Founded in 1983 as SBC Communications (the company bought AT&T in 2005 and adopted the more famous moniker), AT&T is a telecom and media conglomerate that operates four business segments:

Communications (77% of revenue, 79% of operating income): provides wireless and wireline (phone and internet) services to consumers and businesses, as well as paid video (streaming, U-verse, DirecTV). Wireless services account for just over 50% of AT&T's total operating income. Pay-TV and voice services, two areas in secular decline, represent less than 15% of company-wide profits.

WarnerMedia (18% of revenue, 20% of operating income): consists of all Time Warner assets, including Turner Cable TV channels, HBO, and Warner Brothers studios. AT&T acquired Time Warner for $85 billion in June 2018.

Latin America (4% of revenue, -2% of operating income): offers mobile services and satellite TV subscriptions throughout Latin America.

Xandr (1% of revenue, 3% of operating income): AT&T's new data analytics and advertising business.

AT&T has raised its dividend for 35 consecutive years, making it a dividend aristocrat.

Business Analysis AT&T has managed to pay growing dividends for more than 30 consecutive years due largely to the capital intensive nature of the industries it operates in, which creates high barriers to entry.

For example, between 2012 and 2018 AT&T spent more than $150 billion on maintaining, upgrading, and expanding its wireless and wireline networks, including over $20 billion in 2018 (about 13% of revenue).

Few other companies can afford to compete with AT&T on a national scale. Only Verizon (VZ), T-Mobile, and to a lesser extent Sprint (S) have the resources to operate networks that offer similar levels of speed and connectivity.

To make matters even more challenging for potential new entrants, most of AT&T’s markets are very mature. Approximately 96% of U.S. adults own a cellphone, for example. The number of total wireless subscribers simply does not have much room to grow.

Therefore, it would be almost impossible for new entrants to accumulate the critical mass of subscribers needed to cover the huge cost of building out a cable, wireless, or satellite network.

In addition to covering network costs, AT&T’s scale allows it to invest heavily in marketing. Between its company-owned stores and distributor network, AT&T has around 10,000 distribution locations to reach customers. The telecom giant also enjoys strong purchasing power for network equipment and TV content. Smaller players and new entrants are once again at a disadvantage.

Barring a major change in technology, it seems very difficult to uproot AT&T. It’s much easier to maintain a large subscriber base in a mature market than it is to build a new base from scratch. Management continues making strategic moves to help ensure that remains the case.

For example, take AT&T’s wireless division, which is its most consumer-facing business and generates over 50% of firm-wide operating income. Despite T-Mobile's price war in recent years, AT&T has attempted to maintain market share and stabilize average revenue per user by bundling its wireless services with the TV services offered by DirecTV, which it acquired for $67 billion in 2015.

In 2018, AT&T added to its collection of telecom and entertainment assets when it paid $85 billion to acquire Time Warner, a media powerhouse. Management desired Time Warner's vast content library, which it can leverage to launch new streaming services while strengthening AT&T's other offerings.

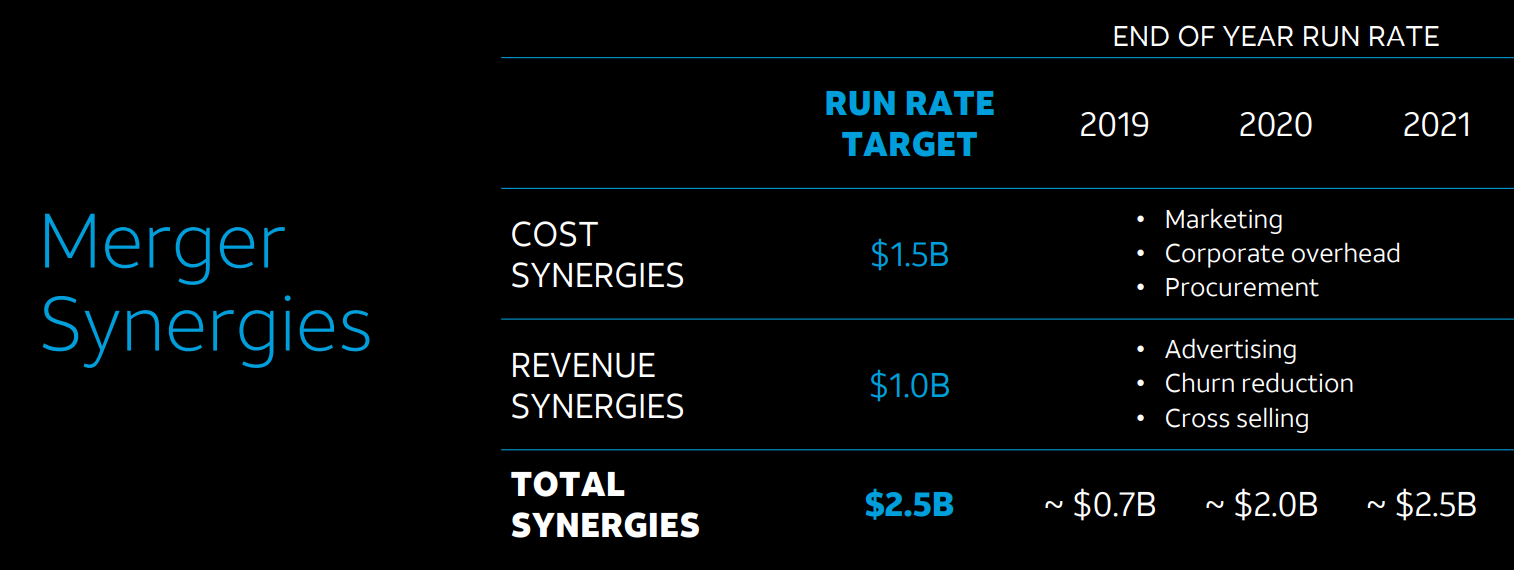

Combining more bundling (to reduce mobile churn and stabilize its pay-TV business) with cost-cutting and cross-selling initiatives between its wireless, TV, and content divisions, AT&T believes it can deliver $2.5 billion in synergies by 2021. For context, the company expects to generate $28 billion in 2019 free cash flow.

Source: AT&T Investor Presenation

While Time Warner added faster-growing content and digital advertising businesses, the acquisition also gave AT&T the highest corporate debt load in America. The company maintains an investment-graded credit rating, but reducing leverage is management's top priority.

By using all discretionary cash flow to pay down debt and selling off non-core assets to raise even more cash for debt reduction, management hopes the firm's leverage ratio will return to its historical norm by 2022. Rapid deleveraging is important because AT&T is going to need to spend a lot on 5G expansion to maintain its moat in wireless, which remains its most stable source of recurring cash flow (and supports its dividend).

Even despite some challenges in the pay-TV market, which represents less than 15% of its profits, AT&T's well-diversified operations have helped the company remain on track to meet its goals while also paying a generous dividend. If the company's leverage profile improves and management realizes success integrating Time Warner, AT&T's Dividend Safety Score will likely be upgraded.

Overall, AT&T seems like a business that will remain relevant for many years. The firm enjoys a solid economic moat due to its ability to provide customers with their video, data, content, and communication needs anytime, anywhere, and on any device. Few companies have the financial firepower and brand strength to effectively compete.

However, the telecom and media industries, as well as consumer preferences, are constantly evolving, making incremental earnings growth more challenging for the large incumbents.

Key Risks While AT&T has historically been a relatively low-risk stock, there are nonetheless several major risks to be aware of.

Given the firm's need to reduce debt following its acquisitions of DirecTV and Time Warner, it's critical that AT&T's business generates the free cash flow that management expects. However, AT&T’s growth profile faces challenges because of the saturated nature of the markets it operates in.

On the wireless side, smartphone saturation and the rise of T-Mobile have intensified competition for existing subscribers. For example, in recent years the major players have been forced to offer unlimited data plans to maintain their subscriber bases.

While price stabilization is finally occurring, a potential merger between T-Mobile and Sprint could create a stronger rival to AT&T and Verizon. On the other hand, it also reduces the number of major carriers from four to three. The point is that AT&T depends on a healthy U.S. wireless market, especially as it invests heavily in 5G, so it's important that the profitability of this business remains stable as the competitive landscape evolves.

Another concern is the issue of cord cutting, which has bedeviled AT&T for years. The rise of over-the-top streaming services is a major reason why DirecTV has lost nearly 10% of its subscribers since AT&T bought the business in 2015.

As more of the population embraces video streaming services, AT&T's satellite TV business will likely continue shedding subscribers. With Time Warner's content under its belt, the company is trying to stabilize its subscriber base by launching its own streaming services. However, this is a crowded field filled with content experts such as Netflix, Disney, and Amazon.

As a result, it may be more difficult than management expects to deliver on AT&T's long-term growth plans with its new media business. Investors should monitor the company's progress here closely to ensure it doesn't prevent AT&T's overall earnings and free cash flow from moderately growing.

After all, AT&T's management doesn't exactly have a solid track record of making wise capital allocation decisions that have created shareholder value. Randall Stephenson has served as AT&T's CEO since May 2007, and the company's stock price is actually lower today than when he took the top job.

Mr. Stephenson's reputation has taken a hit after he significantly overpaid for DirecTV just as the business was peaking. His record also includes multibillion-dollar purchases for two Mexican wireless companies (AT&T's Latin America segment is losing money) and ponying up for Time Warner.

It remains to be seen if these major chess moves to transform AT&T into a telecom and media conglomerate will ultimately create value for shareholders or prove to have been foolish debt-fueled empire-building.

Given the firm's stretched balance sheet and sizable dividend, it’s critical that AT&T is able to leverage its various telecom and media assets to deliver moderately growing free cash flow in the years ahead. AT&T's dividend appears to remain secure for now, but its cash flow generation needs to be watched to make sure management's plans continue playing out as expected.

Closing Thoughts on AT&T AT&T has taken a number of bold steps in recent years to proactively take on changing industry conditions across wireless, video, and media markets.

It will probably take at least several years to determine just how savvy these massive capital allocation bets actually are. For now, AT&T remains a mature cash cow that is a reliable source of income over at least the short to medium term.

However, any dividend investor considering AT&T must understand and accept the risks that come with the company’s significant debt levels and complex merger integration work as its business strategy evolves.