Philip Morris International Faces Growth Headwinds: Is the Dividend Still Safe?

Since being spun off from Altria (MO) in 2008 Philip Morris International (PM) has raised its dividend every year and delivered predictable returns thanks to the steady nature of the tobacco business.

However, this year Philip Morris shares are down nearly 25% on growing concerns over whether its strategy for adapting to the continued global decline in smoking can succeed.

Let's take a closer look at why the market is so bearish on this tobacco giant and whether or not Philip Morris investors need to worry about the safety and long-term growth prospects of its generous dividend.

Philip Morris is Betting Big on Reduced-Risk Products But Has Hit Some Growth Challenges

About 93% of Philip Morris' revenue still comes from combustibles, including its cigarettes which are sold globally under the Marlboro, Chesterfield, Parliament, and Virginia Slims brands.

However, globally cigarette volumes have been declining about 2% to 3% per year, a trend that is expected to continue for the foreseeable future. While Philip Morris' strong brand power usually allows it to raise prices by 4% to 5% per year, more than offsetting volume declines, the company has publicly stated that it plans to transition to a future of reduced-risk products (RRPs).

RRPs include smoking alternatives such vaping systems and "heat-not-burn" products such as Philip Morris' IQOS heat stick featured below. Heat sticks merely heat tobacco to create a nicotine-rich vapor without the toxic chemical-laced smoke that results from a burning cigarette.

Philip Morris began test marketing IQOS in Japan and Italy in 2014 but adoption was so strong that by 2016 it had rolled out the product nationwide in Japan. And between 2015 and 2017 the firm began marketing IQOS in other countries as well (now in 38 countries).

Source: Philip Morris International

The company saw major adoption of IQOS in Japan, which gave management confidence that such RRPs could eventually allow it to get to a point where it doesn't sell traditional cigarettes at all. That's because unlike vaping, heat sticks are very similar to the traditional smoking experience. And since Philip Morris has mostly been marketing IQOS under the well-known Marlboro brand, it has managed to retain a lot of customer loyalty in Japan.

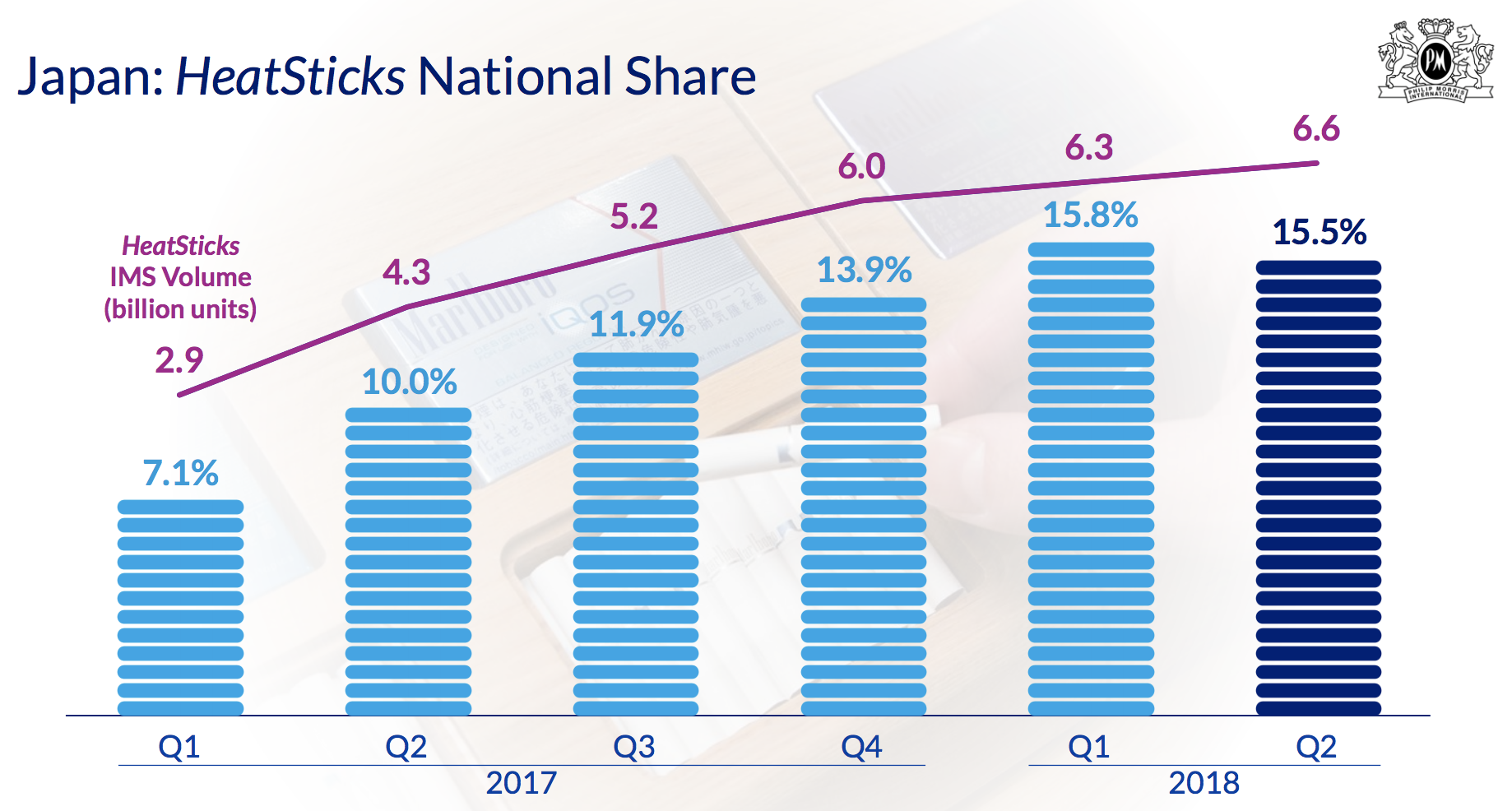

As a result, in 2017, despite Japan cigarette volumes dropping 4%, strength in IQOS allowed Philip Morris to increase shipments into the country by 47%, thanks to a 300% increase in IQOS volumes which offset a 28% decline in combustible products.

At the end of 2017 Philip Morris's IQOS made up 63% of the company's total Japanese product volumes and commanded nearly 14% of Japan's total tobacco market share.

Source: Philip Morris International

Among heated tobacco products in Japan, Philip Morris commands about 80% market share, thanks to getting a huge early lead in launching and marketing the product.

However, how there's growing concern that the company's dominance in heat sticks, both in Japan and globally, may be under threat.

That's because in Japan two major rivals are challenging Philip Morris in heated tobacco products. British American Tobacco (BTI) has begun rolling out its iFuse Glo heatsticks in several major test cities.

By the end of 2017 British American reported low single-digit market share in Tokyo and Osaka, but 11% market share in Sendai. At the end of the first quarter of 2018 British American reported about 4.3% overall market share, a meaningful increase from zero only a few quarters ago.

Meanwhile, Japan Tobacco has announced plans to invest nearly $1 billion into launching its Ploom Tech smokeless tobacco system in 2018. As part of their effort to gain market share these major rivals have slashed prices on their heat stick products, 50% in the case of British American's Glo (for 2018) and 25% for Japan Tobacco. Philip Morris has responded with a 30% reduction in IQOS prices which will significantly impact its margins on that product.

But there's still more bad news for Philip Morris when it comes to heated tobacco products.

In addition to rising competition and a price war, it's potentially facing a much smaller market than initially believed. According to analyst firm Euromonitor International, Japan accounts for 90% of the world's $5 billion heat stick market. That's mostly because in that country vaping products (the major rival to heat-not-burn products such as IQOS) are regulated under pharmaceutical laws.

As a result, systems like IQOS are effectively the only alternative to traditional smoking. However, now that many early adopters have jumped on board and switched to them, British American is reporting that "the growth of the Tobacco Heating Products category has slowed."

That's because, in the words of Philip Morris' CFO Martin King:

"We're now reaching different socio-economic strata with more conservative adult smokers who may have slightly slower patterns of adoption...Device sales were slower than our ambitious expectations".

While the company has seen 75% uptake rates among early adopters, for more conservative smokers that figure falls to 15% to 30%. This is one reason why some investors are worried that the global heat stick market could already be potentially peaking.

For example, in the first quarter of 2018 global heat stick shipments totaled 9.6 billion units, up 118% from the first quarter 2017. However, that was actually down 39% from the prior quarter's 15.7 billion global volumes.

While in Japan heat sticks are largely the only alternative to cigarettes, vaping products like those offered by JUUL Labs are a major potential rival in other markets where regulatory regimes are less strict.

For example, in the U.S. (the only place JUUL now operates), the company's competing lower risk nicotine delivery system has managed to grab nearly 50% market share in reduced-risk products. According to Nielsen, that's a 22% increase in market share in the U.S. RRP market in 2017, which is why JUUL was able to raise money at a $15 billion valuation.

It's true that JUUL is so far only in the U.S., where Philip Morris doesn't compete with it because it doesn't operate in America. However, the point is that there is a risk that JUUL could significantly expand internationally, entering markets where it would directly compete with IQOS and further limit Philip Morris's non-cigarette growth potential.

The good news for Philip Morris investors is that while the potential market for IQOS may not be as large as once believed, management reports that only 1% of existing users have switched to competing brands.

This shows that Philip Morris' brand power in heat sticks remains similar to that of traditional cigarettes. And thanks to its industry-leading economies of scale, analysts believe that eventually (when the price war is over) Philip Morris will be able to deliver similar operating margins on IQOS as its traditional cigarettes.

Going forward, Philip Morris has announced that it plans to aggressively invest in new IQOS products. That includes building a $2 billion heated IQOS factory in Italy, as well as launching lower priced offerings worldwide by October 2018.

In addition, by the end of the year the company plans to launch the next generation of IQOS worldwide, which it believes will help cement its leading market share in most markets.

The downside of these major investments in IQOS is that management expects it to result in lower growth than previously expected in 2018. For example, constant currency revenue growth is now expected to be just 3% to 4%, down from previous expectations of 8%. The company also cut its EPS growth guidance by 5% to $5.07 per share, down from $5.32 earlier.

But do these IQOS growth risks mean that Philip Morris is no longer a safe high-yield dividend growth stock? Fortunately, income investors still have reasons to remain hopeful.

Philip Morris' Dividend is Likely Safe and Set to Continue Growing Over Time

While IQOS is an important part of Philip Morris' long-term growth strategy, remember that reduced-risk products still only make up about 7% of the company's sales.

In the most recent quarter Philip Morris reported a cigarette volume decline of just 1.5% which was more than made up for by a 73% increase in IQOS volumes. In fact, globally IQOS now commands 70% share of the heated tobacco market.

While the size of that overall market may prove smaller than previously believed, the market is still growing for now. As a result of its solid IQOS sales growth, in the second quarter of 2018 the company was able to report 8.3% growth in constant currency revenue and a 24% increase in adjusted EPS.

Meanwhile, despite higher capital investments to support IQOS, Philip Morris' dividend remains comfortably covered by its free cash flow. Over the past 12 months the company's free cash flow payout ratio was just 80%, which is likely why management felt confident enough to recently increase the dividend by 6.5%. The company also still enjoys a strong balance sheet with an A credit rating that means it can borrow cheaply to invest in its IQOS growth efforts.

Over the long term, CFO Martin King still says that IQOS represents the company's best growth avenue. And despite a more competitive market in Japan, the company still saw overall volume shipments in that core market rise 5% quarter-over-quarter in the second quarter of 2018.

In the coming months Philip Morris thinks its new IQOS products, including both stronger flavored premium models and value-focused offerings, will help continue to drive positive sales and earnings growth. That's especially true in large markets such as Russia, where IQOS adoption has been rapid. In fact, the company's heat sticks sales in Moscow command 4.4% of the city's entire tobacco market.

What about the risk of vaping and the fast growth of JUUL? Not surprisingly, CFO Martin King believes IQOS is well-positioned to compete with vaping systems:

"It has higher conversion rates than e-cigs. The taste is closer, and the delivery of nicotine and the satisfaction of smokers is much closer to cigarettes."

What does all this mean for the company's long-term growth prospects?

For now, Philip Morris seems likely to continue squeezing out low- to mid-single-digit annual revenue gains. After all, the economics of its core cigarettes business appear to remain intact (in the second quarter volumes were down 1.5% but prices were up 8%), and IQOS is still growing, even if at a slower pace and with lower margins than previously expected.

While traditional cigarettes were a capital-light cash cow, Philip Morris has to continue ramping up spending to compete in the reduced-risk products of the future. The long-term returns from these investments are less certain, but the firm appears to have the financial flexibility to fund these expenditures and support its dividend (management expects $7.5 billion of free cash flow in 2018 compared to total dividend payments of about $7 billion).

It's too early to say who the winners and losers will ultimately be in a (distant) world where more consumers are using smokeless alternatives rather than traditional cigarettes. In many ways the battle is just beginning, but Philip Morris seems likely to have a leg up over time thanks to its substantial R&D budget, well-known brands, and massive distribution network.

Closing Thoughts on Philip Morris' Dividend and Recent Struggles

Like all tobacco companies, Philip Morris faces challenges thanks to the secular decline in long-term smoking rates and cigarette volumes. However, the firm still enjoys a wide moat thanks to its substantial economies of scale and leading brands which continue to command strong pricing power.

This helps Philip Morris minimize its operating costs and keep growing its earnings and cash flow over time. Meanwhile, while long-term IQOS market expectations may have fallen, the company remains the global leader in this still-growing industry.

With the dividend safely covered by the company's recession-resistant free cash flow and supported by a strong balance sheet, Philip Morris International appears to remain a reliable source of income. The stock's recent selloff has also pushed PM's forward P/E multiple down from nearly 25 in mid-2017 to a much more sensible level of 15.2, reducing valuation risk going forward.

With that said, income investors need to realize that Philip Morris' market conditions are gradually changing, and new technologies, distribution channels, and competitors could impede on its long-term outlook for profitable growth.

The stock remains a reasonable holding in retirement portfolios, but remaining diversified to reduce company-specific risk is especially important in situations like these.