Digital Realty Benefits from Secular Growth in Data

Digital Realty Trust (DLR) is one of the largest publicly traded REITs in the country and supports the data center needs of more than 2,300 customers across industries such as financial services, information technology, and manufacturing.

The REIT has a portfolio of 198 data centers in 12 countries and boasts the second highest global market share, behind only Equinix (EQIX) according to analysts at 451 Research.

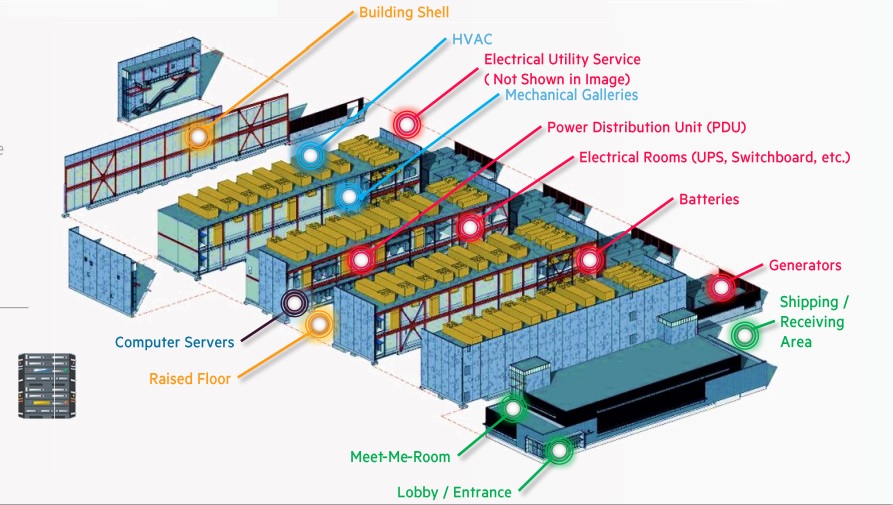

Data centers provide secure, continuously available environments for companies to store and process important electronic information such as transactions and digital communications. Data centers can also serve as hubs for internet communications in major metropolitan areas.

The key components of a data center can be seen below and include servers, network equipment, cooling systems, electrical power systems, and more. Data centers consume a lot of power to keep the servers running and the room’s temperature under control.

Digital Realty’s total rent is comprised of revenue from both turn-key services, in which it provides everything but the servers, and offering a powered base building where customers choose to provide the power components used in the data center (HVAC, battery, generator, electrical, etc.) and design it all themselves.

Geographically, Digital Realty generates about 81% of its rent in North America, 14% in Europe and 6% from Asia. Within those regions, the firm's revenues are highly diversified with its largest market (Northern Virginia) accounting for about 22% of sales, and all other markets (other than Chicago at 12%) representing single-digit revenue concentration. Most of its properties are located in metro areas.

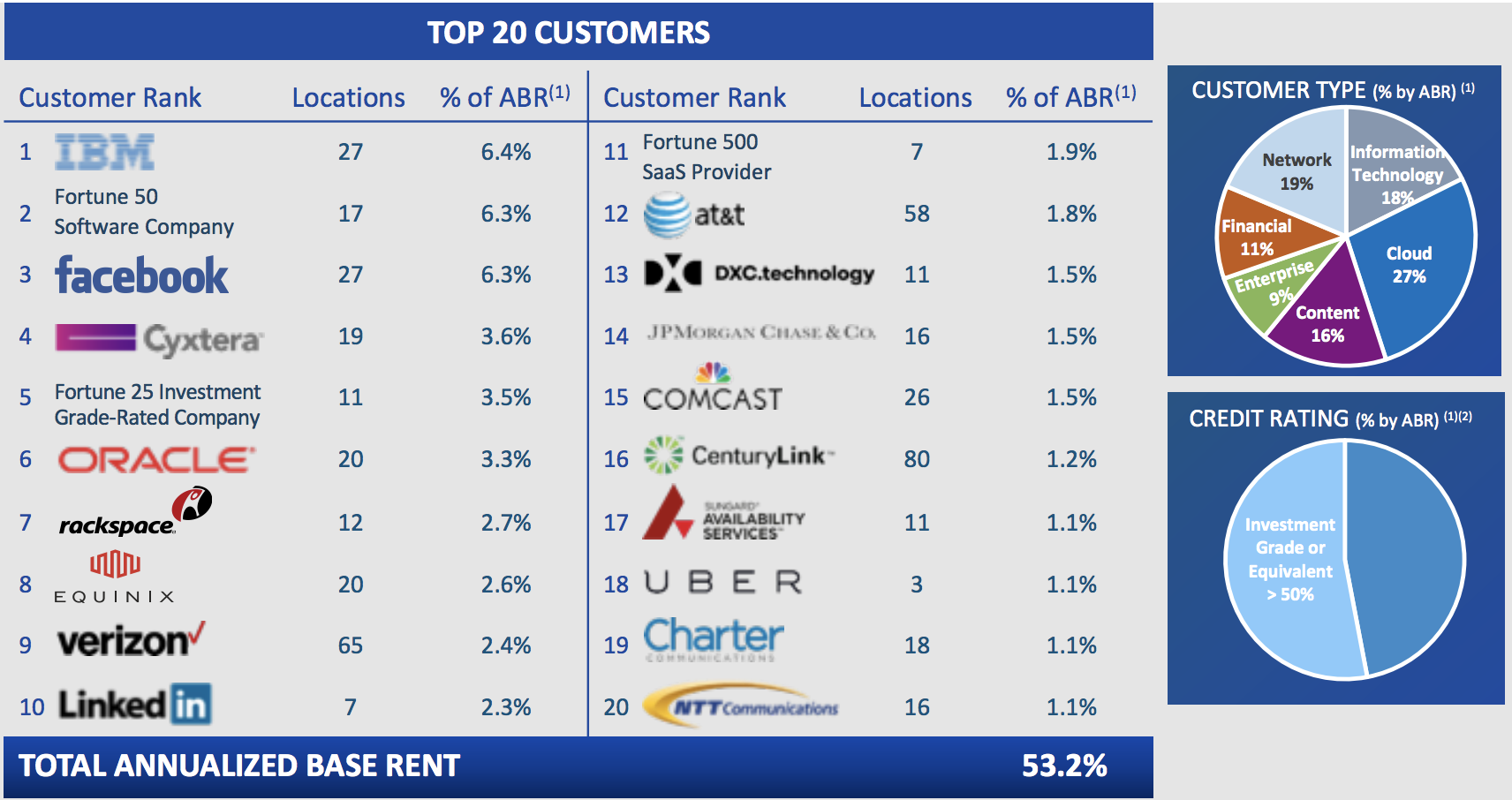

Digital Realty's customer base consists of a diverse assortment of tech companies (cloud providers account for 27% of total rent), as well as communication, financial, and media giants. However, no customer accounts for more than 6.4% of rent, and over half its clients have investment grade or equivalent credit ratings.

Source: Digital Realty Investor Presentation

With 14 consecutive years of higher dividends, Digital Realty has the most impressive payout growth track record of any data center REIT and has compounded its dividend by 12% annually since inception.

Business Analysis

Playing in a growing industry is almost always better than competing in a shrinking market. In Digital Realty’s case, its data center operations are exposed to several long-term secular demand drivers.

For example, cloud computing (using remote rather than local servers to store and process data) is becoming the preferred IT option for more and more companies. According to analyst firm IDC, today about 25% of global IT spending is devoted to the cloud, but that figure is expected to rise to over 50% by 2020.

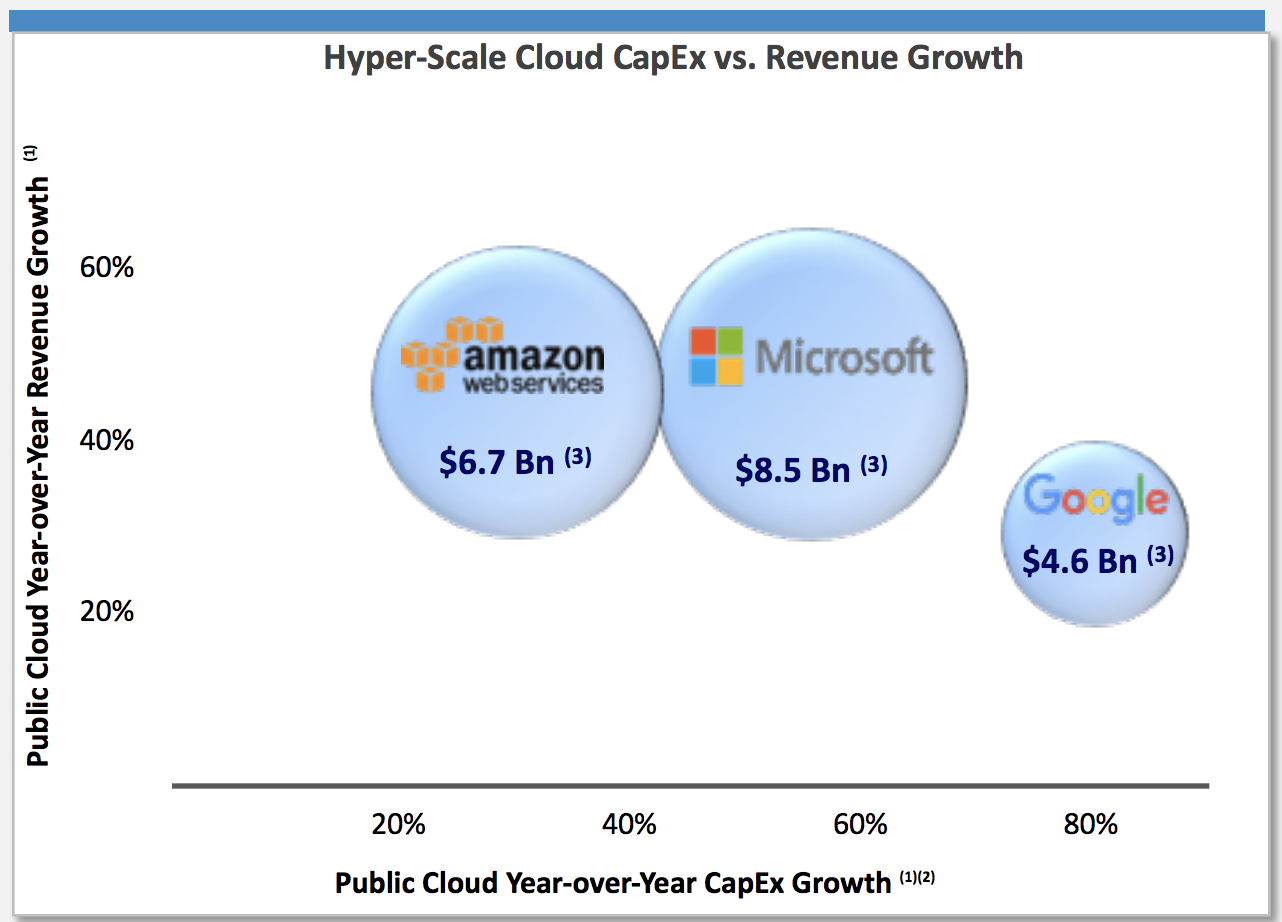

As a result, the industry's three leaders, Amazon (AMZN), Microsoft (MSFT), and Alphabet (GOOG), are putting up impressive 20% to 80% growth in cloud revenue and capital spending.

Source: Digital Realty Investor Presentation

Digital Realty's focus is mostly on hybrid cloud, in which clients use a mix of on-premise data centers and private and public (shared) cloud services. Hybrid cloud is the largest part of the industry followed by public cloud (like what Amazon, Microsoft, and Google offer), which is open to all companies to sign up.

Hybrid cloud is so popular because it allows small to medium-sized companies to maintain more control over their IT but still integrate their systems with those run by other companies to gain operational efficiencies and use various data analytics applications.

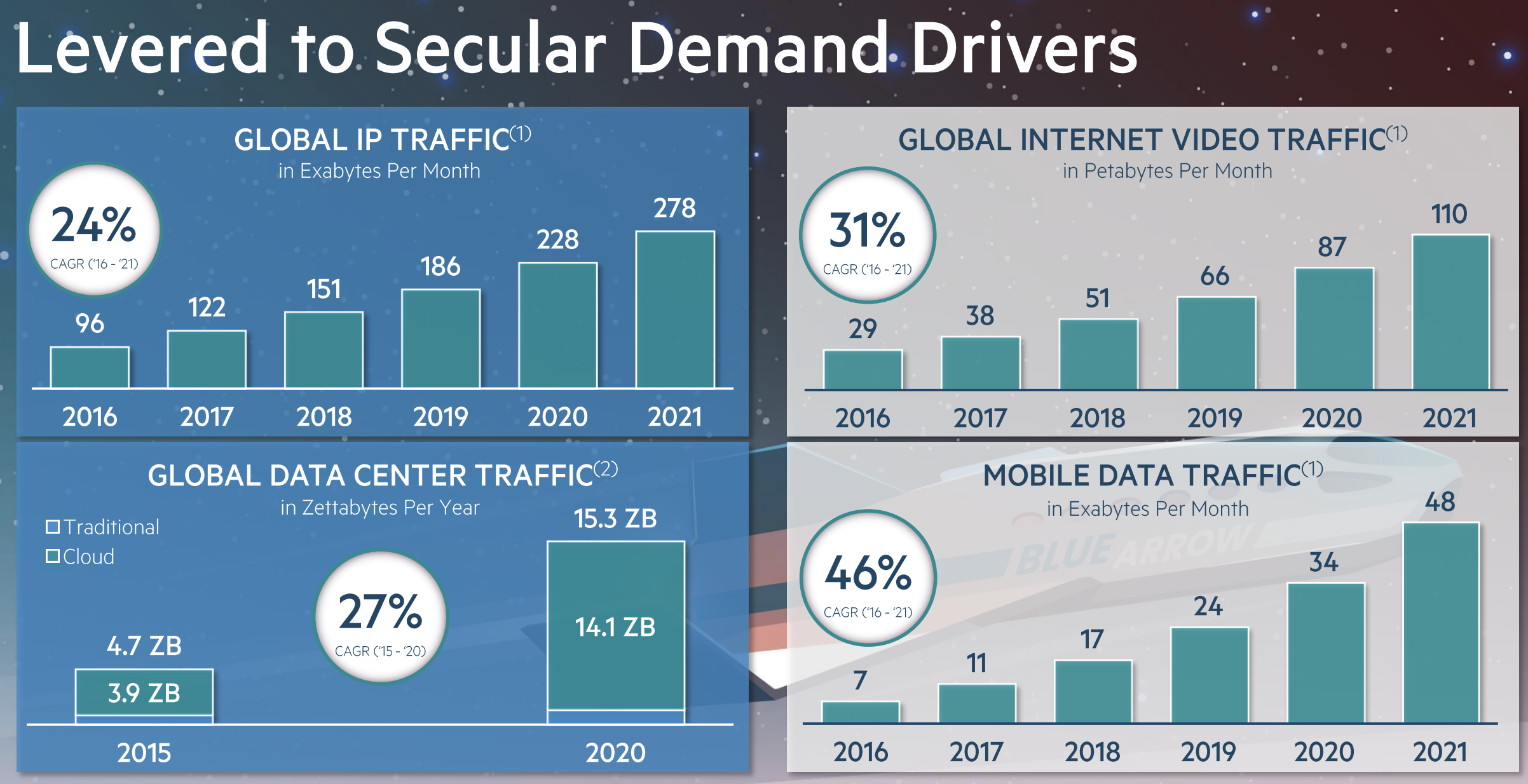

The explosion of both internet-connected devices (including smartphones) and the rise of corporate cloud computing are driving massive data growth across various industries.

Source: Digital Realty Investor Presentation

Artificial intelligence is expected to be one of the fastest-growing industries in the coming years, and when combined with the rise of the internet of things (IoT) and driverless vehicles, should result in an explosion of data that will require more data center capacity.

Source: Digital Realty Investor Presentation

According to Hoya Capital Real Estate, this large secular trend of more connected devices and higher cloud spending is expected to drive over 25% annual cloud spending growth between 2015 and 2025. Simply put, Digital Realty is a leading player in one of the fastest-growing REIT industries.

Data center REITs are also attractive businesses because their services are non-discretionary expenses for companies – the data being stored and processed in data centers is needed to run their operations. As a result, Digital Realty enjoys high utilization rates in most economic environments.

In fact, Digital Realty’s total portfolio occupancy has remained close to 90% or higher in each of the last eight years (currently 90%), including 95% in 2009 during the last recession. The company also notes that its tenant retention ratio has been strong at more than 70% of net rentable square footage.

Occupancy and retention rates are also high because it is costly for customers to switch data center facilities. Digital Realty estimates that it costs customers anywhere from $10 million to $20 million to migrate to a new facility.

Additionally, a new data center deployment typically costs customers $15 million to $30 million, further reducing the incentive to switch landlords. Most of the company’s leases also contain 2% to 4% annual rental rate increases. As long as customers stay financially healthy enough to pay their rent obligations, Digital Realty has very solid cash flow visibility.

What's more, customers provide the actual storage hardware (such as servers and networking equipment) themselves, with Digital Realty merely supplying the physical space, electricity, and interconnectivity assets. This means high profitability including an adjusted EBITDA margin near 60% that management is guiding for in 2019 (in line with its historical level).

The company is also uniquely positioned to meet the needs of major businesses because of its scale, reputation, and favorable real estate locations in major metropolitan areas. Having customers such as IBM, Facebook, LinkedIn, Verizon, and Oracle speaks to the quality of Digital Realty’s properties.

Acquisitions have played an important role in evolving Digital Realty’s business mix to better serve its customers. For example, the company acquired Telx Holdings for about $1.9 billion in October 2015. Telx is a leading national provider of data center colocation solutions and doubled Digital Realty’s high-margin colocation business, which allows companies to rent partial spaces within a data center.

Telx also introduced Digital Realty to over 1,000 new companies it can target for its existing data centers. This is important because over 80% of the company’s traditional large footprint leasing activity in recent years has been repeat business with existing customers.

Digital Realty's acquisitions over the years haven't been just to increase its revenue and scale, but also to evolving its business model.

For example, according to Morningstar, before the 2015 Telx acquisition 95% of Digital Realty's revenue was from wholesale data storage (a highly commoditized service) in which the REIT housed the cloud needs of just one big company. That figure has now fallen to 75% as Digital Realty has focused on colocation (smaller data cabinets serving smaller customers) and interconnections.

Interconnectivity is highly valued by clients because it allows various companies located within the same data center to link together and thus share data, as well communicate across various cloud service platforms (it also helps with cybersecurity, which is a growing issue for all tech companies these days).

Being cloud platform neutral is a key strategy for Digital Realty as well. No matter which cloud company ultimately ends up being dominant, Digital Realty wants to ensure it has access to as large of a total market as possible.

The company's most notable acquisition took place in June 2017 when Digital Realty announced a $7.6 billion merger with DuPont Fabros. Combining the two businesses was primarily done to strengthen the firm's presence in strategic U.S. data center metros.

Not only are the two companies’ portfolios highly complementary, but the combination also enhanced Digital Realty's overall balance sheet strength and created the second-largest data center REIT after Equinix. In fact, the combined company has the most efficient cost structure and the highest EBITDA margin of any publicly-traded data center REIT in the U.S.

Simply put, the merger with DuPont Fabros enables Digital Realty to grow in size and generate economies of scale, helping the company better retain customers in the age of data center commoditization and increasing competition. DuPont Fabros will especially enhance Digital Realty’s cloud portfolio in Virginia, Chicago, and Silicon Valley, three important growth markets.

Management's dealmaking has also helped Digital Realty expand overseas. In December 2018 the company announced it was buying a 51% stake in Brazilian data center provider Ascenty for $1.8 billion. Ascenty is the largest player in Brazil and, in addition to a handful of data centers, owns valuable fiber optic lines which will serve the future data growth needs of Latin America's largest economy.

Despite its numerous acquisitions, Digital Realty has done a good job of maintaining a strong BBB investment grade credit rating. As a result, the firm has solid financial flexibility and enjoys relatively low borrowing costs as it continues investing for growth and rewarding shareholders with growing dividends.

Overall, Digital Realty operates in an industry with favorable secular growth trends and gains benefits from its scale, cost-efficient real estate locations, non-discretionary services, and strong customer relationships.

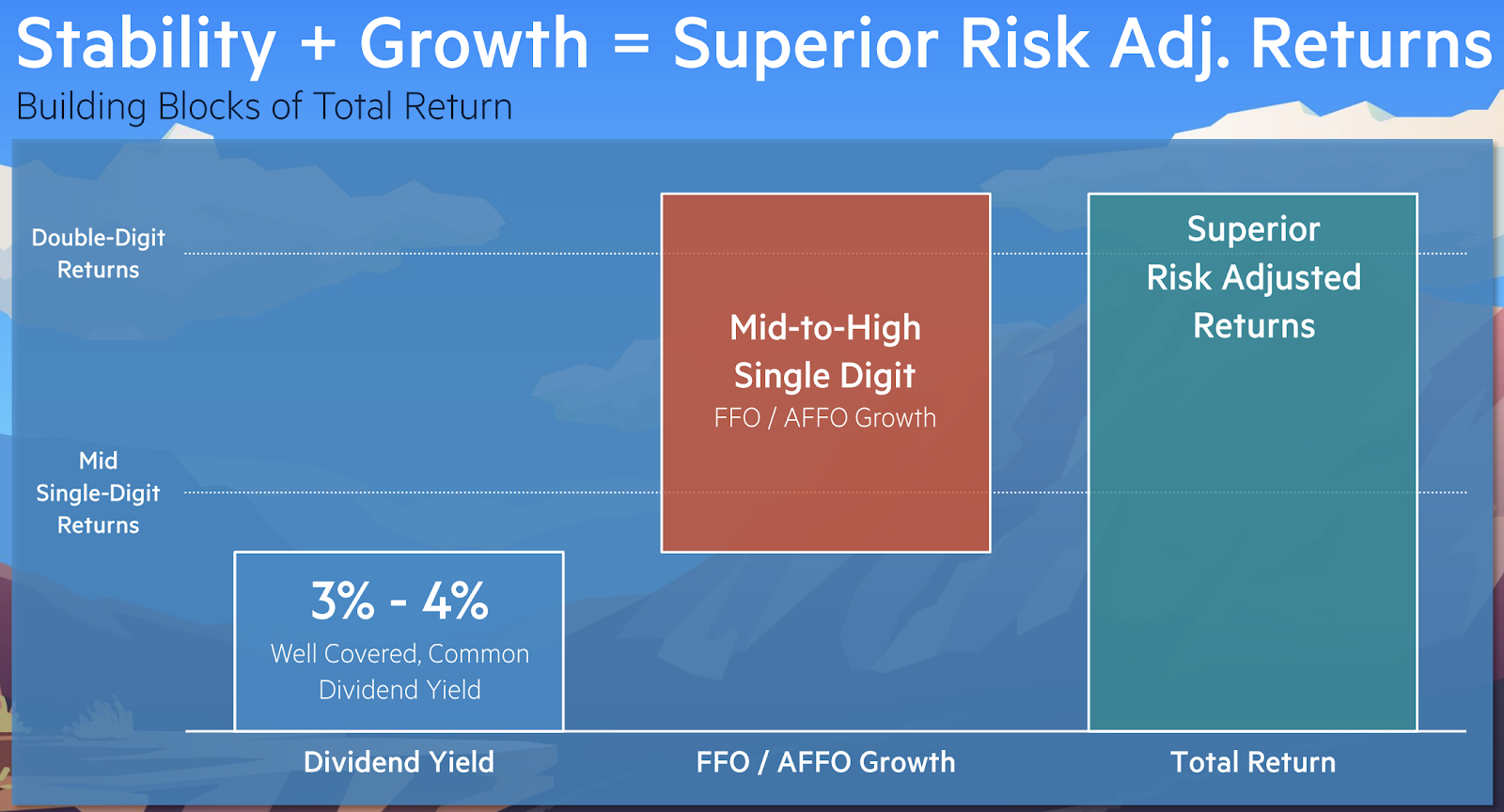

As a result, the company's dividend is on very solid ground, and management expects Digital Realty to deliver mid-to-high single-digit cash flow growth going forward to help drive double-digit total shareholder returns in the long term.

Source: DIgital Realty Investor Presentation

But while Digital Realty is a leader in a fast-growing industry, the company still faces several important risk factors.

Key Risks

Highly conservative investors are often best off avoiding most technology companies because industry trends can unexpectedly and quickly take a turn for the worse. In Digital Realty’s case, the biggest risk is arguably that data centers become overbuilt in anticipation of strong data usage trends.

After all, Digital Realty cannot control the capital allocation of its competitors. As is the case with most secular mega-trends, the rapid growth in data center demand has attracted a lot of interest not just from other data center REITs (Digital Realty is one of five major U.S.-traded data center REITs), but also private equity and tech giants themselves.

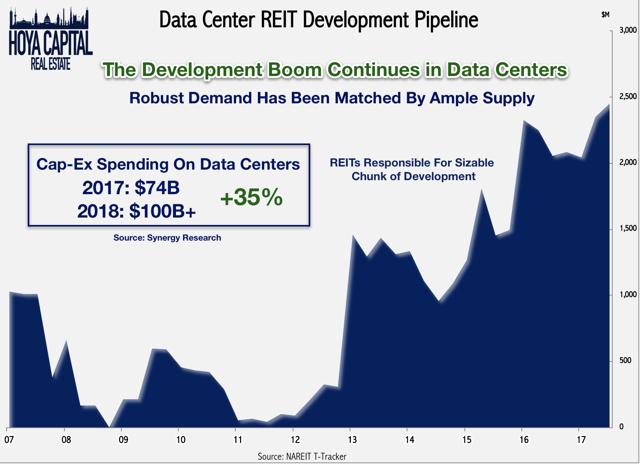

As you can see below, data center REIT construction has boomed over the past few years and is now at record levels. As long as cheap financing is widely available and industry margins are high, more supply will enter the market. If an excess supply of data centers occurs, Digital Realty could experience unfavorable lease renewal rates, weaker profitability, pricing pressure, and lower growth.

Source: Hoya Capital Real Estate

In fact, management's 2019 guidance suggests some of these overcapacity and growth risks are now becoming reality:

Lease renewal rates down high single-digits (vs about -2% in 2018)

Average cash yield on invested capital 9% to 12% (vs 10% to 12% in 2018)

Total revenue growth: 5% (vs 10%+ in each of the past three years)

Core FFO per share growth: 5.5% (historical average growth rate 12%)

While Digital Realty is expected to still grow its top and bottom line, and occupancy is expected to tick up 0.5%, due to competitive pressures management expects the REIT's growth rate is slow far below its long-term guidance.

Digital Realty is now so large that even with such strong industry tailwinds, its days of double-digit cash flow growth are probably behind it. Going forward, mid- to upper single-digit growth seems more achievable.

Another risk is the nature of the tech industry itself. Data centers derive their rent from capacity utilization, and companies are always eager to increase efficiency and thus lower cost. As technology improves, then the amount of physical cloud storage for the world's growing data needs might prove lower than previously anticipated.

Remember that in a booming industry such as the cloud, companies have to make long-term forecasts for their capex and capacity needs. This is why the potential danger of overcapacity is so high because tech companies need to estimate not just future data supply but also what storage technology will be available to supply it.

Basically, as technology evolves, it’s possible that companies learn to store and manage data much more efficiently. This could reduce the demand for physical data center space. However, there would have to be major advancements to offset the 20%+ annual growth in data usage across Digital Realty’s major markets.

Beyond risks unique to the data center market, Digital Realty faces risk from the health of capital markets. REITs are required to distribute 90% of their taxable income as a dividend to keep their REIT classification and the favorable tax treatment it comes with.

Since REITs pay out such a high amount of their earnings, they have less capital on hand to grow their businesses. As a result, they typically issue shares and debt.

In 2018, Digital Realty spent $2.3 billion on growth projects, about 50% of which was funded by issuing shares, 30% from internally-generated cash flow, and 20% from new debt. The company's numerous acquisitions have also largely been stock-based deals. For example, the $1.8 billion Ascenty deal involved Digital Realty selling $1.0 billion in new stock.

Those deals were made possible by the REIT's strong share price. However, like in all sectors, various REIT industries go in and out of favor. It's possible that investor sentiment could shift due to industry worries about possible oversupply and the rise of public cloud.

Simply put, some REITs can run into trouble if credit markets tighten up and/or their share prices sink, raising their cost of capital and potentially causing a liquidity squeeze.

Digital Realty fortunately maintains investment-grade credit ratings from the major agencies and has a relatively conservative debt maturity schedule. However, all REIT investors should remain aware of capital market risk given the unique structure of these companies.

Closing Thoughts on Digital Realty

Data center fundamentals continue to look strong, and it’s hard not to like the themes Digital Realty is benefiting from, especially as many other REITs deal with mature markets and low growth rates. The company should have no trouble continuing to raise its dividend going forward, something it has done each year since going public in 2004.

However, due to rising overcapacity issues and increased competitive pressures from cloud giants like Amazon, Microsoft, and Google, investors need to have realistic growth expectations. The days of double-digit cash flow and payout growth rates shareholders have enjoyed are likely gone for good.

With that said, Digital Realty seems likely to continue riding the secular wave of booming data for many years to come, which has potential to power solid dividend growth (relative to most REITs) of about 6% to 8% per year.

As long as Digital Realty can keep its data centers occupied at healthy rental rates, industry supply and demand stay reasonably balanced, and capital markets remain accessible, the company's long-term future still appears to remain bright.