Shares of regulated utility PPL (PPL) slumped nearly 7% on Tuesday following a proposal made by the Office of Gas and Electricity Markets (Ofgem), the United Kingdom's energy regulator.

In recent years PPL has generated around half of its earnings from the four electricity distribution networks it operates in the U.K. As we discussed in our June 2018 note here (worth reading for a full background of the situation), Ofgem sets price controls that cap the revenue PPL can recover from its investments.

Here are the highlights from our past note that explain why investors had been worried about PPL for most of this year:

Ofgem sets price controls using the RIIO framework. RIIO involves setting Revenue using Incentives to deliver Innovation and Outputs. In 2015, Ofgem set price controls for electricity distribution over an eight-year period, allowing network companies to recover a set amount of revenues in exchange for providing safe and reliable services.

In other words, the current framework that PPL’s U.K. business has been operating under has effectively set base revenues through March 2023, providing a predictable rate of return on its projects so long as no major revisions are made.

Investors were anxious that Ofgem would decide to hold a mid-period review of the current price control in place for electricity distribution, which is the biggest driver of a utility’s earnings. To help with its decision of whether or not to conduct a mid-period review, during their consultation with various stakeholders in the industry regulators included an evaluation of resetting profitability targets for the country’s utility networks.

The fact that this option was included as part of the mid-period review’s consideration really spooked investors. After all, its intention was to cut network revenues by more than $850 million in an effort to reduce costs for consumers at the expense of utility shareholders.

However, Ofgem worried that the damage such an action would cause to investor confidence in utilities would more than offset the cost benefits. That’s because utilities would face much higher financing costs (lower share price, higher cost to borrow) that would need to be accounted for in their allowed return.

In late April 2018, after consulting various stakeholders, Ofgem announced it would not launch a mid-period review, keeping the current framework (including price controls for electricity distribution) in place for the next five years.

While that development was good news, we also noted that PPL was not out of the woods yet:

Therefore, PPL’s outlook over at least the next couple of years appears stable, and its dividend seems likely to remain on solid ground. However, the picture has certainly become murkier the further out you go, and I believe that is why the market has punished PPL so severely in recent months.

Specifically, Ofgem is already looking ahead to the next regulatory period that begins in 2023 for electricity distribution networks such as PPL. Plenty of details remain to be worked out, but all signs indicate that the regulatory framework that will ultimately go into place in five years will deliver much lower returns for regulated utilities.

That brings us to yesterday's news. Ofgem issued a new proposal related to its price controls that will run from 2021 to 2026 for gas distribution, gas transmission, and electricity transmission operators. The intention is to save consumers around $8.2 billion from 2021 onwards.

As investors feared, Ofgem's proposals would set the baseline returns (cost of equity) at 4%, about 50% lower than the previous price controls. In other words, the returns equity investors would enjoy on projects would be cut in half, with more money going back in consumers' pockets instead.

The regulator expects to make a final ruling in December 2020. However, it's worth noting that this proposal technically does not affect PPL's business. Here is a statement the firm issued yesterday:

The consultation document does not apply to electricity distribution network operators ("DNOs"), including PPL Corporation's ("PPL") Western Power Distribution ("WPD") networks in the U.K., and does not have any impact on PPL's current business plans or WPD operations.

A full consultation related to DNOs will begin in 2020, with new rates for DNOs not taking effect until April 2023. PPL and WPD will continue to provide input and engage with Ofgem throughout the consultation process to arrive at the best outcomes for all stakeholders.

So why did PPL's stock price drop on the news? Simply put, investors are already looking ahead to the consultation related to price controls that regulators will begin in 2020 for utilities such as PPL.

Given the initial hard stance Ofgem just took on gas distribution, gas transmission, and electricity transmission operators, it's hard to feel optimistic that electricity distributors like PPL will get to maintain anywhere close to their current level of returns in the next price control period.

Fortunately, PPL's existing operating conditions and rate levels in the U.K. should remain steady through the first quarter of 2023 based on the current framework, providing management with a decent amount of time to gain more clarity on these issues and hopefully position the business accordingly.

Regardless, PPL should be kept on a short leash as regulatory developments need to be closely monitored. The good news is that the company appears to have time on its side, and PPL's stock does not appear to have high expectations.

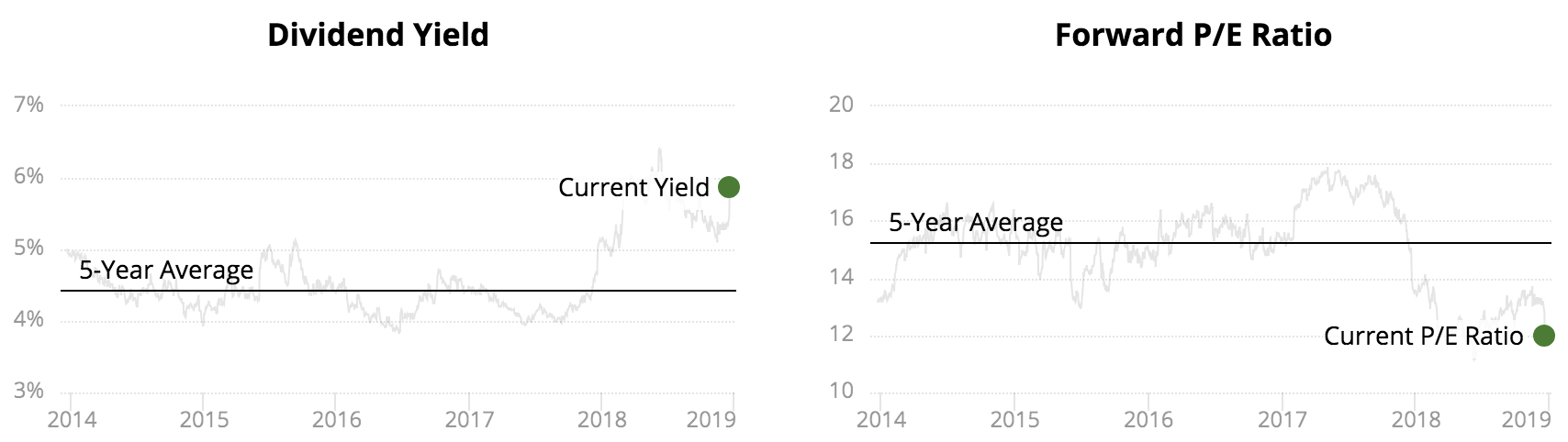

Source: Simply Safe Dividends

PPL's dividend also continues to look safe for now, and we plan to hold our shares (less than 3% of our Conservative Retirees portfolio's value) until more is known in the next year or two. In the quarters ahead management will certainly be discussing the regulatory environment and PPL's mitigation plans with investors, hopefully providing us with more clarity on how to proceed.

Should PPL's situation look increasingly dire, or its valuation revert to more normal levels, we would consider moving onto another utility with less regulatory risk. After all, regulated utilities are expected to serve as a ballast in conservative dividend portfolios, providing stable returns and predictable, growing income.

PPL could certainly continue meeting those objectives like it has for many years (nearly two decades of uninterrupted dividends), but the dynamic regulatory climate in the U.K. makes the firm's long-term outlook cloudier for now.