National Health Investors: High-Yield REIT With Uninterrupted Dividends Since 2001

Formed in 1991 when National HealthCare (NHC) spun off its senior housing properties, National Health Investors (NHI) is one of America's oldest healthcare REITs. The company has built a small but diversified portfolio of properties across various industries, including independent, assisted living, and memory care communities; gated retirement communities; skilled nursing facilities; medical office buildings; and specialty hospitals.

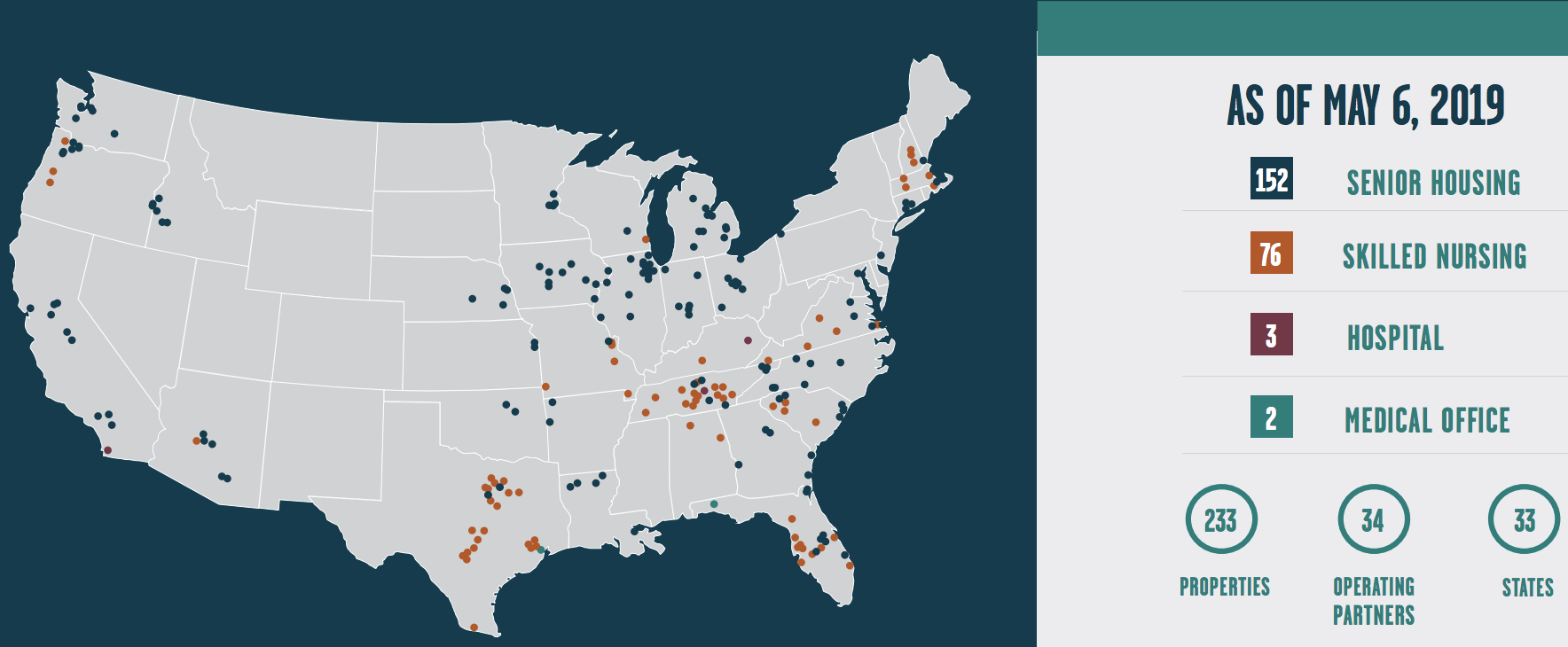

As of May 2019 the REIT owned 233 properties in 34 states, leased to 34 medical facility operators. About 97% of National Health Investors' revenue is derived from triple net leases on sale-leaseback deals (NHI buys a property and then leases it back to operator under a long-term contract), in which the tenant pays maintenance, insurance, and taxes.

Source: NHI Earnings Supplement

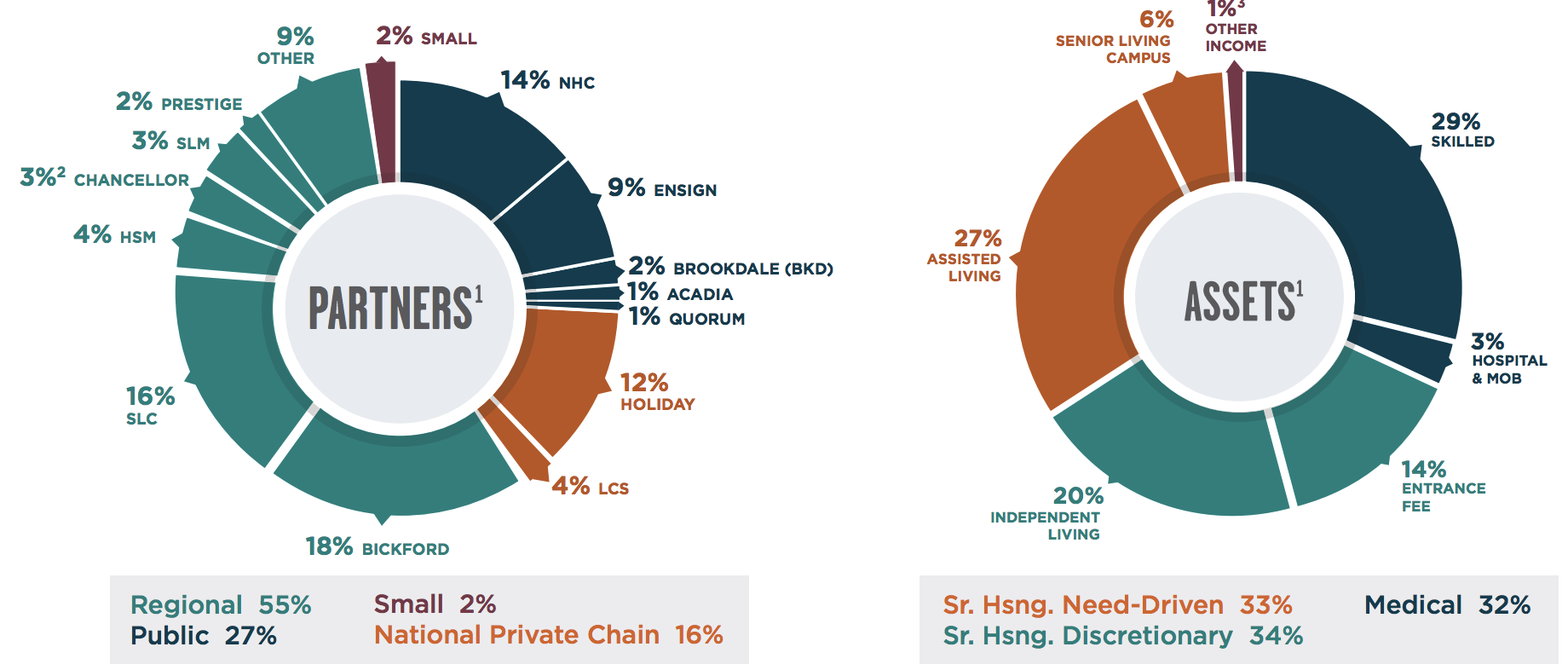

Since being spun off in 1991, National Health Investors has become far more diversified, recently acquiring hospitals and medical office buildings, or MOBs. Hospitals and MOBs generally have more stable economics and cash flows than senior housing (SNH) and skilled nursing facilities (SNF) due to their superior rent coverage ratios (healthier tenants) and lower supply growth risk.

However, it should be pointed out that National Health Investors' diversification, while improving, isn't high in absolute terms. For example, about two-thirds of its assets are still focused in some form on senior housing, with another 30% in SNFs. Just 3% are in more stable MOBs and hospitals.

In other words, National Health Investors has one of the highest exposures (95% of assets) to the SNF and SNH industries of any healthcare REIT.

From a tenant perspective, NHC, from which NHI was spun off, now represents just 14% of rent compared to 100% in the early 1990s. The firm's largest tenant, Bickford Senior Living (manages or operates over 50 independent private senior living, assisted living, and memory care branches throughout the country), makes up 18% of revenue. NHI mostly works with regional operators.

Source: NHI Earnings Supplement

While senior housing relies primarily on private pay sources, note that a significant portion of the revenue of NHI's skilled nursing facilities tenants is derived from government-funded reimbursement programs, such as Medicare and Medicaid.

Specifically, as of the end of 2018, 27% of National Health's SNF revenue was derived from tenants being paid primarily by Medicare or Medicaid. This means the REIT's government-funded rental exposure is about 8%.

National Health Investors' dividend track record is marred by a severe cut in 2000 (due to a seismic shift in Medicare and Medicaid policy at the time) but the REIT has otherwise had a good record, with uninterrupted dividends since 2001 and higher payouts each year starting in 2010.

Business Analysis

While National Health Investors has operated as an independent company since 1991, the REIT's 2018 sales only totaled $295 million since it has taken a very disciplined approach to growth. For context, peer Omega Healthcare Investors (OHI) was founded in 1992 and generates nearly $900 million in annual revenue.

National Health Investors has long opted for quality over quantity when it comes to growing its property portfolio. While some REITs will "reach for yield" and buy properties with cap rates as high as 12%, National Health prefers to deal with the strongest operators in the industry.

Most of its largest operating partners have been in business for more than 40 years, and like many of its rivals National Health also specializes in triple net lease arrangements. Under these contracts, the company merely serves as a landlord collecting rent, leaving the tenant responsible for covering costs such as taxes, insurance, and maintenance.

National Health's leases also typically run 10 to 15 years in duration (no major lease expirations through 2023), ensuring solid cash flow predictability from which to fund its dividend.

Management's payout policy is conservative as well. Over time the firm has grown its dividend slower than its AFFO per share (similar to free cash flow for REITs), maintaining a payout ratio near 80%. This increases National Health's margin for error should any tenant troubles arise and provides the REIT with larger amounts of retained cash flow to reinvest in growth opportunities.

Maintaining a conservative payout ratio has proven especially helpful in recent years as the SNF and SNH industries have faced various financial difficulties.

For example, the REIT had to renegotiate master leases with Holiday (12% of annual rent) at the end of 2018 because they were unsustainable. The master lease rent was lowered 20%, and the lease duration was extended to 2035. The lower rent raised Holiday's lease coverage ratio (net operating income divided by debt and lease payments) from a risky level of 1.16 to a somewhat more reasonable level of 1.25.

National Health Investors, like many healthcare REITs, has had to transition several other properties away from struggling tenants or renegotiate leases that can impact cash flow. In recent years cash flow growth has slowed due to ongoing transition effects offsetting continued investments into new properties.

Despite these headwinds, management expects the company's payout ratio percentage to remain in the low to mid-80s range. While that is historically high for the REIT, it is not unsafe for this industry, where the average payout ratio exceeds 90%. In fact, Omega Healthcare's AFFO payout ratio hit 98% in 2018 as it dealt with its own tenant challenges.

Besides trying to focus on stronger tenants and maintaining a lower payout ratio than most of its peers, National Health is also very conservative with its use of debt. For example, the REIT has a firm policy of maintaining a leverage ratio between 4.0 and 5.0, below the industry average near 5.5. This ensures that the company has ample financial flexibility and can borrow very cheaply.

While the REIT does not have a credit rating from Standard & Poor's, its reasonable debt levels allow it to borrow at an average interest rate of 3.7%, which is about in line with the average yield of BBB-rated bonds. In other words, the bond market appears to price National Health's debt as if its credit rating was around the BBB investment grade level.

When combined with National Health's historical 20% retained AFFO (i.e. the company distributes 80 cents of every $1 in free cash flow it generates as a dividend, retaining the other 20 cents for growth projects), the REIT has been capable of funding profitable growth despite its relatively small size.

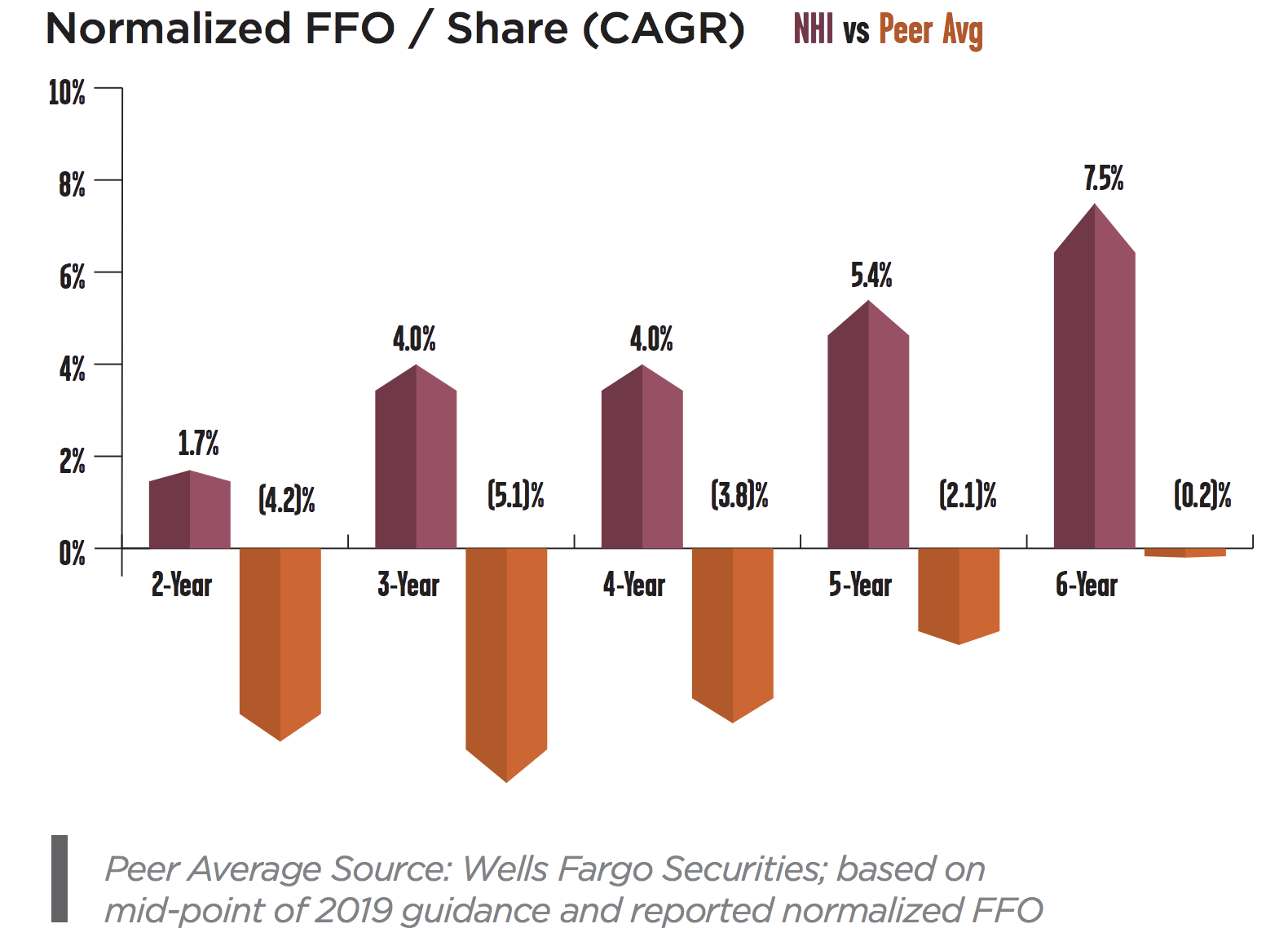

The success of National Health's conservative and disciplined approach can be seen in its industry-leading historical growth in cash flow (FFO) per share. While tenant and industry headwinds have caused many of its peers to report cash flow declines, National Health has continued generating a moderate pace of growth.

Source: NHI Earnings Supplement

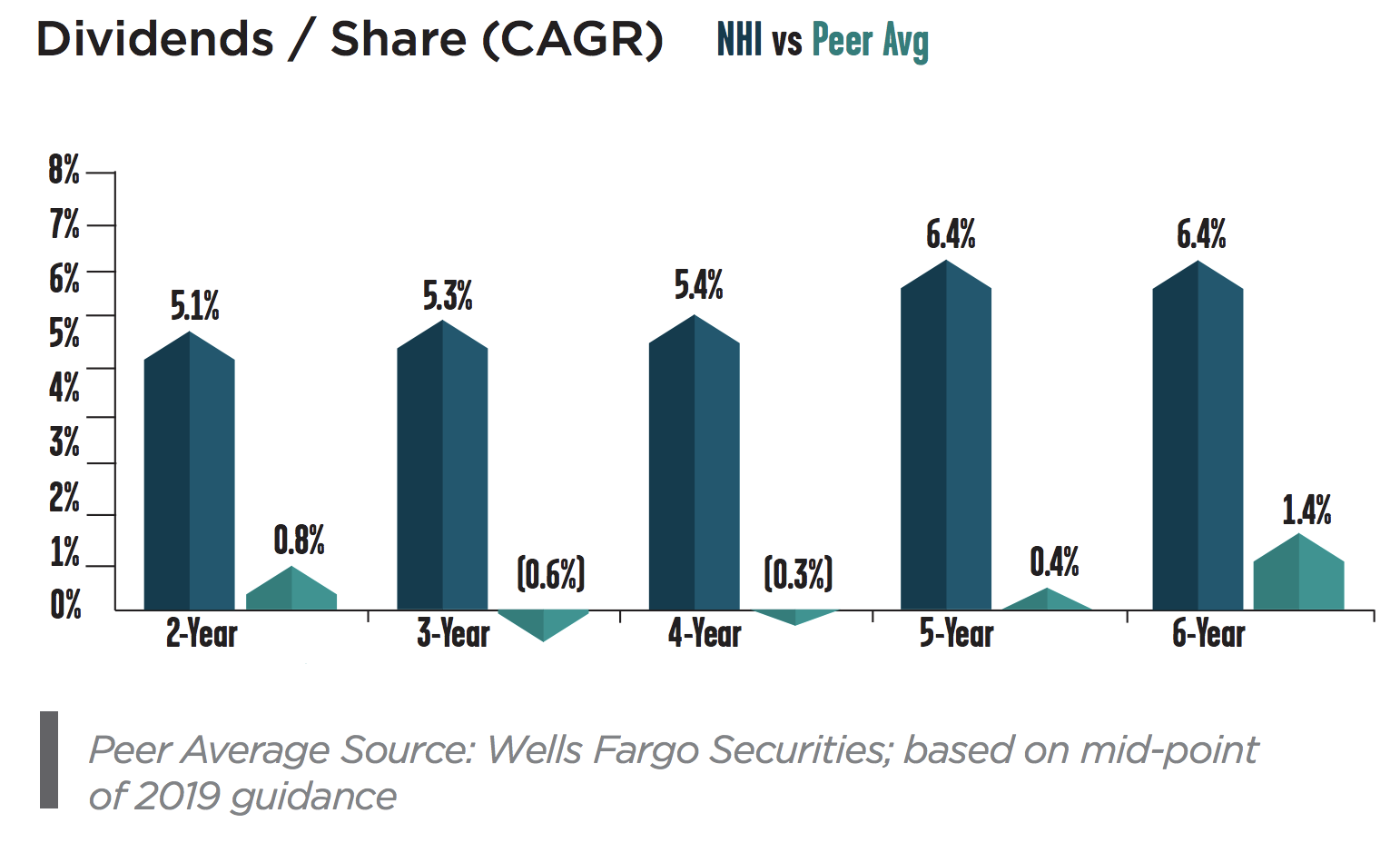

Couple with the REIT's conservative payout ratio policy, National Health has also rewarded shareholders with mid-single digit dividend growth while payouts have largely stagnated across its peer group.

Source: NHI Earnings Supplement

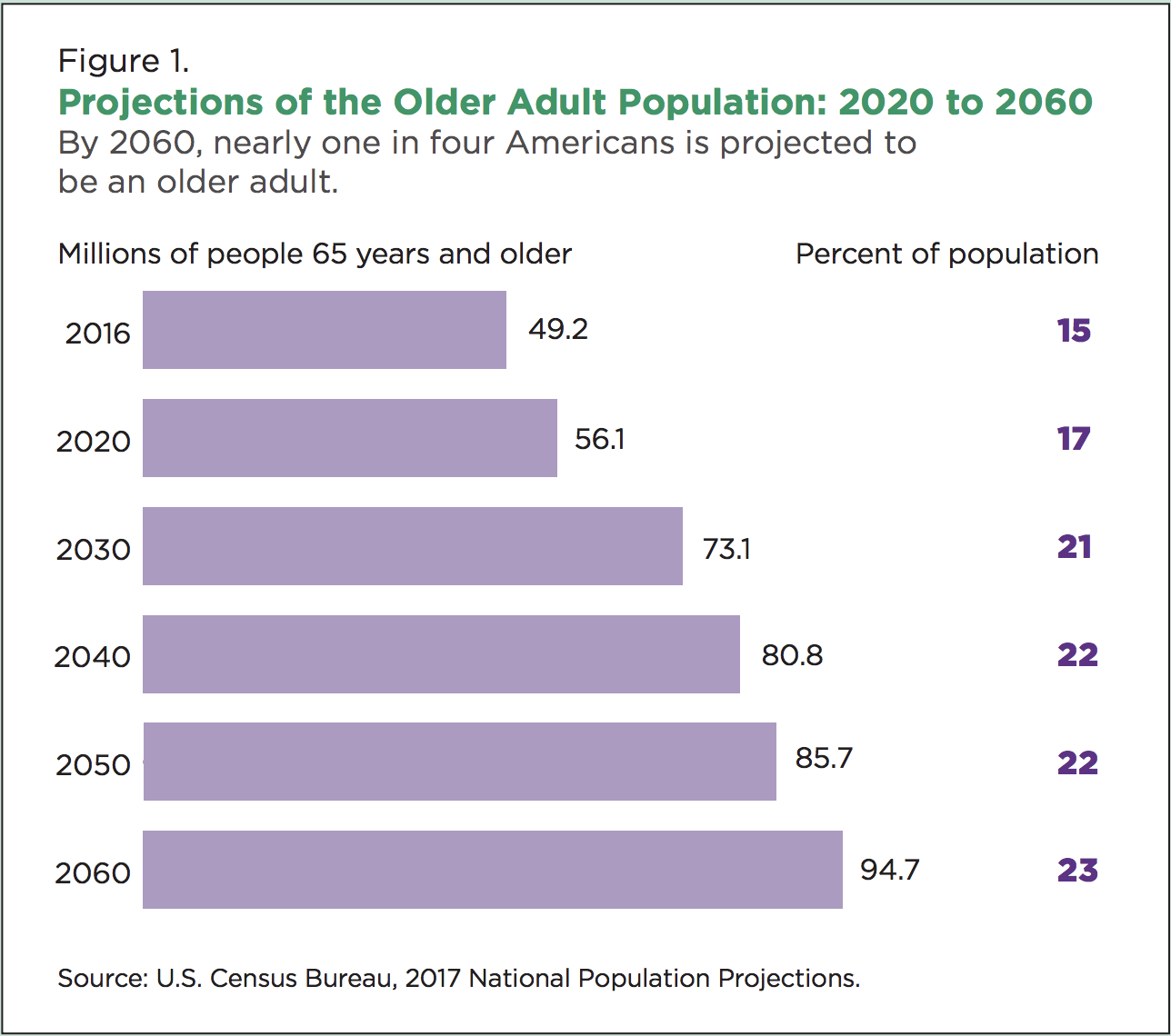

Going forward, America's aging population is expected to eventually improve the fortunes of the skilled nursing and senior housing markets.

The U.S. Census Bureau projects that by 2060 nearly one in four Americans will be over the age of 65, up from 15% in 2016. As a result, U.S. healthcare spending is projected to rise by 5.5% per year from 2017 through 2026, resulting in healthcare accounting for 19.7% of GDP (up from 17.9% in 2016) according to the Centers for Medicare & Medicaid Services.

Source: U.S. Census Bureau

As this demographic shift places out, demand is expected to rise for senior housing and skilled nursing facilities. That is expected to eventually reverse the negative occupancy trends the industry has faced in recent years, when overcapacity combined with falling government reimbursement rates to hurt operator finances.

And with the U.S. healthcare real estate market totaling $1.5 trillion in value and remaining highly fragmented, National Health Investors has a potentially long growth runway in terms of future property acquisitions it can make to continue fueling its rising dividend.

However, while National Health appears to be one of the more impressive REITs in its industry, there are several challenges it could face in the coming years.

Key Risks

National Health Investors has done a solid job of navigating challenging industry waters in recent years. That's thanks to management's focus on buying only high-quality properties which are generally leased to strong operators with above-average rent coverage metrics.

However, the company still faces risk from ongoing struggles in the skilled nursing and senior housing industries. For example, in recent years the Centers for Medicare and Medicaid Services (CMS), which operates government healthcare spending, has made painful but necessary changes to federal healthcare spending policies.

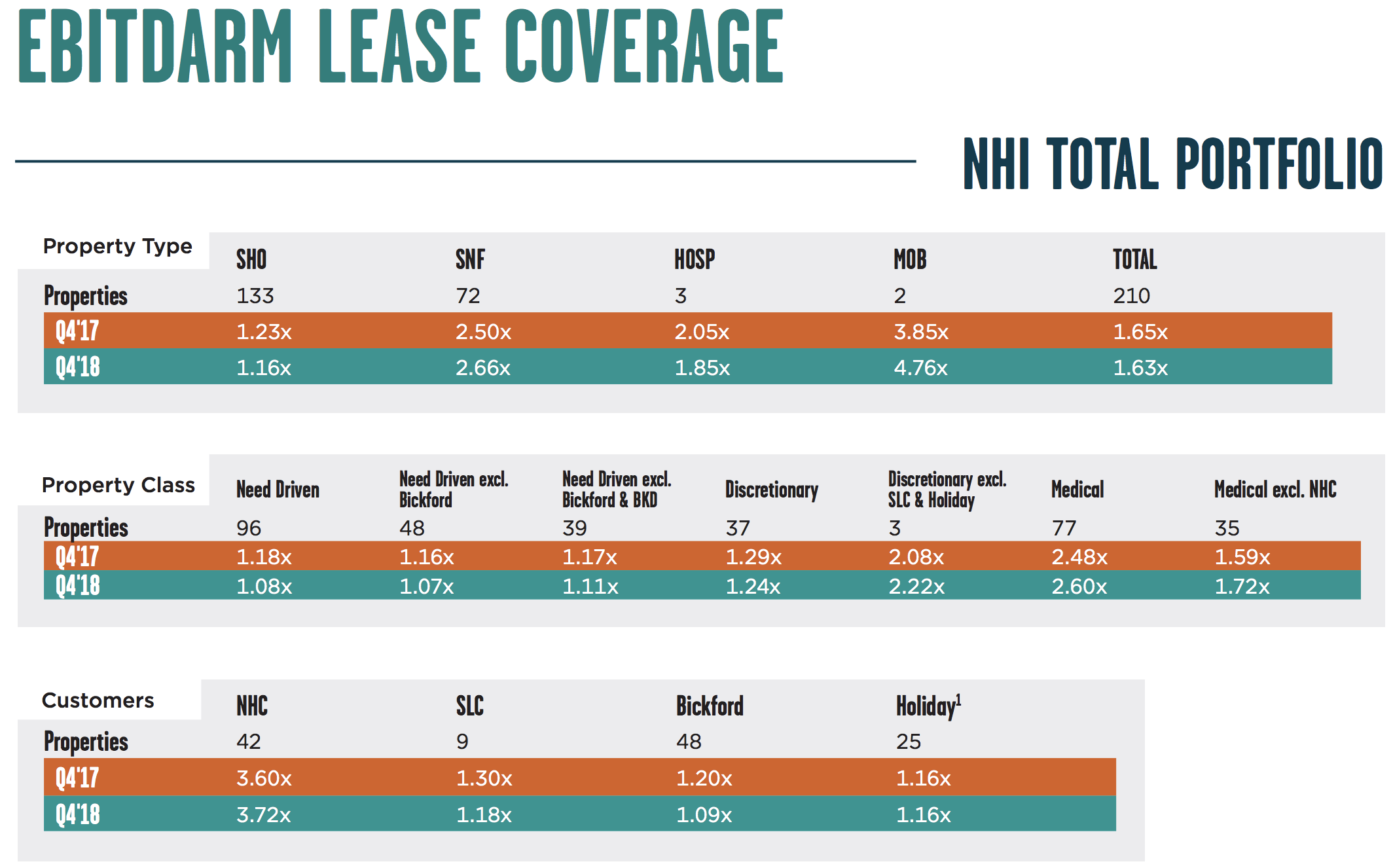

These actions have resulted in shorter patient stays and lower reimbursement rate increases at skilled nursing facilities, which represented 29% of National Health's assets in 2018.

When combined with rising labor costs, tenants' margins are getting squeezed and their lease coverage ratios have declined. This includes some of National Health's largest tenants, who could eventually run into trouble being able to pay their full rent.

Source: NHI Earnings Supplement

Approximately 60% of the REIT's rent is from its four largest tenants, and the lease coverage ratios for those operators was rather weak at the end of 2018 with the exception of NHC.

Bickford and Senior Living Communities especially saw significant lease coverage declines which means a greater risk that those customers may not be able to pay their rent in the future. That's especially true if continued government healthcare policy changes reduce reimbursement rates in the future.

While occupancy at SNH and SNF facilities is expected to rise in the coming years to reduce some of the pressure tenants are facing today, those extra revenues might be offset by rising labor costs, as has been occurring across the industry due to the strong job market.

During the fourth-quarter 2018 conference call the firm's CEO mentioned that about 5% of the REIT's property leases were in trouble, which might require lease renegotiations to keep them solvent (they might also be sold or management might attempt to find healthier tenants).

The good news is that management has done a nice job of managing risks, via use of long-term master leases backed by collateral and securitization, such as an operator's credit lines. However, if enough tenants eventually get pushed over the edge, financial pressure on National Health would mount.

Would it be enough to cause the REIT to once again cut its dividend? That seems unlikely, especially when you take a closer look at the changes that triggered National Health's major dividend cut in 2000.

Back in 2000 and 2001, sweeping Medicare changes caused devastation throughout the skilled nursing industry at a time when National Health was far less diversified. So when a major operator went bankrupt, this triggered a technical default (covenant breach) that forced it to slash its payout

Today the REIT is far more diversified, and its relatively low and stable payout ratio and leverage mean that such a drastic cut isn't likely. Still, the risks of this kind of worst-case scenario have risen somewhat in recent years, as the supposed benefits of the America's fast-aging demographics have failed to stem the falling profits of the skilled nursing and senior housing industries.

Investors will want to monitor the health of the REIT's four largest tenants to ensure they do not require significant financial support or lease renegotiations that would pressure National Health's payout ratio and balance sheet.

In other words, despite its solid financial position today, National Health Investors could prove to be the "nicest house in an unsafe neighborhood" as the healthcare sector continues evolving (reimbursement model changes, demographics, etc.).

Closing Thoughts on National Health Investors

Some healthcare REITs find themselves under financial pressure today as parts of the industry battle excess supply, rising labor costs, and shifting reimbursement models. However, National Health Investors' relatively low debt ratios, focus on stronger tenants, and historically conservative payout ratio has allowed it to continue growing its business and dividend.

With that said, income investors considering National Health still need to recognize the meaningful risks the business could face in the years ahead. About 60% of the firm's revenue is generated by four operators (it's critical they remain healthy and able to pay their full rent obligations), and skilled nursing facilities, which are under some of the most pressure in the sector (high dependence on Medicare and Medicaid reimbursement), account for close to 30% of its assets.

Simply put, an investment in National Health probably requires greater monitoring and may not be appropriate for the most conservative dividend investors, even despite some of the company's impressive industry-leading metrics.