Founded in 1906, Kellogg (K) is one of the world's largest producers of cereals, snacks, and frozen foods. The company also manufactures crackers, toaster pastries, cereal bars, veggie foods, and more.

Kellogg's well-known brands include Special K, Corn Flakes, Pop-Tarts, Eggo, Fruit Loops, Rice Krispies, Pringles, Cheez-It, and Nutri-Grain. In April of 2019, the company sold its struggling cookie and fruit snack businesses (about 6% of sales) to double down on investments in the company's core brands. Kellogg sells its products primarily to large retailers such as Walmart (19% of 2018 sales). 64% of the company’s revenue last year was made in the U.S. However, emerging markets account for about 20% of Kellogg's revenue and are expected to be a key long-term growth driver.

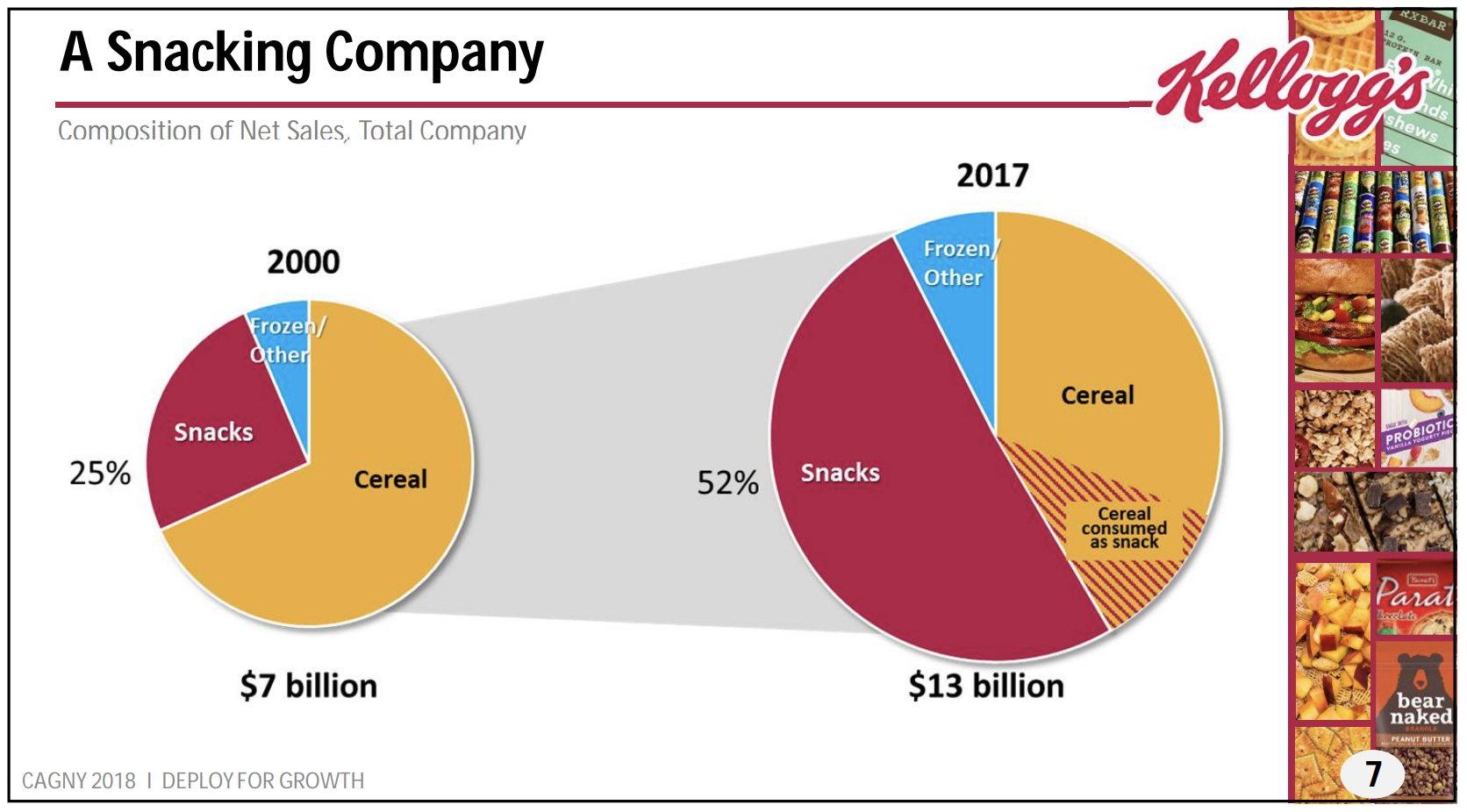

The company operates through seven main segments: U.S. snacks (22% of sales), U.S. Morning Foods (20%), U.S. Specialty (9%), North America Other (14%), Europe (18%), Latin America (7%), and Asia Pacific (11%). Around 30% of global revenue is from cereal.

Business Analysis Over the course of a century, Kellogg has developed one of the best portfolios of name brand cereals and snacks. The company's brand strength, global scale, and ability to adapt to changing consumer preferences have combined to make it possible for Kellogg to pay uninterrupted dividends since 1925.

On the surface, products like breakfast cereal would seem fairly simple for competitors to replicate. After all, many stores have their own generic variety of corn flakes, crackers, cereal bars, and more.

However, what few rivals can match is the billions of dollars Kellogg has spent on advertising to build awareness of and trust in its products. People have historically been unlikely to try something they've never heard of before. Kellogg frequently spends close to $1 billion annually in marketing to protect its brands.

Furthermore, as long as Kellogg's products are selling well, retailers have little incentive to give shelf space to new products. Many of the company's brands have been in stores for decades. Corn Flakes was introduced in 1906, Special K in 1955, and Pop-Tarts in 1964.

Kellogg's popular brands are also a driver of traffic to stores like Walmart, Target, and Kroger, making the firm an important partner for these retailers. Kellogg's relationships with retailers and the slotting fees it pays ensure its products retain good shelf placement.

Having spent over 100 years and tens of billions of dollars building a global supply, distribution, and manufacturing chain, Kellogg has economies of scale that drives down costs and creates another barrier to competing with the firm's established brands. Few food producers can cost-efficiently grow their businesses globally as Kellogg has.

Another key advantage has been the company's ability to adapt to shifts in consumer tastes. For example, when cereals started to fall out of fashion in favor of on-the-go breakfast foods, the company shifted its focus to acquiring and launching snack products, which were enjoying strong growth at the time.

Source: Kellogg Investor Presentation

However, Kellogg will need to adapt once again as people turn away from high-calorie snacks and towards healthier alternatives. Consumption of cereal (Kellogg's core product) continues to decline as well. These trends have combined to contribute to a recent slow down in sales growth at Kellogg.

Fortunately, Kellogg is able to invest substantial amounts of money into developing and acquiring new products to meet the needs of health-conscious shoppers and diversify away from cereal. Few competitors have the financial strength to invest the over $140 million into research and development that Kellogg has over each of the last three years.

In addition, Kellogg intends to build upon its presence in emerging markets (about 20% of revenue), where the company has enjoyed robust sales growth. A growing number of consumers in developing countries have discretionary income to purchase snack foods, but they're generally not well off enough to buy into the same healthy-eating trends as consumers in wealthier parts of the world.

Ultimately, the company believes it can continue to grow sales and profits over the long-term by revitalizing its core brands through inventive marketing campaigns, creating new products to meet the tastes of today's consumers, and pursuing expansion overseas.

Overall, Kellogg's brand equity, global distribution network, economies of scale, and financial flexibility make it likely that the cereal and snack businesses will remain cash cows for years to come. Long-term growth, however, is no sure thing.

Key Risks Kellogg's revenue remains about 7% below its 2013 peak, underscoring the difficulties the company has had achieving sustainable, long-term growth in the face of shifting consumer preferences.

Breakfast cereal, which makes up around a third of the Kellogg's portfolio and is still the company's top money maker, has fallen somewhat out of favor with consumers who increasingly prefer on-the-go eating and what they consider more natural, fresher, and less processed foods. As a result, sales of cereal at Kellogg's has seen essentially no growth over the last decade.

To help fight the lack of sales growth, Kellogg is focusing more on its healthy offerings, particularly its Kashi and MorningStar Farms brands.

However, part of this strategy involves ongoing bolt-on acquisitions of small and fast-growing healthy brands. Trendy products require paying top dollar to acquire, and Kellogg has had to take on above-average debt levels to fund its investments.

For example, in 2017 Kellogg paid $600 million to acquire RXBAR, a fast-growing manufacturer of protein bars. RXBAR only had 75 employees and was projected to generate $100 million in annual sales that year, representing a steep price-to-sales multiple of 6x for the deal and illustrating management's itch to diversify.

The company still maintains a BBB investment grade credit rating from Standard & Poor's and enjoys relatively low borrowing costs, but Kellogg's dividend growth potential will be reduced until management pays down some of its debt. Kellogg's dividend increase in 2019 came in at under 2%.

Moreover, there's no guarantee Kellogg can adapt its portfolio to healthy-living trends without alienating its still-large core group of customers who enjoy the taste of products like Frosted Flakes and Pop-Tarts.

While the company has reported organic sales growth in each of the first two quarters of 2019, suggesting Kellogg's legacy product lines may be stabilizing and investments in new products and emerging markets may be paying off, the company still has to prove that it can deliver profitable growth over the long run.

Finally, it's worth mentioning that Kellogg's short-term results can be impacted by foreign exchange rate fluctuations (36% of sales are from overseas markets), commodity price volatility (although Kellogg maintains long-term contracts for key agricultural inputs), and rising transportation costs. However, none of these issues seem likely to weight on Kellogg's long-term earnings power.

Closing Thoughts on Kellogg

Kellogg's wide assortment of large and well-known brands has served investors well for more than a century. However, all companies need to adapt to changing consumer tastes, and Kellogg has struggled to do that over the past decade.

While management's turnaround plan focused on snacks and emerging markets sounds reasonable, investors have reason to be skeptical that the firm can deliver on its plan. At the very least, Kellogg is probably going to have to grow its dividend slower than in the past, in order to maintain a healthy balance sheet and fund its ongoing turnaround.

As conservative investors, our preference is to invest in companies with stronger long-term outlooks and clearer paths to profitable growth. Many parts of Kellogg's portfolio appear to remain in the crosshairs of changing consumer tastes, and management's long-term track record of adapting the business doesn't inspire much confidence.