S&P Global (SPGI): An Impressive Dividend Aristocrat With Double-Digit Payout Growth Potential

Founded in 1888 and formerly known as McGraw Hill Financial, S&P Global (SPGI) provides independent ratings, benchmarks, analytics, and data to the capital and commodity markets in 31 countries under several well-known brands including: Standard & Poor’s (S&P), S&P Capital IQ, Platts, and SNL.

In 2017, S&P Global rated about $4 trillion in corporate and government debt, and the company operates in three business segments:

Ratings: provides credit ratings, research and analytics, information, and benchmarks to investors and debt issuers. S&P Ratings has been providing important information for over 150 years to help investors make better decisions and improve companies’ access to capital markets.

Market & Commodity Intelligence: offers multi-asset-class data and research and analytical capabilities. Capital IQ, SNL, and Platts are included in this segment.

S&P Dow Jones Indices: provides global indices that investment advisors, wealth managers, and institutional investors use to benchmark over $12 trillion of assets. This segment makes money from exchange traded funds (ETFs), derivatives, and index-related licensing fees (e.g. the S&P and Dow Jones names). It is well-positioned to grow from the trend toward passive investing.

Source: S&P Global Investor Presentation

As you can see, most of the company's revenue is from rating debt and providing market data. However, the firm's highest-margin businesses are in its S&P Dow Jones Indices segment:

Data (Market Intelligence + Platts): 35% adjusted operating margin

Ratings: 55% adjusted operating margin

Indices: 70% adjusted operating margin

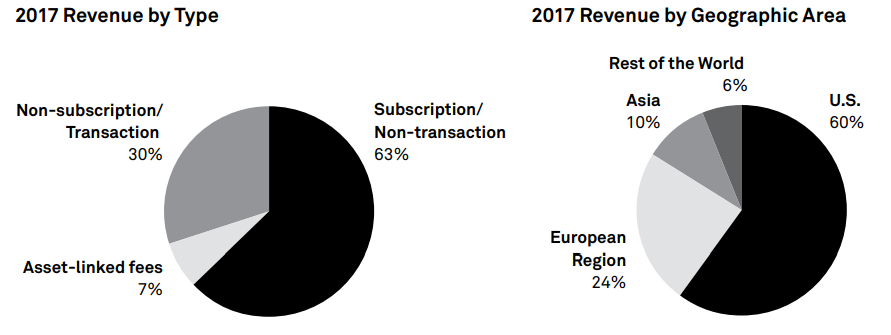

The company derives its revenues from a mix of subscription fees, as well as various corporate, insurance, and government clients around the world. About 63% of the company's sales are in the form of recurring subscription revenue, creating highly stable cash flow.

S&P generates 60% of its sales from the U.S., with 40% coming from overseas. This includes fast-growing emerging markets such as China.

Source: S&P Global Annual Report

With 32 straight years of dividend increases, S&P Global is a dividend aristocrat.

Business Analysis

S&P Global primarily benefits from its strong brand recognition and the mission-critical nature of its data. After all, participants in financial markets and executives in commercial markets need extremely reliable, accurate, and trustworthy information to make critical business and investment decisions.

The company’s primary brand, Standard & Poor’s, has been around since 1860, establishing long-lasting customer relationships built on trust and quality. McGraw Hill purchased S&P in 1966 and hasn’t looked back.

In addition to hard-to-replicate brands built on reputation and trust, S&P’s business benefits from the U.S. Credit Rating Agency Reform Act of 2006 that requires financial market participants to use nationally recognized statistical rating organizations (NRSROs).

These are the only ratings agencies that the U.S. Securities and Exchange Commission permits other financial companies to depend on for regulatory purposes.

There were only 10 NRSROs today, which limits competition and helps S&P maintain strong market share and profitability.

Registration with the government is very costly and difficult, and new players have no reputation built up, which keeps barriers to entry high for the company’s S&P Ratings segment.

As a result, in its bond rating segment, S&P really only competes with Moody’s (MCO) and Fitch, which collectively enjoy 95% market share in this large and highly lucrative business.

And despite a major black eye being created by the financial crisis, when rating agencies labeled toxic mortgage backed assets AAA, rating agency moats have only gotten wider thanks to increased regulations such as Dodd-Frank.

This is because more regulations mean higher compliance costs. For example, according to Morningstar, prior to the financial crisis S&P had $35 million in annual compliance costs.

Since then, the annual cost of complying with many new and complex regulations have soared to $100 million per year. While S&P's enormous revenue stream means that compliance costs make up just 1.6% of it revenue, smaller rivals see these regulatory costs eat into far more of their revenues. This hampers their ability to grow and compete with the industry's dominant players.

In addition to regulations, the industry's oligopoly is due to the fact that bond ratings, which tell investors the risk that a company or government will default on its debt, are based on highly specialized and copious amounts of data.

For example, S&P’s letter grades for debt are derived from over 100 years of proprietary data and algorithms, allowing S&P's statisticians to more accurately develop risk models. It’s almost impossible for an unproven upstart to break into the market and steal significant market share from the entrenched three giants in the industry.

The credit ratings issued by S&P are used by credit markets all over the world to decide whether or not to lend to a company or government and at what interest rate. In other words, S&P's credit rating business represents an essential service without which the modern financial system simply couldn't function.

Ultimately, it's this intellectual property (proprietary data sets) that has enabled S&P to become the dominant player (almost 50% market share) in the roughly $10 trillion per year global corporate debt market.

And since global debt levels are usually rising over time (growing in line with GDP), this means extremely stable business for S&P. Typically S&P charges 0.1% of the debt offering to rate a bond offering. That might not sound like much, but remember that the global debt market is enormous.

Source: S&P Global Investor Presentation

Corporations frequently issue $1 billion bonds (generating a $1 million fee for S&P), and governments frequently sell $10 billion bonds ($10 million fee). While this isn't recurring revenue, debt is usually refinanced rather than paid off.

As a result, companies need to keep returning to S&P to help service their long-term debt needs. And since a rating requires deep knowledge of a company or government's finances, clients are unlikely to switch rating agencies because it would take significantly longer to get a rating (and thus obtain financing).

Over the decades, S&P has branched out beyond credit ratings and added an equally lucrative business model centered around data collection, analysis, and curation. For example, Platts is an industry leader in providing accurate and up-to-data information pertaining to various commodity markets such as agriculture, coal, oil & gas, and metals.

Options and futures markets often link to Platts data, meaning that clients are very unlikely to risk disrupting their business by cancelling their data subscriptions. In other words, S&P is a key leader in providing businesses around the world with the data they need to make smart investment decisions to grow their top and bottom lines.

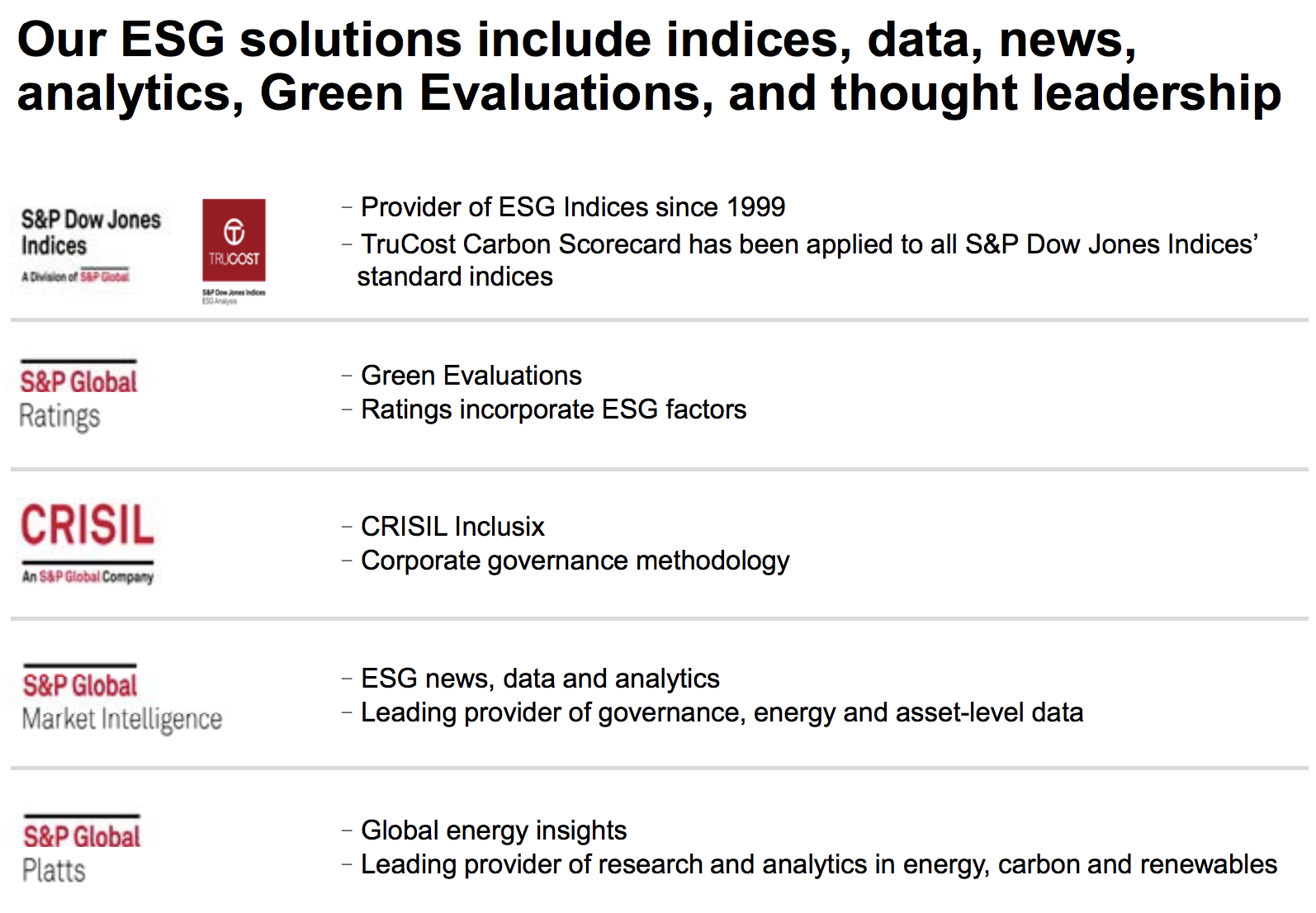

S&P is also a leader in providing data about a company's environmental footprint, social responsibility, and corporate governance. In recent years various large institutions (sovereign wealth funds, pensions, asset managers) have become more interested in aligning their investment goals with social responsibility.

Source: S&P Global Investor Presentation

Thanks to the high quality and essential nature of all this data, S&P's subscription services (SNL, Platts, Capital IQ) have 90% retention rates. Recurring subscriptions help smooth out results and continue delivering free cash flow when the company’s transaction-based revenue (e.g. bond issuance) takes a dip.

Meanwhile, the company's S&P Dow Jones Indices segment is perhaps the most lucrative of all because the company licenses its name to ETFs like the S&P 500 Trust ETF (SPY). With over $250 billion in assets under management, this is the world's largest exchange traded fund.

S&P gets $600,000 per year plus 0.03% of assets under management. This means that over the next year S&P will likely collect about $80 million in licensing fees from this one ETF alone. Other asset managers running ETFs also pay about 0.03% of AUM to use its benchmarks.

Not only are passive index funds becoming more popular over time, but S&P's market share is also increasing. For example, in 2003 about 35% of the assets in index funds were benchmarked off S&P indices. In 2016 that figure had increased to 55% (approximately 20% annual growth in S&P index-linked AUM).

S&P's reputation and brand is so strong that despite its steep licensing fees, its highest margin business is likely to keep growing quickly for the foreseeable future. In the first quarter of 2018, approximately 14% of the company's revenue came from this lucrative asset-indexed source.

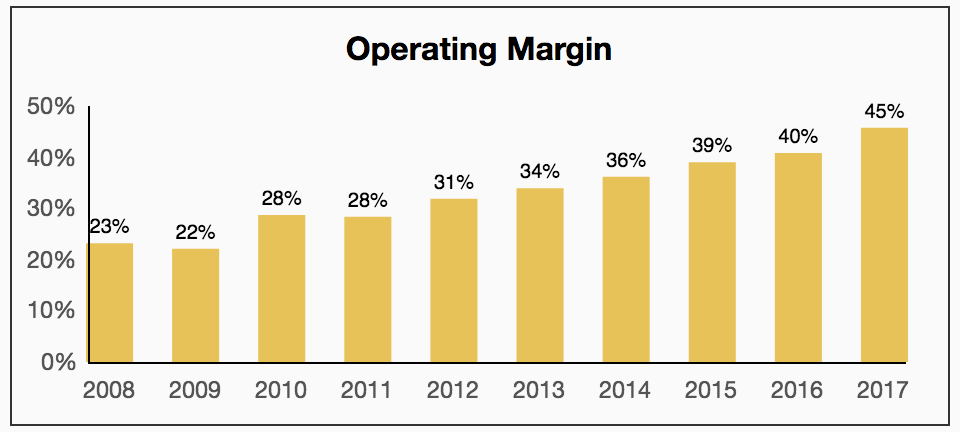

However, S&P's other segment's are also incredibly profitable. No business unit has operating margins under 30%, and profitability has been rising steadily over time.

Source: Simply Safe Dividends

Simply put, S&P operates an incredibly scalable business. The firm can add clients and generate revenue far faster than it needs to expand its overhead (such as employees). This allows it to amortize its fixed costs over an ever-expanding stream of revenue.

S&P's excellent profitability also supports the firm's financial flexibility. Management's stated goal is to maintain a strong balance sheet (debt/Adjusted EBITDA ratio of 2.25 or below) and return 75% of annual free cash flow to shareholders via dividends and buybacks.

This means that over the long term the company will retain about 25% of free cash flow to fund its long-term growth efforts. Those efforts are focused on a few key areas:

Expanding its operations in China (massive debt rating market there)

Expanding Dow Jones Indices to include smart beta (factor investing) and socially responsible products

Investing in bolt-on acquisitions to increase its data flow from various industries (enhance its Market Intelligence and Platts segments)

Continue improving its Market Intelligence platform user interface to make it easier to use and enhance customer retention

S&P often makes small bolt-on acquisitions to augment its data services and also occasionally makes larger strategic acquisitions like the 2015 purchase of SNL Financial for $2.2 billion.

SNL is a major news and data services provider that serves the financial, real estate, energy, media, and metals & mining sectors. This deal helped S&P offer a more compelling bundle of services to its existing customers. S&P also has plenty of opportunity to expand SNL’s services overseas (over 90% of its revenue was from the Americas at the time of the acquisition). All told, between 2015 and 2017 S&P acquired full or partial stakes in 11 companies for about $2.7 billion).

S&P's expanding margins, share buybacks, and exposure to several favorable trends (index investing, corporate debt issuance) have enabled the firm to record double-digit earnings growth in each of the last seven years.

S&P seems likely to continue this trend, which should fuel double-digit dividend growth as well. The firm should benefit as it expands and improves its portfolio of mission-critical financial assets that increase switching costs, generate higher deal values, scale easily, and can be cross-sold to existing customers,

However, there are several risks the company will have to face in the coming years that could result in slower growth.

Key Risks

S&P faces several main risks going forward.

First, its greatest competitive advantage in its largest business segment, debt rating, is dependent on the company’s ongoing credibility and the trust its brand carries in the world of high finance.

As we saw during the financial crisis, when numerous AAA-rated mortgage backed securities proved to be worthless (and nearly destroyed the global financial sector), S&P can and has been wrong before.

This means that another financial crisis, especially one in which S&P-graded debt is the primary destructive catalyst, could harm S&P’s brand, and thus its market share and pricing power.

Normally a recession isn't going to drastically reduce the firm's sales because its clients still need to have their debt rated (to refinance existing loans), as well as data to make investing decisions.

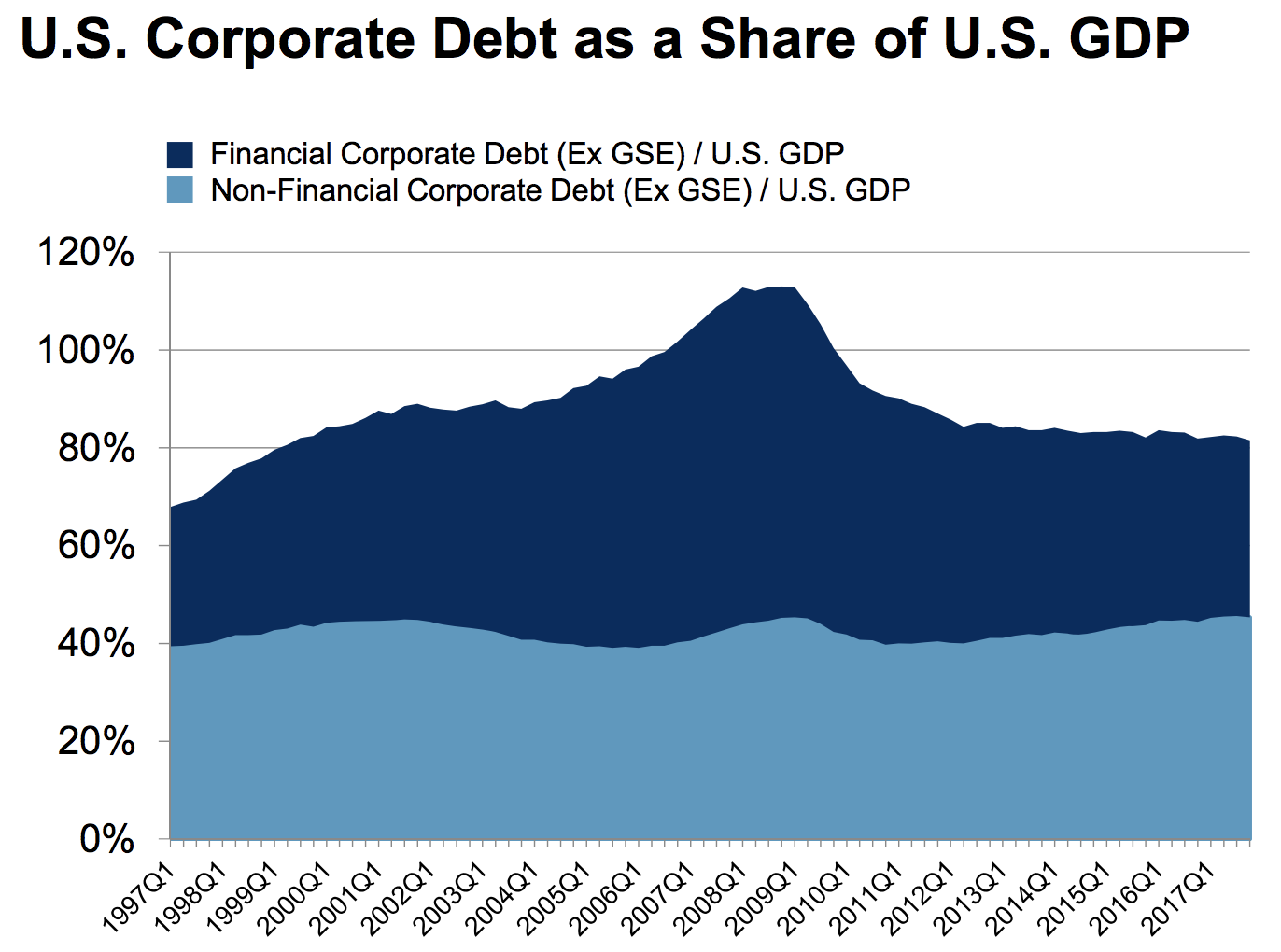

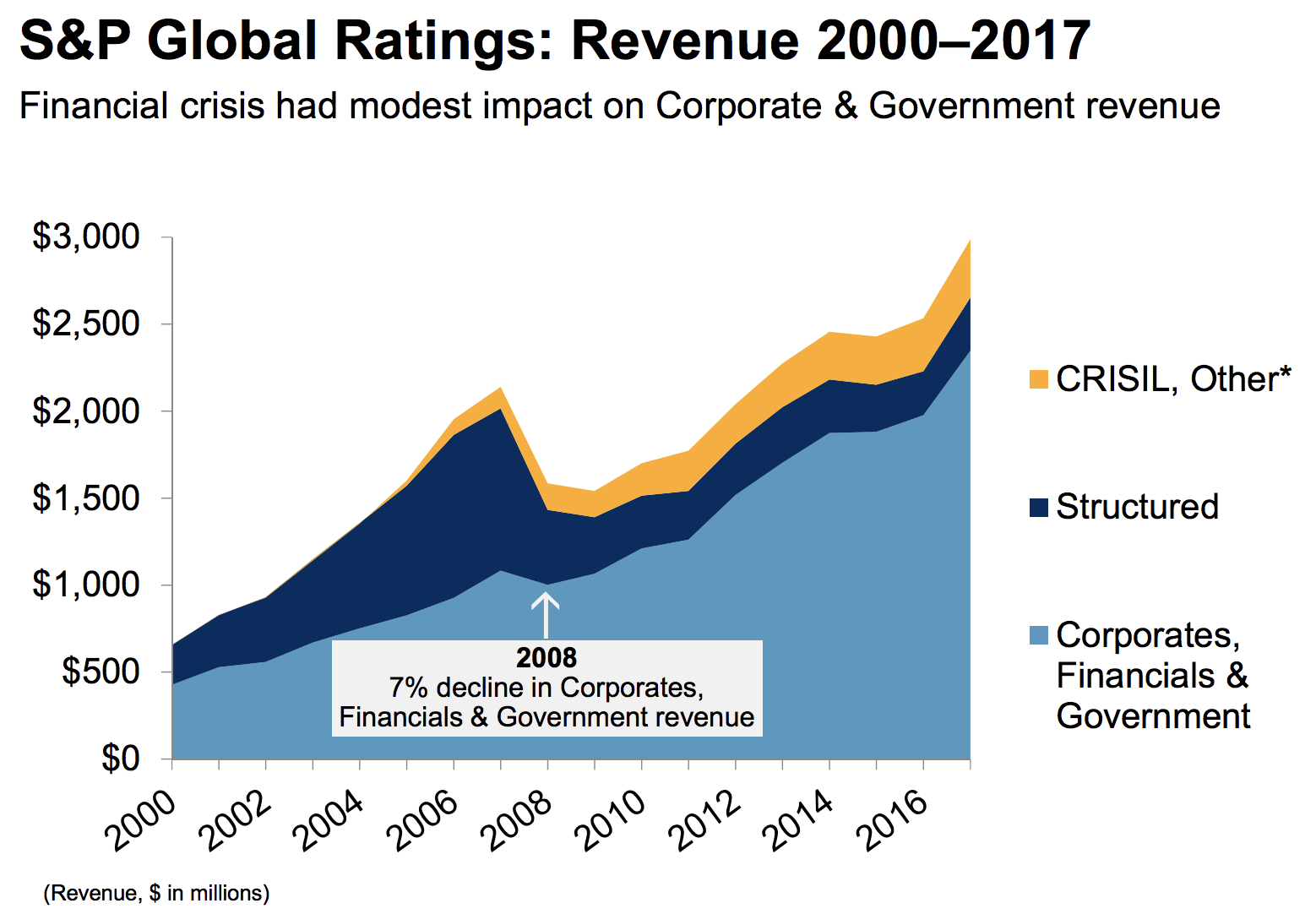

However, as you can see in the chart below, in the event of a financial crisis where debt markets are disrupted, S&P can see drastic swings in its top line. Despite its highly recurring revenue stream, the company is sensitive to the health of financial markets.

Source: S&P Global Investor Presentation

Speaking of financial crises, this also represents another key risk, but for slightly different reasons. Specifically, such an event could force large-scale deleveraging on the part of corporations or even governments.

The world's debt burden has grown to potentially unsustainable levels. At the end of 2017, for example, the Institute of International Finance reports that total global debt/GDP exceeded 300%. Corporate debt levels in many markets are at record levels.

While that has been great for S&P, perhaps one of the bigger risks that could occur over the next several years would be a slowdown in the number of bonds issued, which would dent demand for the company’s ratings services.

Low interest rates around the world have resulted in a surge in borrowing by practically every type of company, and this environment is unlikely to prove sustainable. If less debt is issued in future years, there will be fewer securities for S&P to rate to make money on.

Volatile financial markets are also less favorable environments for companies to issue debt in, and financial clients such as investment banks and asset managers have less money to spend when M&A deal volumes fall, trading volumes drop, and assets under management decline in value. These are all bad things for S&P's business in the short term, although they arguably have little impact on the company’s long-term earnings power.

Additionally, it’s worth mentioning that longer term, the greater availability and affordability of data is likely to remain a theme. Information is becoming cheaper and easier to access every day. Depending on how this plays out, it could begin to erode some of S&P’s competitive advantages, although for now it seems extremely unlikely that its customers would have a trusted, deep enough alternative to consider.

Finally, be aware that S&P faces some regulatory risk. Since the financial crisis the U.S. Congress, the International Organization of Securities Commissions, the SEC, the European Commission, and the European Securities Market Authority have all been giving closer scrutiny to S&P's ratings. In the future the company might face stricter oversight and even higher compliance costs that could dent its margins or at least slow their growth rate.

Closing Thoughts on S&P Global

S&P Global enjoys one of the widest moats of any company in the world thanks to its strong reputation, proprietary data, and the industry's regulatory burdens that limit competition.

The company's cash-rich business model, when combined with high amounts of recurring revenue and a shareholder-friendly dividend policy, indicate that investors can likely look forward to many more years of strong payout growth.

S&P Global's low yield doesn't make it a great fit for some portfolios, but it is an appealing dividend aristocrat for investors seeking a company that offers potential for strong long-term dividend growth and capital appreciation.