Buckeye Partners (BPL) Hints That Payout Cut Might Be Coming

Buckeye Partners (BPL) has long been a favorite master limited partnership (MLP) among income investors. That's thanks to the firm's impressive track record of steadily growing payouts which up until recently included 22 straight years of annual distribution increases and 32 years of uninterrupted payments.

However, the MLP bear market, now in its fourth year, has put Buckeye Partners under immense strain and forced it to freeze its distribution growth in 2017. And now continued deterioration in its fundamentals has sent the yield to 14% as investors start pricing in a potential distribution cut.

How likely is Buckeye Partners to actually cut its payout? Well, as we first pointed out in our March 2018 thesis, the signs aren't looking good.

Fundamentals Continue to Move in the Wrong Direction

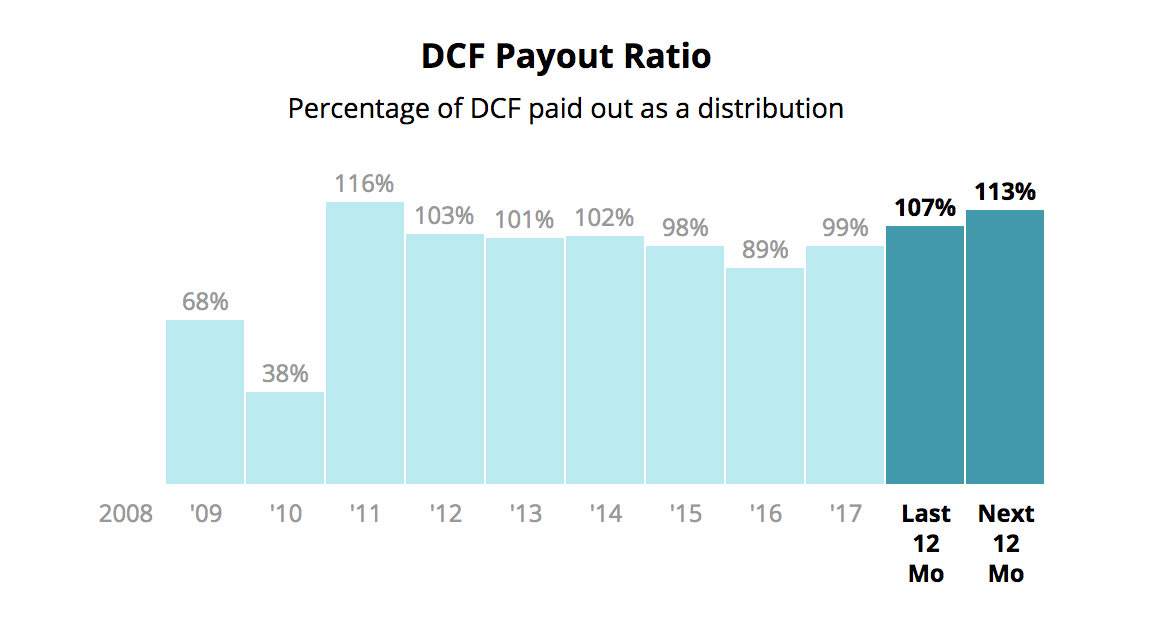

The first thing MLP investors need to focus on in determining payout safety is the distribution coverage ratio, or DCR, which is the ratio of distributable cash flow divided by the distribution.

In this industry, a ratio of 1.1 or higher is considered sustainable. In the second quarter of 2018, BPL's DCR came in at an unsustainable 0.87, which is down from a still high-risk level of 0.95 in the second quarter of 2017.

For the first half of 2018, the MLP's DCR was 0.89 compared to 1.01 a year earlier. Now it's true that throughout its history Buckeye Partners has gone through several periods where coverage was below 1.0, and historically the MLP has never had a particularly strong coverage ratio.

Source: Simply Safe Dividends

However, with management now guiding for full year 2018 coverage of 0.9 to 0.95, despite several projects coming online, investors have good reason to be concerned.

That's because management, which in June stated, "We have no intentions of cutting Buckeye's distribution, and we continue to view a distribution cut as an option of last resort", is now indicating that a potential payout cut is possible.

Management No Longer Confident in Distribution Sustainability

Buckeye's problem stems from the fact that it has focused too much on increasing its distribution at the cost of a potentially dangerous distribution coverage ratio.

For example, including 2018's guidance the average coverage ratio over the last six years will have been 1.0. This means that MLP has been paying out all the distributable cash flow it has been generating, and funding all growth through debt and equity issuances.

The trouble is that since the oil crash the MLP industry has been in a bear market. Low equity prices have sent costs of equity soaring, forcing many firms to revise their financing plans.

Buckeye Partners has been progressively locked out of the equity market and been forced to rely too heavily on debt to fund its growth. This is why its leverage ratio (debt/EBITDA) has now risen to 5.7.

For context, the average MLP's leverage ratio sits near 4.5, and credit rating agencies usually want to see that ratio at 5.0 or less. As a result, BPL's credit has been downgraded to BBB- which is one level above junk bond status.

If Buckeye gets downgraded to junk (which is a very real risk), then its future borrowing and refinancing costs will likely rise significantly, making profitable growth much harder.

While many MLP have faced challenges from sour investor sentiment on the space, Buckeye's challenges run deeper.

Specifically, the firm's marine oil storage business (about 50% of cash flow) is suffering from declining global oil inventory volumes. Global demand is outstripping supply, thus draining global inventories and lowering utilization rates at its key facilities.

As a result, the company's short to medium-term outlook appears poor, especially since Buckeye only has about $645 million in growth projects planned for 2018 (thus little short-term distributable cash flow growth is expected).

These deteriorating fundamentals are why CEO Clark Smith told analysts on the August 3, 2018, conference call that the MLP is considering drastic changes to its business model and distribution policy:

"This morning we announced that Buckeye has undertaken a comprehensive strategic review of asset portfolio with the financial strategy...we're assessing our capital structure and the potential benefits of transitioning to a self funding model for the equity portion of our growth capital requirements limiting our dependency on public equity market. Our strategy is to evaluate any in our business with strategic options that could drive long-term unitholder value and no option will be off the table in our view... Given the challenges we’re facing in our business and our ability to maintaining our investment grade rating, our distribution policy will be part of the strategic review that I just spoke about."

According to Mr. Clark, the strategic review will be completed in the third quarter of 2018, and during the next earnings release and conference call management will provide its new plan for how to sustainably grow Buckeye going forward.

But what exactly does this mean for BPL investors?

Most importantly, the MLP is worried about losing its investment-grade credit rating and no longer feels confident being so reliant on fickle equity markets to supply it with growth capital.

Thus the mention of a "self funding model" which in the MLP industry means retaining enough cash flow (after paying the distribution) to cover the portion of the growth capex budget that previously was provided by selling new equity (at high enough prices to be profitable).

Self funding business models have become increasingly popular in the MLP industry with midstream operators both big and small transitioning to becoming 100% independent of equity markets for future growth potential.

Notable examples of MLPs or midstream corporations that are currently self funding or have announced plans to transition to such models include:

Magellan Midstream Partners (MMP)

Enterprise Products Partners (EPD)

Enbridge Inc (ENB)

MPLX (MPLX)

Energy Transfer Equity (ETE) - post ETP merger expected to close by end of year

Antero Midstream Partners (AM)

Kinder Morgan (KMI)

The thing to note about self funding business models is that they usually require a distribution coverage ratio of 1.2 to 1.5 in order to generate sufficient retained DCF to replace the equity portion of an MLPs growth capex funding.

With BPL's coverage ratio expected to be about 0.93 for 2018 this means that a major distribution cut would be necessary in order for Buckeye to be able to move to this more sustainable and low-risk funding model.

As a result, it's very possible that the MLP will need to cut its distribution by 40% to 50% in order to raise its coverage ratio to self funding industry norms.

And as management just indicated, that cut could be announced as early as next quarter. This is why the unit price has been so beaten down and the yield has skyrocketed to such high levels.

Closing Thoughts on Buckeye Partners' Distribution Safety

While a 14% yield from an MLP that has never cut its distribution in 32 years may sound appealing at first, it's very important for income investors to recognize the difference between a quality highly undervalued income investment and a "yield trap".

Buckeye Partners falls firmly into the "yield trap" category due to its dangerously low distribution coverage level, continued deterioration in business fundamentals, and increasingly dangerous balance sheet.

Management's latest statements on the earnings conference call indicate that painful but necessary fundamental changes to its business model are likely coming, which includes a potentially large (as high as 50%) distribution cut to allow it to self fund its growth in the future.

Therefore, income investors interested in the MLP industry are likely best off avoiding Buckeye Partners and sticking to much stronger industry blue chips such as Enterprise Products Partners and Magellan Midstream Partners.

These MLPs offer much safer but still generous (and growing) yields that are supported by the strongest credit ratings in the industry. More importantly, each firm is already self funding or moving towards that model while still rewarding income investors with sustainable, growing payouts.