Kraft Heinz Remains a Riskier Dividend Stock as Turnaround Work Continues

In August 2019 we published a note reviewing why Kraft Heinz remains a speculative dividend stock.

Kraft Heinz (KHC) has roots dating back to 1869, but the company was technically formed in 2015 by the $45 billion merger of Heinz and Kraft that was put together by a partnership of Warren Buffett's Berkshire Hathaway (BRK.B) and Brazilian private equity firm 3G Capital. This created the fifth largest food maker in the world and the third largest in the U.S. with more than $25 billion in revenue.

Today Kraft Heinz sells products in over 190 countries under numerous household brand names such as Heinz, Kraft, Oscar Mayer, Philadelphia, Velveeta, Lunchables, Planters, Maxwell House, Capri Sun, Ore-Ida, Kool-Aid, and Jell-O.

Source: Kraft Heinz

Kraft Heinz's sales are highly diversified by food type:

Condiments and sauces: 25% of revenue

Cheese & dairy: 21%

Frozen meals: 10%

Meats & seafood: 10%

Shelf-stable meals: 9%

The company's sales are largely concentrated with its largest wholesale clients. For example, Walmart (WMT) accounts for about 20% of revenue. Kraft Heinz's top five customers in the U.S. represent nearly 50% of sales, and in Canada, the top five buyers drove over 70% of revenue.

Geographically, Kraft Heinz remains heavily concentrated in the U.S., which accounts for approximately 70% of sales and adjusted EBITDA. Canada, Europe, and the rest of the world account for 8%, 9%, and 13% of revenue, respectively.

At the end of 2017 Kraft had completed most of the Heinz merger integration. However, in early 2019 the company admitted that Heinz had greatly overpaid for Kraft, taking a $15.4 billion write-down on its two biggest brands and announcing a 36% dividend cut to retain more cash and accelerate de-leveraging.

Business Analysis

Consumer staples companies such as Kraft Heinz enjoy several qualities that can potentially make them attractive income investments. For one thing, these businesses tend to have stable sales and recession-resistant cash flow. That's largely thanks to people's constant need to eat, as well as Kraft Heinz's large portfolio of well-known brands, including eight that generate over $1 billion in sales each year.

Source: Kraft Heinz Investor Presentation

Over their corporate lives, Kraft and Heinz have spent billions of dollars on marketing to improve consumers’ awareness and perceptions of their products. As a result, the company was historically able to raise prices without seeing a major impact on demand.

With products in virtually every U.S. household (management estimates that Kraft's household brands account for about 5% of all U.S. grocery sales) and leading market share positions across most core product categories, Kraft and Heinz are key vendors for the retailers that sell their products. They can also afford to invest in in-store displays, coupons, and rebates to help consumers buy more products.

As a result, it’s not easy for new entrants to take shelf space from these giants and convince consumers and retailers that they are better. They lack the capital for marketing, and building brand awareness takes a long time.

Kraft Heinz’s extensive distribution channels are another competitive advantage. As the company develops new products or acquires other brands, it can sell these new offerings to existing customers while improving their cost profile as they scale. This helps the business respond to evolving consumer tastes to remain relevant.

The company also enjoys large economies of scale thanks to the integration of its own manufacturing, supply, and logistics chain with that of Heinz, which keeps its costs very competitive. This potential benefit helped plant the seed to eventually combine Kraft and Heinz around five years ago.

In 2013, Warren Buffett's Berkshire Hathaway partnered with Brazilian private equity firm 3G Capital to buy Heinz for $23 billion. The deal left Berkshire and 3G with 50% ownership in one of the largest food companies in the world, with nearly $12 billion in 2012 sales. About 60% of revenue was generated outside the U.S., with most from Europe, but about 25% from fast-growing emerging markets.

Then, in 2015, Heinz bought Kraft in a $45 billion deal that would combine Kraft's dominant position in the U.S. with Heinz's stronger global presence. Today Berkshire and 3G own 27% and 24% of Kraft Heinz, respectively. 3G, famous for its cost-cutting prowess, said it would help the combined company slash $1.5 billion in annual costs within three years.

Thanks to a strong focus on cost savings, closures of less efficient production facilities (and opening new ones in lower cost countries), and efforts to streamline supply and logistics chains, Kraft Heinz managed to achieve $1.7 billion in cost savings by the end of 2017, when its major integration efforts were complete.

However, as we'll discuss in the risk section, these cost-cutting efforts, while technically successful, came at a steep cost to the company's core brands.

Kraft Heinz's focus on economies of scale and cost savings is why the company's operating margin in 2018 was 23%, among the highest in the industry. However, cost savings can only grow a company's earnings and cash flow so far which is why management is focused on a multi-pronged approach to achieve more sustainable growth in the years ahead.

The first part of the plan is to expand Kraft Heinz's brands in existing sales channels. Since the food service market is a nearly $700 billion global business, Kraft Heinz believes it can achieve meaningful long-term growth, both domestically and worldwide, by increasing the presence of its well-known brands.

The main targets are Heinz condiments, Kraft snack foods, and Planters peanuts to sales of bars, hotels, restaurants, and institutions. Note that in 2017 Kraft suffered a major distribution loss with Planters due to a weakening of that retail relationship due to insufficient marketing (more on this in a moment).

Source: Kraft Heinz Investor Presentation

The second part of the growth plan includes expanding its brands into related categories. For example, Heinz was best known for ketchup and mustard, but in recent years the brand has found success in launching mayo and barbecue sauces.

Importantly, Kraft Heinz is trying to adapt its portfolio to changing consumer tastes, including preferences for healthier foods, organic products, and less processed selections.

For example, Kraft eliminated artificial preservatives, coloring, and flavoring from its famous macaroni and cheese. Kraft has also launched new brands in frozen foods, including the Devour (frozen snacks) and SmartMade (frozen meals) offerings.

In addition, Kraft Heinz is constantly experimenting with new brands, including highly portable and convenient adult snacks to support an on-the-go lifestyle. These offerings include its new portable protein packs which have helped make Kraft the number one player in the adult meal combo space.

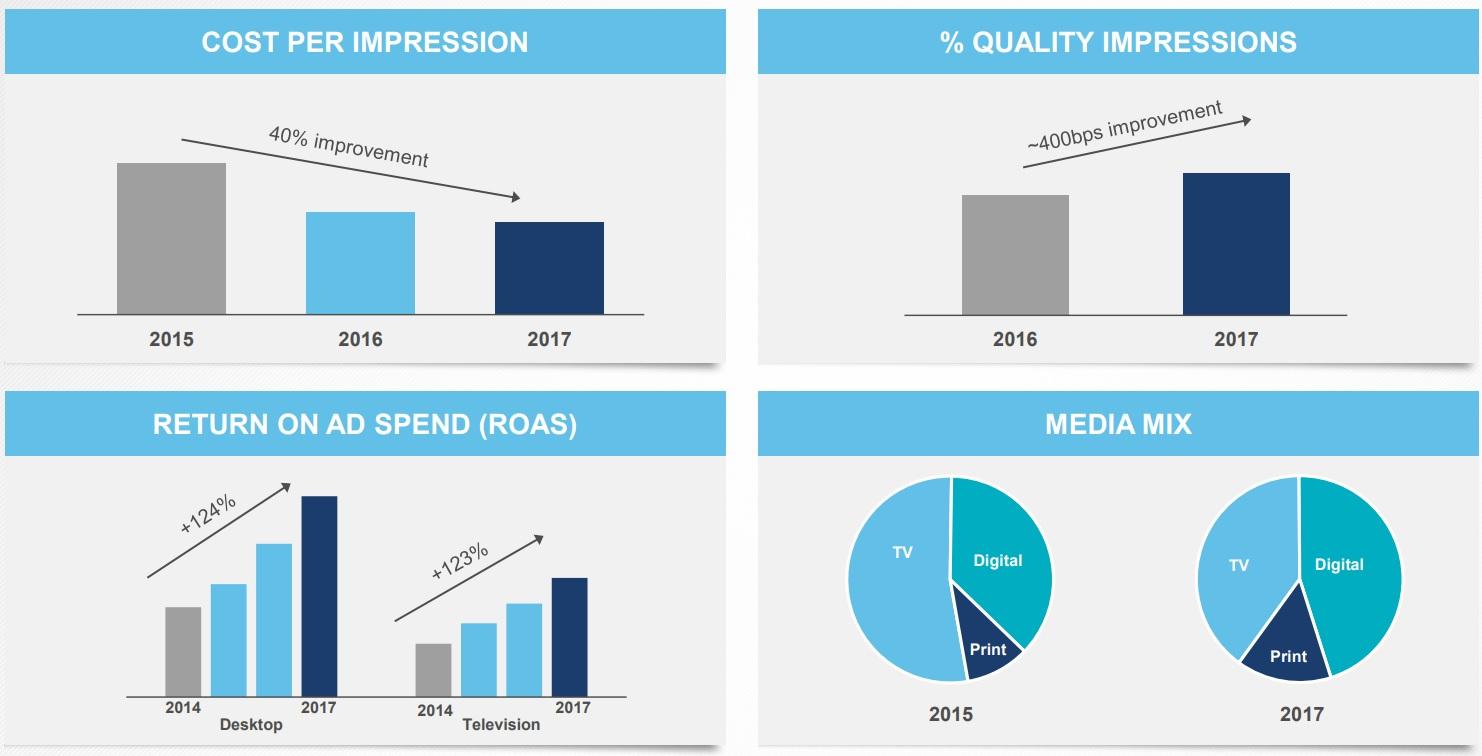

Meanwhile, in an effort to improve its brand equity and pricing power, Kraft Heinz invests heavily in digital data analysis, particularly in regards to its marketing efforts. The goal is to spend marketing dollars most cost-effectively and with the greatest positive effect on sales.

Source: Kraft Heinz Investor Presentation

The company is essentially trying to ensure that it adapts to changing consumer tastes, not just in what people consume, but also how they interact with media. One reason why Kraft Heinz is so excited about online marketing is that, according to management, 80% of consumers research groceries online, and 80% of that group uses digital apps to shop for food.

Going forward, the company hopes that this kind of data-driven, more targeted advertising will help to improve brand loyalty with Millennials, who are now starting families and will only represent a growing share of overall food spending.

Analysts expect the company to increase brand investment (R&D and marketing) by about 60% in the coming years to improve its competitiveness. Kraft Heinz hopes digital marketing can be a way to leverage this spending so that, despite still underspending most of its rivals, it can obtain positive top and bottom line growth.

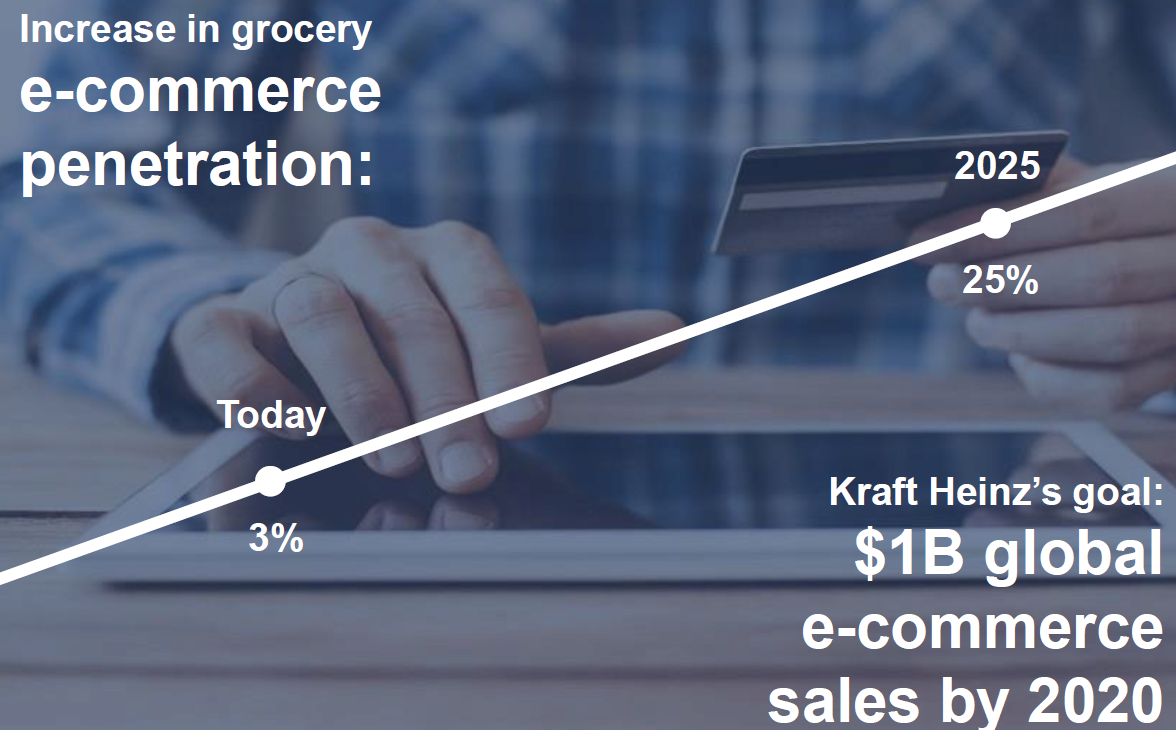

Besides marketing, another important investment area for Kraft Heinz is online grocery sales. By 2020 management expects to grow the firm's online sales to $1 billion, or about 4% of total revenue, as it attempts to gain market share in this fast-growing market. As you can see, e-commerce grocery sales could account for 25% of the industry by 2025, up from 3% today.

Source: Kraft Heinz Investor Presentation

Overall, the company's goal is to pivot its well-known brands and launch new ones that are "on trend" with global consumers' desires for healthier, less processed, and more convenient packaged foods.

Prior to its guidance reduction and dividend cut in early 2019, Kraft Heinz wanted to plug these products into Heinz's large international supply chain and become the No. 1 or No. 2 snack/packaged food brand in 80% of the markets in which it operates by 2023.

For context, Kraft Heinz had the No. 1 or No. 2 market share position in just 10% of its operating countries in 2016, so the company clearly has its work cut out for it. With management needing to address core challenges with many of the company's brands, this ambitious 2023 target seems likely to be pushed back or modified.

A big challenge is that about 30% of Kraft Heinz's sales come from increasingly commodified segments like meats and packaged cheeses, where consumers are increasingly focusing on price and not brand. In fact, management says that these commoditized business lines were largely responsible for the $15.4 billion write-down on its Kraft and Oscar Meyer brands.

And the same online channels Kraft Heinz hopes can revitalize its brands is also making it easier for smaller competitors to sell directly to consumers, including through online-platforms like Amazon (AMZN).

Over the long term, it's hard to imagine Kraft Heinz's revenue growing at more than a low single-digit pace, driven by moderate global population growth, inflationary price increases, and efforts to expand its brand portfolio across channels, food categories, and geographic regions.

However, when combined with ongoing cost savings and share repurchases, Kraft Heinz's earnings per share and free cash flow (as well as its much smaller dividend) have potential to grow at a slightly faster rate, although likely still at a low single-digit pace.

For at least the next year, the company's profits are forecast to decline. Kraft Heinz expects its earnings per share to return to growth from 2020 onwards, but investors are understandably skeptical. The company has encountered several challenges that could continue jeopardizing even those modest growth expectations.

Key Risks

Kraft Heinz faces numerous threats to management's efforts to profitably expand the business.

First and foremost is the fact that the vast majority of its sales are derived from mature markets, where sluggish population growth means that the size of the food market in these regions doesn't change by much each year. Instead, the dollars spent by consumers largely shift between rivals and ultimately gravitate towards the companies offering the most in-demand products.

Unfortunately, Kraft Heinz has been on the losing end in recent years. In fact, about 80% of the company's sales are from North America, where its organic growth has fallen for three years now (about 2% annual volume declines).

In the fourth quarter of 2018 the company saw 4% volume growth, but this was mostly driven by lowering its prices which gained it market share at the expense of profitability.

Source: Simply Safe Dividends

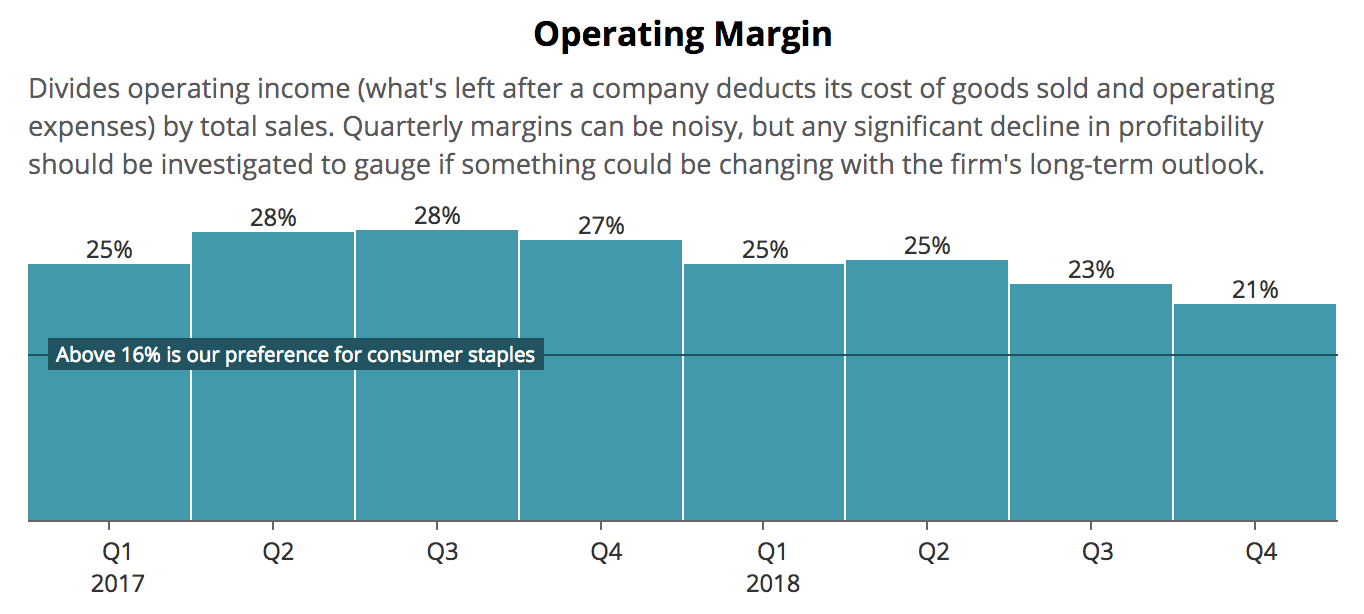

In all of 2018 Kraft Heinz continued to struggle with very weak volumes and profit-sapping cost inflation. While its e-commerce sales increased 79% and the company reported 2% organic sales growth in the second half of 2018, Kraft Heinz's full-year operating margin tumbled from 28% to 23%.

Simply put, Kraft Heinz's brands are losing their pricing power with consumers and retailers. The key problem for the company appears to be 3G's extreme focus on cost-cutting activities, which worked well for its previous M&A activity.

In packaged foods, however, it's proven to be very important to spend sufficiently on marketing and new product R&D to maintain brand awareness and keep relevant products on the shelves as consumer tastes evolve.

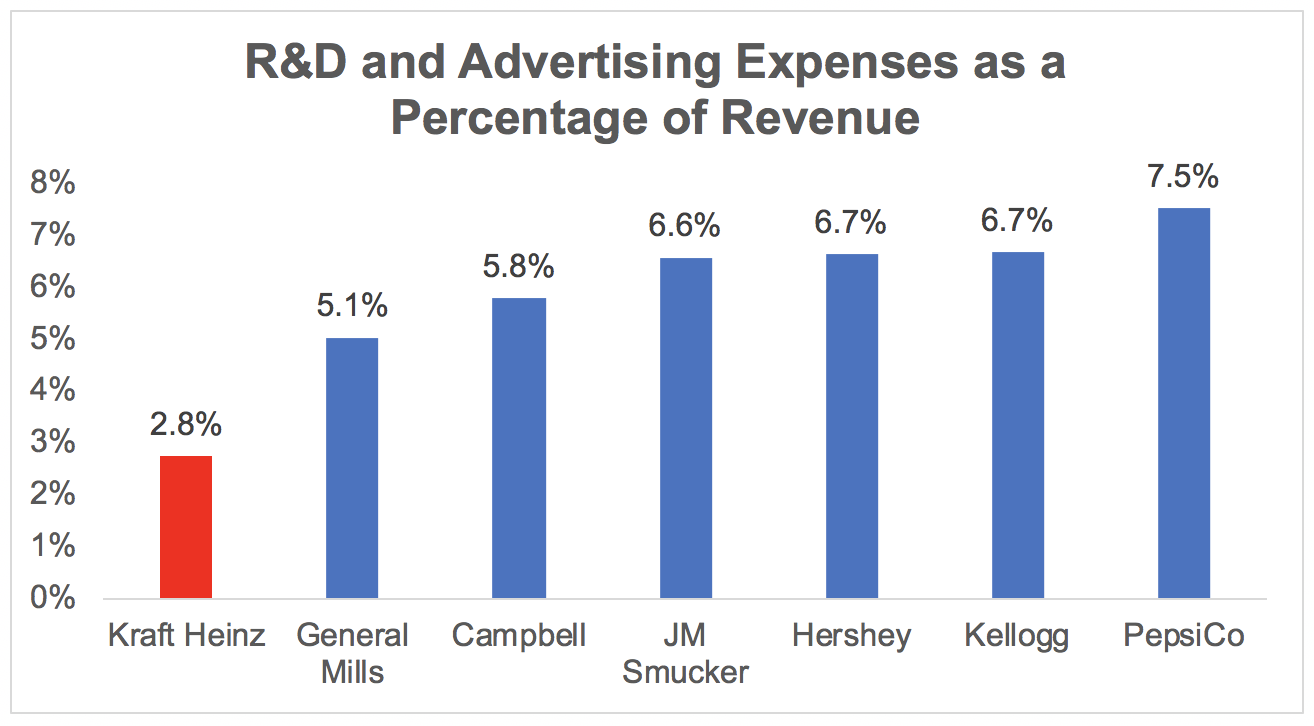

Kraft Heinz's expenditures on R&D and advertising accounted for just 2.8% of revenue in its last reported fiscal year, well below the spending of its major rivals.

Source: Simply Safe Dividends, Company Annual Reports

3G's short-term focus on reducing expenses appears to have come at the cost of weaker brand power. While Kraft Heinz has had to cut prices in a battle to maintain shelf space and relevancy with consumers, its competitors have begun to find success by investing more in their businesses.

General Mills (GIS), for example, was able to recently raise prices thanks to new product launches (due to greater R&D investment) and much higher marketing spending, according to The Wall Street Journal.

It's fair for investors to question whether or not Kraft Heinz's product portfolio is beyond repair given the secular trends working against it in the packaged food industry.

Many of the company's largest brands have thus far been more susceptible to private label competition, and the business does not appear to have much in the way of healthy and organic offerings.

Warren Buffett, who helped put together the Kraft-Heinz merger, summarized the challenge well during a February 2019 interview with CNBC. He said he "was wrong in a couple of ways about Kraft Heinz" and ultimately overpaid for the business as its pricing power deteriorated unexpectedly:

"When you're going toe to toe with a Walmart or a Costco or maybe an Amazon pretty soon...you've got the weaker bargaining hand than you did 10 years ago...

Costco introduced the Kirkland brand in 1992, 27 years ago, and that brand did $39 billion last year whereas all the Kraft and Heinz brands did $27, $26 or $27 billion.

So here they are, a hundred years plus, tons of advertising, built into people’s habits and everything else, and now Kirkland, a private label brand, comes along and with only 750 or so outlets does 50% more business than all the Kraft-Heinz brands.

So house brands, private label, is getting stronger. It varies by country around the world, but it’s bigger. And it’s gonna keep getting bigger."

– Warren Buffett

Kraft Heinz's CEO expects the consumer packed food industry to face similar challenges for years to come:

"Our industry has been and is likely to remain challenged on several front, continued fragmentation of consumer demand, a general lack of affordability to reinvest in brands, retail competition where assortment is likely to grow in importance and, finally, in the short term, ongoing cost inflation."

Essentially, consumer packaged foods is a struggling and brutally competitive industry that is being disrupted globally by shifting consumer tastes, away from boxed and canned goods found in the center of the store and towards healthier offerings.

Thanks to these headwinds, Kraft Heinz battles not only weak sales and eroding profitability (management is guiding for a 10% decline in 2019 EBITDA), but also a strained balance sheet which resulted in management cutting the dividend by 36% in early 2019 to accelerating its deleveraging plan.

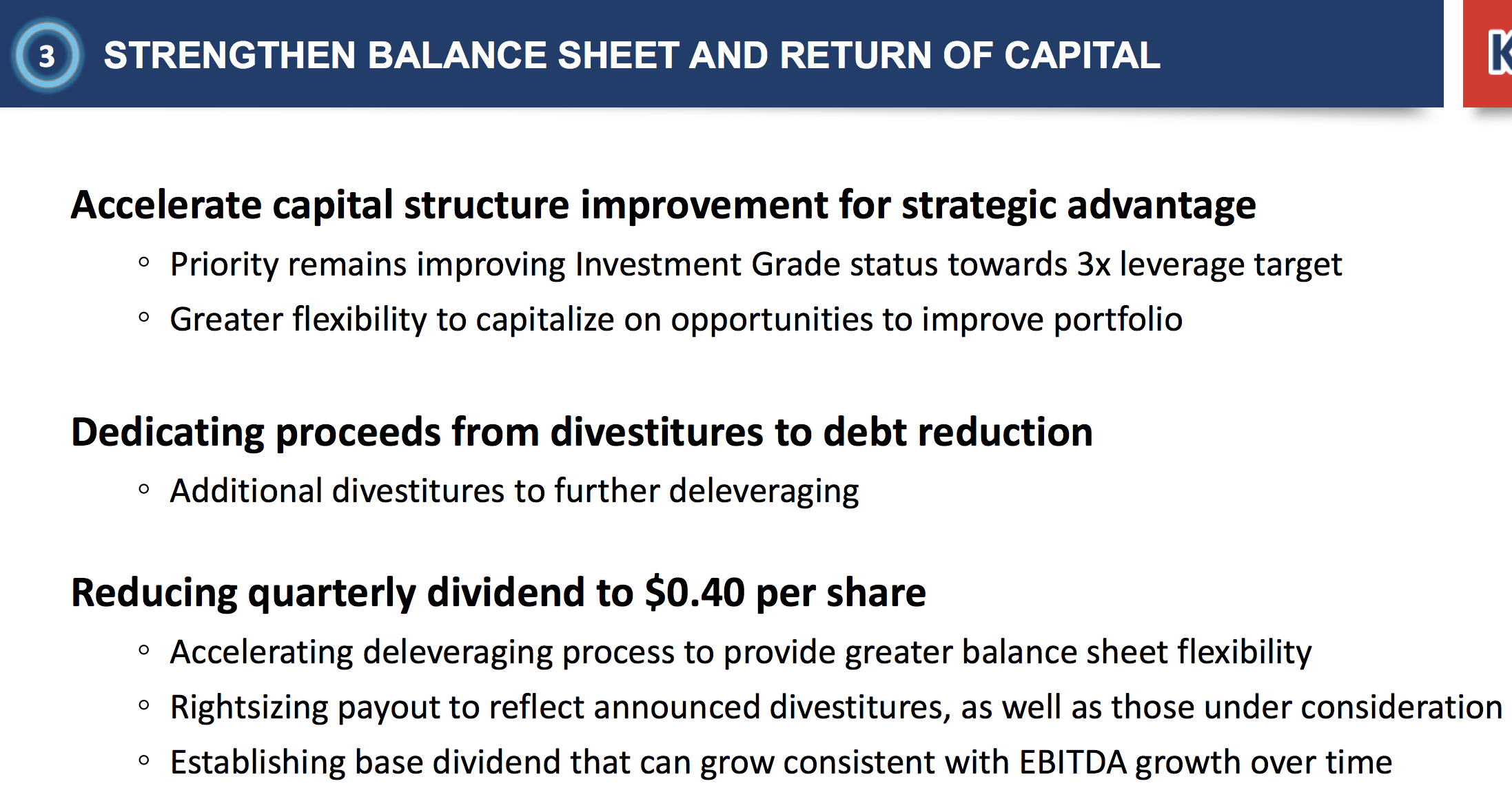

On the company's February 2019 earnings call, management said reducing the dividend, along with executing more divestitures of non-core assets, will allow Kraft Heinz to deleverage faster in order to position it for more industry consolidation (i.e. acquisitions):

“Given the industry backdrop and opportunities in front of us, we now see even greater strategic advantage in accelerating our deleveraging towards our ongoing 3 times leverage target and strengthening the term structure of our debt. To do this, we are undertaking two specific actions. First, we intend to dedicate the divestiture proceeds…to debt reduction.

Second, today we are announcing a reduction in our quarterly dividend…this will not only provide us greater balance sheet flexibility, it will also establish a base dividend we can grow consistent with EBITDA growth over time. And we are comfortable that this level of dividend can accommodate the two divestitures we have already announced, as well as those we are currently considering.

These initiatives will accelerate the strengthening of an already solid balance sheet with a fully funded pension plan and continue to position Kraft Heinz for industry consolidation.”

Consolidation is natural in many slow-growing industries since a larger company can squeeze out more operating efficiencies to expand its profits, all else equal.

However, investors have lost confidence in 3G Capital's reputation as a savvy dealmaker. One analyst on the call even asked management why they would continue seeking consolidation opportunities since it appears that synergies from combining Heinz and Kraft have been largely wiped out given the ongoing slump in EBITDA.

If everything goes well it will likely take many quarters, if not several years, for management to regain investors' confidence. For now, Kraft Heinz needs to stabilize its performance and pay down debt to protect its credit rating.

Moody's downgraded its outlook on the company's debt from Baa2 positive to Baa2 stable (BBB equivalent from S&P). Moody's is concerned about Kraft Heinz's declining operational results but believes the company will remain one of the world's largest food makers and that the $1.1 billion in annual dividend savings each year warrant a low investment grade rating.

Moody's expects the company's leverage ratio to remain above 4.0 for the next 12 to 18 months, but eventually to decline, thanks to increased debt repayments, partially funded by asset sales of weaker brands.

Kraft hopes to eventually bring its leverage ratio down to about 3.0, which is a reasonably safe limit for most corporations.

Source: Kraft Heinz Investor Presentation

Part of that plan calls for asset sales, such as hiring Credit Suisse to look into the possibility of selling Maxwell House coffee, which it believes could sell for about $3 billion, and pay off approximately 10% of its long-term debt.

The company is also considering selling its Breakstone Canadian dairy business, which might be worth $400 million. Kraft Heinz has already sold off India Beverage and Canada Natural Cheese, with proceeds going purely to paying down debt.

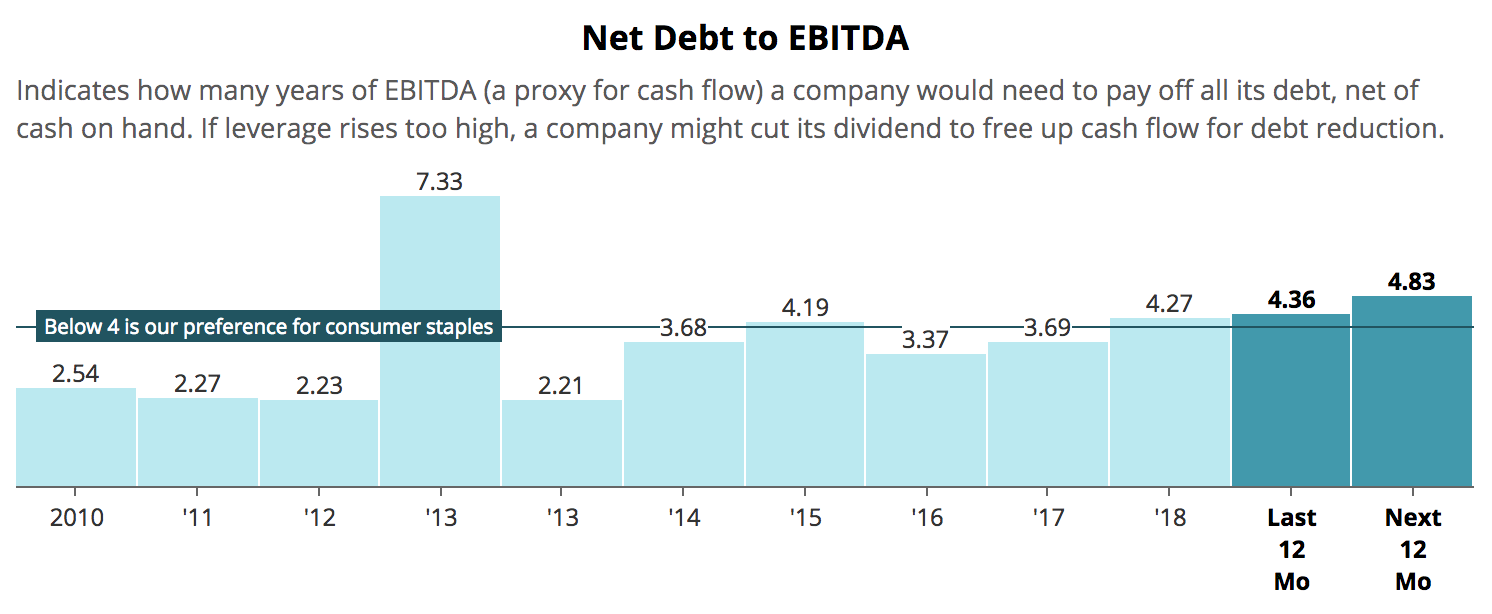

However, in the short term, falling cash flow is expected to increase the firm's net debt / EBITDA ratio to almost five. And paying off debt with asset sales is not always easy. That's because unless the sale price is high enough (seems unlikely for struggling brands Kraft Heinz doesn't want anymore), cash flow can fall roughly in line with the debt reduction, resulting in persistently high leverage.

Source: Simply Safe Dividends

S&P Global has recently placed the company's rating under review for a possible downgrade to BBB-, which would be just one level above junk bond status. Losing an investment-grade credit rating would increase future borrowing costs because many institutional investors are restricted from investing in junk bonds.

Simply put, management does not have a whole lot of time to right the ship. If earnings and cash flow do not return to growth in 2020 as management expects, and asset sales fail to raise enough proceeds to help with deleveraging, then a second dividend cut may not be out of the question.

Finally, it's worth noting that as part of its bombshell earnings release in February 2019, Kraft Heinz revealed an SEC investigation into its procurement accounting procedures. That has resulted in its 10-K (annual report) filing being delayed as the company has to look back and potentially restate several years' worth of financial data.

The company's CFO told analysts on the conference call that the procurement "misstatement was not material to our current or prior year financial statements."

However, until the accounting investigation is concluded and management proves it can live up to its promises to both aggressively deleverage and investing far more heavily (but effectively) in its brands, Kraft Heinz appears to be a dividend stock that is inappropriate for most conservative income investors.

Closing Thoughts on Kraft Heinz

Many of Warren Buffett’s holdings are characterized by strong brands, essential products, and dominant market share positions, so it’s no surprise why he was excited to own Heinz and Kraft.

While Kraft Heinz is likely to remain a force in the food and beverage industry for years to come, it's also facing industry and company-specific headwinds that have come to a head with a large write-down on core brands, a 36% dividend cut, and a plan from management to double down on marketing and brand reinvestment to return the firm to positive earnings growth in the coming years.

However, thus far Kraft Heinz's management, installed by notorious cost cutters at 3G Capital, has proven unable to deliver on its promises, except for slashing spending at the expense of its brands and long-term company health.

Furthermore, the deleveraging effort, which is likely to take several years, could be slowed down by management's desires to continue buying new brands that are "on-trend." But right now such companies carry rich multiples which means that Kraft Heinz's past mistakes with overpriced M&A could be repeated in the future.

Overall, Kraft Heinz appears to remain a riskier dividend stock that conservative investors may want to avoid. At least until management can improve its execution on the firm's turnaround plan, reduce a significant amount of debt, and demonstrate that there is still some meaningful value in Kraft Heinz's portfolio of brands.