Why Mortgage REITs Like Apollo Commercial Appear Riskier

Given the historically low nature of interest rates, many income investors have flocked to high-yield industries like mortgage REITs, or mREITs. Apollo Commercial Real Estate (ARI) is one popular mREIT, thanks to its 10% dividend yield.

However, while this stock might be an acceptable choice for higher risk investors during a strong economy, it isn't a great choice for conservative income investors who seek stable income throughout the entire economic cycle, including during recessions. Let's take a closer look at why that appears to be the case.

Apollo's Management Structure Is Not Shareholder Friendly

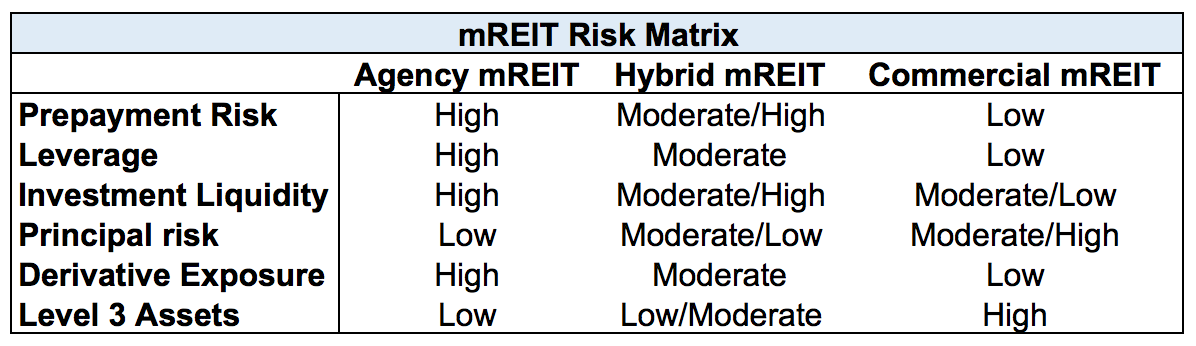

Unlike equity REITs which own physical properties and collect rent (usually under long-term leases), mREITs like Apollo are a kind of "shadow bank" that finances real estate related activities.

Apollo is a commercial mREIT, which is slightly less risky from a dividend safety perspective than residential (agency) mREITs like Annaly Capital Management (NLY). That's because residential mREITs typically fund their investments with short-term borrowing (which can result in highly variable costs) while investing in long-term, fixed rate mortgage based assets.

In contrast, commercial mREITs like Apollo generally borrow at longer-term fixed rates, and their commercial mortgages are floating rate. That gives them upside potential in a rising rate environment, but also downside potential during a recession when interest rates decline, and that's on loans that don't default and result in losses due to naturally high leverage built into the mREIT business model.

Source: Brad Thomas

Another negative to mREITs like Apollo is that they are usually externally managed, in this case by a subsidiary of Apollo Global Management. Founded in 1990, Apollo Global Management is one of the largest private equity firms in the world, with $280 billion in assets under management.

Unlike the vast majority of equity REITs, this means that ARI's management team, which works for Apollo Global, is collecting hedge fund-like fees, in this case, 1.5% of equity each year (in fairness to ARI, other commercial mREITs frequently also have performance fees ARI doesn't charge).

This creates a potential conflict of interest because management fees are typically not based on per share metrics, like EPS or net asset value per share, but absolute figures. In fact, management warns investors about this conflict of interest right in the annual report:

"There are various conflicts of interest in our relationship with Apollo which could result in decisions that are not in the best interests of our stockholders. The ability of the Manager and its officers and employees to engage in other business activities may reduce the time the Manager spends managing our business... Under the Management Agreement, the Manager has a contractually defined duty to us rather than a fiduciary duty... The Manager’s failure to make investments on favorable terms that satisfy our investment strategy and otherwise generate attractive risk-adjusted returns would materially and adversely affect us."

With regular stocks, including pass-throughs like equity REITs, management has a fiduciary obligation to investors, meaning it is legally required to work in shareholders' best interest and not its own. But as the firm states in its annual report, Apollo Global has no such responsibility to ARI investors and is only obligated to run the business and generate deal flow.

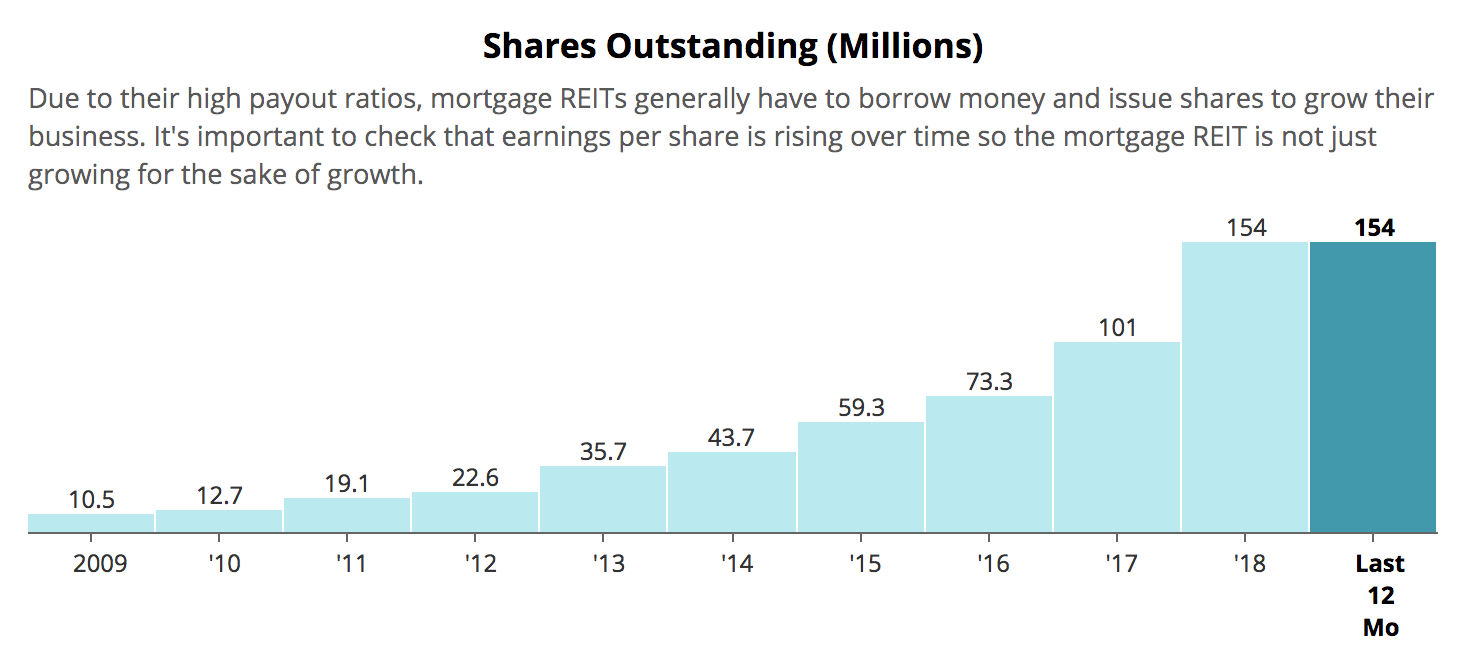

The risk here is that Apollo's management has an incentive to grow its asset base as quickly as possible, but also to do so by taking on increased leverage and selling new shares, potentially at dilutive rates that actually reduce EPS and thus risks the safety of the dividend over time.

That's precisely what Apollo has been doing since its IPO in 2009, with the firm's share count rising more than tenfold.

Source: Simply Safe Dividends

That's helped drive Apollo's assets up from $335 million in 2009 to just over $5 billion today. The firm's increasing portfolio size has resulted in rising management fees as well. In fact, management fees are up from about $3 million in 2009 to $36.4 million in 2018.

Not only have management fees increased on an absolute basis, but they have also risen as a percentage of Apollo's net interest income (revenue):

2016: fees 11.7% of revenue

2017: fees 12.1% of revenue

2018: fees 12.5% of revenue

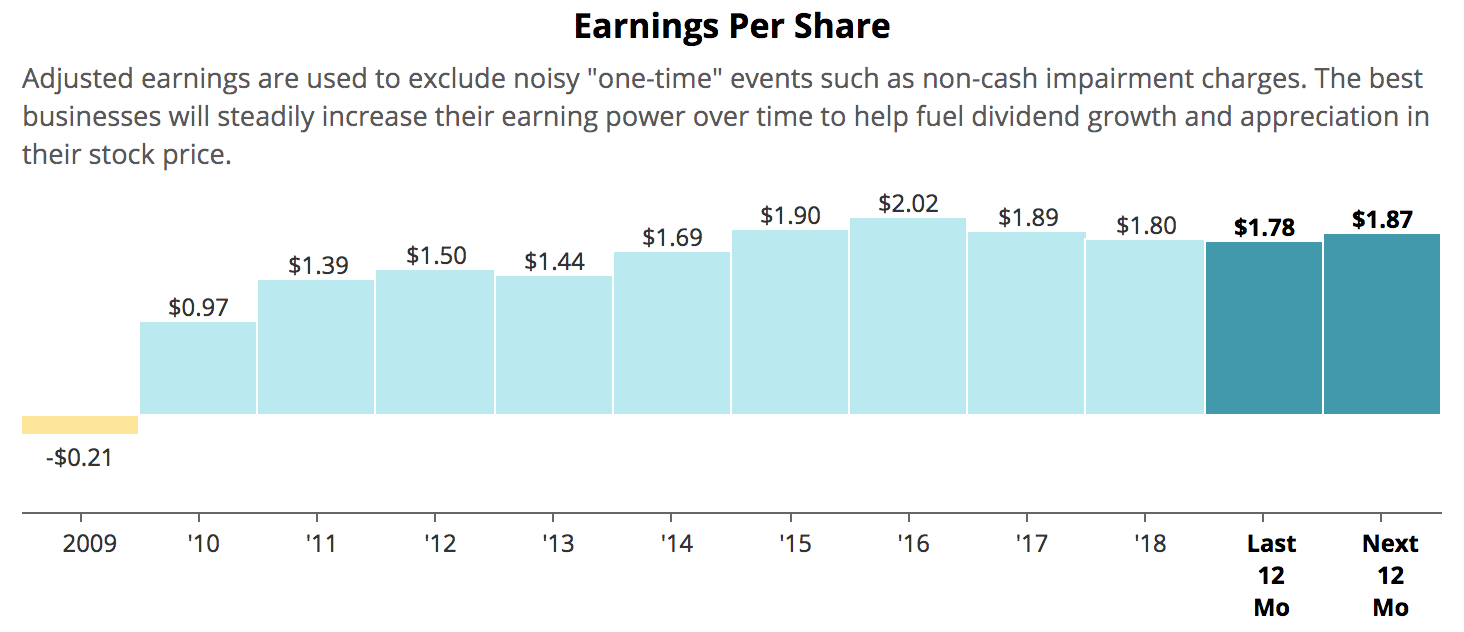

A rising share count, growing asset base, and increasing management fees aren't necessarily bad for shareholders if the business is still growing its per share value. Unfortunately, while ARI investors keep getting diluted, the firm's EPS and the dividend have struggled to grow. In fact, the dividend has been frozen since 2016.

Source: Simply Safe Dividends

In other words, Apollo, like many externally run mREITs, is effectively growing for the sake of growth, because management is getting paid steadily more money for doing so. But the value of the company to shareholders (book value per share) has steadily fallen for the last few years.

That's because Apollo has historically funded 52% of its growth with new equity by selling new shares to investors attracted to the stock's high yield. However, equity is the most expensive form of capital because each new share also gets a claim on Apollo's future earnings and dividends.

In order for equity-funded growth to be accretive to EPS (and increase book value over time and ultimately the share price), an mREIT must sell its shares only when they are trading at a premium to book value.

Apollo's price to book value has ranged from 0.79 to 0.99 since its IPO, with a median value of 0.89, according to Gurufocus. The fact that investors have historically demanded a discount to book value to buy Apollo's shares is an indication that the market doesn't have confidence that the firm's management is working towards maximizing per share value for shareholders.

As a result, nearly all of Apollo's equity raises have been dilutive to shareholders, explaining why the firm's book value per share has been flat over the past decade, despite such impressive asset growth.

That also explains why Apollo's share price has been flat since its 2009 IPO, with zero capital appreciation over the past decade. All of its total return has come from its high dividend.

Thanks to its generous payout, Apollo shares have returned approximately 150% since going public nearly a decade ago. However, the S&P 500 has gained more than 230% during this period, and the Vanguard Real Estate ETF (VNQ) is up over 215%. Simply put, Apollo has meaningfully underperformed the broader market and equity REITs in general.

In effect, Apollo is like an economically sensitive hedge fund, where investors get a high dividend in exchange for allowing management to make lucrative (in a strong economy) commercial real estate investments but pay themselves first, and at the expense of frequently diluting investors.

At first glance, some income investors may feel comfortable with that tradeoff. After all, a little underperformance compared to the market could be acceptable if you still get a double-digit dividend yield and care most about generating current income with your portfolio.

However, during a recession Apollo could be at higher risk of a dividend cut.

Why Apollo's Dividend Could Be Cut During a Recession

Some higher-risk investors are aware of the conflicts of interest associated with mREITs like Apollo and think that it's still worth it, as long as they can get a steady double-digit dividend yield.

Unfortunately, Apollo may not be able to deliver predictable dividends over time.

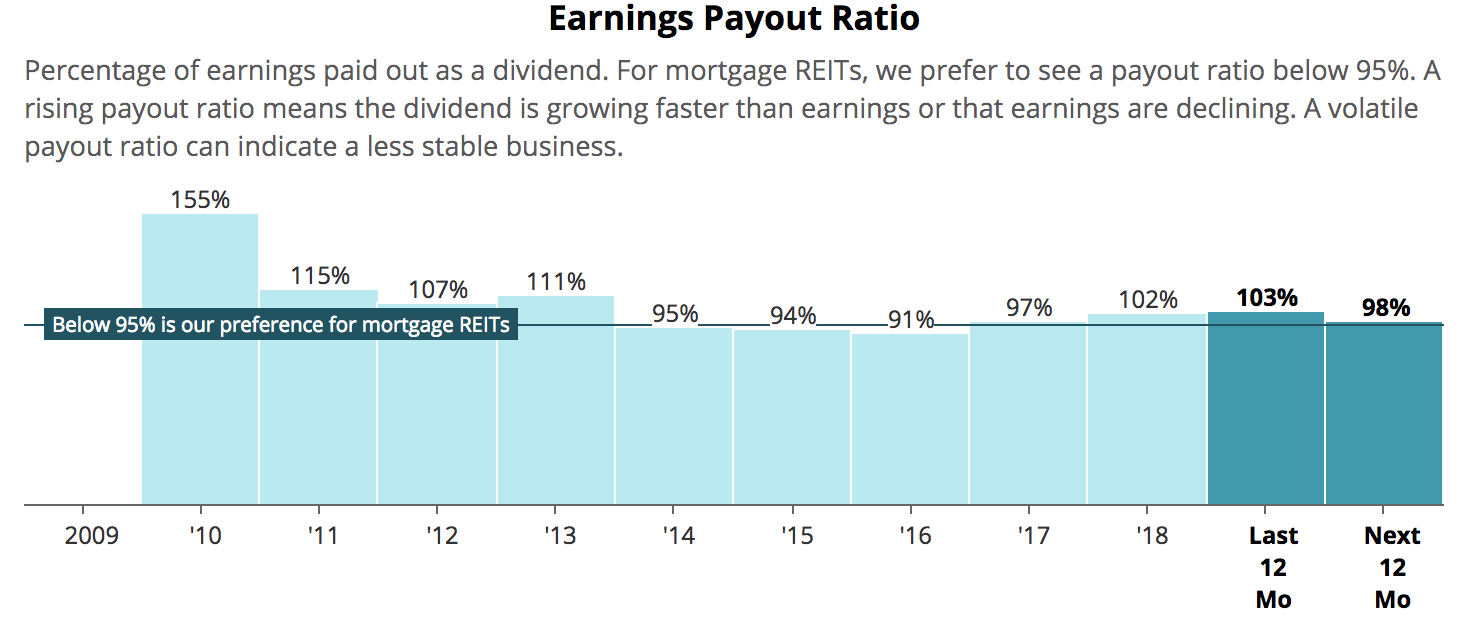

Due to the IRS requirement to pay out at least 90% of taxable income as dividends, mREITs naturally have high payout ratios. Apollo has pushed its dividend to the limit in some years, recording a payout ratio near or even above 100%, thanks in large part to massive share issuances used to grow assets and management fees.

Source: Simply Safe Dividends

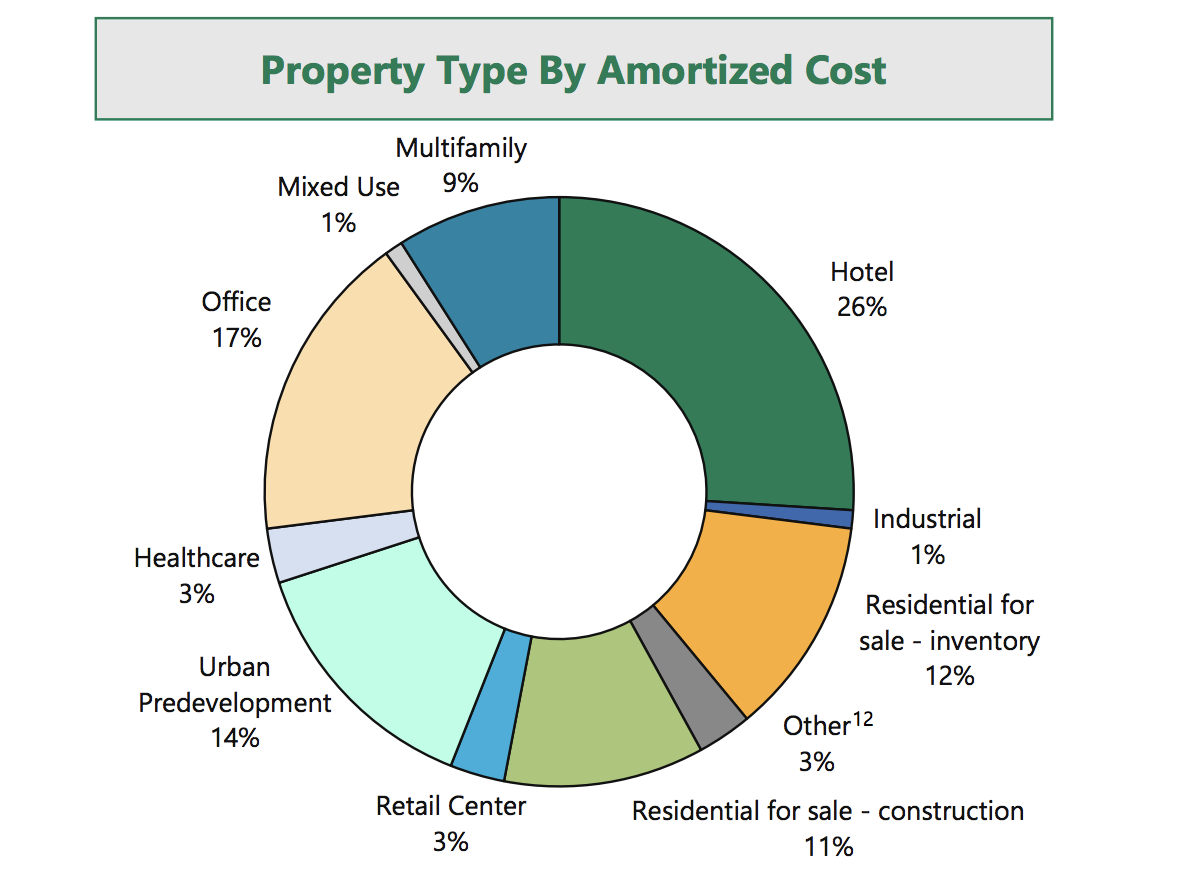

A high payout ratio provides a smaller margin of safety for the dividend if Apollo falls on hard times, especially during a recession. Unfortunately, the mREIT's loan portfolio is most heavily weighted towards hotels, which account for 26% of the portfolio and are known for being sensitive to the economy's health. Apollo's portfolio is fairly concentrated as well, spread across only 69 different investments.

Source: Apollo Commercial Investor Presentation

Furthermore, 35% of Apollo's loan portfolio consists of subordinate loans, meaning they rank below other loans and securities with regard to claims on a company's assets. Should any of these borrowers fall on hard times during the next recession and be unable to honor their full debt obligations, Apollo could be on the hook for some losses.

That's especially true since the weighted average unlevered yield on Apollo's loan portfolio is 9.3%. For comparison, U.S. junk bonds yield close to to 6%. In other words, Apollo appears to own loans that were issued to more speculative borrowers where a higher interest rate is necessary to compensate for their riskier profile.

Whenever the next recession arrives, Apollo seems likely to see higher default rates on its commercial mortgages and loans. Since the firm's payout ratio is already very high today in a healthy economy, it will probably rise well above 100% during the next economic slowdown, pressuring the dividend.

Given that no commercial mREIT managed to avoid cutting its dividend during the last recession, this industry appears to have relatively high risk over a full economic cycle and is thus less appropriate for conservative income investors.

Apollo was founded in 2009, right at the start of the current economic expansion. Thus its dividend track record during recessions, whenever one might finally arrive, is especially uncertain.

While their yields aren't quite as high, equity REITs, which own physical properties and collect rent, are generally a safer choice for dividend investors. Not only are their earnings less sensitive to rates, but the cash flow producing properties owned by equity REITs are permanent in nature, while mREIT assets are all loans that expire and must be replaced, at potentially less lucrative terms.

Equity REITs have also strengthened their balance sheets over the past decade, having learned the dangers of too much leverage during recessions when credit markets tighten. Today the REIT sector's collective leverage is at an all-time low, according to REIT.com.

mREITs like Apollo, on the other hand, have no choice but to maintain relatively high leverage ratios to magnify the yield they earn on their investments. They couldn't afford to pay their high dividends that create investor demand for new shares without doing this.

This strategy works well when times are good, but leverage is a double-edged sword. While Apollo's use of leverage is more conservative than some other mREITs, it still exposes the firm to potentially significant losses during recessions, when loan losses get magnified and dividend cuts have been the norm for commercial mREITs who are old enough to have been through one.

When combined with a high cost of capital (created by external management fees), the rolling off of all loan assets over time, and heightened sensitivity to interest rate fluctuations (91% of Apollo's loans have floating rates), the nature of mREITs' cash flow is too variable to make most of them safe income stocks for the long term.

Concluding Thoughts

While mREITs typically sport some of the highest yields in the market, that doesn't mean they are appropriate for conservative income investors. If your goal is to generate safe and predictable income to help fund expenses, you need stocks with a diversified collection of stable, income-producing assets, reasonable debt levels, and management teams whose interests are closely aligned with investors.

Commercial mREITs like Apollo, while superior in cash flow and dividend stability to residential mREITs, are still a relatively high-risk industry that most conservative income investors probably want to avoid.

While Apollo certainly has some competitive advantages due to its sponsor's large deal flow, ultimately its cyclical and economically sensitive business model, very high payout ratio, and dilutive management structure appear to make it a riskier dividend stock over the long haul.