Reviewing Magellan Midstream's Historically High Yield

Whenever a high-yield stock falls significantly, it's natural that income investors want to know if it's just random noise (and potentially a buying opportunity) or a sign that something is wrong with a company's business model that could threaten the safety of the dividend.

Magellan Midstream Partners (MMP) is one of the popular master limited partnerships, or MLPs, in the market. However, even this blue-chip stock has fallen 15% since mid-August, pushing its yield to an eight-year high of 6.6%.

Let's take a look at why the market is so bearish on Magellan to assess whether the partnership remains on solid ground, or if its distribution and long-term outlook could be in trouble.

Why Magellan's Stock Has Likely Fallen So Hard

While short-term stock prices often fluctuate for any number of reasons, there are three likely drivers behind Magellan's current weakness.

The first is the ongoing MLP bear market, which began in mid-2014 and was triggered by one of the worst oil crashes in history (crude plunged more than 70% from its peak).

Since then, rising long-term interest rates, two stock market corrections, and a major regulatory rule change have combined to create a perfect storm of negative market sentiment.

Magellan has held up better than the average MLP (the Alerian MLP ETF (AMLP) has lost 30% since 2014 while MMP shares returned -18%), but the stock has still delivered negative total returns over the last four years while the broader U.S. stock market soared.

Today the market's bearishness on MLPs is likely being sustained by two additional factors. The first is the breaking of the traditional MLP business model.

That model, in which an MLP raises growth capital from debt and equity markets (sells new units), has been hampered by persistently low unit prices and thus high costs of equity.

Combined with the standard MLP having incentive distribution rights, or IDRs (which send up to 50% of marginal cash flow above a certain quarterly payout to the general partner), this results in much higher costs of capital.

As a result, the MLP industry has seen a wave of corporate restructuring including:

MLPs buying out IDRs in all stock deals (such as MPLX)

General partners (usually corporations) buying out MLPs (like Enbridge recently did with its MLPs)

MLP mergers (like Energy Transfer recently did)

MLPs converting to corporations (like Antero Midstream is doing)

One reason investors generally dislike these deals is because they generally precede a shift to a self-funding business model, in which an MLP will retain enough internally generated cash flow to replace the portion of the growth budget previously funded by issuing new units.

While self-funding business models make MLPs' growth financing independent of fickle stock prices, it also means higher coverage ratios (distributable cash flow / distributions) and lower debt levels (which is a good thing). As a result, self-funding MLPs typically have slower payout growth rates, usually between 2% and 10%, rather than 10% to 20% as seen under the old business model.

Another reason the market might dislike MLPs right now is worries that lower corporate tax rates (plus negative implications of a recent regulatory change from FERC) might cause some MLPs to convert to corporations. That would have negative tax implications for investors (any deferred tax liabilities become due upon completion of either a conversion or buyout by a corporation).

Finally, despite their cash flow being relatively commodity insensitive (due to the tollbooth-like nature of the business model), MLPs might be suffering due to oil prices recently crashing over 30% from their early October highs.

In fact, in November crude prices fell at their fastest rate since October 2008. This price decline is due to fears of a possible global oil glut in 2019 resulting from slowing global economic growth (slower demand growth) and the continued strong growth in U.S. shale oil production.

During the oil crash, all MLPs fell hard and fast due to concerns that bankrupt oil & gas producers might default on or restructure their long-term contracts with midstream businesses, thus hurting MLP cash flows and forcing distribution cuts. The market might be worried that an "oil crash 2.0" is coming that could rekindle such events.

With a better understanding of the potential reasons for Magellan's recent slide, let's examine whether any of these fears are justified.

Magellan Appears to Remain a Fundamentally Sound MLP

First off, let's address the biggest worry that investors might have, that we're at the start of another oil crash that could put MLP payouts at risk. This seems unlikely for two main reasons.

First, the last oil crash was triggered by a price war between the Organization of the Petroleum Exporting Countries (15 oil-exporting nations) and U.S. shale producers. Saudi Arabia and Russia, the world's two biggest oil producers at the time, thought that by pumping at maximum capacity they could drive oil prices low enough to bankrupt the U.S. shale industry. At the time, breakeven prices were estimated to exceed $80 per barrel for most U.S. shale formations.

In addition, before the oil crash many energy producers were funding production growth with not just internally generated cash flow but also debt and equity, resulting in stretched balance sheets and high financing risk. As a result, the first oil crash bankrupted more than 100 U.S. companies (about 3% of the industry).

But since the oil crash ended, U.S. oil producers have become far more conservative (most funding production purely from cash flow) and have aggressively deleveraged.

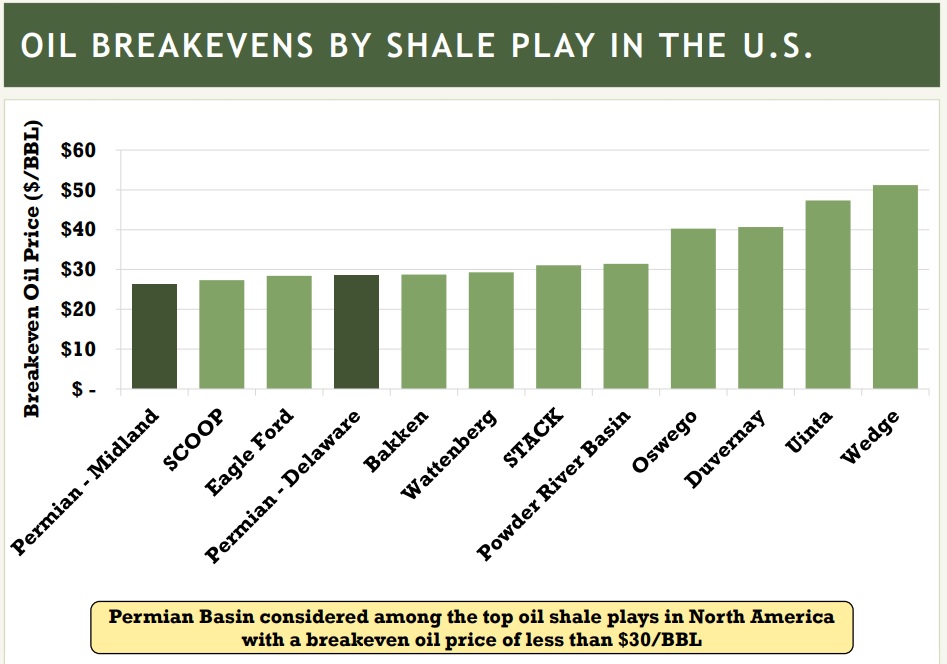

In addition, breakeven prices on U.S. shale have plunged. Most of America's largest shale formations can now be profitably drilled at $40 per barrel or less, with the Permian basin having breakeven costs of just $27 per barrel.

Source: Pioneer Natural Resources Investor Presentation

Today oil is hovering just over $50 per barrel, meaning that most big producers (the major MLP customers) are presumably able to profitably fund growth with operating cash flow even at current or even significantly lower crude prices.

OPEC and Russia have said that they plan to work together to avoid another oil crash (oil hit a low of $26 per barrel in 2016). So while no one can predict where the price of oil will go over the short term, it seems unlikely that prices will fall and remain below breakeven levels for most shale producers.

What's more, one of the main drivers of the current oil plunge is booming U.S. shale production, which is now far more sustainable than before. Strong domestic energy production has maxed out pipeline capacities nationwide and spurred the industry to construct new projects as fast as possible, but only after locking in nearly 100% of capacity under long-term, fixed-rate and often volume committed contracts.

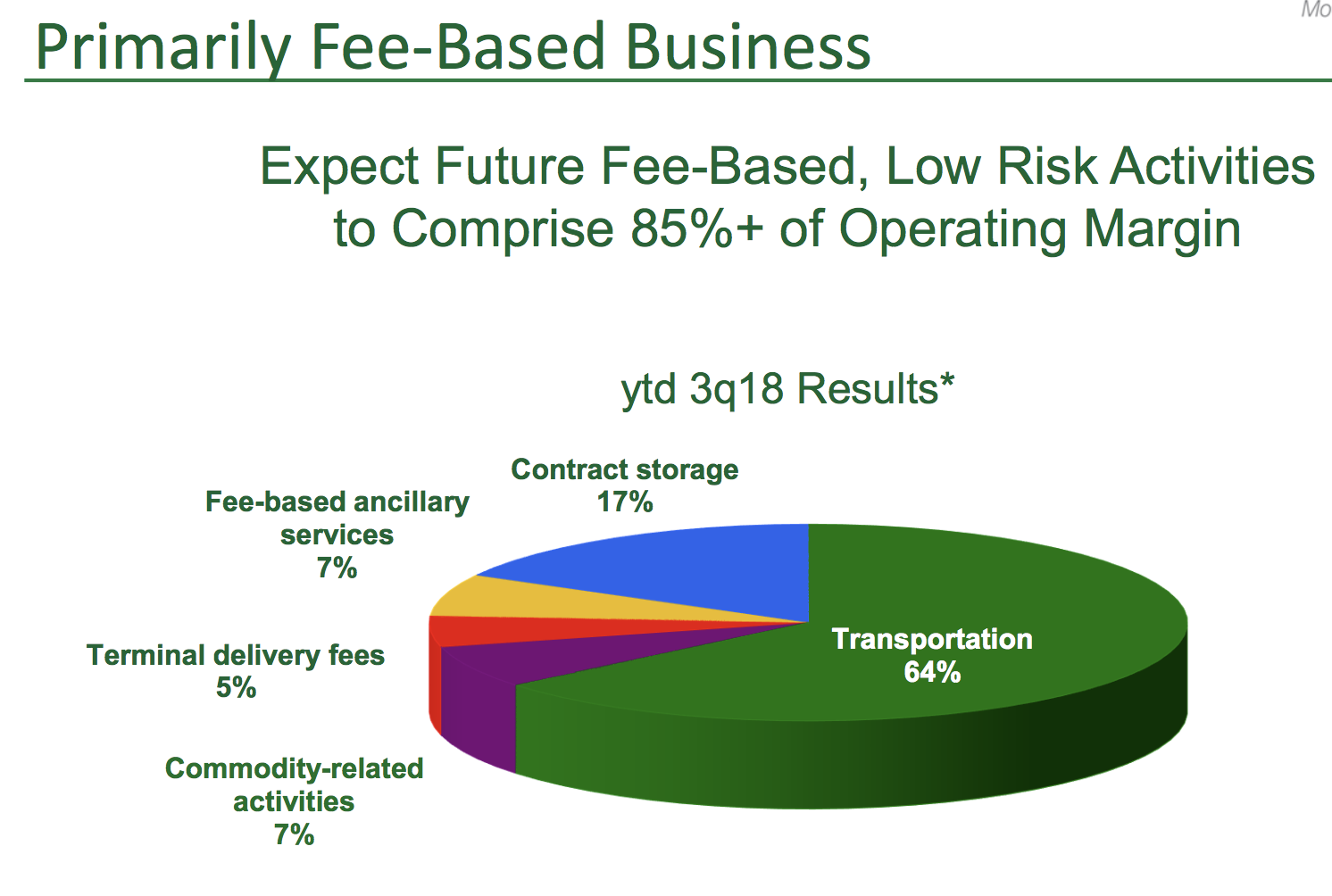

Those contracts help make MLP distributable cash flow (similar to free cash flow for MLPs) very stable and insensitive to the prices of oil and gas. In fact, approximately 85% of Magellan's cash flow is under long-term contracts, with just 7% sensitive to commodity prices.

Source: Magellan Investor Presentation

What about the market's worry about the MLP business model breaking? During the last oil crash, the reason so many MLPs had to cut their distributions was due to dangerously high debt levels and an over-reliance on equity growth funding.

Before the oil crash, MLPs would grow their payouts as fast as possible and the average coverage ratio was around 1.05 times (i.e. for every $1.05 in distributable cash flow that was generated, $1 was paid out in distributions).

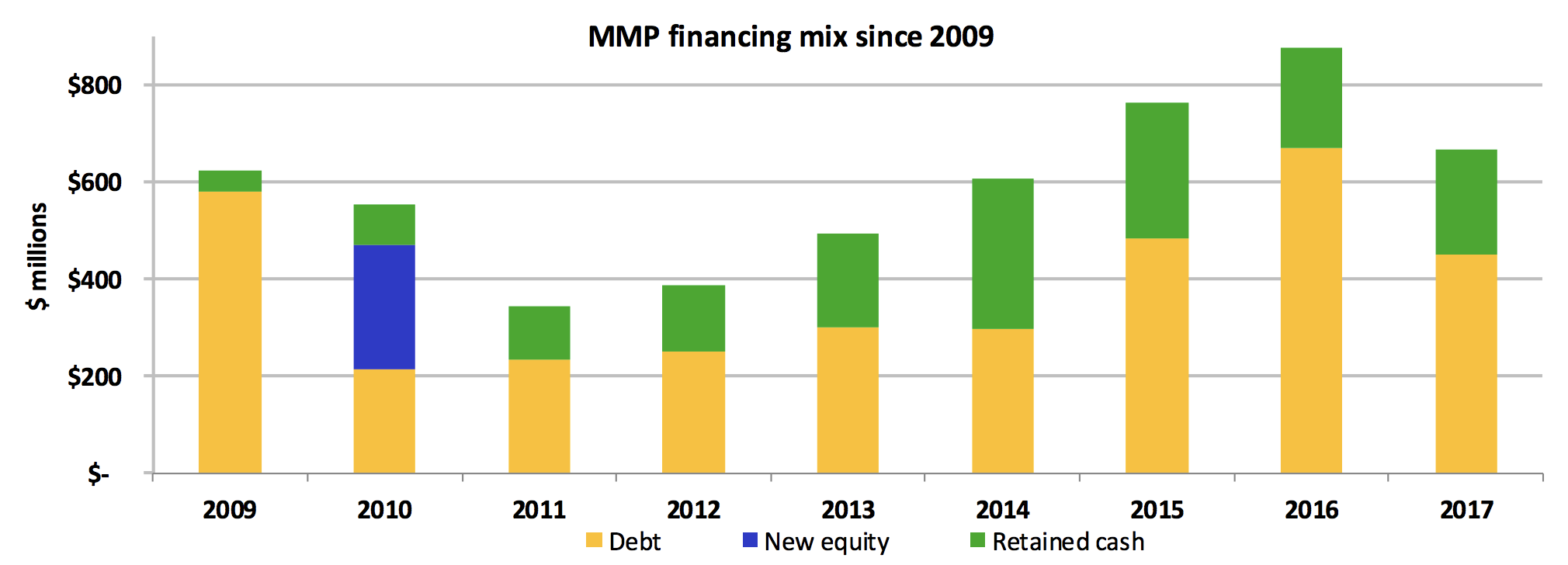

In other words, they were retaining almost no cash to fund growth. Today the big shift to self-funding business models means zero reliance on equity markets, making MLPs' stock prices irrelevant to growth plans or distribution security.

Magellan was the first MLP in the country to adopt a self-funding business model. In fact, the last time it issued equity was in 2010 when it bought out its general partner's IDRs. Since then, Magellan has enjoyed a low cost of capital and its conservative 1.2 distribution coverage ratio (1.1 or above is considered sustainable in this industry) has allowed it to completely avoid new equity issuances.

Rather, Magellan has purely relied on retained cash flow and modest amounts of low cost debt, which it never lost access to thanks to its BBB+ credit rating. That's tied for the strongest in the industry along with other midstream blue-chips such as Enbridge (ENB) and Enterprise Products Partners (EPD).

Source: Magellan Investor Presentation

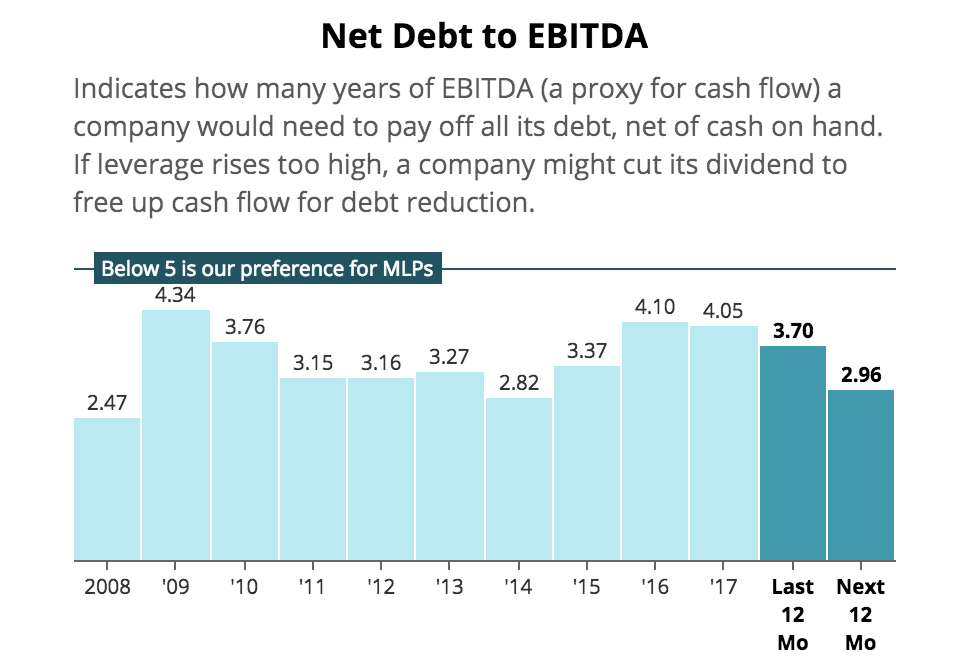

In fact, while the average MLP's debt/adjusted EBITDA (leverage) ratio peaked at 6.5 during the oil crash, Magellan's has never gone above 4.0. Credit rating agencies generally consider 5.0 or below a safe level for most MLPs, due to the stable nature of their contracted cash flow and low commodity sensitivity.

Magellan maintains an official policy of keeping its leverage ratio below 4.0. As of the third quarter of 2018, Magellan's leverage ratio was trending below 3.0, one of the lowest in the industry.

Since Magellan is already self-funding and is unaffected by the recent FERC regulatory change, the MLP does not appear to have a compelling reason to convert to a corporation. The higher tax bill Magellan and its investors would face from a corporate conversion doesn't help either.

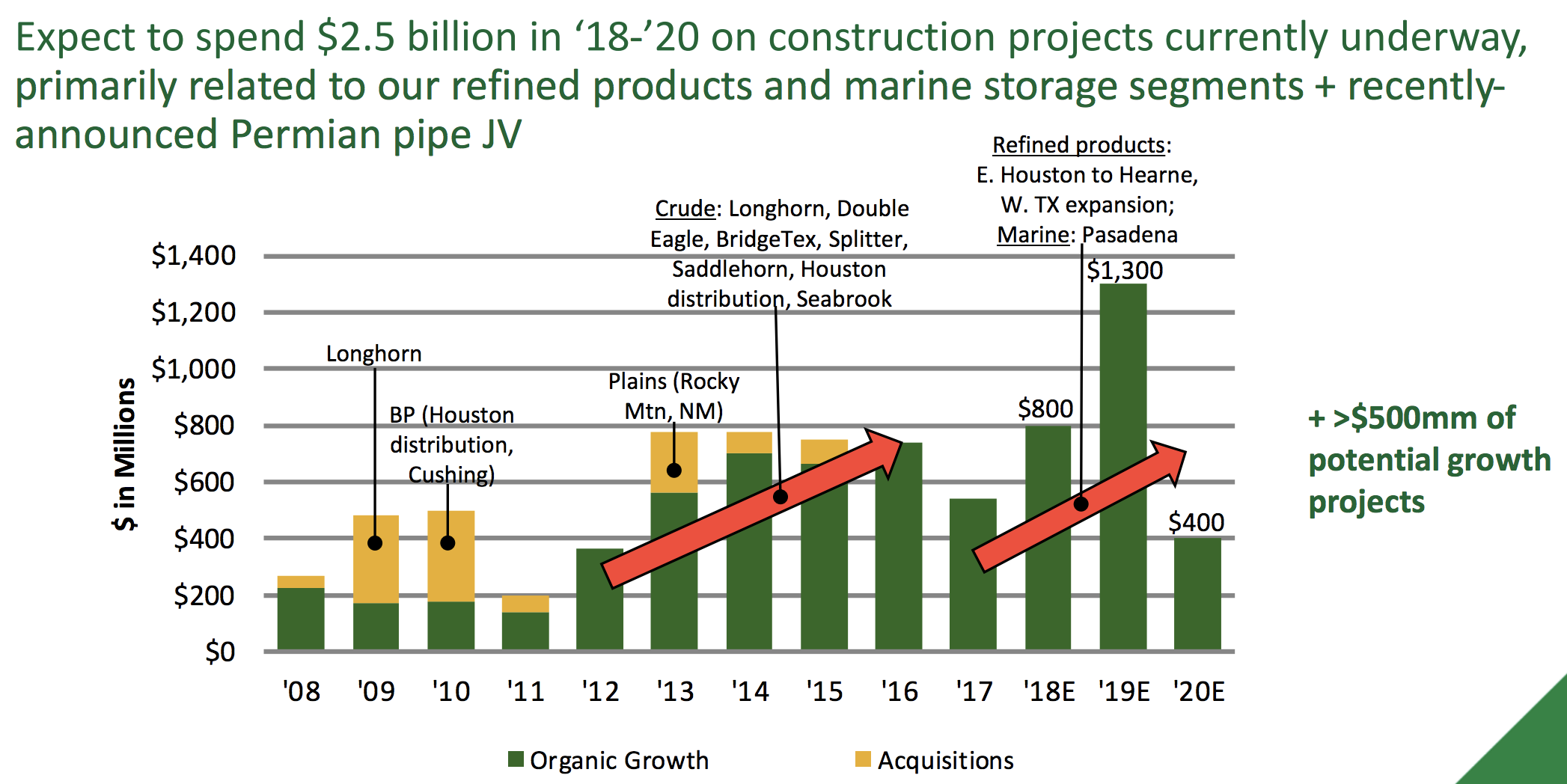

If Magellan's distribution appears safe, then perhaps the recent decline in MMP's unit price be due to worries about slowing future growth? Actually, Magellan's current $2.5 billion project backlog is the largest in the MLP's history.

Source: Magellan Investor Presentation

Management also says that it has "well in excess of $500 million" in new projects it's currently evaluating and attempting to secure long-term contracts for. Note that "over $500 million in projects under evaluation" has been Magellan's standard long-term backlog guidance for the last 16 years.

Adding "well in excess of" to that statement highlights just how many profitable opportunities for growth management is finding today. Some examples include oil export terminals and crude pipelines linking the booming Permian basin to export stations on the Gulf Coast.

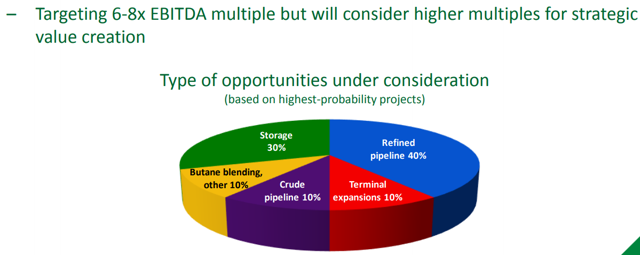

Magellan's management doesn't appear to be pursuing growth for growth's sake, either. The firm targets only projects with EBITDA yields of 12.5% to 16.7% (6-8x multiple) and has consistently earned a mid-teens return on invested capital over the years. It's unlikely that energy market volatility would threaten the viability of these projects.

Source: Magellan Investor Presentation

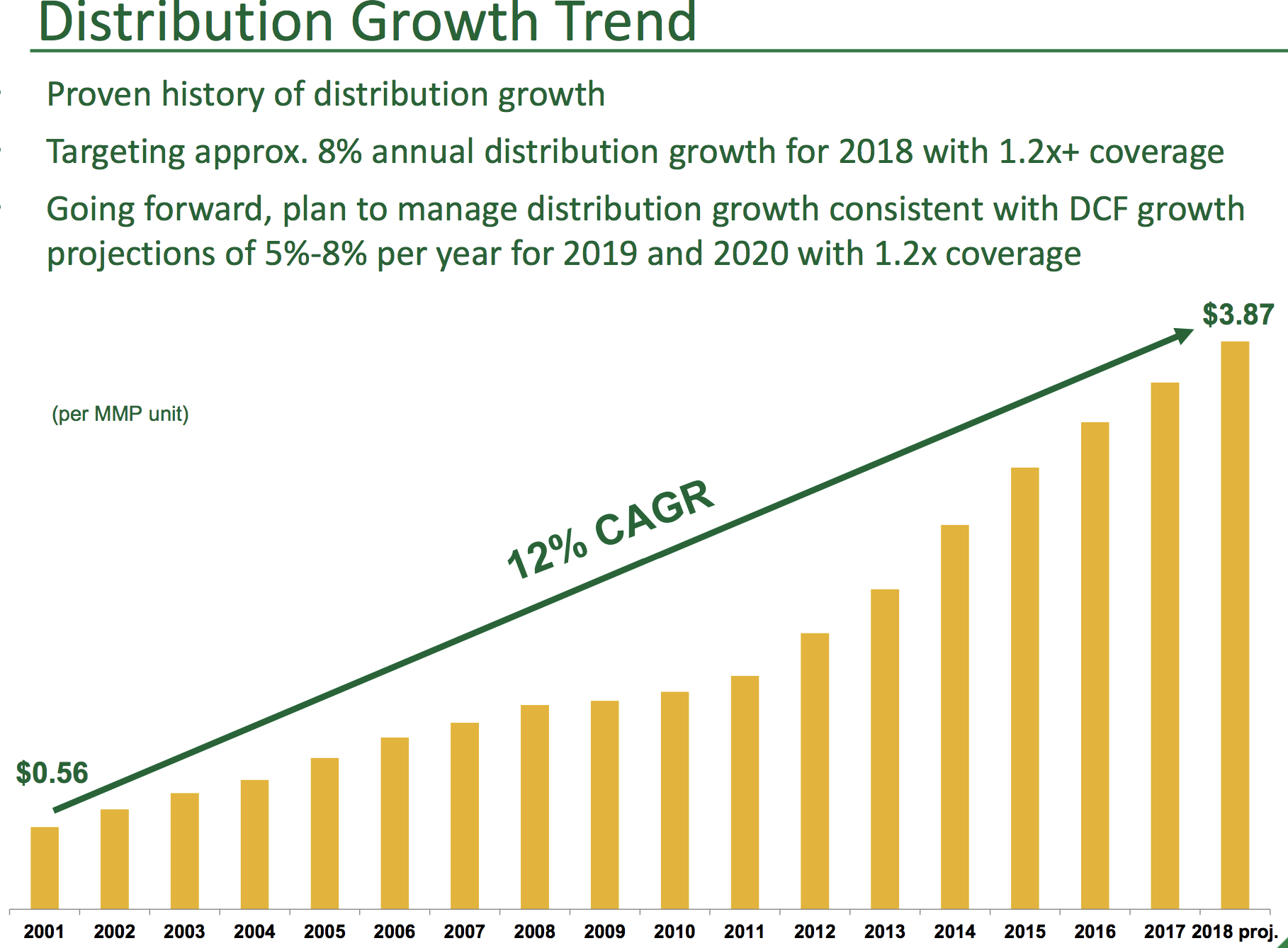

Management's disciplined capital allocation strategy is why in 2018 Magellan is on track for 10% growth in distributable cash flow per unit, which is fueling an 8% increase in this year's payout with 5% to 8% growth planned for 2019 and 2020.

Source: Magellan Investor Presentation

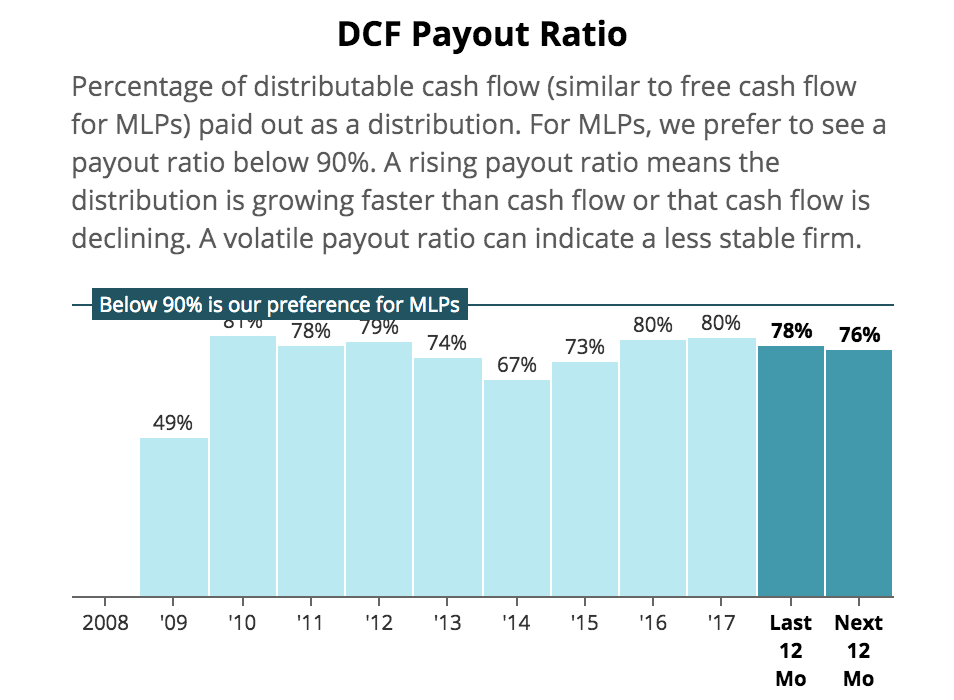

Magellan has raised its distribution for 65 consecutive quarters, or 17 straight years. That time period includes two recessions (including the financial crisis), two oil crashes, and interest rates as high as 7%. With a healthy balance sheet and a conservative payout ratio below 80%, the firm's impressive track record seems likely to continue despite the recent slump in its unit price.

Source: Simply Safe Dividends

Simply put, Magellan is a proven MLP and seems likely to continue delivering reliable and fast-growing payouts for years to come, no matter what the economy, oil prices, or interest rates are doing.

Concluding Thoughts

While there are many reasons that midstream MLPs have been in a bear market for four years, Magellan's recent price decline does not appear to have anything to do with its company-specific fundamentals.

The firm's stable and growing cash flow remains nicely secured by long-term contracts, Magellan's balance sheet is among the strongest in the industry, and the partnership's long-term growth funding has no need for issuing equity. There also does not appear to be risk of the MLP needing to convert to a corporation.

For investors interested in the MLP space, Magellan appears to remain one of the safer bets. With the stock's yield at an eight-year high, now could be a reasonable time to give the firm a closer look as part of a diversified income growth portfolio.