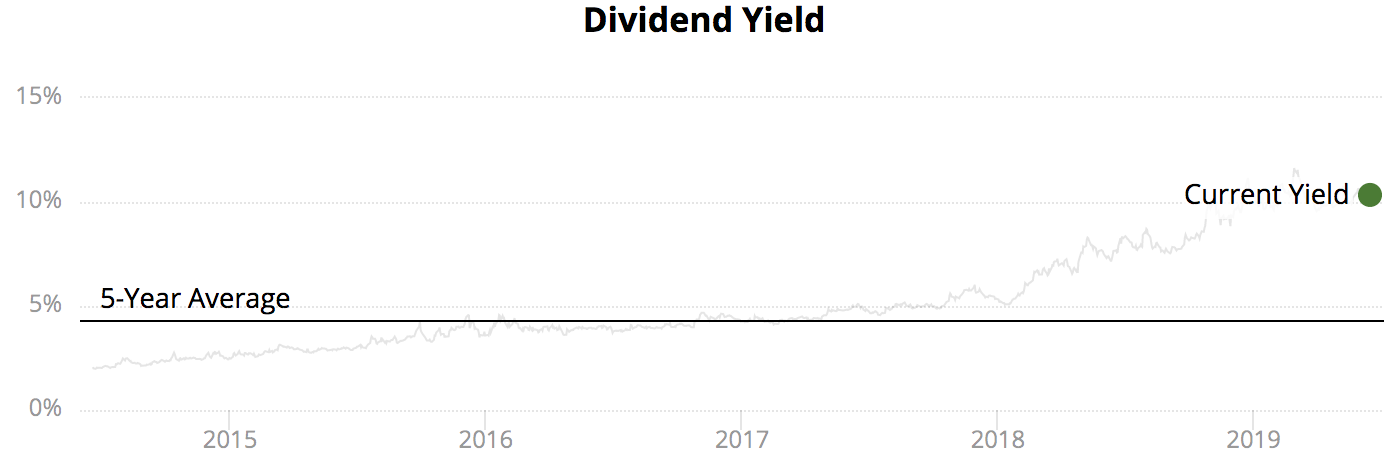

The successful completion of the MVP is critical to EQM's ability to maintain a healthy balance sheet and safe distribution. Continued delays and project cost increases have caused investors to worry about the firm's future financial health, causing EQM's dividend yield to double since early 2018 and sit at a lofty 10% today.

Source: Simply Safe Dividends

Let's take a look at the latest developments with the MVP and the factors that could positively and negatively affect EQM's distribution safety over the next year.

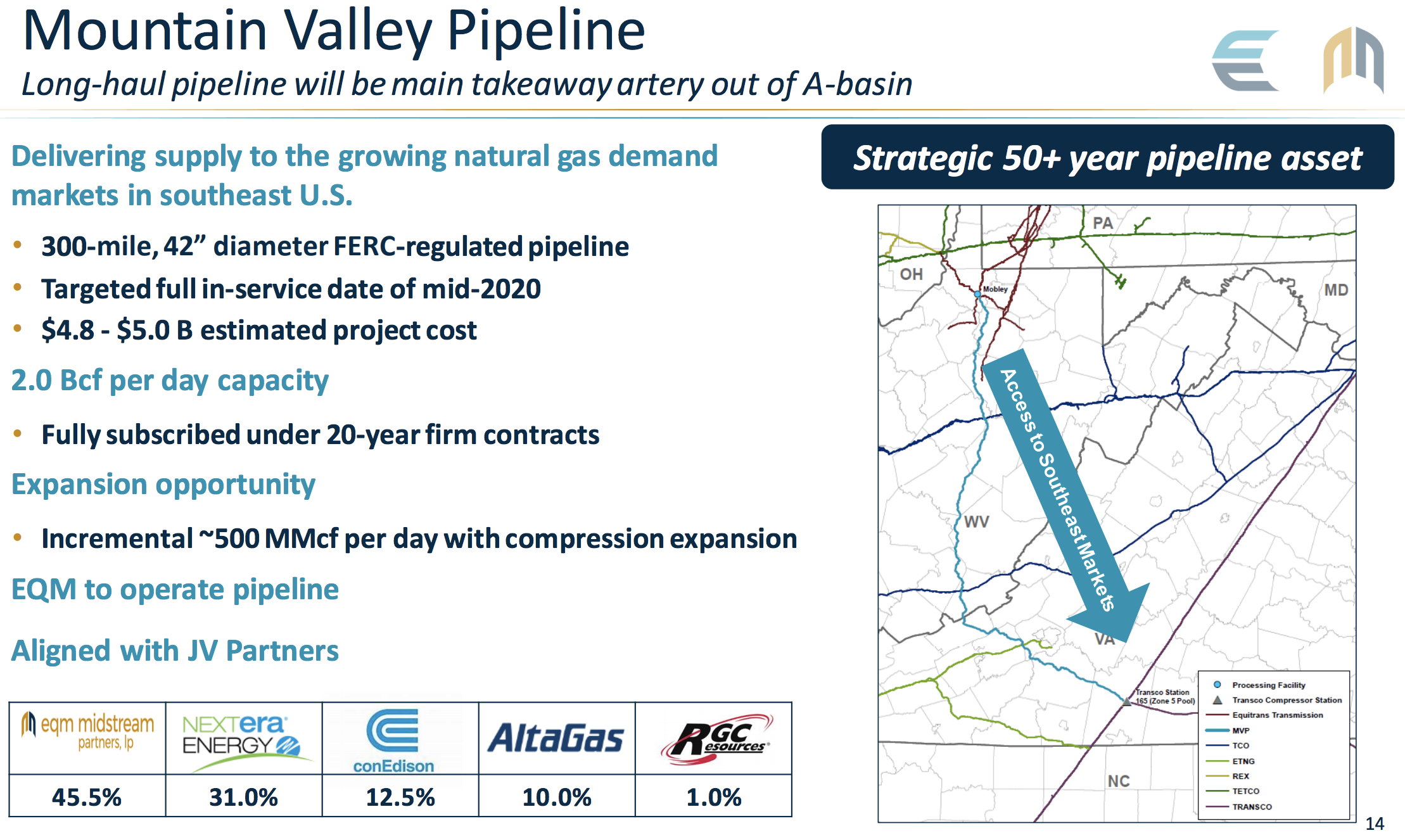

Mountain Valley Pipeline Further Delayed The MVP is a 300-mile natural gas pipeline regulated by the Federal Energy Regulatory Commission. The pipeline will run from West Virginia to Virginia, helping bring a vast supply of natural gas from the Marcellus and Utica shale basin to markets in the U.S. Southeast.

Once completed, the MVP has capacity to deliver 2 billion cubic feet per day (bcfd) of gas. For context, one billion cubic feet is enough gas to supply approximately 5 million U.S. homes for a day, according to Reuters. The pipeline is already fully subscribed under 20-year firm contracts.

EQM owns a 45.5% stake in the pipeline and has partnered with other major companies including NextEra Energy (NEE), ConEdison (ED), and AltaGas (ATGFF).

Source: EQM Investor Presentation

Project planning and development for the pipeline began in October 2014, and the partners on the project originally expected the MVP to cost $3.5 billion and go into service in the fourth quarter of 2018.

Following a series of regulatory and legal challenges, especially from environmental groups, the pipeline's completion was initially pushed back a year to the fourth quarter of 2019, with its estimated cost rising to $4.6 billion.

EQM's latest estimate, announced earlier this week, further pushed the targeted in-service date to mid-2020 and upped the cost estimate to $4.8 billion to $5.0 billion.

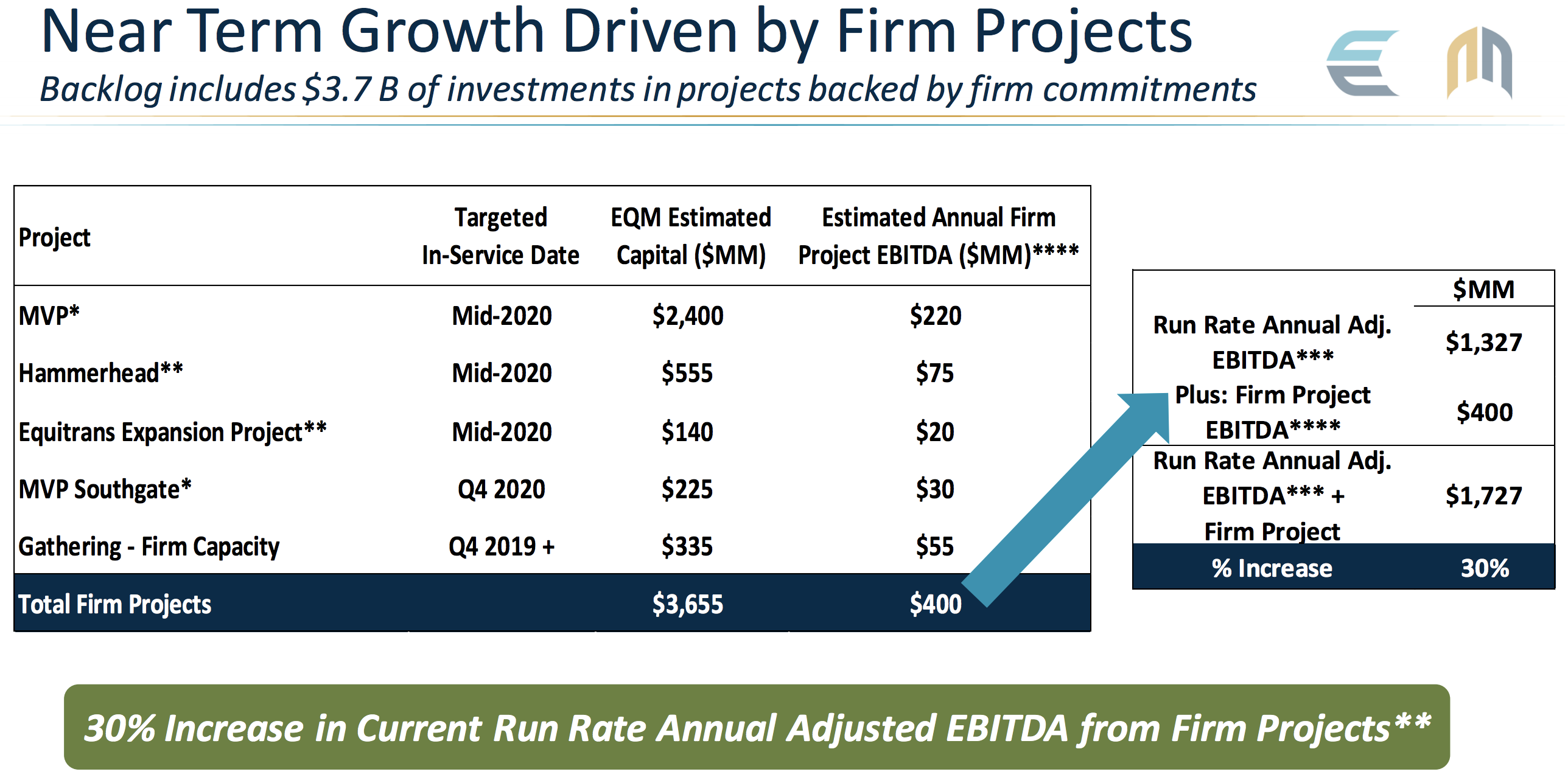

EQM's share of MVP's total capital costs is $2.4 billion, with an additional $225 million earmarked for an expansion project ("Southgate") tied to the MVP.

The stakes are high. Not only does this opportunity account for more than two-thirds of EQM's growth backlog, but a $2.4 billion cost also represents more than 25% of EQM's current market cap.

Additionally, the MVP is expected to generate $220 million in annual EBITDA for EQM, with another $30 million from the Southgate expansion. Once all current growth projects are hopefully finished by the end of 2020, potentially boosting EQM's EBITDA by 30%, MVP-related pipelines are expected to account for close to 15% of the firm's total EBITDA.

Source: EQM Investor Presentation

Pipelines can provide very stable cash flow and healthy returns once they are completed and in service. However, they require significant capital outlays upfront, often years before they go into service and begin generating cash flow.

Project delays and cost overruns can put financial strain on the companies involved with the construction. That's the primary risk with EQM today.

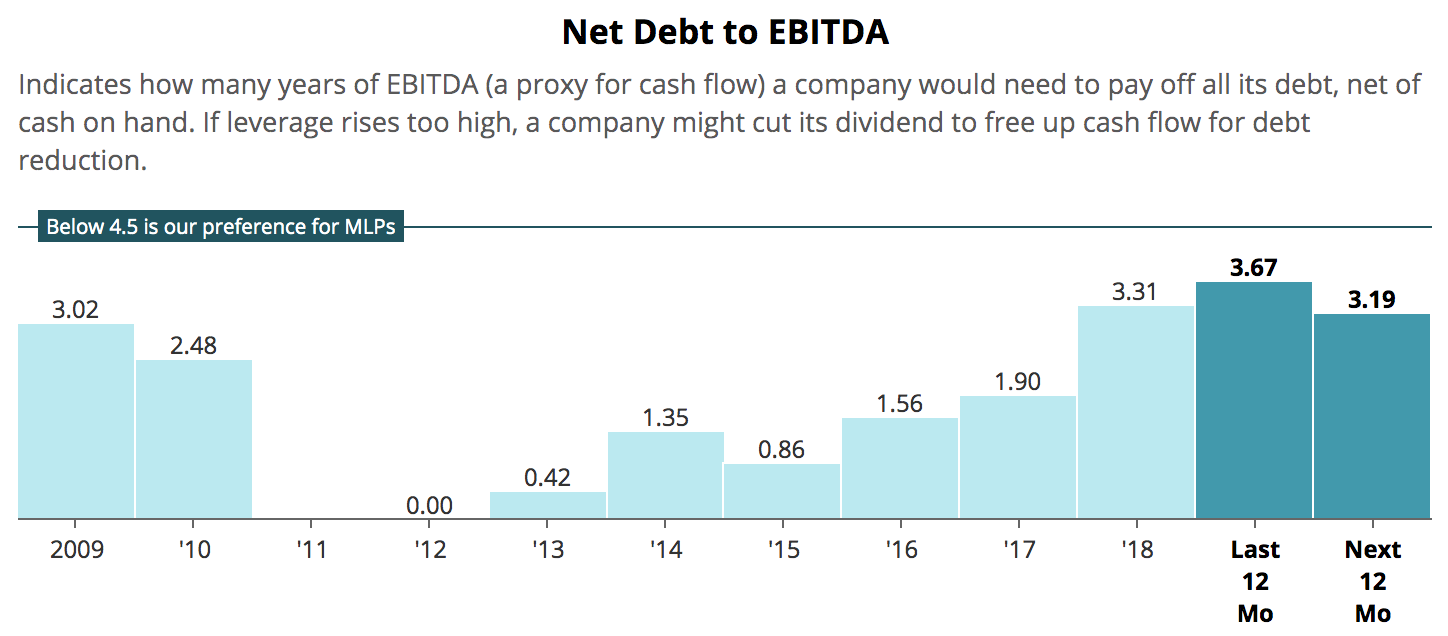

The firm's debt load has increased from about $1.3 billion at the end of 2017 to $4.7 billion today, driven by its merger with Rice Midstream Partners, a large drop-down transaction with natural gas producer EQT (EQT), and meaningful spending on the MVP.

As you can see, EQM's net debt to EBITDA leverage ratio has nearly doubled since 2017, though it remains at a reasonably healthy level for now.

Source: Simply Safe Dividends

While the partnership maintains a BBB- investment grade credit from Standard & Poor's, the credit ratings agency placed a negative outlook on EQM in March 2019. A downgrade to junk status would raise EQM's cost of capital, potentially getting in the way of its ability to profitably fund its growth projects going forward.

S&P states that its negative outlook "reflects uncertainty around the timing of completion and final project costs of Mountain Valley Pipeline. Regulatory delays continue to affect MVP's in-service service timing and resulting cash flows to EQM."

Every year the project's in-service date gets pushed out marks another year that EQM is unable to recognize the $220 million in EBITDA that the MVP can generate. Meanwhile, the firm's balance sheet continues to hold a growing amount of debt as EQM continues funding the project's rising costs and dealing with various regulatory and environmental liabilities.

The end result is a stubbornly elevated leverage ratio, which at some point won't justify EQM's investment grade credit rating. S&P says it could lower its credit rating on EQM "if meaningfully further delays or rising construction costs for MVP occur without management taking mitigating actions to lower leverage" by 2021.

Should additional challenges emerge, the "mitigating action" that income investors fear most is a distribution cut, which would free up cash that could be used to strengthen EQM's balance sheet.

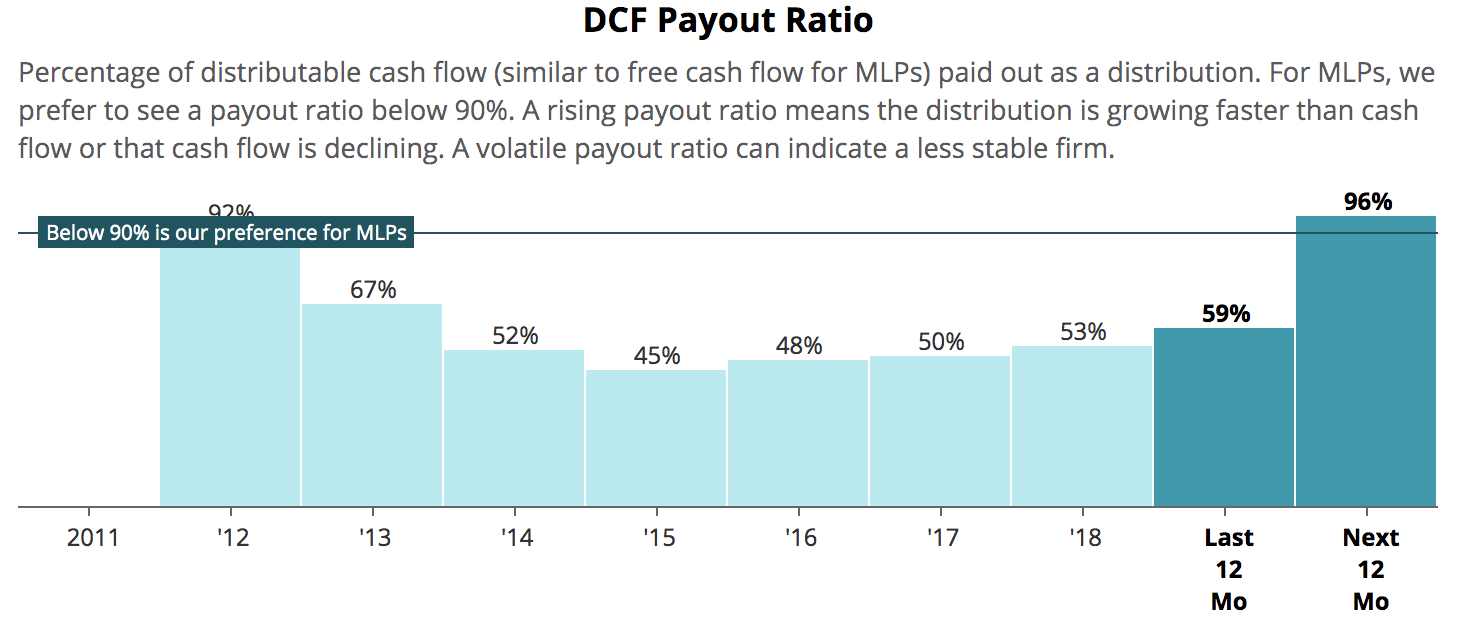

While EQM expects its current project backlog to be funded with retained cash flow and debt capacity, eliminating the need to issue equity to fund growth, the partnership's high payout ratio doesn't leave much cash flow leftover after paying distributions.

Source: Simply Safe Dividends

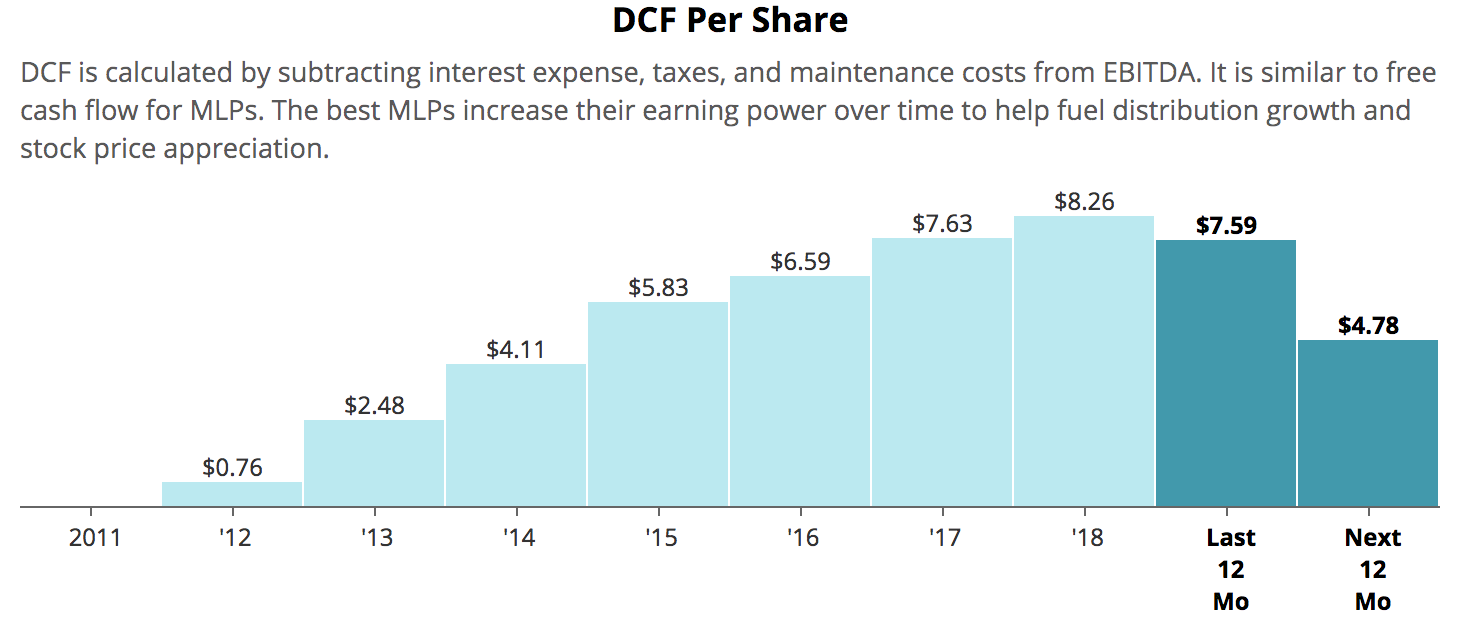

EQM's payout ratio spiked following its move to eliminate incentive distribution rights in February 2019. While this simplification transaction was necessary to reduce its cost of capital and ultimately provide more financial flexibility in the long term, the firm had to issue a substantial number of new units to fund the deal, causing its distributable cash flow per share to nearly get chopped in half.

Source: Simply Safe Dividends

The takeaway is that EQM's distribution is still covered by the firm's cash flow, but it doesn't provide the partnership with much wiggle room to accommodate additional project delays or cost overruns without risking a credit rating downgrade.

On the bright side, when S&P changed its outlook to negative for EQM in March, the firm had already revised its forecast "to incorporate additional conservatism on the timing of MVP's completion, assuming it is in-service by June 2020."

So while EQM's latest announcement is disappointing, a targeted in-service date of "mid-2020" still jives with S&P's latest outlook. It's just even more important that no further slippage occurs, which the market clearly remains nervous of.

What levers could EQM pull to protect its credit rating if the project was further delayed or saw yet another cost increase? Management made the following comments during the firm's earnings conference call in April 2019:

"There are several alternatives that we would consider to defend the investment grade ratings. Clearly, there is advantages to maintaining it and that's certainly our preference.

And we have considered several alternatives, looking at whether it's distribution growth rates, whether it's spending, cost reductions, we're basically exploring all options in order to make sure that we are able to continue to execute on our growth strategy as expected.

So we have good line of sight once we get that 20-year, fully contracted, $300 million of annual EBITDA from MVP online, and at that point we believe that we will be in line with those investment grade targets.

So it's more in the near term and we expect that leverage will creep up as MVP is coming online and even from the inception of EQM we made sure that we funded our drop-down in a debt-friendly manner using equity...and then you saw on our most recent acquisition, we financed that in a way that was mindful of our ratings."

Of course, management would never come out and say that they would cut the distribution to maintain EQM's credit rating. However, there appear to be some levers the firm could pull while keeping its distribution intact, again assuming the higher leverage issue is truly just a temporary problem.

Management's June 2019 presentation, which incorporates the latest project delay, reiterated EQM's "consistent and growing distribution" and 6% annual distribution growth target.

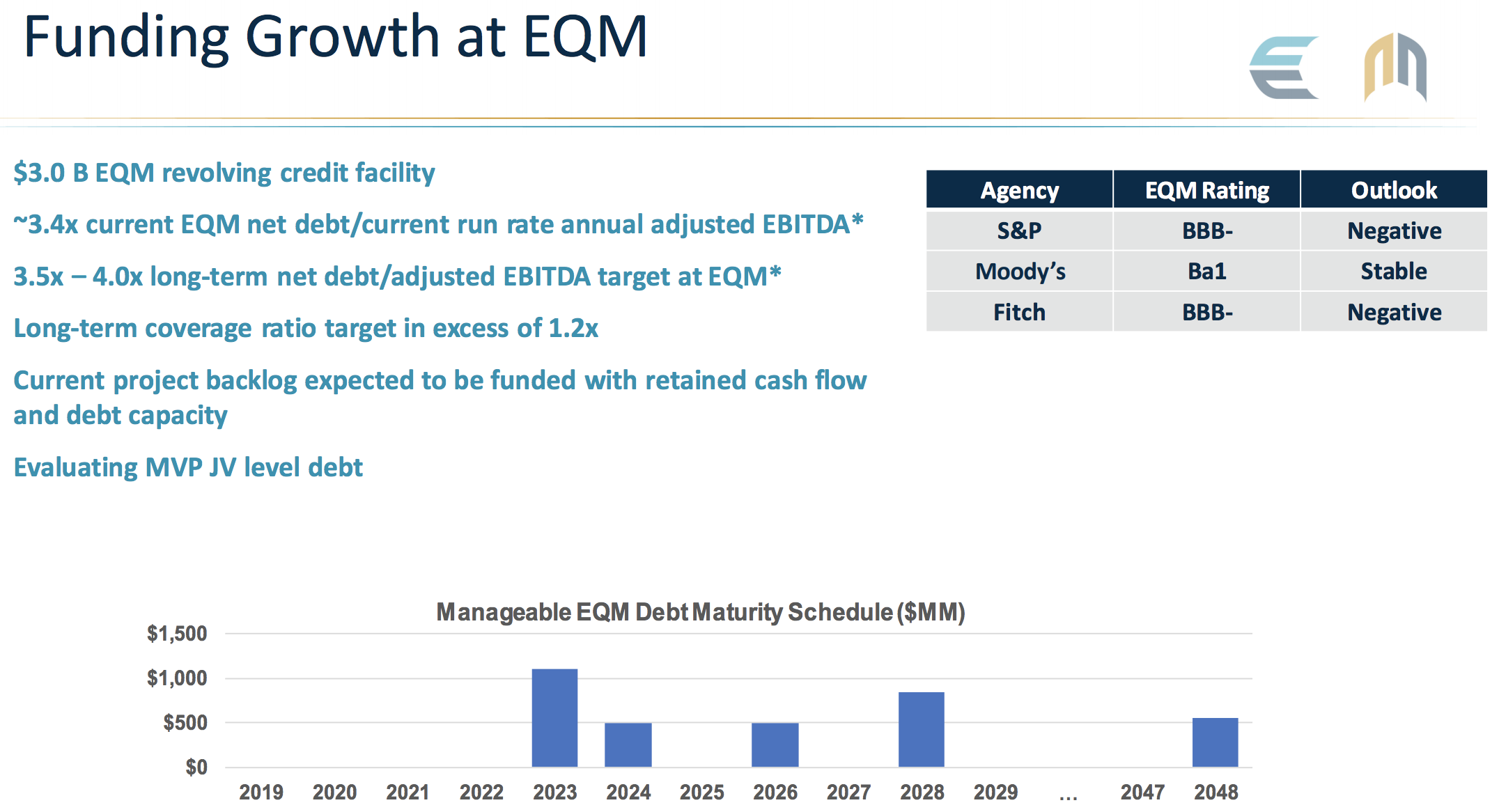

The presentation highlighted EQM's liquidity position as well, which remains decent overall. As you can see below, the firm has no debt maturities until 2023 and has a $3 billion revolving credit facility it can tap.

Management also seeks to improve EQM's distribution's coverage ratio from about 1.04 today to a healthier level above 1.2 as the current slate of projects is completed and cash flow grows.

Source: Simply Safe Dividends

So why is the market still so pessimistic? Assessing the latest happenings with the MVP project is difficult due to its low visibility, but it would seem that investors are still skeptical that the project can be delivered by mid-2020.

Or perhaps some think the project will never be completed, which would deal a big blow to EQM's future cash flow generation potential, or the MVP won't be economical in the long term with natural gas prices recently hitting a three-year low.

Per EQM, the latest delay and cost increase was in connection with a land exchange proposal with the government and "the resolution of a few remaining legal and regulatory components."

The Roanoke Times has provided solid coverage of the MVP's development, including an article reviewing the project's latest setbacks. The land exchange proposal being discussed would potentially allow EQM to construct its pipeline over part of the Appalachian Trail.

Should this effort fail, then EQM might need to reroute part of the pipeline's path. As management explained on the first-quarter earnings call in April, this would likely result in yet another setback:

"A reroute, as I have said repeatedly and we have been pretty consistent on this, that's the path of last resort because it would require the greatest time delay and cost increase. And as long as we continue to have traction and some positive movement on the other paths, we are going to continue down those paths."

For now, both analysts and management are hopeful a mid-2020 in-service date is within reach. However, given the multiyear challenges EQM has already faced, plus the remaining permit issues needing to be resolved and continued protests from environmental groups, the stock will likely remain a "show me" story with investors.

Investing in MLPs can be tricky business. The high payout ratios and substantial leverage employed by these capital-intensive firms reduces their margin for error. Assets such as pipelines generate steady cash flow that can sustain a high distribution, but they are costly to build and can run into challenges that create financial strain.

Smaller midstream MLPs usually have more elevated business risk profiles because their operations are concentrated in just one or two production regions, their sales are dominated by only a couple of customers, and their growth backlogs are not very diversified, raising the importance of each project.

Essentially, they are rifle-shots into certain markets and lack the diversification enjoyed by bigger firms such as Magellan Midstream Partners (MMP) and Enterprise Products Partners (EPD).

EQM is not a small business with total assets approaching $10 billion, but much of its short-term growth potential and financial flexibility still hinges on a single project – the Mountain Valley Pipeline.

Should EQM experience further delays and cost overruns with the MVP, then management will likely need to act to protect the firm's credit rating. A distribution cut is probably a measure of last resort, but it could become a possibility if future cash flow growth won't be as robust as expected, especially given the firm's elevated payout ratio.

For now, EQM maintains a low Borderline Safe Dividend Safety Score. We will continue monitoring the latest developments with the MVP project and provide an update if any material events occur. Much of this uncertainty should be resolved over the next year, for better or worse.