Thoughts on Walgreens' Sell-Off and Dividend Safety

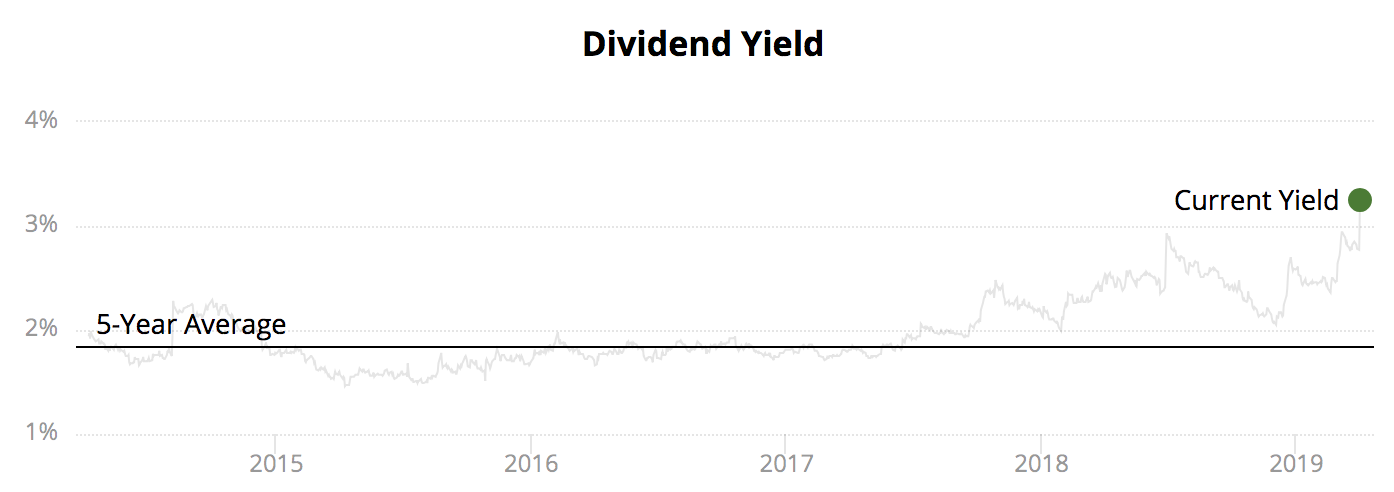

Last week Walgreens (WBA) shares fell 13% and reached a five-year low after the pharmacy chain reported a big earnings miss and reduced its guidance. WBA's dividend yield also spiked above 3% to its highest level ever.

Source: Simply Safe Dividends

Let's review why the market has turned so bearish on Walgreens to see if the company's dividend remains safe and whether or not its long-term outlook appears to remain intact.

Why Walgreens Fell 13% After Reporting Earnings Last Week

On April 2, Walgreens lowered its fiscal 2019 guidance from 7% to 12% adjusted EPS growth to flat growth. The company is facing pressure on almost every front right now.

Here's what Walgreens CEO Stefano Pessina told analysts on the conference call:

"I want to acknowledge upfront that this has been a very disappointing quarter for us...a number of the trends that we had been expecting and preparing for impacted us significantly more quickly than we had anticipated.

We found ourselves facing a combination of increased reimbursement pressure in the quarter, lower generic deflation, lower brand inflation and lower than anticipated benefits from our work to refresh and renew our retail offerings, primarily in the U.S.

Of course, the pharmacy trends are not only impacting our business, they are impacting the overall market and will likely continue to do so over the coming months."

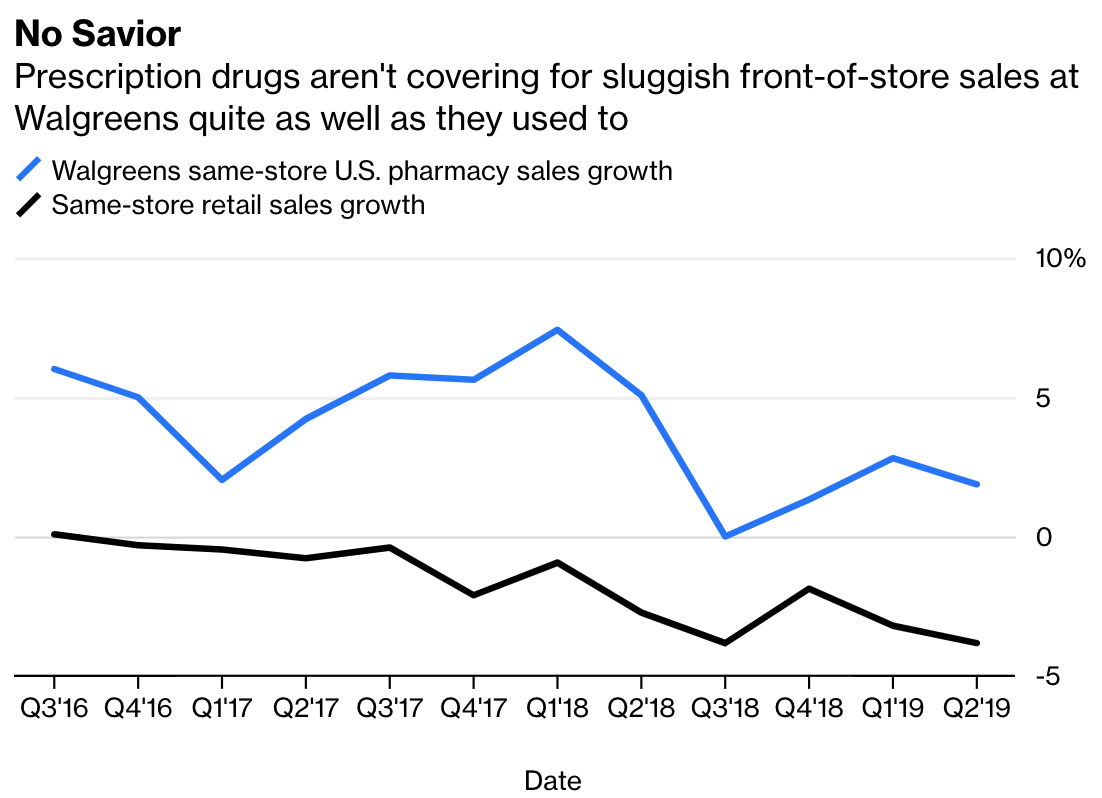

As you can see below, Walgreens' same-store retail sales have declined for over two years, with the pace moderately accelerating in recent quarters. The company's U.S. pharmacy business, which generates the bulk of Walgreens' profits, had helped stabilize results during most of this period. However, its pace of growth has also decelerated, and its margins are now under increased pressure.

Source: Bloomberg

Lower drug reimbursements, created by consolidation in the pharmacy benefit management industry, have hurt Walgreens the most. Pharmacy benefit managers, or PBMs, serve insurance companies and employers by determining which drugs are covered for patients and negotiating price discounts with drugmakers.

Walgreens' pharmacy business negotiates with insurance companies and PBMs on the amount of reimbursement it will receive for the prescriptions it fills. As drug prices have come under greater pressure, PBMs have become more aggressive with the reimbursement rates they are willing to offer Walgreens.

To maintain its pharmacy margin, Walgreens historically relied on paying lower prices for generic drugs, which account for the vast majority of prescriptions. Unfortunately, generic drug prices have not fallen fast enough to offset the reimbursement pressure from PBMs.

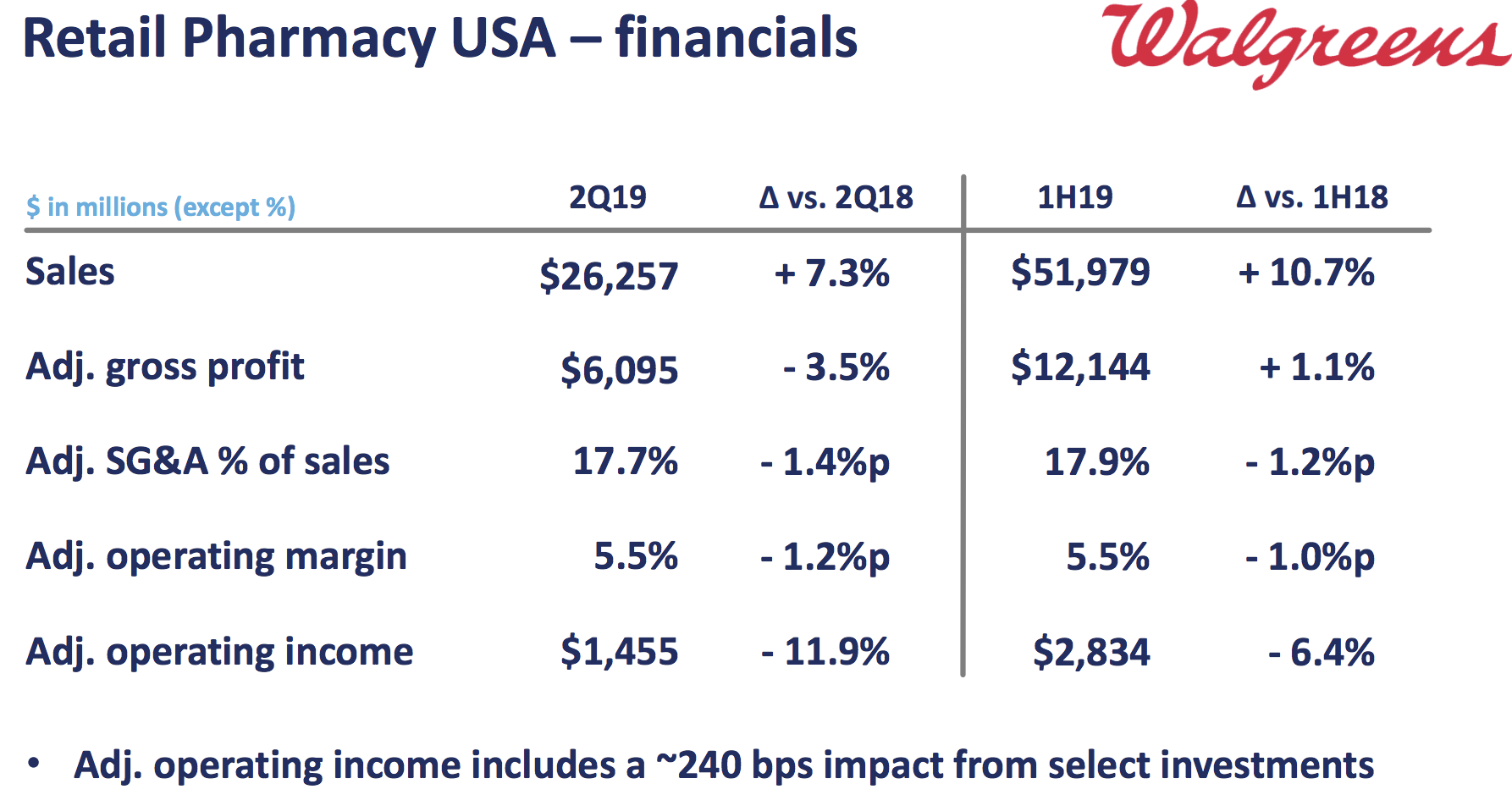

That explains why in the firm's U.S. retail pharmacy business (74% of sales and 76% of operating profits) sales were up but profits declined, with Walgreens' adjusted operating margin falling 120 basis points to 5.5%.

Source: Walgreens Earnings Presentation

Rising healthcare costs have created a big push from both private and public payers to slash costs throughout the medical supply chain. That's why we've seen so many large mergers in recent years, as companies like CVS Health (CVS) attempt to maximize economies of scale to both squeeze suppliers and maximize their own pricing power.

Walgreens has mostly stayed in its own lane by remaining focused on retail pharmacy, unlike CVS which has made several large deals to become a leading player in not just pharmacy but also PBM services, and now health insurance with Aetna.

CVS faces plenty of risks from its debt-funded deals, especially as changing regulatory and political forces create an increasingly dynamic healthcare landscape, but it also has more avenues for potential growth.

In contrast, Walgreens remains mostly focused on retail, which is itself being disrupted by e-commerce. In fact, the company has struggled with falling non-pharmacy retail sales for several years, both in the U.S. (same-store sales -3.8% last quarter) and in Europe (-2.3%).

To fix its struggling retail operations management plans to:

Invest $1 billion over three years to improve its stores (both Rite Aid and overseas, by making them "experiential" locations)

Focus on higher-margin health and wellness products

Improve its loyalty program

Partner with LabCorp to install patient service centers (think CVS Minute Clinics) at about 15% of U.S. Walgreens locations by 2023

To offset the rising power of PBMs, Walgreens plans to keep consolidating the pharmacy chain industry (23% market share) to drive higher drug volumes. It also plans to increase non-pharmacy retail volumes in an effort to reduce product costs.

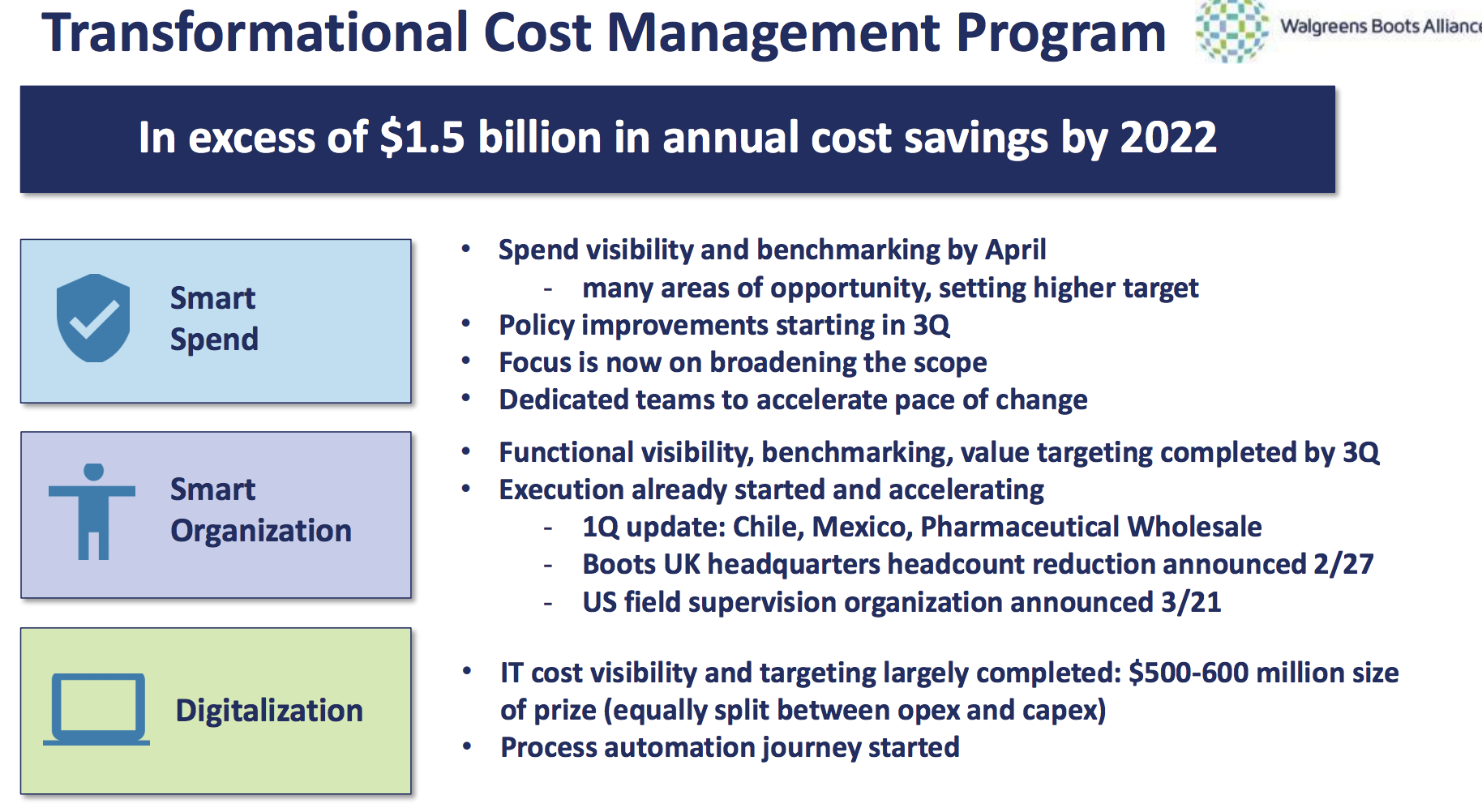

Cost cutting is another major component of the turnaround plan, with management upping its targeted cost savings from $1 billion to $1.5 billion by 2022. A 20% headcount reduction at the U.K. headquarters of Boots is also part of the company-wide restructuring.

Source: Walgreens Earnings Presentation

Starting in 2022 management also expects the various joint ventures it's made with AmerisourceBergen (ABC) and Express Scripts (ESRX) to begin paying off. These alliances will hopefully help to offset continued pressure in reimbursement rates and, combined with higher drug volumes (thanks to an aging population), should result in continued top line growth.

To execute on this accelerated turnaround strategy Walgreens has made numerous management changes including a new:

Chief digital officer

Global chief marketing officer

Global chief supply chain officer

Global controller and chief accounting officer

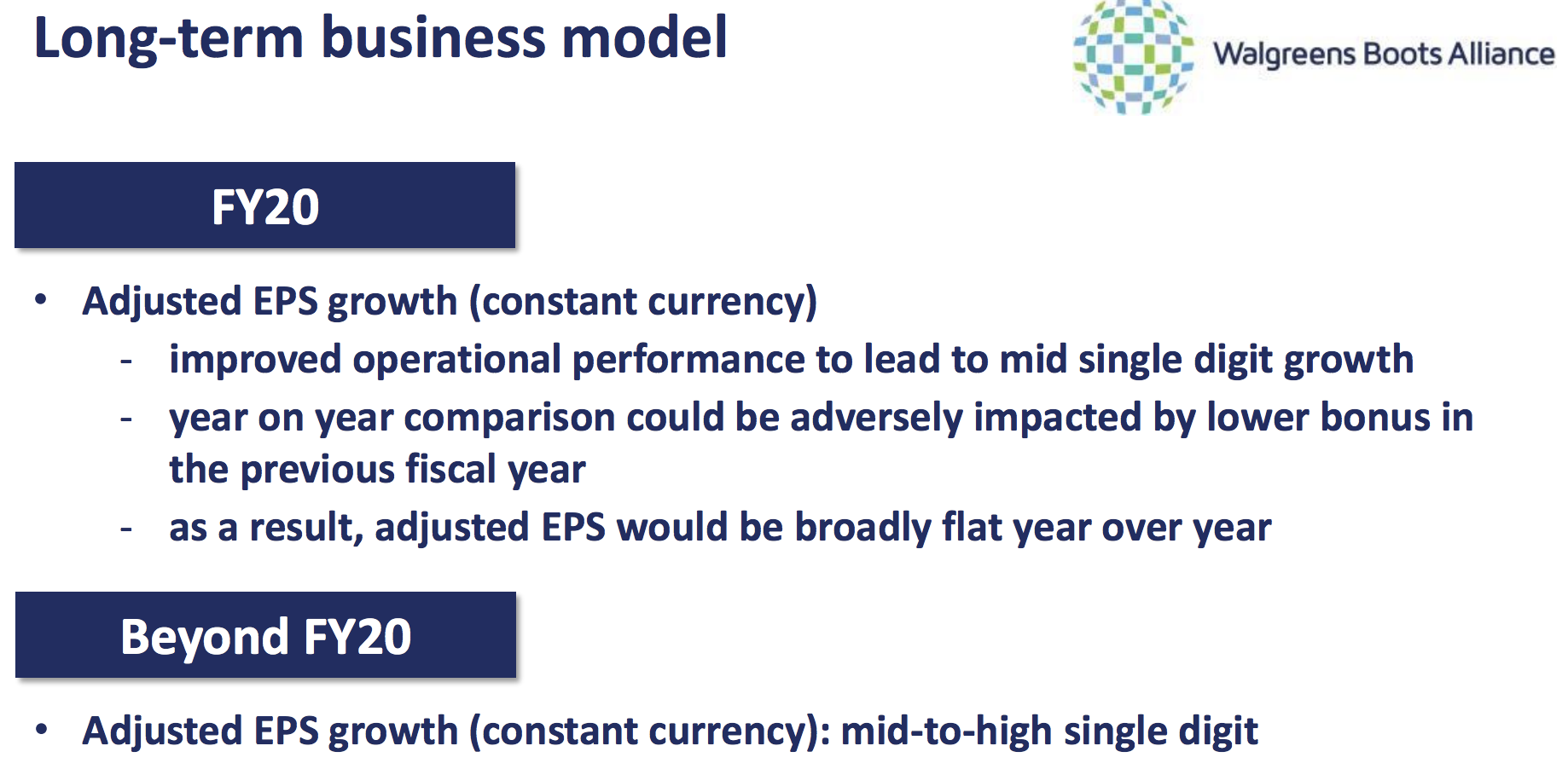

According to its CEO, Walgreens is "convinced" that starting in 2021 the company can deliver mid-to-high single-digit earnings growth (about 5% to 9%) due to its strategic plans.

Source: Walgreens Earnings Presentation

How realistic is this turnaround plan? It sounds good in theory, especially the part about replacing lower margin retail store space with clinics as CVS has done in recent years.

However, Walgreens may be paying the price for its conservative approach over the past few years as well as not diversifying its business away from traditional retail in which it has struggled to adapt to the new world of omnichannel (seamless online and brick-and-mortar store shopping).

Management's decision to up its cost savings target by 50%, or $500 million, also feels a little desperate and creates risk that Walgreens cuts too deep to the bone. Meanwhile, visibility in pharmacy remains low. It's difficult to monitor trends in drug reimbursement rates and generic drug prices, which directly affect Walgreens' margins in this critical segment.

Essentially, Walgreens faces growth challenges in both its pharmacy and traditional retail businesses that could take a while to be resolved. Cutting costs and repurchasing shares can only boost earnings for so long, so management's turnaround plan ultimately needs to work to restore investors' face in the drugstore's long-term growth prospects.

With roots dating back to 1849 and 43 consecutive years of dividend growth under its belt, Walgreens has battled through its fair share of challenges in the past. The company deserves the benefit of the doubt for now, but investors will need to have patience as the business maneuvers through these headwinds over the next few years.

"However, the healthcare and retail sectors are increasingly complex and rapidly evolving. Amazon and others are increasingly taking share from brick-and-mortar retailers as more consumers shop online, and drug prices are under pressure as governments and insurers seek to control rising healthcare costs.

Simply put, the entire distribution chain that delivers drugs from manufacturers to patients is under different pressure points. Walgreens has managed to continue growing despite increasingly challenging industry conditions, but the lines continue to blur between insurers, PBMs, drugstores, and other players.

While rising overall medical spending could continue to drive steady growth for the company, the question facing Walgreens and investors is whether or not the firm will be able to continue adapting fast enough to maintain its overall profitability... Conservative investors need to have realistic growth expectations from this dividend aristocrat and may even prefer investing elsewhere until the industry settles into a steadier state."

Fortunately, investors who are comfortable with the industry's challenges and Walgreens' turnaround plans can likely bank on the dividend while they wait for improvement.

Walgreens Still Appears to Offer a Safe Dividend

Turnarounds often require a good deal of financial flexibility to execute. More specifically, a company facing growth challenges is better positioned to maintain its dividend if it has a reasonably low payout ratio and a healthy balance sheet.

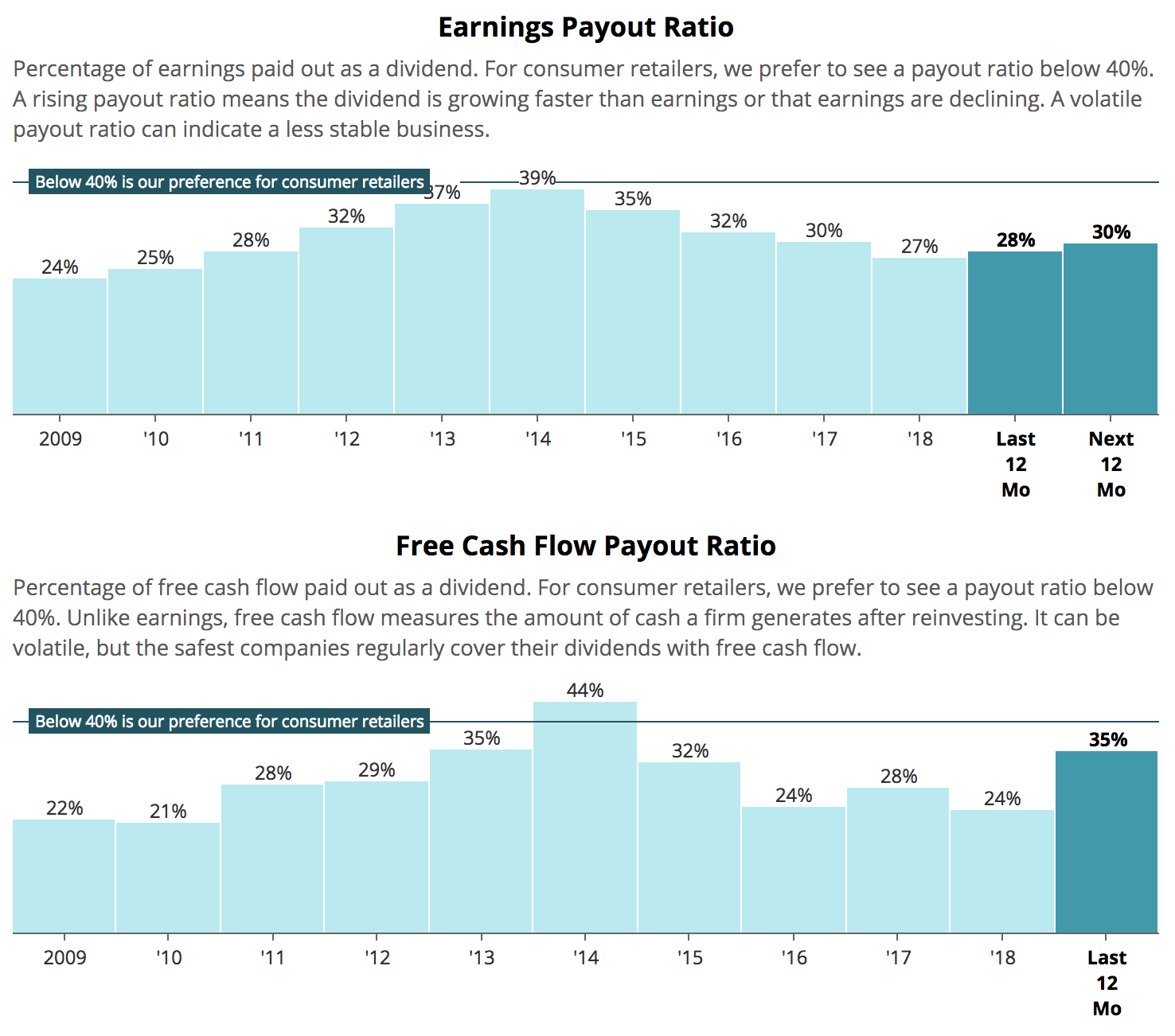

Starting with the payout ratio, which measures how much of a company's earnings and free cash flow are consumed by its dividend, Walgreens has a solid track record of maintaining a relatively low payout ratio below 40%.

Source: Simply Safe Dividends

Most years Walgreens generates $5 billion to $6 billion of free cash flow, which management expects to deliver again in fiscal 2020 and its current dividend amounts to a $1.7 billion annual commitment.

As a result, even with flat growth, Walgreens should have around $3 billion to $4 billion of retained cash flow after paying dividends. The drugstore can use these funds to invest in turnaround as well as pay off maturing debt. Simply put, the company's payout ratio suggests its dividend is sustainable.

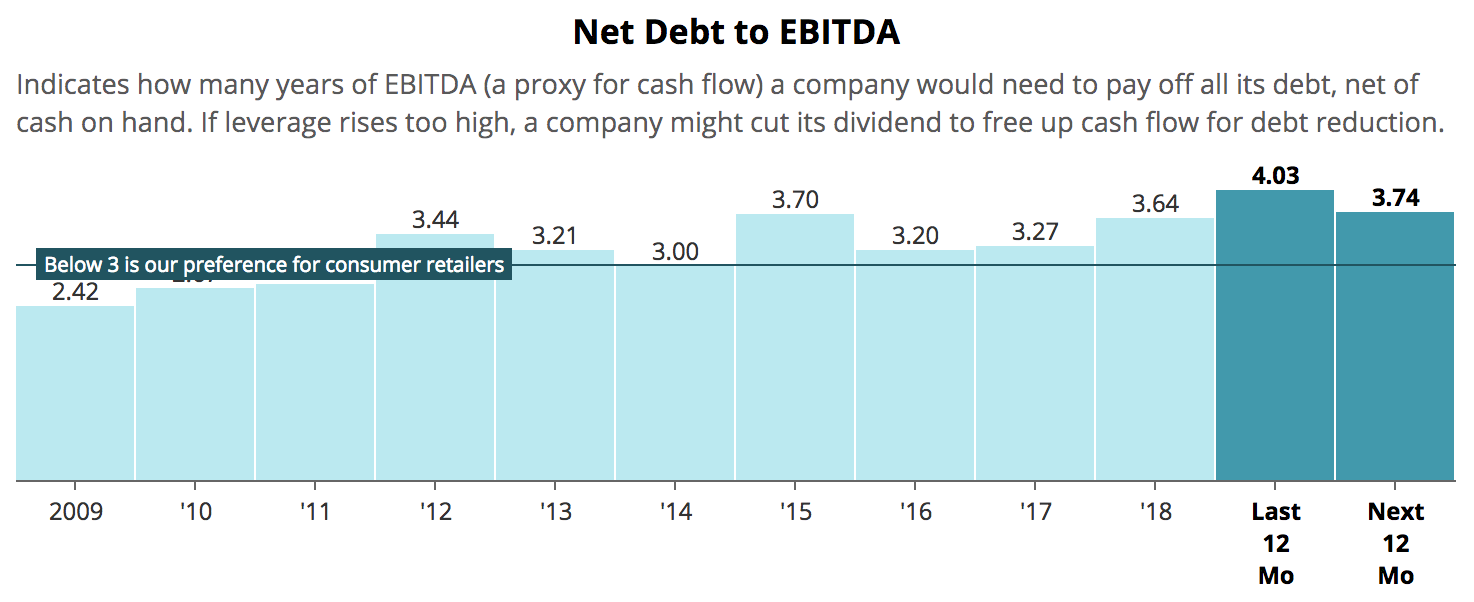

Turning to the balance sheet, Walgreens has a somewhat higher leverage ratio than we prefer to see, although it's in line with the company's historical norm and not much of a concern given the drugstore's predictable cash flow.

Source: Simply Safe Dividends

While Walgreens has about $18 billion of book debt, less than $4 billion of its long-term debt matures through 2022. Therefore, the firm's annual retained cash flow, plus its $800 million of cash on hand, could comfortably cover these maturities without jeopardizing the dividend if management chose not to refinance the debt.

Thanks to these strengths, credit rating agencies and bond investors are not worried about Walgreens' somewhat elevated debt, because the firm's high amounts of retained free cash flow is more than enough to deleverage to safer levels over time. In fact, Standard & Poor's gives the drugstore a solid BBB investment grade credit rating.

Importantly, management remains uninterested in large acquisitions that could compromise the company's financial health while introducing new operational risks. This conservatism further supports the long-term sustainability of Walgreens' payout.

"We don’t see any reason to use our cash overpaying for something just because there is a deterioration of the market. If anything, we have to be more careful now when we buy something because if we don’t believe that the market will turn around, we have to action more carefully." – CEO Stefano Pessina

Overall, Walgreens' dividend appears to remain on solid ground despite the company's growth challenges. There is no guarantee that management will achieve its turnaround goals as industry conditions continue shifting, but the company has the financial flexibility to invest for the future while continuing to reward income investors with predictable payouts as it has for many years.

Concluding Thoughts

Walgreens may appear to be a simple business on the outside, but the last few quarters have shown just how complicated some of its core drivers have become. From generic drug price deflation trends to PBM negotiations and the rise of e-commerce, Walgreens has its work cut out for it.

Simply put, Walgreens' impressive track record of more than four decades of rising dividends can't hide the fact that the company is struggling to adapt to changing retail and healthcare environments. These appear to be secular headwinds that will likely continue for the foreseeable future.

That being said, the company's balance sheet remains relatively strong, and Walgreens' dividend is well covered by recession-resistant cash flow. Only time will tell whether or not management can deliver on its turnaround plans and generate 5% to 9% long-term earnings, cash flow, and dividend growth.

The company deserves the benefit of the doubt for now as it works on implementing a long-term plan, and the stock's seemingly low valuation creates a higher margin of safety. However, as stated in our thesis, conservative investors need to have realistic growth expectations (dividend growth could be much slower over the next two years) and may prefer investing elsewhere until the industry settles into a steadier state.