We reviewed Qualcomm's dividend safety and legal risks in February 2019 here.

Qualcomm (QCOM) was founded in 1985 and is a leader in the development and commercialization of digital communication technologies called CDMA (Code Division Multiple Access) and OFDMA (Orthogonal Frequency Division Multiple Access), including LTE (Long Term Evolution).

The company owns significant intellectual property applicable to products that implement any version of CDMA and OFDMA, including over 46,000 patents. Any company in the mobile communications industry trying to develop, manufacture, or sell products using CDMA and/or LTE standards usually requires a patent license from Qualcomm.

The company also develops other technologies used in handsets and tablets, including certain audio and video technologies, advanced WLAN functionality, and memory controllers.

The main factor that drives the company’s performance is cell phone penetration, particularly with smartphones (where it is the leading phone modem maker). For example, about 1.8 billion smartphones were sold around the world in 2018, and Qualcomm's chips were in 804 million of them, representing 45% global market share.

Here's a look at a chip from Qualcomm's popular Snapdragon series of smartphone chips.

Source: Qualcomm

Qualcomm operates through three business segments: Qualcomm CDMA Technologies (QCT), Qualcomm Technology Licensing (QTL), and Qualcomm Strategic Initiatives (QSI).

QCT (76% of revenue, 45% of income): develops new chips and software packages for CDMA and upcoming 5G-based smartphones. This includes the company's Snapdragon series of smartphone chips, which are found in most of today's phones, ranging from the low end (200 series) to premium phones like the Samsung Galaxy and Note product lines (800 series).

QTL (23% of revenue, 54% of income): the company's licensing business, in which smartphone manufacturers pay royalties Qualcomm's 3G and 4G LTE patents. Typically this amounts to 3% to 5% of the wholesale cost of the phone.

QSI (1% of revenue, 1% of income): invests in early-stage companies in various industries, including automotive, internet of things (IoT), mobile, data center, and healthcare.

While the vast majority of Qualcomm's sales come from QCT, the company's profit margins are far higher in its licensing business (QTL) due to the lack of manufacturing and overhead costs. In fact, in 2018 pre-tax margins in QTL were 68% compared to just 17% for QTC.

However, QTL's 2018 profitability was far lower than usual due to various legal issues that segment is facing (more in the key risks section) that has resulted in revenue withholdings and legal expenses. In recent years QTL has accounted for 80% of the company's pre-tax profits.

Meanwhile, QSI has a negligible amount of revenue and generates essentially no profit on its own. That's because its role isn't to be a direct money maker but rather an incubator for new technologies that Qualcomm is working on perfecting and bringing to market.

Qualcomm has raised its dividend for 15 consecutive years, recording growth each year since it began making payouts in 2003.

Business Analysis

Qualcomm's impressive long-term growth was fueled by the rise of global connected internet devices, which numbered less than 60 million in 1994 but reached 7.9 billion by the end of September 2018, according to GSMA Intelligence.

The company's dominance has traditionally been in its near monopoly on 3G (voice) and 4G (data) wireless patents. Qualcomm also holds numerous non-essential patents pertaining to how smartphones operate, manage power, and process audio and video.

At the end of September 2018, 69% of all global mobile connections were either 3G or 4G, demonstrating the ubiquitous nature of many of Qualcomm's technologies.

Source: Qualcomm Investor Presentation

In 2018 Qualcomm invested $5.6 billion, or 25% of its revenue, in R&D to continue innovating new phone chip technologies. This intellectual property has allowed Qualcomm to sign numerous lucrative licensing deals in the past with pre-tax profit margins as high as 85%.

When combined with the fast growth of smartphones around the world, Qualcomm quickly became a wildly profitable and fast-growing company. In fact, Qualcomm's free cash flow margin has usually been above 25%.

This has allowed the company to be very generous with its cash returns, including substantial share buybacks and a fast-growing dividend that has compounded at a double-digit annual pace over the long term.

Source: Qualcomm Investor Presentation

Qualcomm is also a leading chip designer, selling its "systems on a chip," or SOC, to various phone makers around the world. This is where much of the company's R&D spending goes, in order to continually upgrade its offerings for the highly competitive and fast-changing world of consumer electronics.

For example, the company's premier phone SOC is the new Snapdragon 855, which includes some of the industry's top performance specs and is going to power most of the high-end smartphones on sale in the U.S. in 2019.

In February 2019 Qualcomm announced that the next generation SOC (possibly called Snapdragon 865 and coming in 2020 phones) will be the first to not just boost overall specs, but also include a built-in 5G modem. Until now the company's modems have not been bundled with its SOCs, meaning this new offering will be a lower cost option for smartphone makers and potentially help keep QTL growth strong in the future.

According to Cristiano Amon, the head of Qualcomm's chip business, these more advanced 5G chips are critical to the company maintaining or even improving its pricing power (moat) in QTC as technology eventually transitions to 5G in the years ahead.

Source: Qualcomm Investor Presentation

Qualcomm's 5G chips aren't just about smartphones, but also include various Internet of Things, or IoT, designs in large markets such as automotive. According to ARM Holdings, a leading chip designer, by 2035 IoT has potential to connect 1 trillion total devices to the internet using 5G networks, showing the significant growth potential Qualcomm potentially has in QTC.

While the company's IP dominance has waned in recent years (it's 3G patents are stronger than its 4G patents), Qualcomm is still likely to benefit from a strong royalty stream for the next 10 to 20 years. That's because even as wireless technology evolves and advances, phone makers still need to ensure backward compatibility for long periods of time.

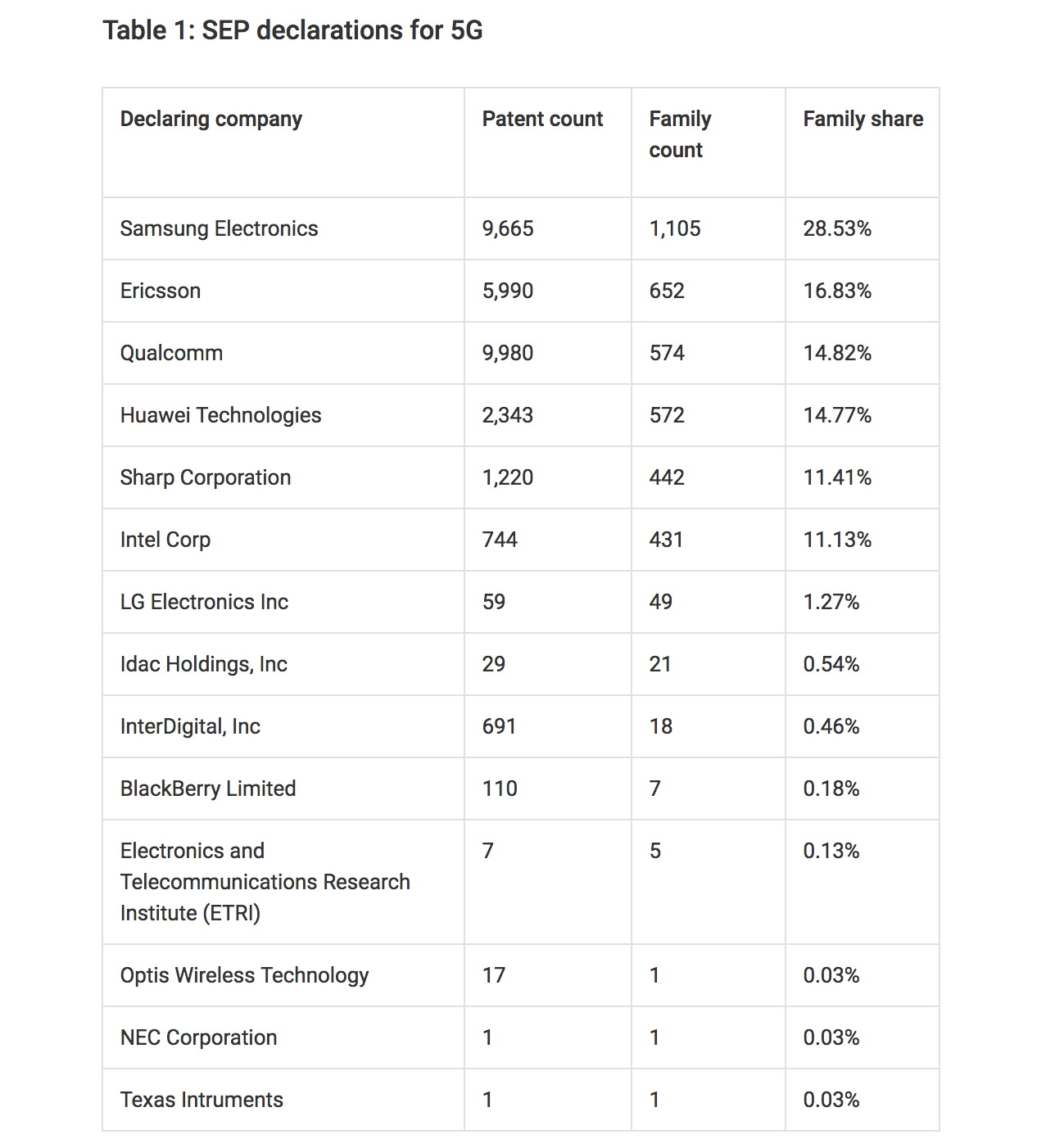

And though Qualcomm's lead in 5G patents isn't nearly as strong as it was in 3G and 4G, it still owns about 15% of the total declared 5G Standard Essential Patents, or SEPs, putting it at No. 3 of any tech company.

Source: IAM Media

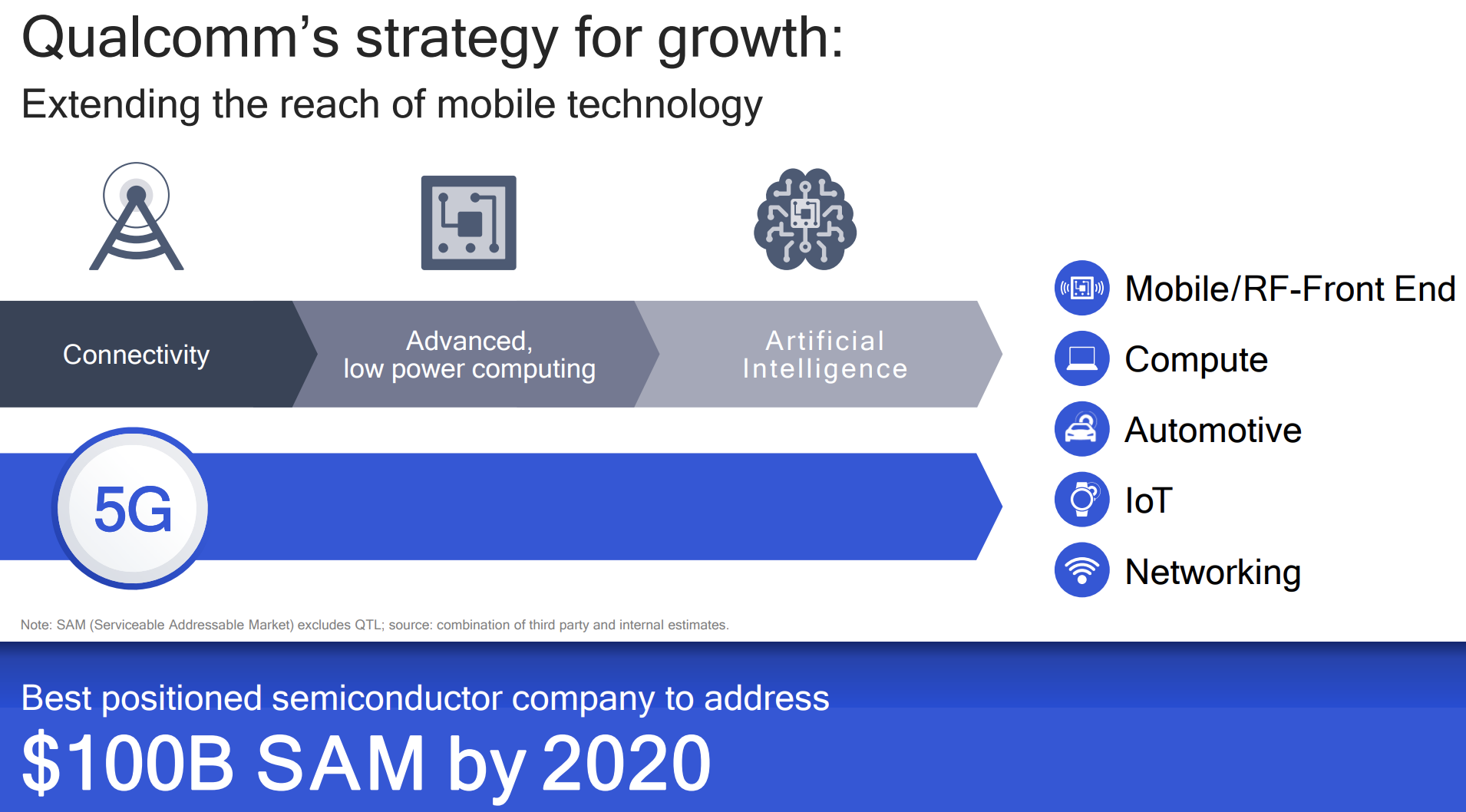

The company estimates that even after its attempted 2018 merger with NXP Semiconductor (NXPI) fell through, its addressable market by 2020 will be about $100 billion, representing a potentially long growth runway (it has about 22% market share based on 2018 revenue).

Source: Qualcomm Investor Presentation

The NXP deal was designed to help vault Qualcomm into a dominant position in the automotive market since that Dutch semiconductor company had 14 of the 15 biggest global automakers as its customers. With modern cars continuing to use more electronics, Qualcomm saw this acquisition as a chance to diversify away from its troubled QTL business.

However, that deal was quashed by Chinese regulators dragging their feet on the final regulatory approval needed for the merger. Going forward, Qualcomm will still benefit from more 5G-enabled chips in cars, but will have to win these contracts without the deep industry connections NXP enjoys.

When the deal was killed, Qualcomm announced it would cut costs by $1 billionby the end of fiscal 2019 and use $30 billion that had been set aside for the deal to repurchase shares.

That massive buyback plan was part of an effort to discourage its shareholders from voting in favor of Broadcom's (AVGO) hostile takeover in which it offered Qualcomm shareholders $70 per share in cash and stock. That mega-deal was ultimately blocked by the U.S. government over concerns about how it might affect 5G tech development.

Overall, Qualcomm has always been, and continues to be, an innovative technology leader for some of the most important industries of the future. However, before getting too excited, there are some major risks involved with Qualcomm.

Key Risks

Qualcomm faces major threats on two important fronts.

First, the firm's lucrative QTL licensing agreements have been under fire from regulators around the world. You can read our in-depth February 2019 note hereto get a deeper look at Qualcomm's legal issues, but here's a brief summary.

In recent years, regulators in China, South Korea, Taiwan, and the EU have fined the company a total of $3.8 billion over its royalty payments, and China said that Qualcomm's 3% to 5% royalties could only be applied to 65% of a phone's wholesale price. The company is appealing the $1.2 billion EU fine but now the U.S. government is also going after Qualcomm's QTL business on several fronts.

Meanwhile, major former customers like Apple (AAPL) have withheld $7 billion in royalties over the years as they battle the company in courts arguing that it's been violating anti-trust law. In fiscal 2018 the company says QTL saw $600 million in revenue withheld due to these ongoing legal issues.

The biggest risk to the company's QTL business is the court case in California (completed in early 2019), in which the FTC argued that the company's forcing QTC customers to also sign licensing agreements was an anti-trust violation.

The much higher legal expenses, combined with numerous licensees withholding revenue while court cases are pending, has already boosted the firm's free cash flow payout ratio to dangerous levels.

Source: Simply Safe Dividends

Some investors have said they expect the court ruling to force Qualcomm to adopt the fair, reasonable, and non-discriminatory, or FRAND, licensing practices, which could potentially cut QTL earnings in half, force a large dividend cut, and send the share price crashing to as low as $21.

That is certainly the worst-case scenario for Qualcomm, and management and other analysts, such as Morningstar senior equity analyst Abhinav Davuluri, don't think that the company is facing such a thesis-breaking outcome.

"After reviewing transcripts of the closing arguments and the trial itself, we reiterate our view that we expect Qualcomm to maintain its licensing business model. CEO Steve Mollenkopf also noted that management expects to reach a resolution with Apple through settlement or litigation in 2019 as additional court rulings in the U.S., China, and Germany come to fruition." – Abhinav Davuluri

With most of the legal cases set to be resolved (one way or another) in 2019, Qualcomm might very well be able to quickly return its free cash flow payout ratio to a sustainable level. In fact, analysts expect Qualcomm's payout ratio to improve to around 70% in 2019 and 2020 while also allowing management to increase the dividend between 4% and 7% both years, according to data from FactSet.

Basically, Qualcomm's largest profit driver by far is facing major legal and regulatory uncertainty that make such forecasts very murky. In a worst-case outcome, a dividend cut or at least a freeze would not be out of the question, however unlikely such a scenario might be.

Until we get further clarification on what the future of QTL's licensing agreements will look like, Qualcomm's Dividend Safety Score will remain in our Borderline Safe risk bucket.

What about Qualcomm's QCT division (close to 80% of sales), which has enjoyed strong double-digit growth in the past due to rising global smartphone sales and that will likely be its key revenue growth driver in the future? There are potential risks to consider here as well.

For example, in recent years, while Qualcomm's QTC sales and earnings have remained strong and rising, the number of actual chips sold and its overall market share for smartphone chips have actually declined.

Source: Qualcomm Investor Presentation

The problem for Qualcomm stems from the increasingly commoditized nature of smartphones. For example, analysts currently estimate that only three phone makers in the world are actually profitable when it comes to hardware: Apple, Samsung, and Huawei. The rest are running at a loss (and thus arguing that Qualcomm's royalty based on the entire phone is unfair when they are merely licensing wireless components).

These three companies have all begun moving their wireless chip designs in-house, meaning designing and manufacturing their own chips. Thus Qualcomm has faced declining demand from its largest customers, as well as increased competition from low-cost wireless chip makers such as Himax Technologies (HIMX).

While Qualcomm's larger R&D budget and decades of expertise in wireless chips give it a technological edge over rivals like Himax, at the end of the day cost could prove the driving factor for many smaller phone makers struggling to stay in business.

After all, as technology advances, wireless chips become "good enough" for low to medium end phones. Therefore, Qualcomm's market share and pricing power could come under increasing pressure. That's especially true given that one of Qualcomm's largest customers, Samsung, also declared the highest number of 5G standard essential patents and thus might look to replace Qualcomm as a component vendor in the future.

Basically, Qualcomm's status as a reliable dividend growth blue-chip is currently up in the air and hinges on the uncertain outcomes of legal battles that will likely be resolved this year. If the company comes out victorious (as management predicts), then Qualcomm will probably have proven to be a solid high-yield investment.

However, if it loses its legal and regulatory fights, then shares might be set to plunge hard as the dividend's safety profile takes a clearer hit.

Closing Thoughts on Qualcomm

Qualcomm has proven itself to be a highly innovative and dominant force in the world of tech for decades. Its industry-leading intellectual property has made QTL a major cash cow for the firm, helping the company historically serve as a fast-growing tech stock and appealing income growth investment.

However, it is looking more and more likely that Qualcomm's best days are behind it. That's because its IP-driven QTL business is under siege from both companies and governments around the world, resulting in multibillion-dollar fines, a seemingly never-ending stream of litigation, and collapsing revenue (from withheld royalties) and profitability. And if the most recent FTC lawsuit goes against it, QTL's profitability might potentially fall drastically, putting the current dividend at risk of a cut.

Meanwhile, the QTC business, while still growing, is facing ever-larger competition from giant and very well-capitalized phone makers who are increasingly taking their integrated chip design needs in-house. This potentially puts the company's pricing power on future chips at risk.

Given all of this uncertainty, as well as the industry's sheer complexity the rapid pace of change in the tech sector in general, more conservative income growth investors are probably better off passing on Qualcomm. The concluding remarks from our February 2019 note reviewing Qualcomm's dividend safety remain true:

Given the binary nature and unpredictability of trial outcomes, including the possibility of a settlement with U.S. regulators, Qualcomm's increasingly wide range of potential outcomes seems to make the stock a less ideal option for conservative income investors whose top priority is a safe dividend in all environments (and legal outcomes).

At the same time, Qualcomm remains confident that it will prevail in court. That's why in 2019 management and analysts expect to see a permanent resolution to the firm's legal woes that could not only result in a substantial infusion of cash (back payments on withheld royalties) but also the elimination of its biggest risk and stock price overhang (litigation damaging QTL's economics).

As long as the worst-case scenario doesn't actually occur, the company's intellectual property, including a strong position in 5G wireless technology, means income investors will likely continue enjoying a safe and growing dividend going forward. However, as conservative investors our preference is to invest in simpler businesses whose futures don't hinge on low-probability, high-severity events.