T. Rowe's Dividend Looks Safe Despite Performance Headwinds

Shares of T. Rowe Price have slumped nearly 50% since late 2021, sending the stock's dividend yield to levels not seen since the depths of the pandemic and the 2007-09 financial crisis.

As one of the world's largest money managers, T. Rowe generates most of its revenue from investment advisory fees charged for managing clients' portfolios. Fees are typically assessed as a percentage of assets under management (AUM).

With stocks off to a rough start in 2022, T. Rowe's AUM has slumped 16% year-to-date. But based on how poorly the stock has traded, investors seem braced for more bad news ahead.

We believe the culprit is T. Rowe's heavier exposure to growth-oriented equity strategies.

After reviewing T. Rowe's roughly 50 equity mutual funds (31% of AUM), we estimate about half of their AUM resides in growth-focused funds.

Assuming a similar proportion of growth stocks are held in T. Rowe's separately managed equity strategies (24% of AUM) and blended asset products (30%), we would not be surprised if at least 25% to 33% of the firm's overall AUM was invested in growth stocks.

Rising interest rates and fading pandemic tailwinds have caused growth stock valuations to rapidly come back to earth this year, causing more of T. Rowe's strategies to struggle than usual.

For example, two of the firm's largest mutual funds, the Blue Chip Growth Fund (5% of AUM) and the Growth Stock Fund (4%), have lost over 30% in 2022, significantly trailing the S&P 500 as well as the tech-heavy Nasdaq.

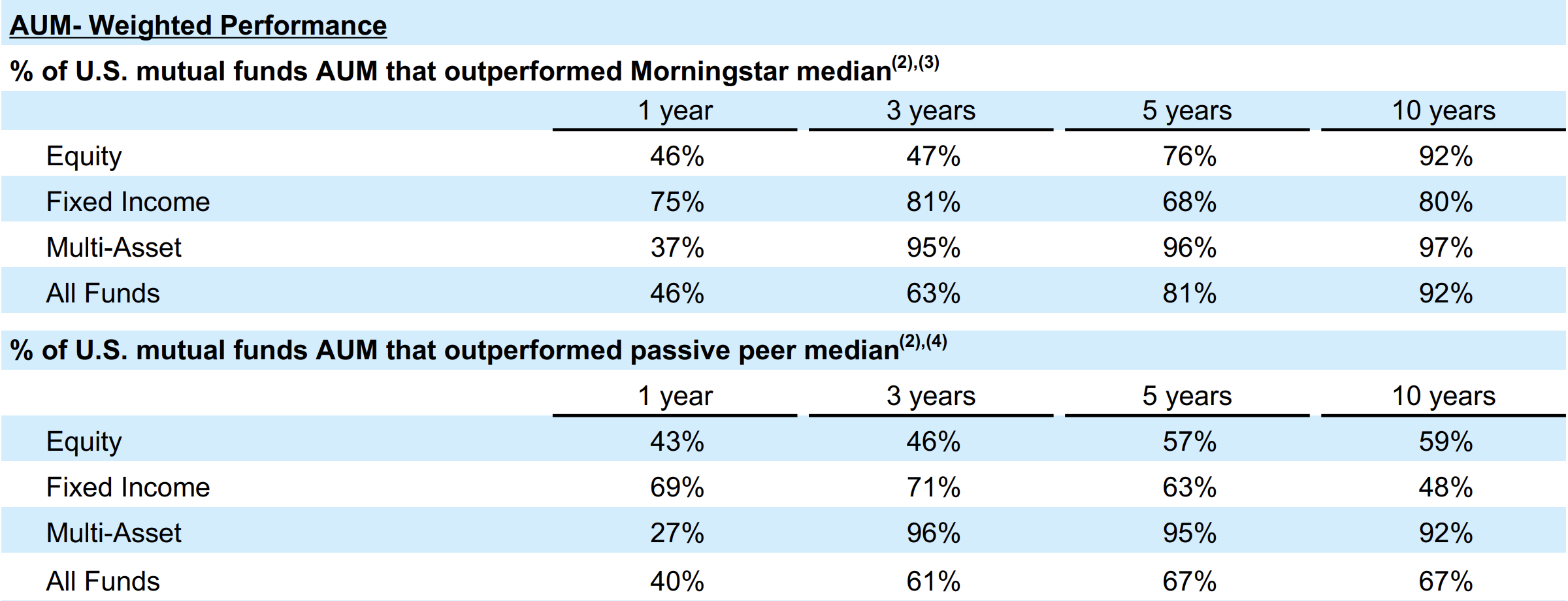

On an AUM-weighted basis, less than half of T. Rowe's funds have outperformed their Morningstar peers in recent years, with an even lower share beating their passive rivals.

Source: T. Rowe Price Press Release

Investors in some of T. Rowe's equity strategies may increasingly head for the exits as they rebalance their portfolios, rotate towards value stocks, or opt for cheaper passive funds.

In 2021, T. Rowe experienced net outflows representing about 2% of AUM. Another 0.3% of assets left in the first quarter of 2022, with outflows concentrated in equity strategies.

Management targets 1% to 3% organic AUM growth over time, but the current market environment and T. Rowe's growth-oriented asset mix may continue to make this objective hard to meet.

That said, T. Rowe's dividend continues to look secure despite these challenges. Even if earnings fell 30% in the year ahead – twice the decline expected by analysts – T. Rowe's payout ratio would still sit at a healthy level below 60%.

The company's balance sheet remains pristine as well, with no debt, $2 billion of cash, and $2.9 billion of investments. For context, T. Rowe's dividend costs about $1.1 billion annually.

A continued slump in equities, particularly growth stocks, could further pressure T. Rowe's stock. But we do not expect it to threaten the firm's track record of increasing its quarterly dividend every year since T. Rowe's IPO in 1986.

Looking beyond recent stock market volatility, T. Rowe and other active managers face an uphill battle to organically grow their businesses as lower-cost passive funds continue taking share and pressuring fees.

However, this does not seem like an existential threat to T. Rowe's $1.4 trillion diversified investment platform.

Active management is needed for capital markets to function efficiently, and in the U.S., passive funds already account for over half of equity investments. Perhaps the point of equilibrium between active and passive strategies is close to being reached.

Either way, T. Rowe has one of the best reputations, distribution networks, and long-term performance track records in the industry. The firm's high mix of stickier retirement-focused assets (over 60% of AUM) provides additional insulation.

While moving the organic growth needle is challenging for a firm of T. Rowe's size, management sees opportunity to expand the company's base of international investors (10% of AUM) and relatively small fixed income business (12%).

The Baltimore-based firm also made an uncharacteristic acquisition in late 2021, buying a hedge fund for several billion dollars to expand into private credit markets. Alternative credit strategies (now 3% of AUM) are in higher demand with institutional investors, providing a new growth vector.

Management emphasized that organic growth remains a key focus for the company. But this deal could suggest that T. Rowe does not see an easy path to solid growth for its core mutual fund retirement business beyond the built-in AUM lift provided by the market's appreciation over time.

Overall, it's hard to argue that T. Rowe's long-term outlook or dividend safety has materially changed despite the slump in its stock price.

With T. Rowe shares trading at a forward P/E ratio near 11 and a dividend yield north of 4%, investors appear to be reasonably discounting the industry's weak organic growth prospects or anticipating more market turbulence ahead.

We expect T. Rowe and its dividend to weather almost any storm. The stock may be worth a closer look for investors who are comfortable with T. Rowe's sensitivity to stock market fluctuations and the murkier long-term growth outlook for active managers.