Uniti Group (UNIT), a wireless infrastructure REIT, has sported a "Very Unsafe" Dividend Safety Score and a double-digit yield for years. In our April 2018 thesis we made the following remarks:

"Uniti Group appears to be cheap for a reason and is a very high risk dividend stock. The company's payout could be reduce substantially at any time in order to redirect the cash flow to the REIT's much needed diversification efforts...

Uniti's high yield is due to some major problems that the REIT has not yet shown an ability to overcome. The company's reliance on just one distressed tenant has caused its own credit ratings to be slashed to low-grade junk status, and Uniti now faces an inability to raise any equity capital at profitable prices.

While Uniti's dividend is currently covered by cash flow that is expected to rise very slowly, the company's ability to ultimately secure its dividend for the long term is in doubt. Simply put, Uniti Group is a very high risk stock with a wide range of potential outcomes, making it inappropriate for conservative income investors."

Unfortunately, as feared, earlier this month the REIT was hit with some very bad news. UNIT's share price plunged by as much as 42% in a single day and has lost over 50% of its value since February 15.

Let's take a look at why the market has punished Uniti so severely, the company's increased likelihood of an imminent dividend cut, and where the stock could go from here.

Why Uniti Shares Fell Off a Cliff

On Friday, February 15, 2019, regional telecom company Windstream (WIN), which currently accounts for 64% of Uniti's pro-forma (accounting for recent acquisitions) revenue but nearly 90% of adjusted EBITDA, lost its court battle with hedge fund Aurelius Capital Management.

Judge Jesse Furman didn't mince words, writing that Windstream's "financial maneuvers – and many of its arguments here – are too cute by half."

At issue in the $370 million lawsuit was whether or not Windstream's 2015 spin-off of Uniti (to offload billions in debt from its balance sheet) was a sale-leaseback transaction that violated some of Windstream's bond covenants. If a bond covenant is breached the creditor (Aurelius being one of them) has the right to immediately call in the loan.

Windstream didn't believe its spin-off was a sale-leaseback transaction because of how it structured its master lease with Uniti, which owns 80% of its former fiber optic cables and leases their use back to Windstream.

Windstream had previously gotten all other creditors other than Aurelius to refinance the 2023 notes in question, including with a provision stating that the Uniti spin-off wasn't a bond violation.

Management exuded confidence in the months leading up to the ruling:

There's no uncertainty here in my mind in terms of the outcome. … Obviously, we are going to win." – Anthony Thomas, Windstream CEO, September 14, 2018

"As I have shared my view many times previously and will share here once again, the only uncertainty regarding this proceeding is when the decision will be issued."– Anthony Thomas, November 8, 2018

"We still feel very, very good about our case, our position. We feel very confident in our positions and prevailing." – Robert E. Gunderman, Windstream CFO, December 5, 2018

"[M]y view here is unchanged. The only uncertainty we have around this litigation is timing." – Anthony Thomas, January 8, 2019

However, the judge sided with Aurelius that Windstream's legal trickery didn't change the underlying fact that the very formation of Uniti was a violation of its bond covenants. He basically said it doesn't matter what all other creditors think – Aurelius is right and now owed over $300 million in the next few months.

Windstream responded to the ruling quickly saying it plans to appeal:

“We are disappointed in, and frankly surprised by, the ruling and will be taking immediate steps to pursue all available options, including post-trial motions and an appeal...Additionally, we will work with our creditors on the next course of action."

Windstream will now have to discuss with not just Aurelius, but all its creditors how it plans to pay this large judgment, which itself could trigger other bond covenant breaches and potentially billions in debt being called in the year ahead. (Windstream has over $5 billion in long-term debt and just $37 million in cash on the balance sheet).

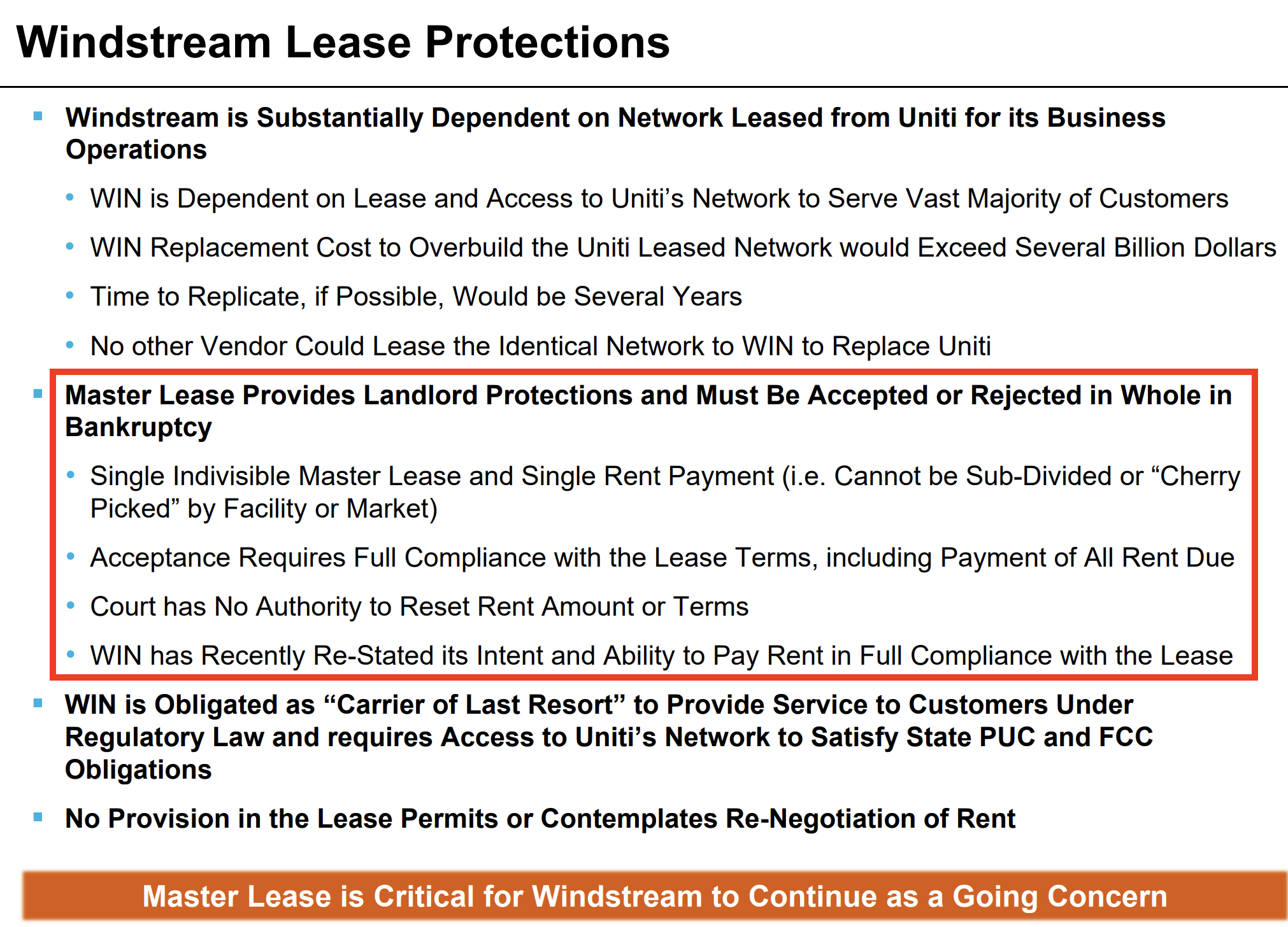

Effectively, Windstream faces a very high risk of bankruptcy because it can't possibly hope to pay off even Aurelius (much less any other creditors that might be calling in loans early). Should Windstream file for chapter 11 bankruptcy, its $650 million lease with Uniti will be tested.

A key reason Uniti investors owned the REIT was the language in its master lease agreement. Specifically, the lease theoretically ensures that Windstream is obligated to continue making its current lease payments.

That's because the contract can't be renegotiated, even in bankruptcy court. In the event of a chapter 11 filing, Windstream has 90 days to either reject the lease agreement outright or accept it. If Windstream rejects the lease (because it wants lower rental rates), then Uniti will be free to try to find other tenants for its fiber-optic assets.

Source: May 2018 Uniti Investor Presentation

However, Windstream probably won't reject the lease because as

“It is our understanding that Windstream intends to take action and pursue all available options. The validity of our master lease agreement with Windstream was not impacted by the ruling, and access to our network remains critical to Windstream’s operations and its ability to serve its customers.”

Basically, Windstream could not continue providing its customers with service without accessing Uniti's infrastructure. Filing for chapter 11 bankruptcy would not alter that dependency since this action would be designed to eliminate most of Windstream's debt and allow it to continue as a going concern.

It's also worth noting that, in theory, Windstream's lease payments to Uniti, which consume about 33% of the telecom's annual EBITDA, are an operating expense senior in its capital structure to even its bondholders.

Mind you that's only what the master lease theoretically means. Aurelius and other creditors could claim that the latest court ruling against Windstream might, in fact, invalidate the lease, since Uniti's very creation is ultimately a covenant breach that Windstream shouldn't have done.

Regardless of whether or not Uniti's lease with Windstream remains intact, ultimately the REIT's dividend seems likely to get slashed in the coming days.

Why Uniti's Dividend Appears Very Likely to be Cut

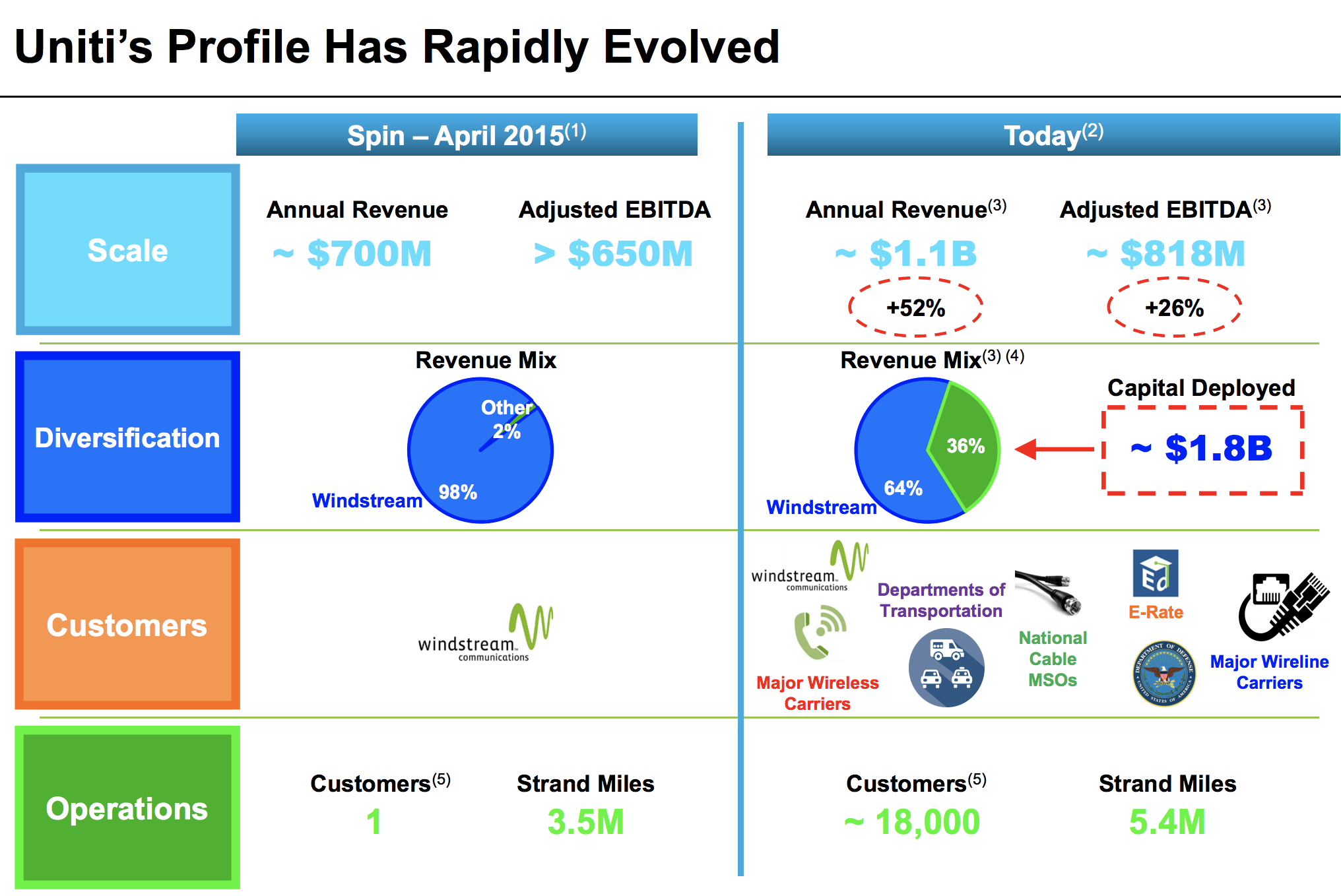

When Uniti was spun off in 2015, 98% of its revenue came from Windstream. Relying completely on a troubled regional telecom created a lot of uncertainty which weighed on Uniti's stock price.

Source: Uniti Investor Presentation

Uniti spent over $2 billion in recent years acquiring non-Windstream assets to diversify its revenue base. Moody's has said it would upgrade the REIT's credit rating once it generates 50% of its revenue from sources other than Windstream. An upgrade would help lower Uniti's cost of capital, although its credit rating would still remain deep in junk bond status.

In late 2018, Uniti announced it had lined up four potential private equity deals that could help it hit and exceed that 50% revenue diversification target in 2019.

The first of these was recently announced, a $319 million deal with Macquarie Infrastructure Partners (MIC) that would cost Uniti $175 million in cash, and result in a 20-year triple net lease with a cash yield of 9.6%.

The REIT just announced it would fund $100 million of that cost by selling 500 of its Latin American telecom towers. Essentially, this single deal will wipe out all of Uniti's liquidity (cash and remaining credit line borrowing power) even after accounting for the asset sale.

This is the smallest of the "transformative" deals that management is working on, with larger ones supposedly capable of single-handedly getting Uniti to its 50% diversification target.

But here's why Uniti's dividend is likely facing a major cut (probably 50% or so). On the firm's third-quarter 2018 conference call, management disclosed it had sold 3.3 million more Uniti shares at an average price of about $20.50 per share to pay off the credit revolver that the REIT had used to fund its acquisitions and growth investments.

Uniti says that its net debt/adjusted EBITDA ratio of 6.0 is as high as it's comfortable going (likely also as high as its own debt covenants allow). Therefore, if Uniti desires to continue growing and diversifying its revenue base, the firm will need to issue new shares to finance this spending.

However, in order for the REIT's AFFO per share (similar to free cash flow for REITs) to increase, the cash yield on its investments needs to be higher than its cost of equity.

Unfortunately, thanks to the plunge in Uniti's share price, its stock now sports an AFFO yield near 30% and a dividend yield above 25%. Management's planned acquisitions are unlikely to generate more than a 10% cash yield (the first deal is estimated at 9.6%), so it no longer makes sense for Uniti to issue new shares to fund these deals.

Even if Uniti's rent from Windstream doesn't decline (it very well might), the REIT is still firmly locked in a liquidity trap in which it can't profitably grow via selling new shares. With a payout ratio near 95%, Uniti does not retain significant internally generated cash flow to help fund its growth or strengthen its balance sheet either.

That leaves Uniti just one source of growth capital, cutting its $425 million dividend. A 50% reduction, which is roughly how much the firm can likely cut to retain its REIT status (required to pay out at least 90% of taxable income as dividends), would free up $213 million per year which at least funds its organic growth spending.

However, Uniti wouldn't likely be able to entirely fund the remaining private equity deals it identified. Each of these acquisitions appears to be larger than the $175 million cash cost of the first one. What does that mean for Uniti investors?

A major dividend cut is very likely coming (probably 40-50%), perhaps as soon as Uniti's next earnings report on February 28

A dividend cut increases Uniti's retained cash flow, but it's still not enough for the REIT to execute on its full growth plan

Management would have to pursue extremely dilutive share issuances that reduce AFFO per share in order to achieve its 50% diversification target

Further dividend cuts might be necessary, particularly if Windstream declares bankruptcy and is pressured to reduce its rent payments to Uniti

Management will either have to pump the brakes on its diversification goal, keeping the company shrouded in uncertainty as it remains dependent on an increasingly fragile Windstream, or continue pushing for growth at the expense of falling AFFO per share due to the REIT's depressed stock price.

Simply put, Uniti's first dividend cut might not be its last, and declining AFFO per share over time will likely continue reducing the REIT's intrinsic value. Uniti proved to be a value trap and should continue to be avoided by conservative income investors.

Concluding Thoughts

Uniti's double-digit yield turned out to be a clear sign that this REIT's dividend was risky and dependent on a speculative turnaround story, one that required a lot of factors (some outside of management's control) to go right.

That included Windstream winning the Aurelius lawsuit, Uniti's share price remaining at healthy enough levels to make equity financing viable, and management being able to fund accretive acquisitions to hit the firm's diversification goals.

With the disastrous trial results now making a Windstream bankruptcy a very real possibility, Uniti's thesis, which includes the current dividend being maintained, is almost certainly shattered.

Even if the master lease isn't rejected by Windstream, keeping Uniti's cash flow from its largest tenant intact, the REIT's ability to fund its ambitious growth plans will likely be severely impaired for the foreseeable future.

With over $200 million in annual organic growth capital expenditures, plus at least three more large acquisitions in the works, junk-bond-rated Uniti simply can't profitably fund its growth at current share prices.

That puts its $425 million annual dividend firmly in the crosshairs as a way to free up more capital. With earnings coming up at the end of February, and the quarterly dividend declaration usually occurring a day or two before this, investors can likely expect a steep dividend cut, perhaps about 50%, in the coming days.

The market is obviously expecting a large cut to happen given the stock's current yield, but the bottom line is that Uniti remains a very speculative investment. While even a 50% dividend cut would mean Uniti shares still sport a double-digit yield, the company continues facing a number of uncertainties which could further impair its long-term outlook.

It's possible investors have more than priced in these risks and the future won't be as bad as many people fear, but these situations just aren't in our wheelhouse. Our preference is to invest instead in financially healthy businesses which are more in control of their own destiny and appear very likely to continue paying safe, growing dividends.