Cincinnati Financial (CINF) was formed in 1950 and is among the top 25 U.S. property casualty insurers today, offering business, home, and auto insurance.

Insurance companies make money by writing and selling insurance policies (which typically break even or lose money for most insurers), and investing policy proceeds for income until claims need to be paid out (this is where the money is really made). Local independent insurance agencies market Cincinnati Financial’s policies within their communities, which span across more than 40 states.

The company’s revenue mix in 2017 was 55% commercial, 22% personal, investment income 11%, 4% life, 4% excess & surplus and 5% investment gains and other.

By state, 16% of Cincinnati Financial’s premiums came from Ohio, 6% from Illinois, 6% from Indiana, 6% from Georgia, 5% from North Carolina, 5% from Pennsylvania, and 5% from Michigan.

In other words, Cincinnati Financial is nicely diversified by insurance line, premium mix, and geography.

Business Analysis

Insurance companies live and die by managing risk. If insurers fail to price risk accordingly in their policies, they won’t be around for long.

Compared to some insurers, Cincinnati Financial’s underwriting process is somewhat more aggressive because the company targets a combined ratio between 95% and 100%, which means that it expects its policies to be slightly profitable at best (when a combined ratio is below 100%, the company achieves an underwriting profit).

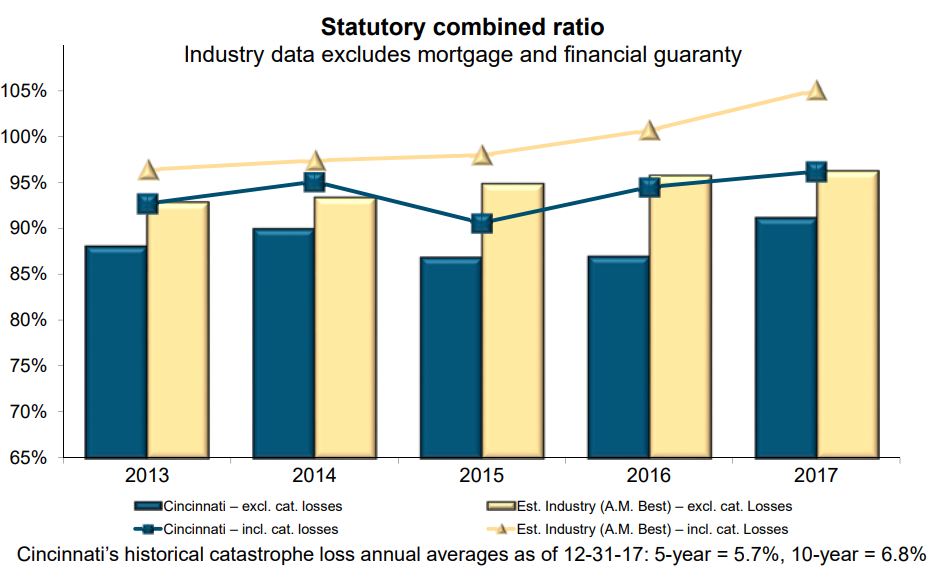

The company ended 2017 with a combined ratio of 97.5%, which is in line with its target range and also marks the company's sixth consecutive year of underwriting profit. Impressively, Cincinnati Financial's results once again exceeded the estimated property casualty industry aggregate of 105%, as per A.M. Best.

In fact, as you can see below, the firm’s combined ratio (dark blue) has meaningfully outperformed the industry (yellow) in the past five years, demonstrating Cincinnati Financial's disciplined risk management practices.

Source: Cincinnati Financial Investor Presentation

The company has also produced 29 years of favorable loss reserve developments, which means it has conservatively booked more losses than it has actually realized each year. This is yet another sign of management’s conservatism.

Cincinnati Financial’s reinsurance program also limits its losses beyond certain thresholds in the event of catastrophes such as earthquakes, and its pristine balance sheet provides additional comfort.

In addition to Cincinnati Financial’s proven risk management track record, the company has several other competitive advantages.

First, its large size (Cincinnati Financial is one of the 25 biggest U.S. P&C insurers) provides economies of scale in marketing, administrative operations, and support staff. Cincinnati Financial is able to spread these costs over a sizable pool of insurance policies to keep its prices very competitive.

Cincinnati Financial is also able to price its premiums lower than smaller competitors because its risk is reduced with a larger pool of policies.

Furthermore, the company’s long operating history, range of insurance products, and size provide branding benefits and trust with the agencies that market Cincinnati Financial’s policies.

Establishing and supporting relationships with agencies takes significant time and cost but provides Cincinnati Financial with relatively low-cost distribution advantages as it expands geographically.

Cincinnati Financial has over 1,700 agency relationships in more than 2,200 locations across the country and does everything possible to support them.

The company doesn’t compete with agencies by selling online or direct to consumers and instead employs more than 3,200 headquarters associates who provide support to over 1,600 field associates (there has also been a 31% increase in field staff since the end of 2012).

As a result, Cincinnati Financial is the number one or number two carrier by premium volume in 75% ofagencies partnering with it for five years or more, although an agency may represent dozens of carriers.

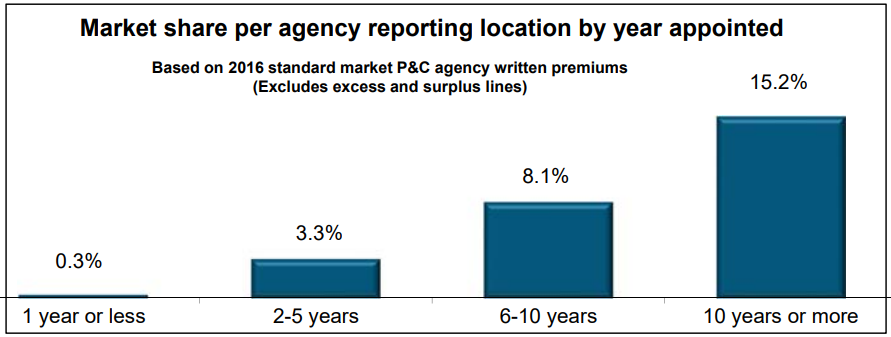

As seen below, Cincinnati Financial has also been effective at expanding its market share with agencies over time. Cincinnati Financial says that its net amount of agency relationships has increased by 44% since the end of 2009 and that it still only has about 9% market share of the estimated $54 billion total P&C premiums produced by currently appointed agencies, leaving plenty of room for future expansion of relationships.

Source: Cincinnati Financial Investor Presentation

In addition to effective distribution channels, the insurance market also requires strict compliance with regulations and substantial amounts of capital to compete.

A large pool of policies and financial assets are needed for an insurer to be able to pay out claims and survive catastrophes, creating barriers to entry for new players.

While catastrophic events can strike at any time, some states are more prone to them than others. For example, California and Florida are frequently hit by earthquakes, hurricanes, and other natural disasters.

One of the things to like about Cincinnati Financial is that it has only a minimal presence in California and Florida. Most of its operations are in the Midwest, perhaps reducing its exposure to major catastrophes.

The wildfires in California and several major hurricane events in Florida last year caused the industry's combined ratio to spike well above 100% (an underwriting loss), but Cincinnati Financial's favorable geographic mix allowed it to continue turning out an underwriting profit.

Finally, the mature state of the P&C insurance market provides another advantage for Cincinnati Financial. When a market’s growth rate is low, new entrants have to steal market share from incumbents to gain a foothold.

Cincinnati Financial’s policy renewal rate has been between 80% and 90% most years, providing a solid base of recurring revenue that helps it keep its policy prices competitive and market share stable.

Insurance is also a product that is always in demand regardless of economic cycles, which has helped Cincinnati Financial generate consistent results over the course of many years.

Key Risks

The insurance industry is known for going through pricing cycles, which significantly impact the profitability of practically all players.

Insurance is essentially a commodity, so pricing follows supply and demand. Demand is generally stable given the non-discretionary nature of insurance, so supply is the main driver of these cycles.

When insurers have a healthy pool of profits, strong capital reserves, and excess underwriting capacity, they are more apt to lower pricing to chase market share for growth. This environment typically results from several years of minimal natural disasters and catastrophes.

After a period of catastrophes and tighter capital conditions, there is less underwriting capacity in the market as insurers look to improve their financial condition. These periods are marked by better profitability and more rational pricing.

Cincinnati Financial must put up with this cyclicality and remain disciplined with its pricing of risk and balance sheet strength (the company maintains an investment grade credit rating), regardless of market conditions.

Of course, unexpected catastrophes are arguably the biggest risk faced by insurers. A “perfect storm” can wipe out smaller, less disciplined players completely.

As mentioned earlier, Cincinnati Financial is fairly well diversified with the states it does business in, avoids some of the riskier areas like California, and has a long operating history, which adds to the confidence investors can have in the firm’s conservative underwriting process.

Underwriting aside, Cincinnati Financial does have more risk with its investment portfolio than many other insurers because it has around 36% of its portfolio invested in common stocks (most other insurers invest 10%-20% of their portfolio in stocks).

The portfolio is diversified (no stock is more than 4% of the portfolio) and invested in many quality dividend growth stocks, but these investments are still more volatile than a portfolio with a higher mix of investment-grade bonds.

Finally, it’s worth noting that while the insurance industry is generally slow to evolve, it is changing. Technology is leading to more advanced data models that are pricing risk more efficiently on a policy-by-policy basis, which will only result in more competition for accounts with the best risk profiles.

Moreover, easy availability of capital and increasing market competition may further exert pressure on policy pricing.

Cincinnati Financial is also completely dependent on independent agencies to sell its insurance policies. According to the Independent Insurance Agents and Brokers of America, independent agencies write about 60% of overall U.S. property casualty insurance premiums today.

However, more policies will likely be purchased online over the coming decade, and a number of "InsurTech" upstarts are looking for ways to disrupt the industry's status quo. Selling policies online could actually result in lower prices and greater profits for insurers because they do not need to pay commissions and can save labor costs as well.

To help mitigate this risk, Cincinnati Financial partners with numerous startup incubators and deliberately focuses on insurance lines of business that are more likely to need an agent: personal lines high net worth, commercial lines key accounts and excess and surplus lines business.

Overall, Cincinnati Financial’s financial conservatism and long-standing customer and agency relationships help reduce many of these concerns.

Closing Thoughts on Cincinnati Financial

Conservative income investors must be very careful if they decide to purchase shares of almost any insurance business. Larger, diversified insurance providers with long track records of managing risk conservatively are often the best bets.

That’s why Cincinnati Financial is a favorite pick for income investors. The company is a proven, well-managed insurance business that has been a sound bet for safe, growing dividend income with 57 consecutive years of higher payouts. Only seven U.S. public companies can match this record.

While the insurance industry will continue experiencing its fair share of performance cycles and needs to adapt to technological changes going forward, Cincinnati Financial has proven to be a disciplined risk taker with both its underwriting and investment portfolio.