AmeriGas Partners, L.P. (APU)

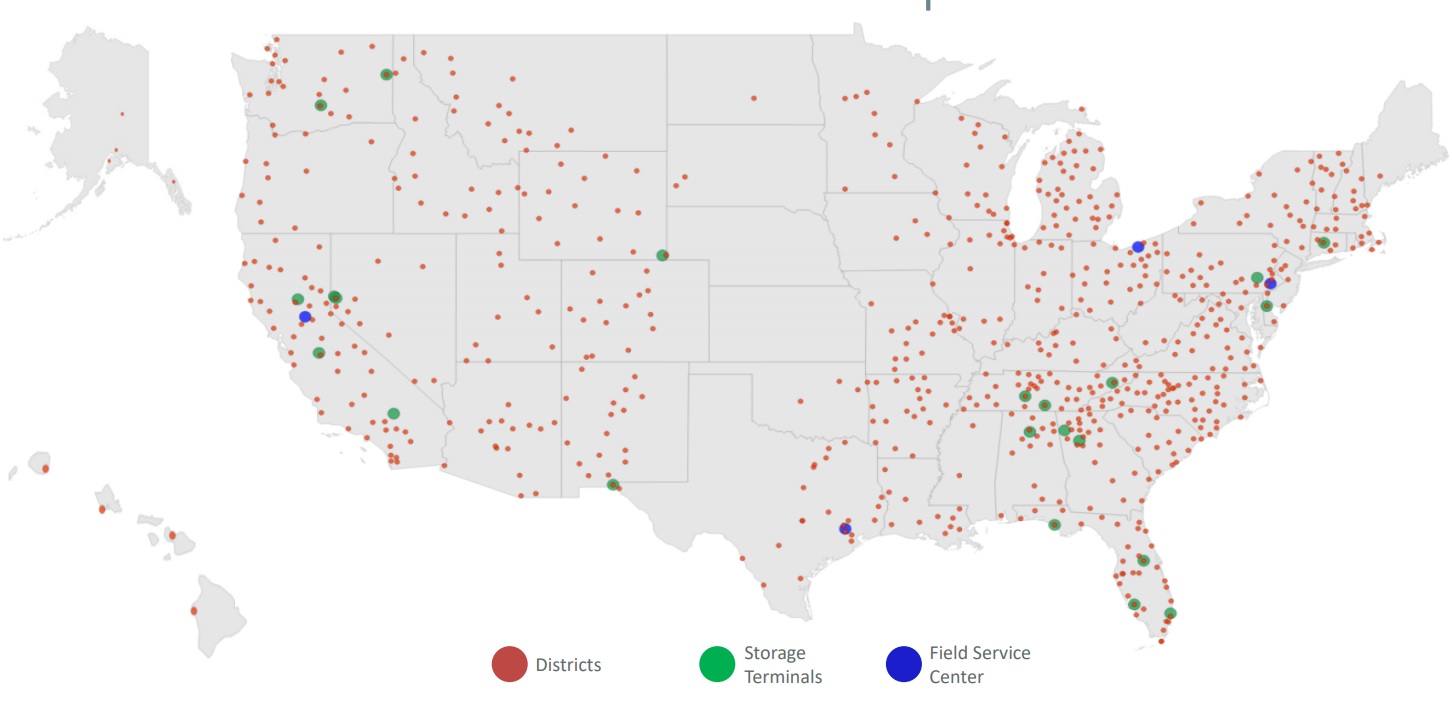

Founded in 1994, AmeriGas Partners (APU) is a master limited partnership (MLP) that is America's largest distributor of propane. The MLP sells propane to 1.8 million residential, commercial, industrial, agricultural, wholesale, and motor fuel customers in 50 states through approximately 1,900 propane distribution centers.

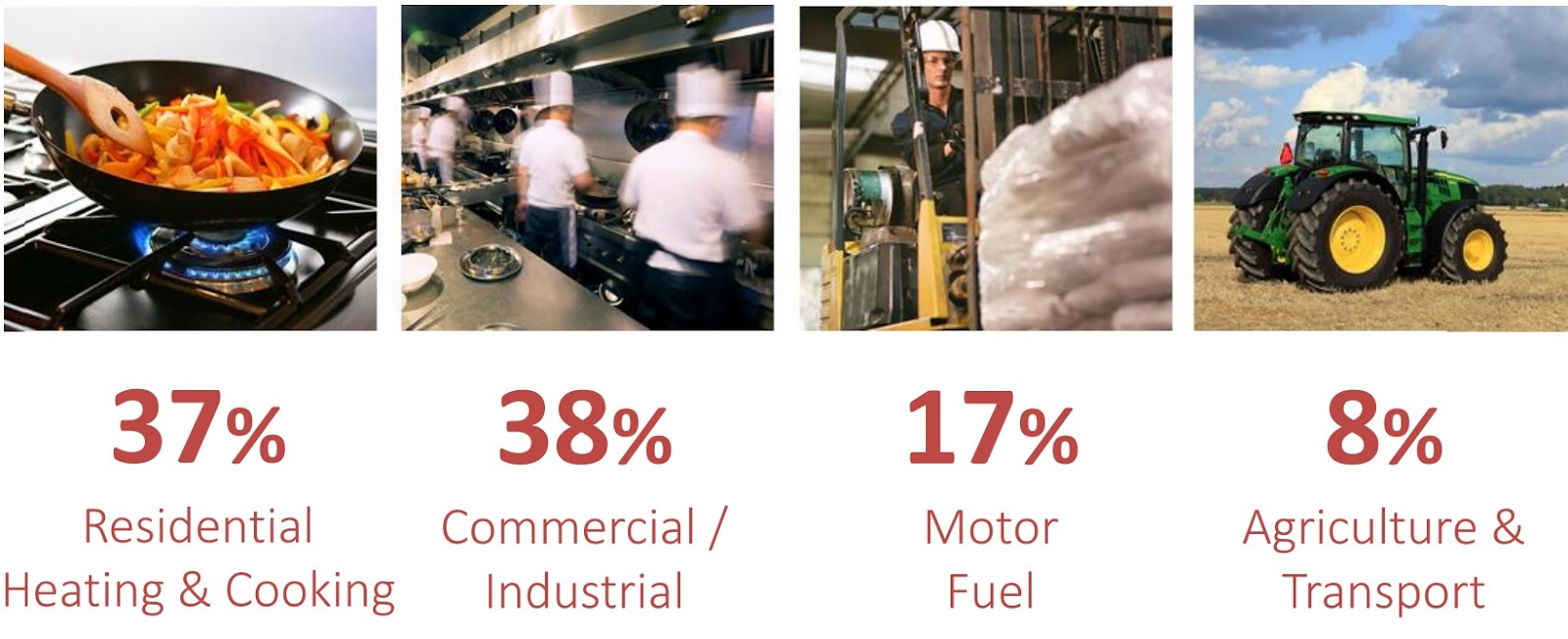

AmeriGas Partners’ propane is used for home heating, water heating, and cooking purposes; to fire furnaces, as a cutting gas, and in other process applications; as a supplemental fuel and motor fuel; and for tobacco curing, chicken brooding, crop drying, and orchard heating applications.

The company also sells, installs, and services propane appliances, such as heating systems; and offers residential heating, ventilation, air conditioning, plumbing, and related services.

However, the vast majority of the AmeriGas Partners' propane is used by residential and commercial clients for heating and cooking purposes.

The company also sells, installs, and services propane appliances, such as heating systems; and offers residential heating, ventilation, air conditioning, plumbing, and related services.

However, the vast majority of the AmeriGas Partners' propane is used by residential and commercial clients for heating and cooking purposes.

The company markets propane and other services primarily under the AmeriGas, America's Propane Company, Heritage Propane, Relationships Matter, Metro Lawn, and ServiceMark names. UGI Corporation (UGI), one of America's largest distributors of propane and liquefied petroleum gas, is the MLP's general sponsor. UGI owns 26% of Amerigas' limited units and its incentive distribution rights (IDRs).

Business Analysis

Most MLPs are tollbooth-like operators of energy distribution assets. They generate mostly fixed-fee revenue under long-term and volume committed contracts, resulting in a predictable stream of cash flow. However, propane MLPs such as Amerigas Partners are actually very cyclical businesses.

That's because their distributable cash flow, or DCF (similar to free cash flow for MLPs), is very sensitive to unpredictable winter temperatures, which greatly influence propane sales. Margins are also affected by the cost of propane, which MLPs like AmeriGas must buy at wholesale prices and then try to sell at a profit.

The U.S. propane market has also been in secular decline since 1998, with annual volumes in the industry expected to drop by about 2.5% per year in the future. The decline is due to more cost-effective natural gas taking market share from propane, which has historically dominated in more rural markets where natural gas distribution infrastructure was lacking.

However, there is a silver lining to the industry's growth struggles. Specifically, America's propane market remains highly fragmented. For example, AmeriGas is one of the nation's largest propane distributors yet commands just 13% of the country's market share. AmeriGas has been able to achieve industry-leading economies of scale via numerous small acquisitions over time, including about 200 deals since 1980 and six in 2017 alone.

The company's leading scale has allowed AmeriGas to generate some of the industry's best margins, including an 18.3% operating margin in 2017, which compares favorably to the industry's average margin of 13%.

The MLP's superior profitability is partially due to AmeriGas' above average pricing power. Many of its customers lease their propane tank from AmeriGas and are thus contracted to buy only from it for future refills. This creates higher switching costs and less customer turnover.

The MLP's superior profitability is partially due to AmeriGas' above average pricing power. Many of its customers lease their propane tank from AmeriGas and are thus contracted to buy only from it for future refills. This creates higher switching costs and less customer turnover.

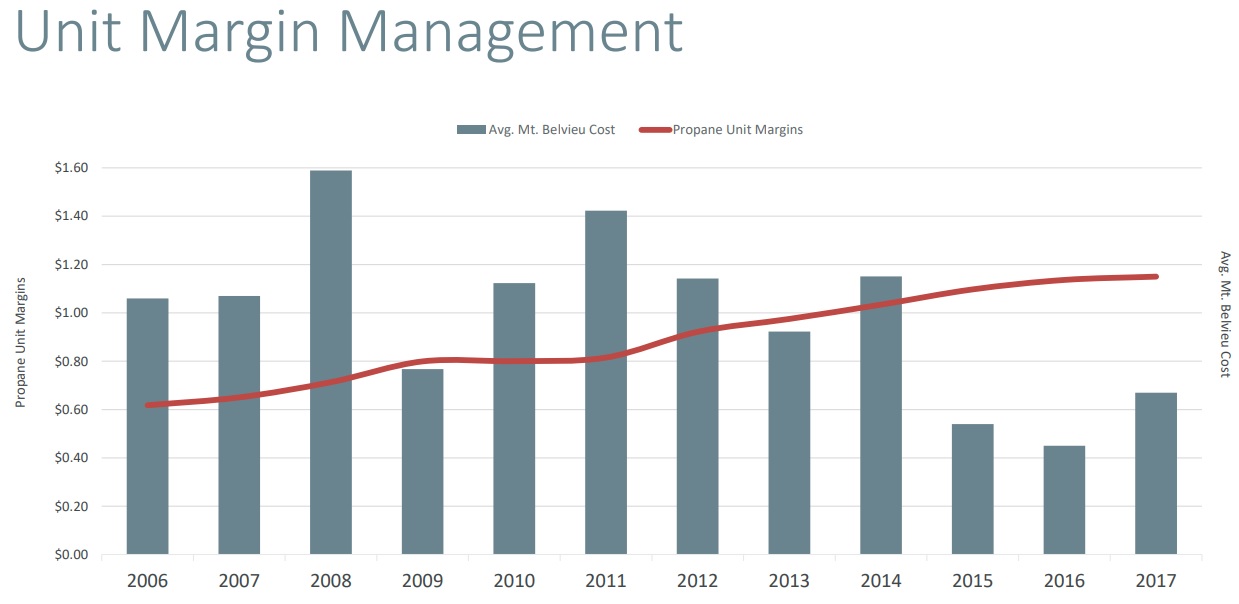

The company's acquisitive growth strategy has also allowed AmeriGas to generate relatively stable and rising cash flow despite sharp swings in both propane prices and winter temperatures.

You can see that AmeriGas' propane unit margins (red line) have remained fairly steady for more than a decade despite volatile propane prices (dark grey bars).

You can see that AmeriGas' propane unit margins (red line) have remained fairly steady for more than a decade despite volatile propane prices (dark grey bars).

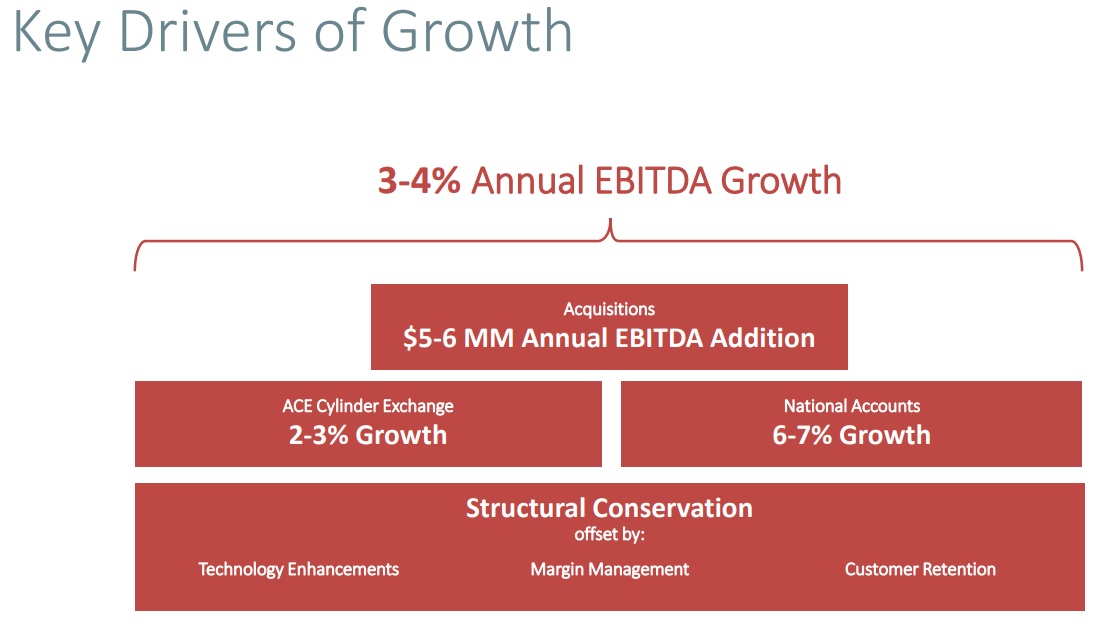

AmeriGas has been attempting to further stabilize its cash flow over time through two main growth strategies. The first is its AmeriGas Cylinder Exchange, or ACE, business, which allows customers to exchange empty propane tanks for full ones at over 50,000 retail locations around the country.

ACE sales are often most significant during the summer grilling season and thus provide a nice source of relatively stable revenue outside of the MLP's core winter business season. Management believes the convenience of this service is largely why ACE volumes increased 8% in 2017, making it one of the MLP's strongest growth drivers.

ACE sales are often most significant during the summer grilling season and thus provide a nice source of relatively stable revenue outside of the MLP's core winter business season. Management believes the convenience of this service is largely why ACE volumes increased 8% in 2017, making it one of the MLP's strongest growth drivers.

The company's other major growth driver is national accounts through which the MLP encourages multi-location propane users to enter into a supply agreement with it rather than use multiple suppliers.

National accounts allow AmeriGas to serve about 43,000 locations across the country and leverage its industry-leading distribution network and economies of scale to provide lower cost than the competition. Growth in national accounts is primarily driven by the company's largest sales force in the industry (an advantage few rivals can afford to replicate) and is also less cyclical than individual retail sales.

National accounts allow AmeriGas to serve about 43,000 locations across the country and leverage its industry-leading distribution network and economies of scale to provide lower cost than the competition. Growth in national accounts is primarily driven by the company's largest sales force in the industry (an advantage few rivals can afford to replicate) and is also less cyclical than individual retail sales.

However, despite these two growth programs, AmeriGas' internal volumes continue to decline at about 1.5% a year, a trend that is expected to continue over the long term. As a result, management will need to continue growing the business through acquisitions in order to offset secular volume declines.

Fortunately, AmeriGas estimates there are about 3,500 potential small-scale acquisitions it could make in the future to achieve its long-term goals of about 3-4% annual cash flow growth.

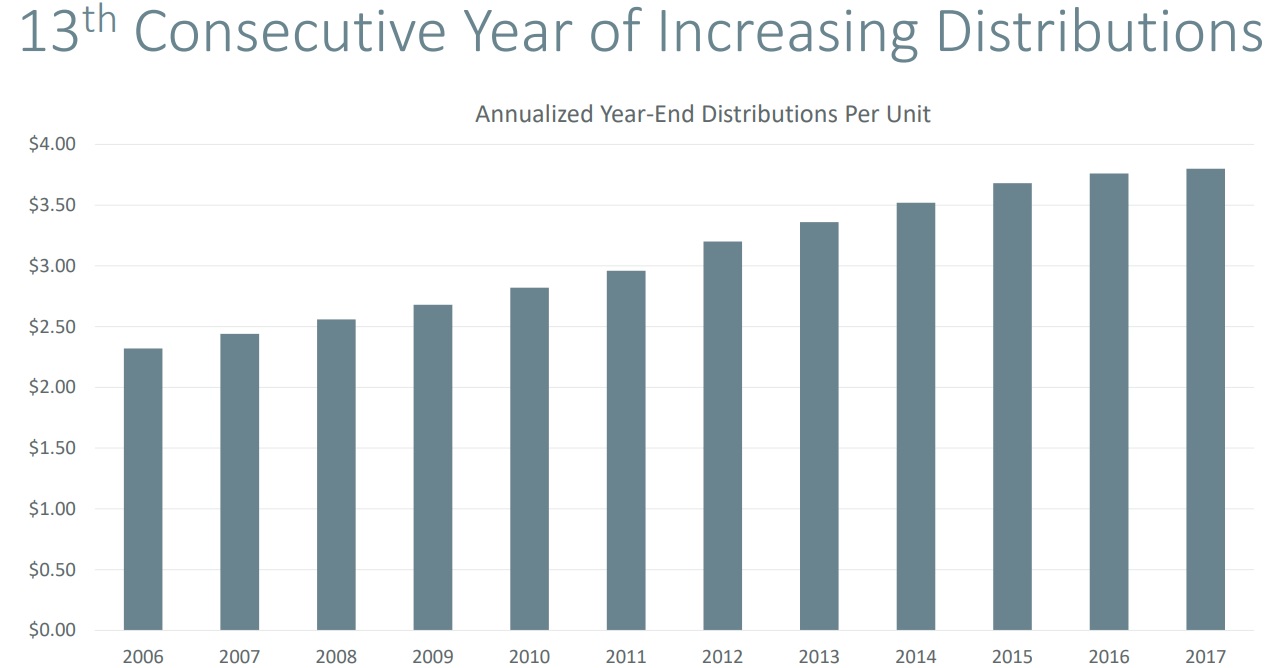

Therefore, management believes it can continue rewarding income investors with the industry's most impressive distribution track record: 23 years of stable or rising payouts, and 13 consecutive years of annual distribution increases.

However, despite AmeriGas' impressive payout growth record and management's confidence that it can achieve moderate long-term growth, there are several risk factors that make this high-yield MLP unsuitable for conservative investors.

Key Risks

AmeriGas has three main challenges to its long-term growth prospects.

First, the MLP is in a declining industry which makes organic growth harder to come by. According to AmeriGas' 2017 annual report:

"Retail propane industry volumes have been declining for several years and no or modest growth in total demand is foreseen in the next several years. Therefore, the Partnership’s ability to grow within the industry is dependent on its ability to acquire other retail distributors and to achieve internal growth, which includes expansion of the ACE program and the National Accounts program (through which the Partnership encourages multi-location propane users to enter into a single AmeriGas Propane supply agreement rather than agreements with multiple suppliers)."

In other words, AmeriGas needs to continue consolidating the industry via acquisitions and stealing market share from smaller rivals. While this might work in the short term, the fact remains that the MLP is on the wrong side of America's ongoing shale gas boom. Natural gas is simply a more economical way of both heating and generating electricity, clouding the firm's long-term outlook.

"As long as natural gas remains a less expensive energy source than propane, our business will lose customers in each region into which natural gas distribution systems are expanded. The gradual expansion of the nation’s natural gas distribution systems has resulted, and may continue to result, in the availability of natural gas in some areas that previously depended upon propane." - AmeriGas 10-K

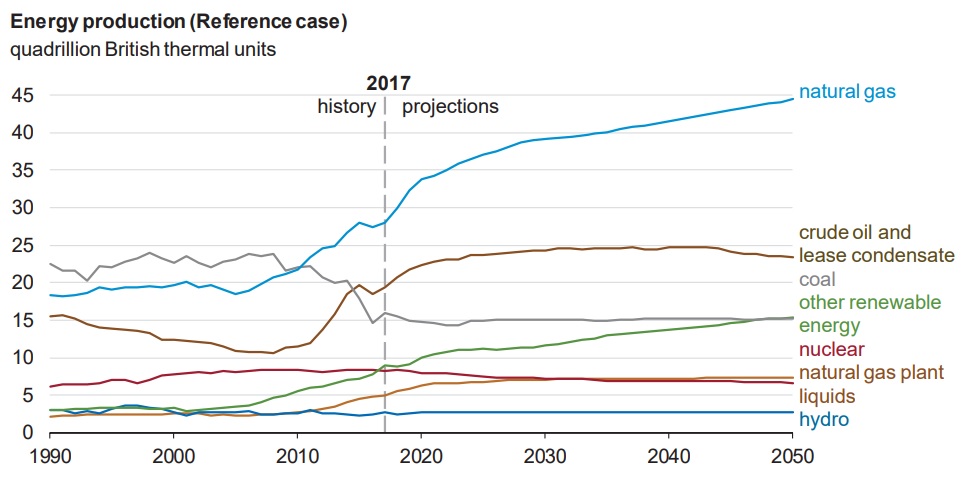

America's boom in natural gas, courtesy of improved fracking technology. means that U.S. natural gas production is expected to soar in coming years. The U.S. Energy Information Administration expects this trend to continue for decades.

Due to the strong growth projected in U.S. gas and oil production, more energy transportation infrastructure will be needed. As a result, natural gas distribution networks seem likely to continue expanding over the long term and continue whittling away at America's overall propane market.

And in the short term, AmeriGas may also face problems growing its cash flow. That's because the MLP has a relatively high debt burden which could be a liability in a rising interest rate environment.

For example, the company's leverage ratio (debt/Adjusted EBITDA) is currently 4.8, which is significantly higher than the industry average of 3.6. AmeriGas' relatively high leverage is due to the company taking on a lot of debt as it's acquired smaller rivals over the years.

For example, the company's leverage ratio (debt/Adjusted EBITDA) is currently 4.8, which is significantly higher than the industry average of 3.6. AmeriGas' relatively high leverage is due to the company taking on a lot of debt as it's acquired smaller rivals over the years.

AmeriGas therefore lacks an investment grade credit rating which means that it could have a more challenging time raising cheap capital in the future. In fact, the company's average interest costs are relatively high today at about 5.7%.

Management has said that it plans to lower AmeriGas' leverage ratio to a much safer 3.5 to 4.0 level over time. However, deleveraging will restrain the company's ability to acquire smaller rivals and continue growing its sales in an otherwise slowly decaying propane market.

MLPs can also raise capital by issuing new units. However, AmeriGas faces a high cost of equity that makes it hard to grow profitably for two reasons. First, the incentive distribution rights UGI holds redirect a substantial portion of AmeriGas' marginal cash flow to the sponsor and away from the MLP. Since MLPs in general are in a bear market, AmeriGas' low unit price has also raised the MLP's cost of equity significantly.

The relatively high cost of debt and equity capital means that AmeriGas' external cost of capital is very high, so management has said that it wants to fund its growth organically by retaining cash flow. However, there are two challenges with this plan.

Specifically, AmeriGas plans to grow its distribution much slower than its overall cash flow in order to raise its DCF coverage ratio (distributable cash flow/distributions) to 1.1 to 1.2 in the long term. Analyst expect long-term distribution growth to be about 2%, or half the overall rate of cash flow growth.

Specifically, AmeriGas plans to grow its distribution much slower than its overall cash flow in order to raise its DCF coverage ratio (distributable cash flow/distributions) to 1.1 to 1.2 in the long term. Analyst expect long-term distribution growth to be about 2%, or half the overall rate of cash flow growth.

However, according to the firm's annual report, AmeriGas' DCF coverage ratio (including growth capex) was only 0.7 in 2017, indicating that the company is paying out more in distributions then it is generating in cash flow. In other words, the current payout could prove to be unsustainable, especially given the MLP's high debt burden and need to fund growth organically.

With that said, a potential source of growth funding is a standby agreement AmeriGas has with its sponsor UGI, in which UGI has offered to buy up to $225 million in class B units.

These units don't count towards the MLP's IDR fees, but they have a distribution yield that's around 1% higher than the common units. They also have the option of being paid in distributions rather than cash, which means that in the short term AmeriGas could raise growth capital without increasing its cash distribution costs.

However, should the MLP choose to use this option, then it could prove highly dilutive to existing investors over time and could lower the safety of the payout over the long term.

These units don't count towards the MLP's IDR fees, but they have a distribution yield that's around 1% higher than the common units. They also have the option of being paid in distributions rather than cash, which means that in the short term AmeriGas could raise growth capital without increasing its cash distribution costs.

However, should the MLP choose to use this option, then it could prove highly dilutive to existing investors over time and could lower the safety of the payout over the long term.

In other words, should AmeriGas fall into a liquidity trap, the sponsor is willing to supply it with emergency equity capital, but at extremely onerous rates. Management says that this is just an emergency backstop and the company has no immediate plans to tap this source of funding.

Combine this with the highly seasonal nature of propane sales (64% of 2017 sales were from October through March), and you have a rather unsafe payout that might have to be cut in the future. This is what both of Amerigas' major rival propane MLPs have done in recent years.

- Suburban Propane Partners (SPH): 33% distribution cut in Q3 2017

- Ferrellgas Partners (FGP): 81% distribution cut in Q3 2016

Overall, the best case scenario for AmeriGas is that it might be able to grow its cash flow very slowly, and its distribution even slower, potentially allowing it to eventually achieve more sustainable long-term leverage and payout coverage ratios. In the meantime, the MLP faces a major challenge with how it can fund this growth given current debt and equity market conditions, as well as its dangerous payout ratio.

Closing Thoughts on AmeriGas Partners

AmeriGas Partners is the nation's largest propane distributor, and its substantial economies of scale give it an inherent advantage over smaller rivals. As a result, the MLP has generated one of the most impressive long-term payout growth track records in the industry.

However, the MLP's payout safety is questionable due to the secular decline in the propane market created by America's accelerating shale gas boom. Ultimately, AmeriGas may represent one of the best names in a troubled and declining industry, but it is a company that conservative income investors might want to avoid all together.