Founded in 1994, GameStop (GME) is a video game, consumer electronics, and wireless services retailer. The company operates 7,200 stores in 14 countries in North America, Europe, and Australia.

GameStop's core business model is selling new and pre-owned video games, as well as accessories like: controllers, gaming headsets, virtual reality products, memory cards.

The company has attempted to pivot from its original business model of reselling video games and video game hardware (still 80% of sales) through physical retail stores, into a rather haphazard focus on the digital content, distribution, and various accessory businesses.

GameStop now markets downloadable content such as video games, network points cards, prepaid digital subscription cards. In addition, the company operates e-commerce sites under the GameStop, EB Games, Micromania, and ThinkGeek brands.

It also runs collectibles stores under the Zing Pop Culture and ThinkGeek brands, and its Spring Mobile subsidiary is an authorized AT&T reseller operating AT&T branded wireless retail stores.

GameStop publishes the Game Informer magazine as well, a print and digital video game publication, and operates Simply Mac, an authorized Apple reseller that sells Apple products.

As you can tell, the company has cast a wide net in an effort to evolve and protect its payout.

Unfortunately, the company's turnaround efforts have not been going well. As a result, GameStop's dividend has been frozen for the last five quarters and could be at risk of a substantial cut.

Let's take a closer look at what has been going on at GameStop to see if its high yield is more likely to be an opportunity for contrarian income investors or a yield trap.

GameStop's Turnaround Plan Isn't Working

GameStop shares have plunged about 75% from their 2013 peak as management has struggled to find a way to offset the looming demise of its core used video game resale business.

This segment boasts rich gross margins of 45% and makes up just over 25% of the company's total sales. That's by far the highest margin business GameStop has. For context, gross margins at the company level are 29%, and sales of new games and video game consoles generate gross margins of just 23% and 7%, respectively.

Management's diversification efforts have been to launch online gaming sites, run a print magazine, open a chain of third-party phone stores, and in 2015 acquire Geeknet for $140 million to turbocharge its collectibles business.

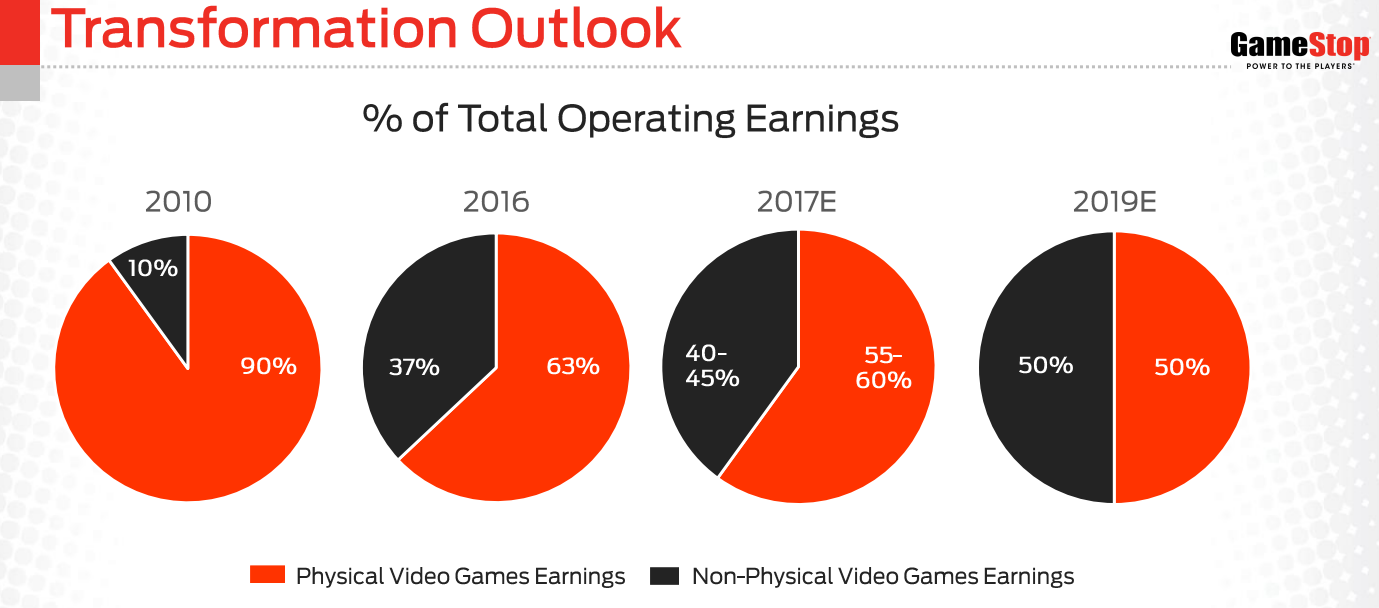

Collectibles are expected to grow into a $16 billion market by 2019 and management believes that this business can be a core future growth driver for the company. GameStop's goal is to achieve $1 billion in collectible revenue by 2019 (company-wide revenue was $9.2 billion in 2017) and diversify its operating earnings from physical video games from 90% in 2010 to 50% in 2019.

Source: GameStop Investor Presentation

Unfortunately, among its various diversification efforts, only collectibles have born fruit. Management is guiding for about a 4% sales decline in 2018, and a 2.5% decrease in same-store sales, which indicates the company's multi-year diversification efforts are failing.

In fact, GameStop is facing falling sales in nearly all of its business lines which led it to report a 40% decline in adjusted EPS in its most recent quarter (despite a much lower tax rate).

Source: GameStop Earnings Presentation

Mike Mauler who took over in February 2018 but resigned for "personal reasons" after just three months, leaving 70-year-old interim CEO and GameStop co-founder Daniel DeMatteo with a major challenge in righting the company's long-term turnaround strategy.

A key component of that is reinvesting in remodeling hundreds of GameStop's stores to focus on a 50/50 mix of video games (its core business) and its fast-growing collectibles business (over 20% annual growth but just 7% of revenue today).

These new store layouts are designed to appeal to more casual gamers including, according to the new CEO, "moms and families". GameStop's latest diversification efforts also include trialing the sale of comic books at 40 of its stores. If that goes well, it will expand comics to more stores later.

While GameStop believes that it can eventually return to both top and bottom line growth, there are plenty of reasons to be skeptical. Especially about the long-term viability of its dividend.

Why GameStop's Dividend Is Likely To Be Cut

Arguably the biggest reason to question GameStop's turnaround plans is because its highest margin business is selling used video game disks. However, the industry is now shifting to a digital subscription business model in which gamers will be subscribers that play games without actually owning them.

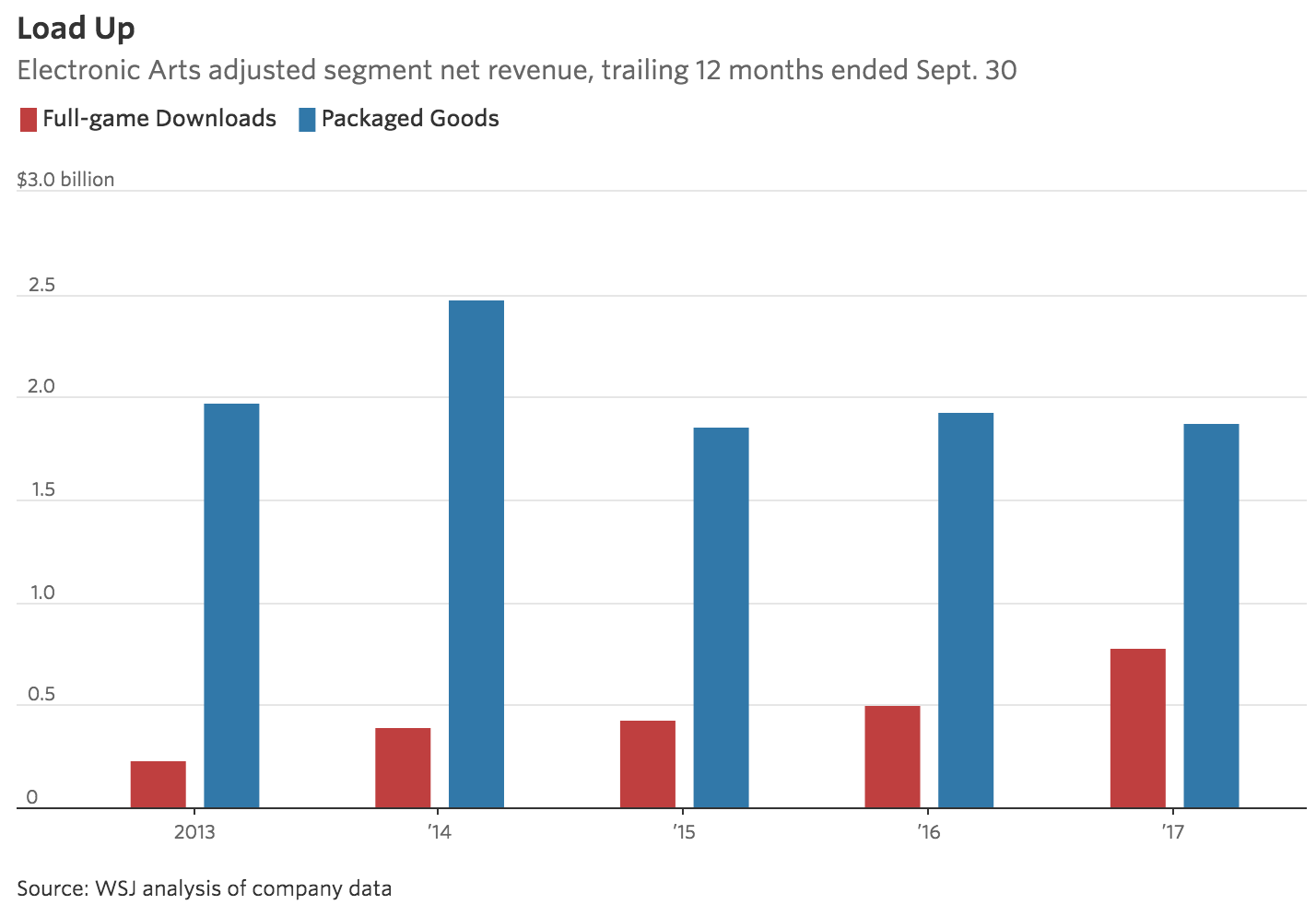

In November 2017 Electronic Arts noted that 36% of its game unit sales took place over digital platforms, up from 30% a year ago, per The Wall Street Journal. As you can see, Electronic Arts' full-game downloads revenue is ramping up while sales of packaged video games are declining as gamers increasingly bypass retail stores such as GameStop.

Source: The Wall Street Journal

In fact, future video game consoles might not use physical disks at all. Therefore, GameStop appears to be setting up to face a Blockbuster-like existential threat to its main source of cash flow.

While GameStop has managed to keep its overall revenue relatively stable (until recently) over the past few years at it attempts to diversify into non-core businesses, the company's profitability has fallen off a cliff.

In fact, earnings have now been declining for six consecutive quarters and management's guidance calls for 2018 earnings to decline for a third straight year.

Operating margin: 7.2% in 2016, now 3%

Net margin: 4.2% in 2016, now 1.5%

Free cash flow margin: 5.2% in 2016, now 0.5%

Meanwhile, revenue from Simply Mac, Spring Mobile, and Cricket Wireless stores has actually been falling at double-digit rates. This is because GameStop has no competitive advantage or pricing power in the wireless accessory business. As a result, in the last two quarters the company has taken about $430 million in write-downs on its technology and collectibles businesses.

As a result of GameStop's struggling diversification efforts, management has announced a "pause on investing in additional new businesses or acquisitions". Rather, the focus will be on cutting costs, boosting customer loyalty, and expanding its customer base to more casual gamers.

However, none of those strategies are likely to overcome the main challenges facing its core business model, which is at real risk of eventually going to zero. Not surprisingly, that spells trouble for the company's dividend.

One of the most important profitability metrics for income investors to focus on is free cash flow. Free cash flow is what's left over after running the business and investing for future growth. It's ultimately what pays a sustainable dividend.

In the past 12 months GameStop, despite recording $9.1 billion in sales, generated just $49 million in free cash flow. But it paid out $156 million in dividends, meaning its free cash flow payout ratio exceeded 300%.

To cover that $107 million shortfall, the company has been draining its cash reserves. However, that isn't a sustainable long-term plan given that GameStop also has over $800 million in long-term debt and just $264 million in remaining cash on the balance sheet.

Management believes the company can achieve $300 million in 2018 free cash flow which would result in a much healthier payout ratio near 50%. However, given that GameStop continues to over promise and under deliver on its results, investors have good reason to be skeptical. That's especially true given the new CEO's focus on remodeling stores to an entirely new format which will require a lot of capital investment.

GameStop's heavy investments into diversifying its business and remodeling hundreds of stores have left it with steadily rising leverage metrics as well. As a result, the company has a junk bond credit rating of BB and average borrowing costs of about 7%.

In a rising interest rate environment GameStop's deteriorating balance sheet, coupled with its weak free cash flow generation, is not just threatening the companies turnaround efforts but potentially the long-term viability of the business itself.

Further lending credence to bearish expectations is the fact that on June 19, 2018, GameStop confirmed a Reuters story that it had retained financial advisor firm Sycamore Partners to advise it on selling the company. Sycamore is famous for its "cigar butt" ability to find private equity buyers for struggling retailers including orchestrating earlier sales of Talbots, Anne Klein, Hot Topic, and Nine West.

The fact that management is considering a sale of the company tells us that its confidence in the struggling turnaround is likely flagging. And if GameStop is bought out, there is no guarantee that it will be for a high enough price to justify taking the risk of owning this unsafe income investment.

Closing Thoughts on GameStop

GameStop's turnaround plan has been unable to compensate for the secular decline in its core used video game disk business. Worse yet, management's questionable diversification efforts into businesses with little to no moat have come at the cost of falling margins and slumping sales.

As a result, the company's dividend is not well covered by GameStop's free cash flow, especially considering the firm's rising leverage ratios, high borrowing costs, and need to remodel many of its brick-and-mortar stores.

With the rise in digital video game downloads only accelerating, GameStop is racing to avoid technological disruption turning it into another Blockbuster Video. And even if it manages to survive as a company, the dividend is likely living on borrowed time.

Simply put, the company's chance of long-term survival would increase if it redirected most or all of its $156 million in annual dividend payments to more pressing issues, such as its need to reinvent itself and improve its balance sheet.

When combined with management's poor execution and high rate of executive turnover in recent years, GameStop is a high-risk dividend stock that's not appropriate for conservative income investors.