Enbridge: A Quality Midstream Company Paying Higher Dividends Since 1995

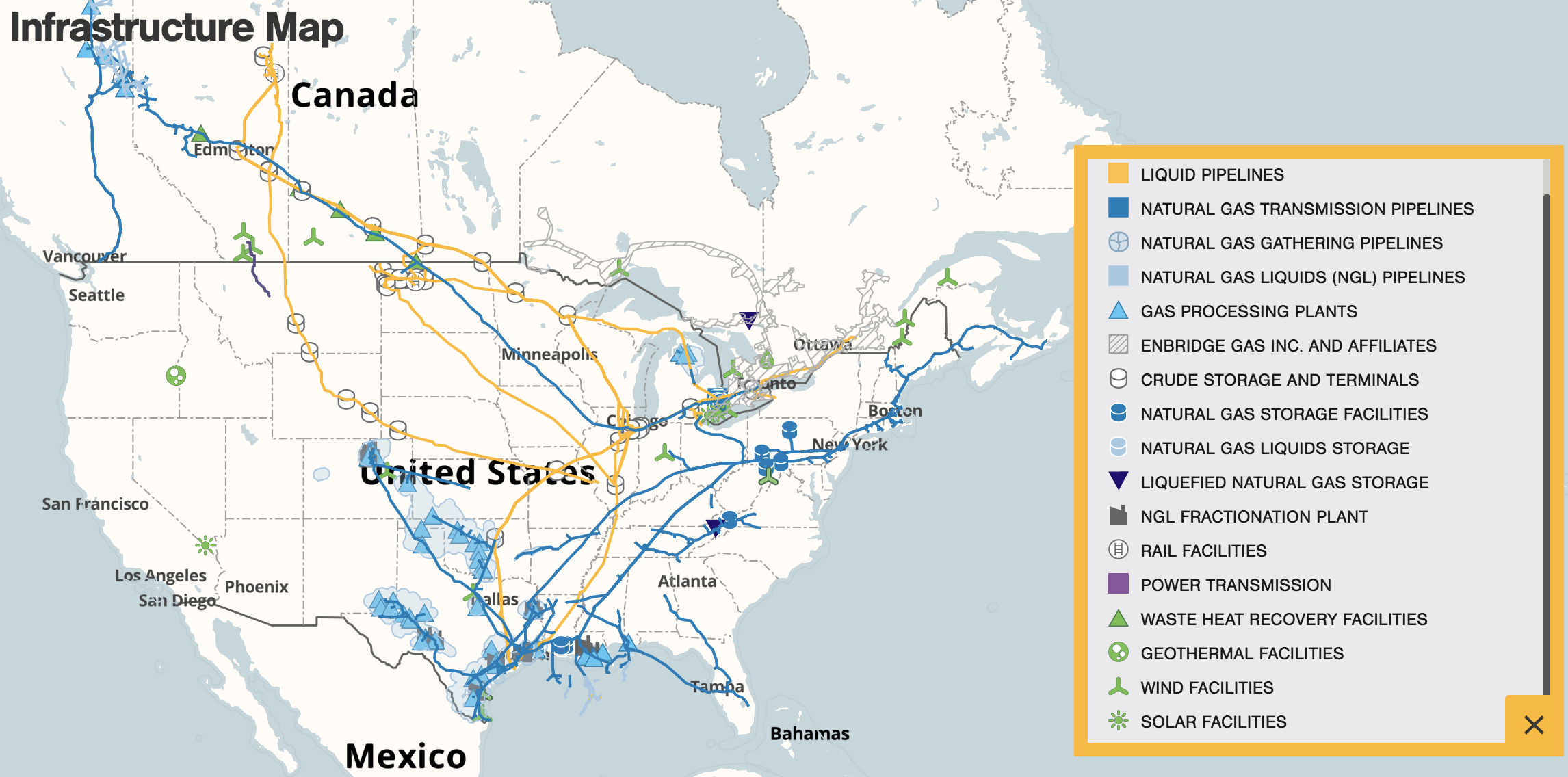

With roots tracing back to 1949, Enbridge (ENB) is North America's largest midstream energy company. The firm's oil & gas pipelines, terminals, storage facilities, and processing plants help connect the continent's most vital energy producing regions. Enbridge also owns regulated natural gas distribution utilities and various renewable power generation assets.

Source: Enbridge

Enbridge's core businesses include:

Liquids Pipelines (55% of EBITDA): the largest network of pipelines and terminals in the continent, this business transports about 25% of the crude oil produced in North America from supply regions (especially in Western Canada and North Dakota) to end-user markets such as refineries and exporters located on the U.S. Gulf Coast.

Gas Transmission and Midstream (26% of EBITDA): Enbridge's natural gas pipelines and gathering and processing facilities in Canada and the U.S. move gas from supply basins to demand centers, transporting about 20% of the natural gas consumed in America.

Gas Distribution (13% of EBITDA): Enbridge owns the largest regulated natural gas utility in North America, serving 3.7 million retail customers in Ontario and Quebec.

RenewablePower & Energy Services (6% of EBITDA): uses wind and solar to generate power that is sold to utilities under long-term agreements. Enbridge also provides various transportation, storage, supply management, and product exchange services for its customers.

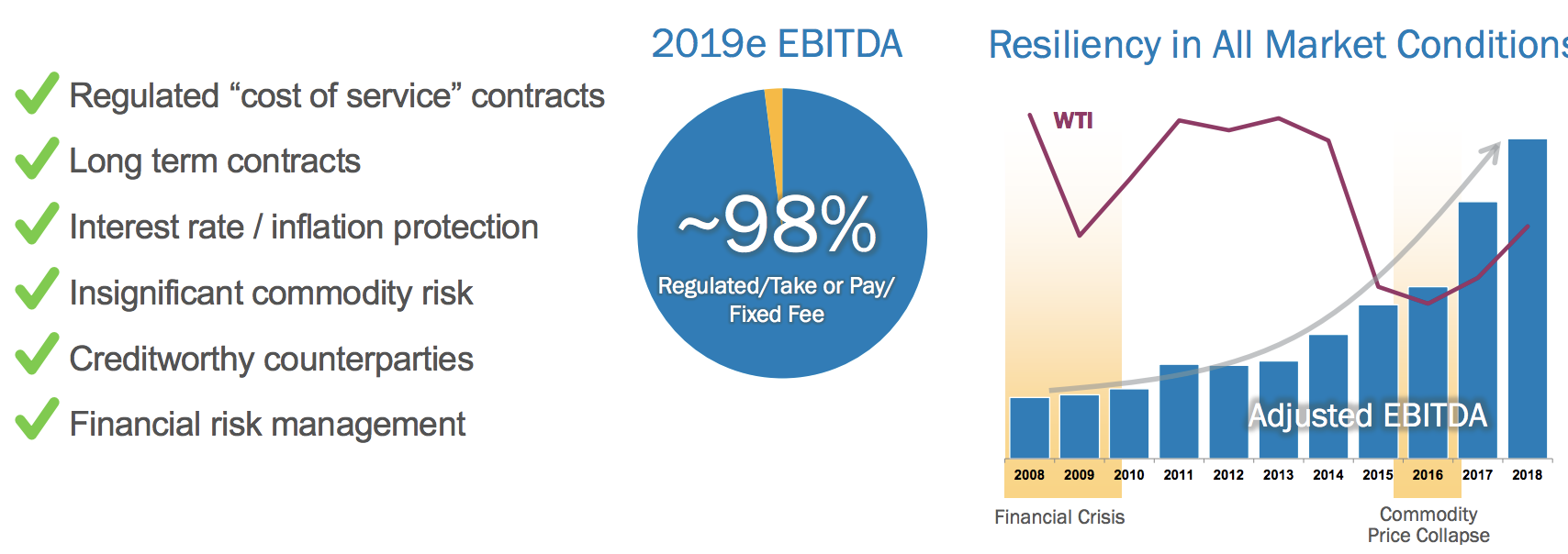

Across all of its businesses, Enbridge has minimal direct exposure to commodity prices. Approximately 98% of the firm's EBITDA is generated from regulated "cost of service" contracts, has take or pay volume commitments, or is underpinned by fixed fee agreements.

Enbridge has increased its dividend each year since 1995.

Business Analysis

The midstream industry enjoys numerous competitive advantages that have helped Enbridge reward income investors with predictable payouts for more than two decades.

Unlike energy producers, whose profitability is directly tied to oil & gas prices, virtually all of Enbridge's revenue is supported by long-term contracts with fixed fee provisions and often minimum volume commitments.

Regardless of short-term energy price volatility, Enbridge's cash flow remains steady as long as its customers can continue honoring their agreements.

On that note, the company's energy and utility customers are among the financially strongest in the industry, including blue-chips such as Exxon, Con Ed, and Chevron. In fact, 93% of Enbridge's cash flow is derived from customers with investment-grade credit ratings.

As a result, the company's cash flow has proven to be very resilient over time. Enbridge's adjusted EBITDA even grew during the financial crisis and the 2014-16 oil price crash.

Source: Enbridge Investor Presentation

Besides the low-risk commercial agreements that back Enbridge's cash flow, the energy infrastructure industry also has high barriers to entry due to its high capital intensity and regulated nature.

Major projects often cost billions of dollars to complete, with a single mile of new pipeline costing over $7 million per mile to build in recent years. Meanwhile, various regulators have to sign off on new construction.

Most projects don't get approved unless there is an obvious need for additional takeaway capacity to address bottlenecks and price disparities between production hubs, creating relatively little overlap of pipeline systems.

In other words, pipeline companies often enjoy an oligopoly that helps ensure they earn a reasonable return on their substantial infrastructure investments. There are also few substitutes for pipelines given their safety and cost-efficiency, along with geographical constraints. (Many oil & gas formations are in hard-to-access areas.)

Furthermore, pipelines enjoy relatively stable demand patterns since many of the products that require refined oil and gas are non-discretionary in nature. In a way, the midstream industry is similar to the utility sector in that it provides an essential service for energy producers, resulting in a stable cash flow stream.

Enbridge's assets are particularly important to customers and difficult to replicate given Canada's limited pipeline system and the firm's scale. For example, on any single day, Enbridge is the largest single conduit of oil into the U.S., transporting over 60% of all U.S.-bound Canadian exports. Without Enbridge, North America's energy economy could not function.

Customers especially value the firm's integrated system since it connects the largest supply basins to the best markets, including three-fourths of the refineries in North America (which especially need the heavy crude produced in Canada). This provides energy producers with more flexibility to maximize the value of their output.

Management also runs the business conservatively to ensure Enridge retains its strong competitive position. The company is not dependent on any specific supply basin, and its operations are nicely diversified across oil, gas, and utilities markets.

Enbridge also maintains a BBB+ investment-grade credit rating from Standard & Poor's (tied for the highest rating in the industry), has a self-funded business model which requires no equity issuances to fund its growth, and targets a reasonable payout ratio of 65% of distributable cash flow.

Looking ahead, Enbridge expects to deliver 5% to 7% annual cash flow per share growth, with its dividend likely rising at a similar pace. The company sees opportunities to extend and expand its pipelines, continue building out its export infrastructure, and serve more customers with its gas utilities.

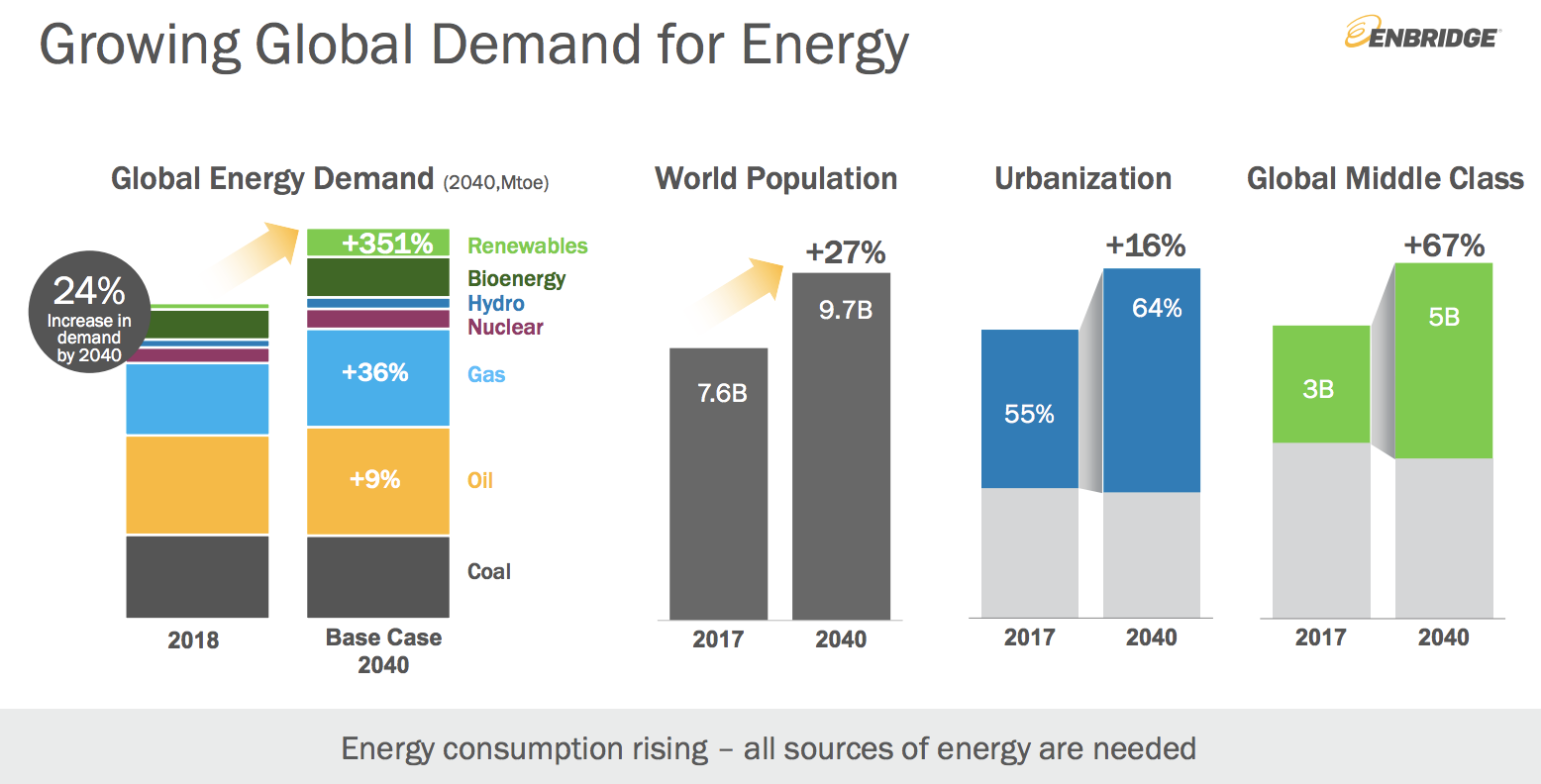

Enbridge's growth plan is supported by an expected 24% increase in global demand for energy by 2040, fueled by the world's population growth, increased urbanization, and rising living standards in developing markets.

Source: Enbridge Investor Presentation

As this plays out, Enbridge believes North American liquids and natural gas supply will rise thanks to the continent's status as a low-cost energy producer and the opportunity that creates for oil and liquefied natural gas exports.

If the future develops as management hopes, the company's pipelines, terminals, and processing facilities should enjoy solid demand for years to come. However, there are several risks that could weigh on the firm's future growth.

Key Risks

First, note that as a Canadian company, Enbridge pays its dividend in Canadian dollars. This creates some currency risk in that a stronger U.S. dollar might decrease the effective dividend amount for American shareholders, at least in the short term (each quarterly dividend is converted from Canadian dollars to U.S. dollars when it is paid, based on prevailing exchange rates).

In addition, like all Canadian stocks, U.S. Enbridge investors face a 15% foreign dividend tax withholding. Tax treaties between the U.S. and Canada allow U.S. investors to potentially recoup this withholding, but it can be a complicated and lengthy amount of paperwork at tax time.

As for fundamental risks to the business, one of the biggest uncertainties facing the energy sector is how long demand will grow for oil and gas.

Some investors worry that the world's growing push to reduce carbon emissions and embrace renewable energy will cause fossil fuel demand to peak within 20 years, sooner than many energy executives expect.

While North America's low-cost supply position wouldn't be threatened, a decrease in future production growth rates could dampen Enbridge's growth ambitions and weigh on the company's valuation.

In the short term, Enbridge's growth also faces some challenges due to execution risk with its Line 3 replacement project, which accounts for nearly half of the firm's backlog.

This pipeline project has encountered various delays due to various permitting challenges. We previously reviewed these issues and do not expect them to affect Enbridge's dividend safety profile, even if Line 3 were to be scrapped. However, further setbacks could slow the company's short-term growth prospects.

Finally, investors should also note that Enbridge's stock price is correlated to oil prices, even if its cash flow is not. In other words, while Enbridge is effectively an energy utility, it's stock performance is nowhere near as stable as actual regulated utilities.

Closing Thoughts on Enbridge

Enbridge has proven itself to be one of the best-run midstream companies in North America. The business has enjoyed predictable cash flow for many years thanks to its long-term, commodity price-insensitive contracts with investment-grade customers.

While weak energy prices have raised some concerns about the industry's long-term growth potential, Enbridge remains a financially solid firm with a conservative self-funding business model, reasonable payout ratio, diversified asset mix, and strong commitment to its dividend.

The company's short-term cash flow and dividend growth could be slowed by additional unfavorable developments with its delayed Level 3 project, but Enbridge otherwise looks like a reasonable long-term income investment for investors who are comfortable with the industry's risk profile.