Although it was officially founded in 1968, Cintas (CTAS) started out as a laundry service for businesses during the Great Depression. The company has since grown to become the largest provider of uniform programs in North America.

Cintas' core business provides workers with rental uniforms that they wear each day. The company provides uniform delivery and pickup services via its local delivery routes, cleaning the uniforms before they are returned to workers each week.

As the firm has grown, it has added facility services, first aid and safety services, entrance mats, restroom supplies, fire protection, and more to its offerings.

Today Cintas serves over one million businesses and clothes more than five million workers every day in North America.

Approximately 70% of its customers are in the service-providing sector of the economy, and the remaining 30% are in goods-producing industries such as oil, gas, coal, construction, and manufacturing. The business is divided into three segments:

Uniform Rental and Facility Services (79% of 2017 sales): provides rental and servicing of uniforms and other garments including flame resistant clothing, mats, mops, shop towels, restroom supplies, and other ancillary items. In addition to these rental items, restroom cleaning services and supplies, carpet, and tile cleaning services are also provided.

First Aid and Safety Services (10% of sales): provides sale and servicing of first aid and safety products and training.

All Other (11% of sales): provides fire protection services and direct uniform sales.

Business Analysis

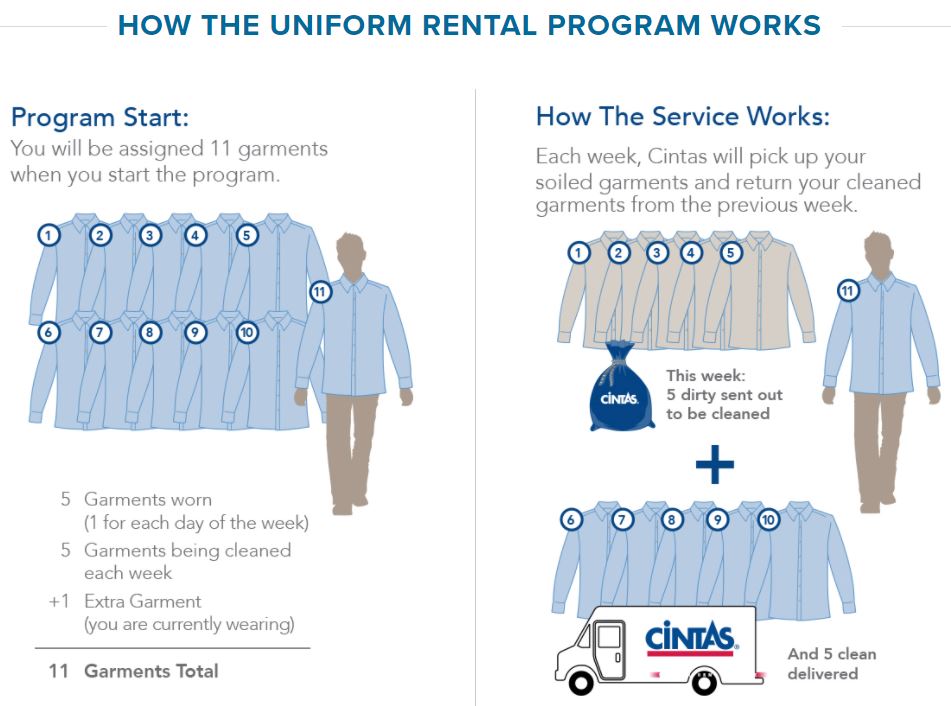

In some ways, Cintas’ business is comparable to a garbage collection company. The business provides each worker with enough uniforms for two weeks. One clean set is for his current workweek, while the other is being laundered and repaired by Cintas.

Cintas will send a rep to the customer’s facility to pick up worn garments and drop off each worker’s clean uniforms for the next week.

Source: Cintas

It doesn’t take a genius to do laundry, so this commodity business is all about efficiency and being the low-cost provider in a particular area (friendly service reps help, too).

With weekly stops made at every customer, route density is the best way to achieve lower costs than competitors because the cost of transportation (i.e. truck trips) can be spread across numerous customers.

To accomplish this, Cintas is the largest company in its industry with over 525 distribution facilities and more than 11,000 local delivery routes. Some customers prefer or need to do business with larger players that have more of a nationwide reach, and being closer to customers also results in better service because delivery times are shorter.

Smaller competitors will have minuscule margins if they try to compete in one of Cintas’ established areas because their transportation and operating costs are higher.

They would also have to disrupt long-standing relationships that Cintas’ reps have with each customer, although that seems like a smaller competitive advantage.

On the other hand, Cintas has the luxury of acquiring these companies to gain new geographies and increase its network density in existing regions, realizing meaningful cost synergies from its acquired businesses.

For example, the company acquired ZEE Medical Inc. for $130 million in the first quarter of 2016. This company was about one-third the size of Cintas’ First Aid business and expanded its product portfolio and ability to reach more customers across North America.

During the third quarter of fiscal year 2017, Cintas closed its $2.2 billion acquisition of rival G&K Services, with expected annual synergies of $130 million to $140 million in the year following the acquisition. The G&K acquisition added 170,000 new customers, further extending Cintas’ services capability and geographic density.

Once Cintas has a local area locked down for business, it can work on increasing its amount of sales with each customer by offering new products and services, such as restroom supplies and tile cleaning. This helps the company increase the productivity of its reps, lower its customers’ costs, and create stickier customer relationships.

Furthermore, many of the industries in need of rental uniforms experience high employee turnover, which drums up even more business for companies like Cintas.

Cintas is also making a substantial investment in a new SAP-driven system that will enable cost savings and better cross-selling capabilities once fully implemented. This project is contributing to the significant capital expenditures Cintas is incurring ($30 million to $35 million in fiscal 2017 and an estimated $45 million to $50 million in fiscal 2018) but should further enhance the firm’s competitive advantages going forward.

While it is very competitive and sensitive to price, the rental uniform market also has a very slow pace of change and provides an essential service – it’s hard to imagine many businesses vertically integrating to start doing their employees’ laundry in-house anytime soon.

These factors have created a relatively stable competitive environment that has helped Cintas gradually grow in size over the decades. The company commanded 25% market share of the $16 billion North American uniform rentals market prior to acquiring G&K, which brings the combined company’s market share above 30%.

However, Cintas has plenty of room for growth as there are still more than 15 million businesses that don’t do business with the company currently. Other than opportunities to expand its market share, the company also has a huge potential to grow revenue and profit by penetrating its existing customer base.

The company’s diversification is another strength as no customer accounts for over 1% of its total sales and no end market is greater than 10% of revenue.

Overall, Cintas is a very durable business that has taken steps in recent years to further strengthen its moat by adding route density, expanding its service line, and taking out costs.

Key Risks

Cintas appears to have a lower fundamental risk profile than many other companies. However, its results can be impacted by employment trends, fuel, and energy costs, and the health of its end markets (e.g. the low price of oil hurt demand from its oil & gas customers as they reduced their headcount).

Fortunately, none of these issues seem likely to impair Cintas’ long-term earnings power. If anything, they could be buying opportunities for patient dividend growth investors.

The longer term issues that could hurt the company’s earnings growth are continued outsourcing of U.S. manufacturing jobs, the rise of automation, and potential changes in the ways businesses choose to dress their employees.

With the U.S. labor market tightening, labor costs may increase in the near future. This might make domestic manufacturers less competitive than overseas competitors, resulting in factory closures and companies choosing to offshore or outsource their operations.

Rather than outsourcing, especially given the Trump administration’s stance, companies are likely to increasingly turn to automation to save on labor costs. In fact, one report believes robots will replace 6% of U.S. jobs by 2021.

Since robots don’t require uniforms, demand could be adversely affected in some of Cintas’ core industries if automation advancements accelerate over the coming years.

Not unlike consumers, businesses could also begin to develop a change in taste for their work environments and try to increase employee morale by moving away from uniforms altogether.

However, Cintas’ strong industry diversification, expanding lineup of products and services, and continued opportunities for acquisitions largely mitigate these concerns for now.

Closing Thoughts on Cintas

Cintas is a boring yet remarkable business. Few companies have survived for so long doing basically the same thing (especially something so simple as providing uniforms and doing laundry), and even fewer have been able to raise their dividend for more than 30 consecutive years like Cintas has.

With a number of enduring competitive advantages and one of the best outlooks for long-term dividend growth, Cintas is a company worth watching.