Founded in 1916, Boeing (BA) is the world's largest aerospace manufacturer, with over 140,000 employees providing goods and services in more than 150 nations around the globe (about 60% of sales are from outside the U.S. although 90% of pretax earnings are domestic). The company recently restructured its operations into three business segments:

Commercial Airplanes (61% of 2017 sales and 54% of 2017 operating earnings): designs and builds commercial jetliners such as 737, 747, 767, 777, and 787 families of airplanes, as well as business jets (private versions of these aircraft).

Defense, Space & Security (23% of sales and 22% of operating earnings): designs, produces, and supports military rotorcraft, satellites, human space exploration, and autonomous systems. Examples include the Air Force KC-46 refueling tanker (based on the 767 jet), AH-64 Apache helicopter, F/A-18 Super Hornet jet fighter, 702 family of satellites, CST-100 Starliner spacecraft, and the autonomous Echo Voyager exploratory probe.

Boeing Global Services (16% of sales and 23% of operating earnings): aftermarket maintenance and service support for military and civilian customers around the world. Currently Boeing Services has over 2,500 aircraft enrolled with more than 60 airlines.

The company also has a financial arm, Boeing Capital Corp (approximately 1% of operating earnings), which helps finance customer purchases. At the end of 2017 Boeing Capital had a loan portfolio of about $3 billion.

Boeing achieved record results in 2017 largely due to its commercial aircraft business, which saw margins soar from 3.4% to 9.6%. These margins are expected to rise to over 11% in 2018 (and remain at that level through 2020), because the large amount of capital investment the company has been making on developing new planes is now largely complete. As a result, Boeing will be able to monetize the heavy investments of the last few years.

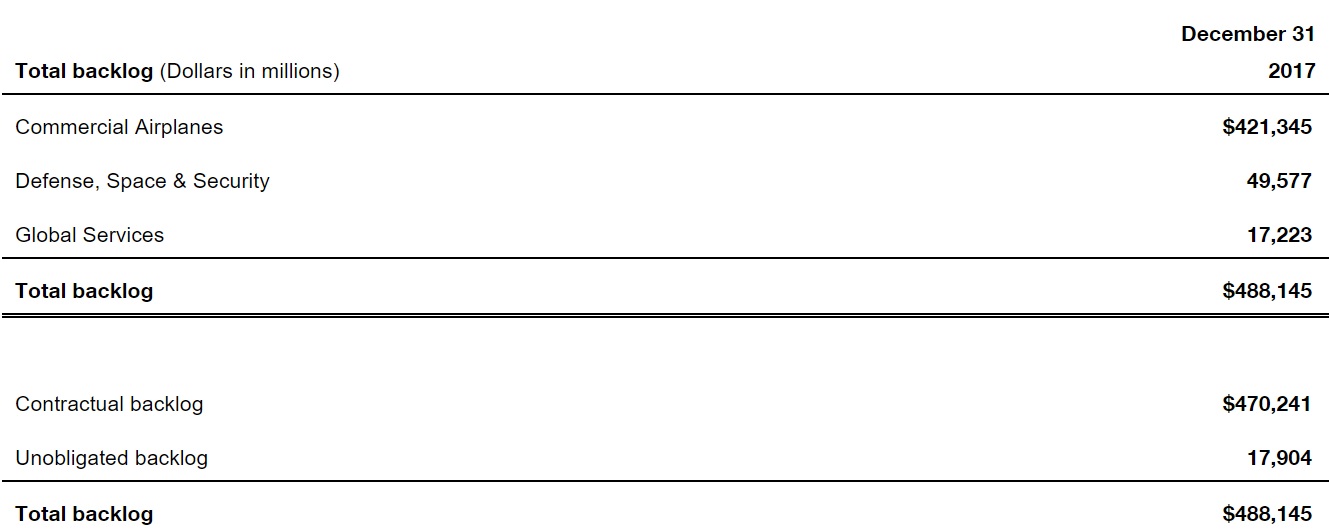

The company finished 2017 with a backlog of 5,864 planes (worth nearly $500 billion), which would take just over seven years to deliver at 2018's projected delivery rate. As commercial plane deliveries ramp, Boeing expects another record year in 2018 with margin expansion across all business units.

Business Analysis

You'd be hard pressed to find an industry with greater barriers to entry than commercial aircraft. As a result, Boeing and Airbus have an effective duopoly in which each owns about 50% of the global commercial plane market.

There are three main reasons for this. First, the complexity involved with developing a reliable, safe, and cost-effective jet airliner is enormous and incredibly time consuming.

For example, the typical new airframe requires eight to 10 years of initial R&D and around five years for a variant of an existing model. The development cost is also immense, with the Boeing 777 and Airbus A380 costing over $10 billion each. Then there's the long and frustrating cost overruns that companies need to deal with. For instance, the 787 Dreamliner ended up being three years delayed to market, and the 777 jet wound up $8 billion over budget thanks to several years in design and production delays.

And we can't forget the most important aspects to building fleets of jets for the world's airlines - safety and reliability. Because these plane costs $250 million to $350 million each, airlines, customers, and regulators require them to be the most reliable and safest form of transportation in the world. Boeing has been manufacturing jets since 1955, demonstrating a long-term track record of success that airlines can trust.

The typical commercial jet needs to be able to operate for at least 25 years and fly tens of millions of miles for airlines to recoup their costs and earn a sufficient profit. As a result, designing and manufacturing such craft requires a deep amount of institutional expertise that rival upstarts are often unable to provide.

Government regulations add another layer of complexity to the market. In the U.S., commercial aircraft products must comply with Federal Aviation Administration regulations governing production and quality systems, airworthiness and installation approvals, and more.

Internationally, similar requirements exist for airworthiness, installation and operational approvals. Since most of the industry’s products are exported around the world, manufacturers most comply with these regulations on a global basis. Naturally, government contracts in Boeing’s defense business are heavily regulated as well.

Basically, it's highly unlikely that any major rival to Boeing or Airbus is likely to appear, owing to the enormous challenges, costs, and long time horizons it takes to start a new plane manufacturing business. Boeing actually lost money over its first twenty years of operations and was only able to strengthen itself as a leader in aerospace because of the high volume of production it achieved during World War II (BA was able to develop its first commercial jet airliner because of the technology and knowhow it had developed in the construction of military jets).

Meanwhile, Airbus required 20 years of subsidies totaling $25 billion from three European governments before it became profitable and self sufficient. Few governments have the will or financial ability to maintain such a burden for such long periods of time.

With such massive investment required to commercialize a new airplane and generally hundreds of orders needed to achieve profitability, national and regional markets are too small for a company to turn a profit, too. In other words, a new entrant would need to be able to take its business globally from day one to be financially viable, creating another barrier to entry. This seems very unlikely.

Network effects are also meaningful and further strengthen Boeing's competitive advantages. Airlines (Boeing's customers) are a very tough business that have to deal with cyclical passenger demand (which fluctuates with the economy), as well as volatile fuel prices and the threat of periodic labor strikes.

This means that they want and need to remove as much uncertainty as possible from their business models. As a result, most airlines will operate just a few types of planes, usually sourced from either Boeing or Airbus. This helps cut down on costly maintenance requirements and lowers the number of skilled technicians needed to service their fleets. Boeing offers them a proven track record going back more than 50 years and has built a global distribution network that ensures spare parts are always available for delivery.

This network effect helps further insulate Boeing and Airbus from competition and creates a potentially lucrative and recurring source of high-margin revenue. Boeing's global services business allows airlines to outsource their maintenance needs to the company and cut down their need to maintain their own technicians (most of whom are unionized and expensive).

Overall, Boeing enjoys enormous competitive advantages that allow it to earn strong margins and returns on capital over time. Profitability is expected to remain strong in the years ahead, too. Now that the development of the 787 is complete, and the 777X nearly so, Boeing will be able to amortize those costs (and boost operating margins) by increasing plane deliveries.

In other words, Boeing is expected to see at least another three very strong profitability years, where it reaps the rewards of many years of expensive R&D and capital investments.

Not only will Boeing likely be enjoying higher margins in the coming years, but its backlog of products and services continues to grow, up $15 billion in 2017 to nearly $500 billion.

Source: Boeing Earnings Report

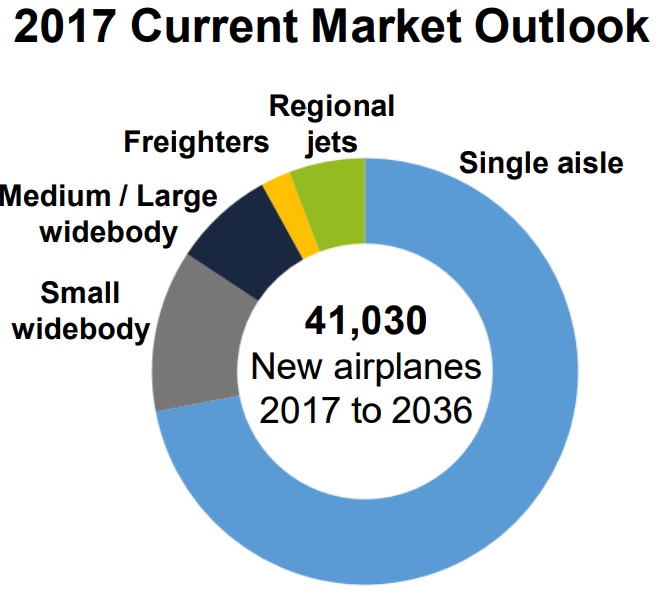

Of course, the key to Boeing's long-term investment thesis isn't necessarily the current large backlog (representing over seven years of sales) but rather future orders. Fortunately, a steadily rising and more prosperous world is expected to fuel strong growth in air travel. This means that over the next three decades airlines are estimated to need over 40,000 new planes (tripling the number of commercial jets in service today).

Source: Boeing Earnings Presentation

And as for Boeing's smaller (but still important) defense side of the business, the company is likely to benefit from the recently passed two-year budget deal, which boosts defense spending by approximately 13% over the next two years.

At the end of the day, Boeing appears to have meaningful growth tailwinds at its back, with 2017 through 2020 likely to be years of record profits and cash flows for the company. This is likely to translate into strong dividend growth and major buybacks. However, there are numerous risks to consider before investing.

Key Risks

While Boeing may enjoy duopoly status with Airbus, investors need to understand that this enormous rival is still a major threat to Boeing's ability to grow its jet backlog in the future.

Boeing is most dominant in wide body jets, but Airbus's A321 is gaining market share in the single aisle market, thanks to boasting the lowest operating costs per passenger mile. This happens to be the largest future jet market, so it's critical that Boeing address this threat.

To do so, Boeing is developing new 737 variants, such as the 737 Max, which it estimates will ultimately cost close to 10% less to operate than the A321. However, such variants mean that Boeing will have to once again go through the costly, complex, and highly uncertain jet design process, which could result in higher than expected costs that eat into cash flow and profitability.

Then there's the rumored development of the 797, a mid-market, small twin aisle jet. Boeing has confirmed that Terry Beezhold, former head designer for the 777X jet, would lead the design team if it decides to greenlight this completely new airframe. If the company does, shareholders need to be prepared for upwards of 10 years of higher development costs and untold potential cost overruns.

In addition, in the future there is risk that Boeing and Airbus may end up having to split the world jet market with a third rival, such as the Commercial Aircraft Corporation of China (Comac). China is one of the few governments in the world with the resources, long-term focus, and political structure (lack of elections to pressure politicians to cut subsidies) to launch a legitimate rival to Boeing and Airbus on the global stage.

And as for big U.S. defense spending increases? While this might benefit Boeing in the short-term, keep in mind two things. First, there is no guarantee that Boeing will necessarily win the contracts it bids for against rivals like Lockheed Martin.

Second, Defense spending, like commercial aircraft, is highly cyclical. And with the federal budget deficit expected to reach as much as $1.2 trillion in 2019, it's very possible that defense spending sees cuts in 2020 and beyond.

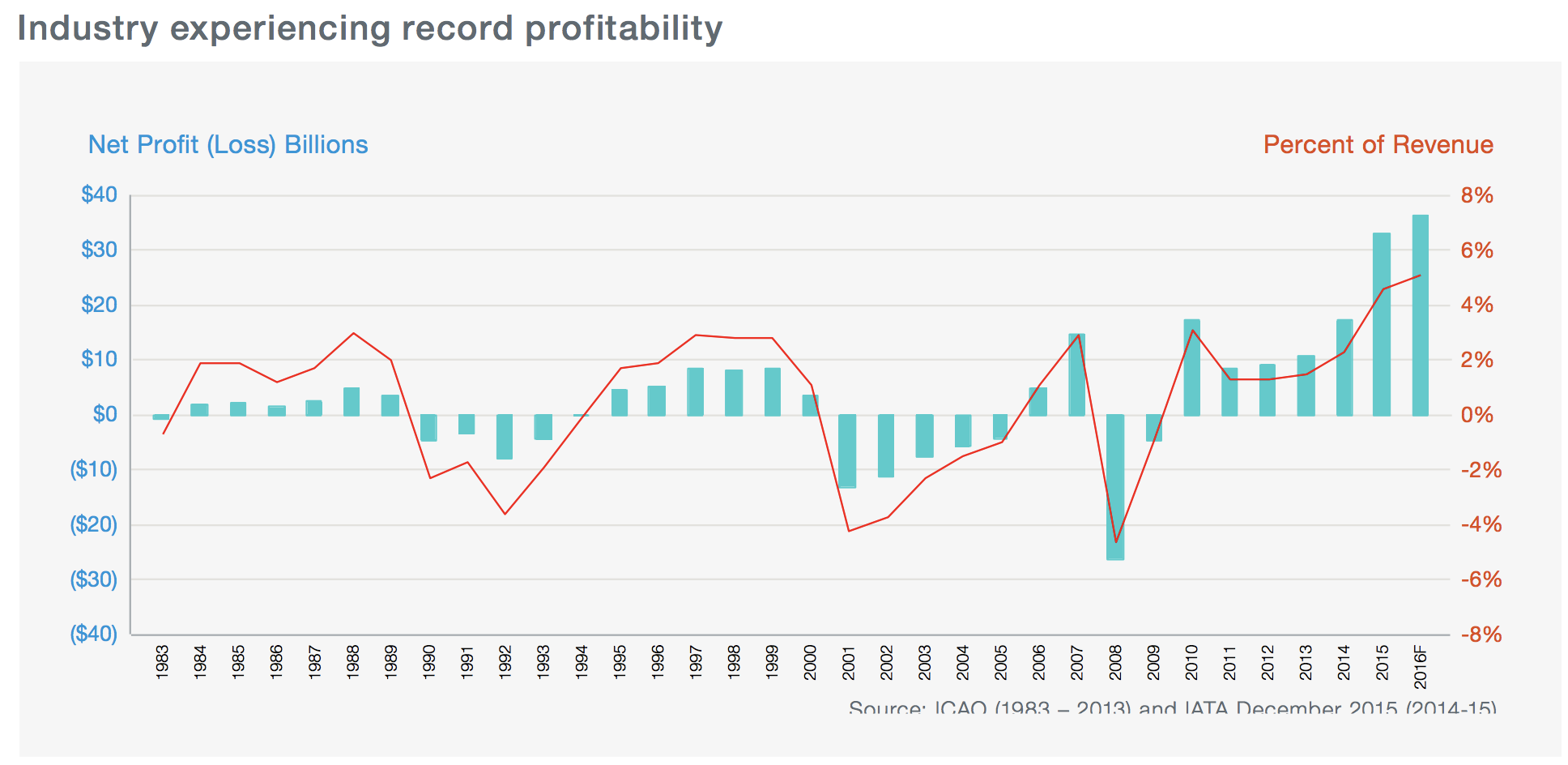

Finally, investors must respect that Boeing operates in a highly cyclical industry. As you can see below, the industry has experienced its fair share of profitability swings throughout the years, and profits are at an all-time high today.

Source: Boeing

There is risk that the industry heads towards overcapacity, with Boeing and Airbus ramping up production rates to fulfill their growing backlogs just as airlines unexpectedly create too much supply in anticipation of stronger future traffic growth or experience economic weakness (especially in emerging markets). Oversupply results in lower prices and declining profits, resulting in canceled aircraft orders. As a result, Boeing and Airbus would have too much supply and will need to lower prices, denting their profitability.

Assuming Boeing’s hefty backlog remains firm, execution is really the biggest challenge going forward. As previously mentioned, supply chains are very complex and delivery delays are somewhat common. When production delays occur, earnings are typically materially disrupted.

Combined with long, costly, and uncertain plane development programs, Boeing's free cash flow (which ultimately funds its dividend) can by incredibly volatile. Not surprisingly, because of Boeing's inherent boom and bust cyclicality, its stock price can experience big swings as well. Taking an extra cautious approach with the price one pays to own the stock is especially important.

Closing Thoughts on Boeing

As one of the two dominant commercial airline manufacturers in the world, Boeing's market share is protected by extremely high barriers to entry. The company’s long-term contracts, healthy backlog, ramping production, and strong replacement and servicing business provide meaningful opportunity for solid margins and profit growth over the years ahead.

Better yet, the company has shown a willingness to share these strong profits with shareholders via an excellent dividend growth track record, including more than 25 consecutive years of uninterrupted payouts. That being said, aircraft orders are still highly cyclical, so the company frequently experiences booms as well as much leaner times.

In other words, investors interested in Boeing need to recognize the potential for several years of much slower or even no dividend growth at some point in the future. This makes it all the more important to consider waiting to buy this blue chip during one of its downturns, when its price is low and its dividend yield is relatively high.