What does Genuine Parts' Potential Spin-Off Mean for this Dividend King?

There is a lot to love about Genuine Parts Company (GPC) for dividend investors:

Sales have increased in 85 years out of its 90-year history

Profits have increased in 74 years out of its 90-year history

The dividend has increased in each of the last 62 years (including 2018)

These types of businesses form the backbone of many investors’ dividend portfolios. However, GPC recently signaled that it wants to separate off its Business Products (S.P. Richards) segment.

Spin-offs can be tricky for income investors. For one thing, you wonder if the regular dividend you have been depending on will remain safe or need to be reduced to better match the remaining company's smaller pool of cash flow.

And when shares are received in the new spin-off company, you must also decide whether that is a business you want to keep for the long term. Reviewing what's left of the original business is important to ensure it's still worth owning going forward, too.

To help answer these questions I consulted Joe Maginot, an experienced equity analyst who runs the website Spin-Off Insights. He helps investors discover compelling spin-off investment opportunities by providing in-depth analysis and a variety of organizational tools. His website is worth checking out if you are interested in these types of investments.

Here is his take on Genuine Parts Company's spin-off situation as it pertains to dividend investors...

The Spin-Off Announcement

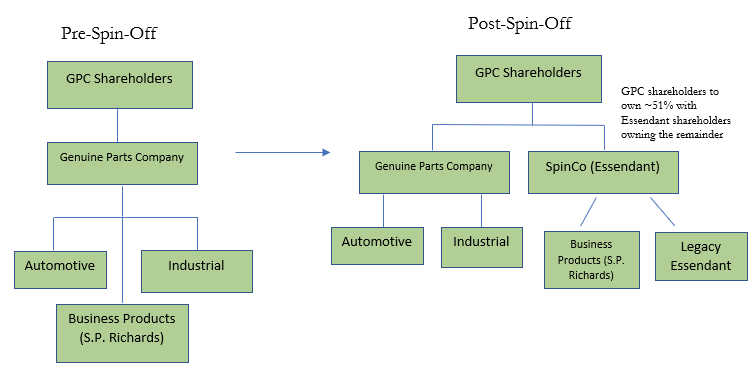

On April 12, 2018, GPC announced its intention to spin-off its S.P. Richards segment and merge it with Essendant (ESND). GPC shareholders will own approximately 51% of the “New” Essendant and legacy Essendant shareholders will own the remainder. Also, GPC will receive a one-time dividend payment of nearly $350 million.

A spin-off transaction is where a new, independent company (the “SpinCo”) is formed through the separation of a segment or subsidiary from the parent company (“RemainCo”). In this case, S.P. Richards is the “SpinCo” and GPC is the “RemainCo”. GPC’s management expects the transaction to close before the end of 2018.

Depending on how the transaction is ultimately structured, GPC shareholders will either receive a distribution of Essendant shares or they can elect to exchange their GPC shares for shares of Essendant. The diagram below illustrates the transaction.

Staples Recent Offer to Buy Essendant

The GPC spin-off of S.P. Richards and subsequent merger with Essendant appeared to be on track. However, on September 10, 2018, Essendant announced they received an offer to be bought by Staples for $12.80 per share in cash.

Essendant believes this is superior to GPC’s offer and would end its merger agreement with S.P. Richards unless GPC improves its offer.

Regardless if the deal with Essendant happens or not, it is very clear that GPC is determined to separate off the S.P. Richards business which has several important implications for shareholders to understand.

Is Genuine Parts' Dividend Safe without S.P. Richards?

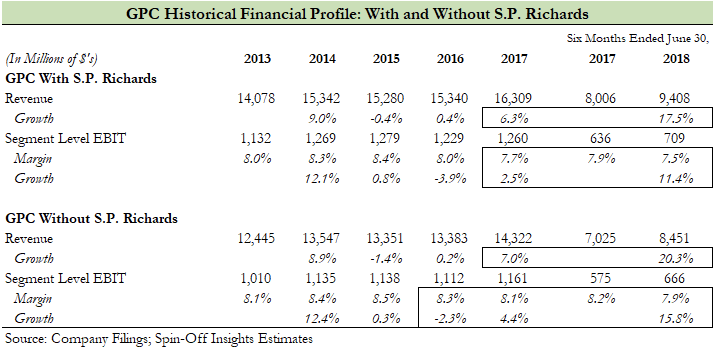

In short, yes. In 2017 S.P. Richards made up approximately 12% of GPC’s total revenue and 8% of its total profits. Currently, GPC has a reasonable dividend payout ratio of about 50%.

That figure will only increase to the mid-50% range without S.P. Richards. As a result, GPC should continue to generate plenty of cash flow to cover the current dividend while leaving room for investing in the business.

In fact, this could be a long-term positive for GPC investors.

S.P. Richards has been struggling over the last couple years and even more so in 2018. As you can see in the table below, GPC’s overall performance would’ve been improved in 2017 and 2018 if S.P. Richards was not part of GPC.

Through the first six months of 2018, total GPC revenue has grown about 17.5% and segment level operating income has grown about 11.4%. If S.P. Richards was not part of GPC, then revenue growth would’ve been over 20% and operating profit growth would’ve been nearly 16%.

Therefore, from a dividend investor’s perspective, GPC will arguably be in a similar if not better financial position after the separation of S.P. Richards than before it.

What is Essendant?

If the spin-off and merger ends up going through, the “New” Essendant will be comprised of the legacy Essendant business combined with S.P. Richards.

S.P. Richards is GPC’s lowest quality business. The company is the second largest distributor of facilities, breakroom and safety supplies, general business products, and business technology products and office furniture. The business generated roughly $2 billion in revenue during 2017.

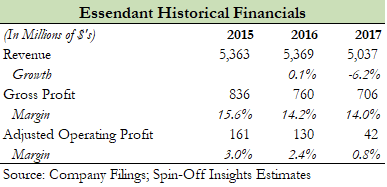

Essendant is a competitor to S.P. Richards and is a wholesale distributor of janitorial, foodservice and breakroom supplies, office products, technology products, automotive and industrial products, and office furniture. The business generated roughly $5 billion in revenue during 2017.

If the spin-off and merger goes through, as you can see in the table below, the “New” Essendant will generate roughly $7 billion in revenue and $225 million in EBITDA. This is prior to an expected $75 million in synergies from the merger.

This is a very difficult business that operates with razor-thin margins and requires significant working capital.

Also, the traditional distribution model for office products is being challenged by competition from Amazon and other online retailers, mass merchants, and specialty distributors.

As you can see in the table below, Essendant has been struggling as both revenue and margins have been falling. The company is responding to this difficult business environment through cutting costs and restructuring the business.

Needless to say, this merger is driven by the difficult environment and an attempt to get bigger and leverage shared services in order to lower the company's overall cost structure.

Will the “New” Essendant Pay a Dividend?

Essendant has paid a quarterly dividend to shareholders since the end of 2011 and management expects that to continue. However, the quarterly dividend hasn’t grown at all since they increased it at the end of 2012 to 14 cents per share.

While the current dividend yield of nearly 4% could appear interesting to some investors, the dividend looks like it could be at risk of a cut if the potential S.P. Richards merger does not go well.

As mentioned in the section above, the competitive environment continues to rapidly evolve and these businesses are struggling to adjust.

If revenues continue to fall, then it will be difficult for the business to maintain profitability levels, pay-back debt, invest in restructuring the business, and have enough left over to maintain the dividend.

Also, Essendant has significant debt on the balance sheet. Pro forma for the potential merger, the firm's net leverage ratio will be around 3.8x. This level of debt is well above comfort levels for most conservative dividend investors.

Closing Thoughts on Genuine Parts' Spin-off

Genuine Parts Company has been a good long-term holding for dividend investors. Management’s determination to separate off the S.P. Richards segment will ultimately free the company of its lowest quality business and allow it to focus on growing its higher quality Automotive and Industrial divisions.

Simply put, the remaining GPC will have a higher growth rate, a superior margin profile, and better prospects for growing the dividend going forward.

On the other hand, Essendant appears to be a risky investment for legacy GPC investors if the spin-off and merger still end up going through despite Staple’s interest in Essendant. The company is facing intense competition, undergoing restructuring, and has significant debt on the balance sheet.

As a result, the spin-off's dividend could be in jeopardy if the merger goes poorly and does not generate management's expected synergies.

If you’re interested in learning more about spin-offs, a good place to start is with Spin-Off Insights' guide here.