Philip Morris: High Dividends and a Leading Position in Smoke-Free Alternatives

Philip Morris International (PM) was spun off from Altria (MO) in 2008, with Altria serving the U.S. and Philip Morris owning the international rights to all of Altria’s most famous brands, including the industry's best-selling brand, Marlboro.

Philip Morris sells its cigarette brands, which mostly target the higher end of the market, to more than 150 million customers in over 180 countries and has close to 30% international market share (excluding China and the U.S.).

While traditional tobacco products still generate the vast majority of the company's profits, reduced-risk products, or RRPs, account for about 15% of the firm's sales and are growing rapidly as smokers seek cigarette alternatives.

By 2025 management aspires for RRPs to account for roughly 40% of the firm's revenue. Most RRPs also carry higher margins because unlike cigarettes they currently have low or no excise taxes.

Geographically, the European Union (31% of sales, 36% of income) and Asia (35% of sales, 32% of income) are the company's most important regions, followed by Eastern Europe, Middle East and Africa (24% of sales, 22% of income) and Latin American and Canada (10% of sales, 10% of income).

Since separating from Altria in 2008, Philip Morris has raised its dividend each year.

Business Analysis

The tobacco market has served investors well for decades. Warren Buffett described the business best when he once remarked, “It costs a penny to make. Sell it for a dollar. It’s addictive. And there’s fantastic brand loyalty.”

Philip Morris has certainly benefited from these qualities over time, relying on its popular cigarette brands to establish itself as a leader in the tobacco world.

In fact, at the end of 2018 the company was the market share leader by volume in seven of the 10 largest OECD countries (an organization of 37 international countries) excluding the U.S. and is the second biggest player in another two.

Outside of OECD countries and China, Philip Morris holds onto the No. 1 market share spot in three of the 10 biggest countries by industry volume and is the No. 2 player in another four.

Source: Philip Morris Investor Presentation

The company’s dominance is driven by the strength of its brand portfolio. Philip Morris owns six of the world’s top 15 cigarette brands, including the world’s No. 1 brand – Marlboro.

As a result of its loyal following of consumers, the company enjoys excellent pricing power. Since 2008, Philip Morris’s annual pricing gains have ranged between 5% and 8, excluding excise taxes.

A key factor supporting Philip Morris's pricing power is the firm's focus on premium brands, which account for about half of the company's volume (compared to less than 30% for the industry).

Studies have also shown that premium brand smokers are less likely to quit, helping cushion the company's exposure to a powerful secular decline in global smoking rates.

Philip Morris's cigarette volumes are also buoyed by the firm's geographic diversification and lack of exposure to the dynamic U.S. market. Just over 50% of Philip Morris's net revenues and more than 70% of its total volume is derived in emerging markets, lessening its dependence on regulatory and consumer developments in any single market.

Importantly, Standard & Poor's also believes that developing markets experience steadier cigarette volumes because "smoke-free alternatives are generally more expensive and less available than cigarettes." The populations in these countries are usually younger and faster-growing compared to America's, too.

As a result, Philip Morris's volume has only declined about 2% to 3% annually, a manageable trend management expects to continue more than offsetting with mid-single digit price increases.

However, the company also realizes that the tobacco world is heading towards a smoke-free future in the long term. Philip Morris is working to transition from a company that sells cigarettes to a company that delivers nicotine through various delivery systems.

Since 2008 the firm has invested $6 billion in R&D, with the majority of that spending focused on smoke-free offerings. Today the company markets four reduced-risk products: two that heat tobacco to produce a vapor, and two that produce a nicotine-containing vapor without tobacco (e-cigarettes).

IQOS, a heat-not-burn tobacco product, is the company's biggest hit with more than 12 million global users in over 50 markets worldwide. Impressively, management claims that over 70% of IQOS users have stopped smoking.

Source: Philip Morris International

Thanks to these development efforts, reduced-risk products will account for about 15% of Philip Morris's net revenue in 2019, according to management. That's up from 0.2% in 2015 and about halfway to the company's 2025 goal of deriving 38% to 42% of its net revenue from smoke-free offerings.

Simply put, Philip Morris has proactively adapted its business to help position it for the continued rise of cigarette alternatives. Management is banking on growth in heated tobacco to help offset continued volume declines in cigarettes.

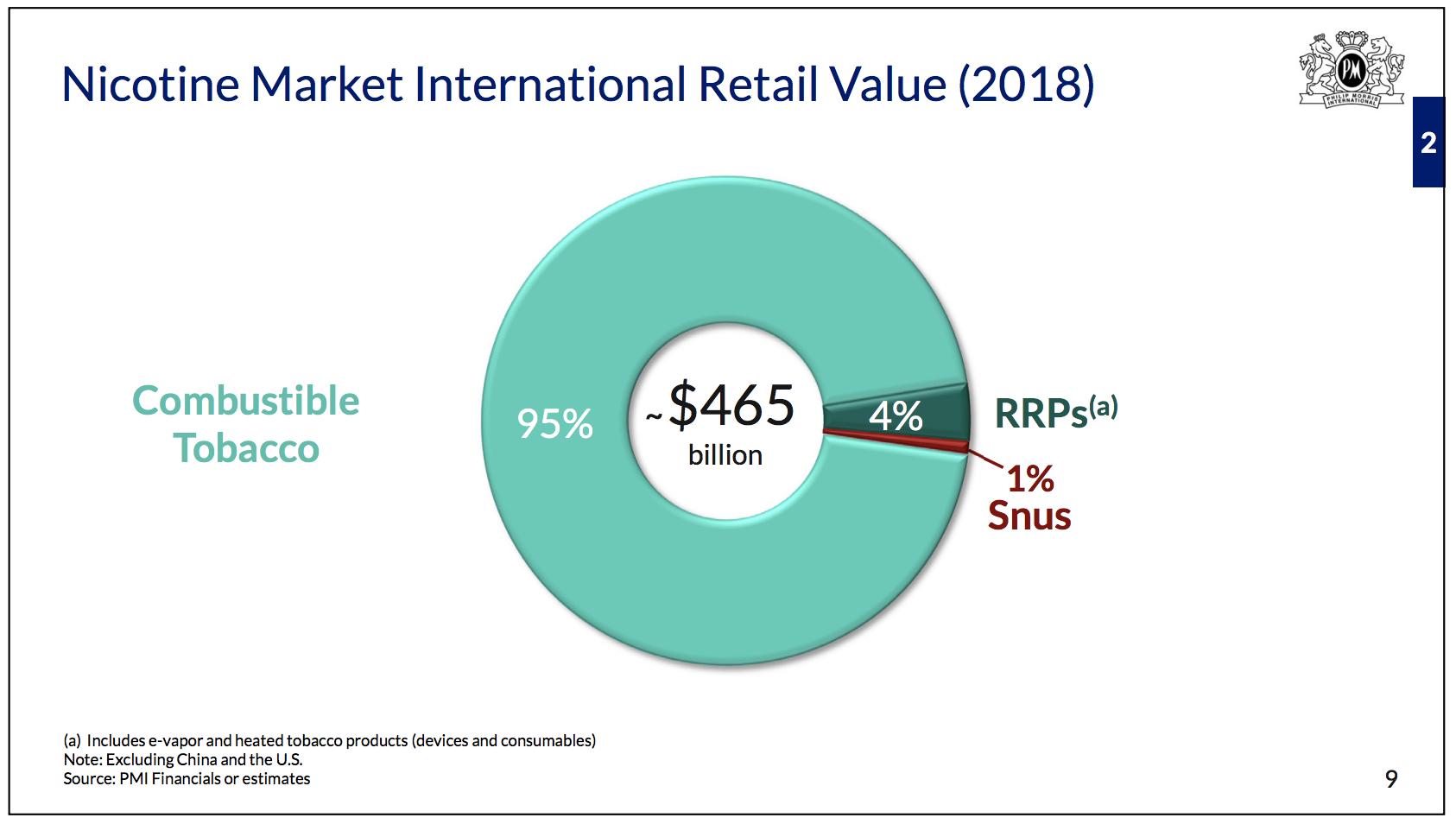

In 2018 reduced-risk products accounted for just 4% of the international nicotine market (excluding China and the U.S.). As more consumers quit combustible cigarettes and switch to presumably lower-risk alternative offerings, this piece of the market will likely grow significantly over the next decade.

Source: Philip Morris International

In fact, the Global State of Tobacco Harm Reduction report (GSTHR) estimates that by 2021, over 55 million people will be using e-cigarettes or heat-not-burn tobacco products and that the global market will be worth $35 billion.

Disruption is happening at different paces around the world, and Philip Morris is trying to lead the transition so it can maintain a strong position in the nicotine markets of the future.

Overall, the firm's leading technology investments, geographic diversification, global distribution channels, excellent cash flow generation, and lack of exposure to the dynamic U.S. market seem likely to keep Philip Morris on steady ground as the global tobacco market continues evolving.

That being said, there are numerous uncertainties facing Philip Morris in the coming years.

Key Risks

High margins, strong pricing power, recession-resistant demand, and a slow pace of industry change historically enabled tobacco companies to pay out the bulk of their earnings as dividends. For example, over the last five years Philip Morris's payout ratio has sat near 90%.

However, governments around the world continue cracking down on tobacco, including bans on marketing, steadily rising taxes that threaten to price more people out of the market, and increasingly gruesome warning labels on packaging.

These actions, coupled with more smoke-free alternative products becoming available, could put greater downward pressure on global smoking rates and weaken Philip Morris's brand equity and pricing power.

As a result, major tobacco companies are under pressure to invest in next-generation products such as heated tobacco and e-cigarettes to ensure they can remain dominant in the nicotine markets of the future.

If they fall too far behind, bet on the wrong products, or experience unexpected pressure in their core cash cow tobacco operations, then their high payout ratios could eventually strain their ability to adapt.

Philip Morris has done a nice job pouring money into reduced-risk products over the last decade, but we are still in the early stages of RRP adoption, making it difficult to discern which companies will be the biggest winners and which types of products (vaping, heat-not-burn tobacco, etc.) will see the greatest adoption.

Only time will tell whether or not Philip Morris’s customers will decide that “heat-not-burn” alternatives to traditional cigarettes are truly a fulfilling substitute, and more importantly, whether they wish to continue using them or just view them as a tobacco cessation method. Future excise taxes, marketing restrictions, and other regulations affecting RRPs are also a major uncertainty.

The company's diversification and early-mover advantage in RRPs help mitigate some of these risks, but the path won't be linear. Growth could increase or slow any given quarter, creating some anxiety for investors who are nervous about the tobacco giant's ability to thrive in a smoke-free world.

Closing Thoughts on Philip Morris

If you are willing to overlook the secular decline of the overall tobacco industry and don't have moral misgivings about investing in an industry whose products ultimately harm its customers, Philip Morris has the potential to be a reasonable high-yield investment for a diversified retirement portfolio.

The tobacco industry's pace of change appears to be accelerating in certain parts of the world, but Philip Morris continues enjoying recession-resistant cash flows, strong pricing power, manageable cigarette volume declines, a strong balance sheet, and intriguing potential across its portfolio of reduced-risk products.